Embed Size (px)

Citation preview

©The McGraw-Hill Companies, 2005

Advanced Macroeconomics

Chapter 17

MONETARY POLICY AND AGGREGATE DEMAND

©The McGraw-Hill Companies, 2005

THEMES

Keynes, the Classics and the Great Depression

Goods market equilibrium and the determinants of aggregate demand Monetary policy and the formation of interest rates

The relationship between short-term and long-term interest rates

Derivation of the aggregate demand curve

©The McGraw-Hill Companies, 2005

KEYNES VERSUS THE CLASSICS

The classical economic orthodoxy: If only market forces are allowed to work, economic activity will quickly adjust to its natural rate determined by the supply side.

Winston Churchill, British Secretary of the Treasury 1925-1929: ”It isthe orthodox Treasury dogma, steadfastly held, that whatever might bethe political and social advantages, very little employment can, in fact, be created by state borrowing and state expenditure”.The Great Depression of the 1930s undermined the Classical orthodoxyand paved the way for the Keynesian view that aggregate demand playsan important role in the determination of economic activity.

©The McGraw-Hill Companies, 2005

THE GOODS MARKET

Condition for goods market equilibrium

Y C I G (1)

Investment demand

( , , )

0, 0, 0Y r

I I Y r

I I II I I

Y r

(2)

Consumption demand

( , , )

0 1, 0, 0( )

Y T r

C C Y T r

C C CC C C

Y T r

(3)

©The McGraw-Hill Companies, 2005

THE GOODS MARKET Define

Aggregate private demand

D C + I

We assume a

Balanced public budget

T = G

©The McGraw-Hill Companies, 2005

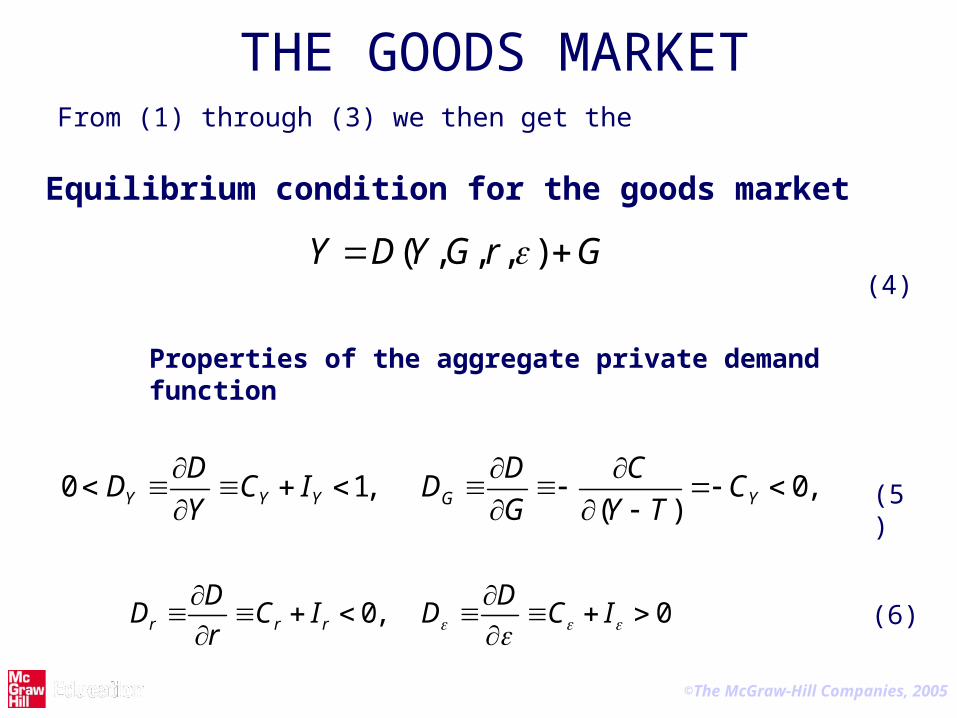

From (1) through (3) we then get the

( , , , )Y D Y G r G

Properties of the aggregate private demand function

0 1, 0,( )Y Y Y G Y

D D CD C I D C

Y G Y T

0, 0r r r

D DD C I D C I

r

(4)

(5)

(6)

THE GOODS MARKET

Equilibrium condition for the goods market

©The McGraw-Hill Companies, 2005

-11

-8

-5

-2

1

4

7

1971 1973 1975 1977 1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999

Percentage of GDP

-7

-5

-3

-1

1

3

5

PercentPrivate sector savings surplus (left axis)

Real interest rate (right axis)

Year

Figure 17.2: The real interest rate and the private sector savings surplus in Denmark, 1971-2000

©The McGraw-Hill Companies, 2005

THE GOODS MARKET

In the chapter text we show that (4) may be log-linearized to give the following Approximation of the goods market equilibrium condition

1 2 1 2( ) ( ) , 0, 0y y g g r r v (11)

1 2

1ln , ln , ln , ln ,

1

(1 ) , , ln ln

Y

rY

y Y y Y g G g G mD

DDGm C m v m

Y Y Y

Note that the equilibrium real interest rate is determined by the condition for

Long run equilibrium in the goods market ( , , , )Y D Y G r G (13)

We now wish to transform (11) into a relationship between y og . For that purpose we must study

©The McGraw-Hill Companies, 2005

THE MONEY MARKET The equilibrium condition for the money market

( , ), 0, 0Y i

M L LL Y i L L

P Y i

(14)

The money demand function

( , ) , 0, 0, 0 iL Y i kY e k (15)

Note: i is the short-term interest rate which is controlled by the central bank.

©The McGraw-Hill Companies, 2005

THE MONEY MARKET

Constant money growth rule (Friedman)

lnM - lnM-1 =

Motivation for the CMG rule: If is close to 1 and is close to zero, equations(14) and (15) roughly imply that

M = kPY

A constant rate of growth of M will then ensure a stable growth in aggregate money income PY.

©The McGraw-Hill Companies, 2005

Interest rate policy under the CMG rule

Money market equilibrium under the CMG rule

1

1

(1 )

(1 )iM

kY eP

(16)Assume that we have

Long run equilibrium in the previous period ( )1

1

* rML kY e

P

(17)

Taking logarithms in (16) and (17) and using the approximationsln(1+) and ln(1+) , we get

ln * lnL k y i

ln * ln ( )L k y r (18)

(19)

Substitution of (18) into (19) yields

Monetary policy under the CMG rule

1( ) ( )i r y y

(20)

©The McGraw-Hill Companies, 2005

INTEREST RATE POLICY UNDER THE TAYLOR RULE

Note that may be interpreted as the central bank’s target inflation rate. Problem with the CMG rule: A stable growth in total money income

cannot beachieved if the parameters and change in an unpredictable way (for example through financial innovations).

As an alternative to the CMG rule John Taylor proposed the

Taylor rule

( *) ( ), 0, 0i r h b y y h b (21)

Note: It is important for economic stability that the parameter h is positive so that an increase in inflation triggers an increase in the real interest rate.

Taylor’s proposal for USA

h = 0.5 b = 0.5

©The McGraw-Hill Companies, 2005

Estimated interest rate reaction functions of four

central banks

h b Estimation period

German Bundesbank1 0.31 0.25 1979:3 - 1993:12 (monthly data)

Bank of Japan1 1.04 0.08 1979:4 - 1994:12 (monthly data)

U.S. Federal Reserve Bank1 0.83 0.56 1982:10 - 1994:12 (monthly data)

European Central Bank20.74 0.82 1999:1 - 2003:1 (quarterly data)

Estimate of

©The McGraw-Hill Companies, 2005

Three-month interest rate and the estimated Taylor rate in the euro

area

©The McGraw-Hill Companies, 2005

FROM THE SHORT RATE TO THE LONG RATE

The problem: the central bank may control the short-term interest rate, but aggregate demand mainly depends on the long-term interest rate.Assumption: Short-term and long-term bonds are perfect substitutes This implies the Arbitrage condition

1 2 1(1 ) (1 ) (1 ) (1 ) ........ (1 )l n e e et t t t t ni i i i i (24)

Taking logs on both sides of (24) and using the approximation ln(1+i) i, we get

The expectations theory of the term structure of interest rates 1 2 1

1( ...... )l e e e

t t t t t ni i i i in (25)

Implication: The current long rate is a simple average of the current short rate and the expected future short rates.

©The McGraw-Hill Companies, 2005

FROM THE SHORT RATE TO THE LONG RATE

Further implications of (25):

Monetary policy can only have a significant impact on long-term interest rates by influencing the expected future short-term interest rates A change in the current short-term rate which is expected to be temporary will only have a very limited impact on the long-term interest rate When the market expects a future tightening of monetary policy, the yield curve is rising

If the market expects a future relaxation of monetary policy, the yield curveis falling The yield curve is flat when market participants have

Static interest rate expectations

iff for all 1, 2,..., 1l et t t j ti i i i j n (26)

©The McGraw-Hill Companies, 2005

0

2

4

6

8

10

12

14

August 1st, 1996

August 2nd, 1993

January 2nd, 2000

Term to maturity (logarithms)

Effective yield (percent)

14 days 1 month 3 months 6 months 2 years1 year 5 years 10 years 30 years

The term structure of interest rates in Denmark

©The McGraw-Hill Companies, 2005

1

2

3

4

5

6

7

Percent p.a.

Jan. Feb. Mar. Apr. May. Jun. Jul. Aug. Sep. Oct. Nov. Dec. Jan. Feb.

10-year government bond yield

Federal funds target rate

The decoupling of short-term and long-term interest rates in the United States, 2001-2002

©The McGraw-Hill Companies, 2005

0

2

4

6

8

10

12

14

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

10-year government bond yield 'Signaling' interest rate of the central bank

Percent

The ’signalling’ interest rate of the central bank and the 10-year government bond yield in Denmark

©The McGraw-Hill Companies, 2005

DERIVING THE AGGREGATE DEMAND CURVE

The ex post real interest rate

11

11

1a air r i

(27)

Investment and consumption are governed by

The ex ante real interest rate

11

11

1e

e

ir r i

(28)

We assume Static expectations

1e (29)

Equations (28) and (29) imply

r i (30)

©The McGraw-Hill Companies, 2005

DERIVING THE AGGREGATE DEMAND CURVE

Recall that

1 2 1 2( ) ( ) , 0, 0y y g g r r v (11)

( *) ( ), 0, 0i r h b y y h b (21)

Inserting (21) and (30) into (11), we get

The aggregate demand curve

1 2( ) [ ( *) ( )]

( * )

r r

y y g g h b y y v

y y z

(32)

2 1

2 2

( )0

1 1

h v g gz

b b

(33)

©The McGraw-Hill Companies, 2005

PROPERTIES OF THE AGGREGATE DEMAND CURVE

The AD curve has a negative slope: higher inflation induces the central bank to raise the interest rate, causing aggregate demand to fall The AD curve is flatter, the more weight the central bank attaches to stable inflation compared to output stability (see figure 17.7)The AD curve shifts upwards in case of more optimistic growth expectations in the private sector or in case of a more expansionary fiscal policy

The AD curve shifts downwards if the central bank reduces its inflation target

©The McGraw-Hill Companies, 2005

B

y

AD (h low, b high)

AD (h high, b low)

Figure 17.7: The aggregate demand curve under alternative monetary policy regimes

©The McGraw-Hill Companies, 2005

IMPORTANT CONCEPTS AND RESULTS IN CHAPTER 17

Properties of the investment function

Properties of the consumption function

The relationship between the real interest rate, public consumption,expectations and aggregate demand

Money market equilibrium

The goods market equilibrium condition

©The McGraw-Hill Companies, 2005

IMPORTANT CONCEPTS AND RESULTS IN CHAPTER 17

The constant-money-growth rule and its implications for interest rate policy

The Taylor rule and its implications for interest rate policy

The relationship between the short-term and the long-term interest rate: The expectations hypothesis and the yield curve

The ex ante versus the ex post real interest rate

Poperties of the AD curve, including the importance of monetary policy for the position and the slope of the curve