Embed Size (px)

Citation preview

© NCEL

Prospective Investor@

Pakistan Mercantile Exchange Limited

December 2006

© NCEL

Contents

• Welcome

• Risks in Trading Futures

• Introduction to Futures

• PMEX Highlights

• PMEX Business Model

• How to Trade at PMEX

• Investor Safeguards

• Demo

© NCEL

Risks in Trading Futures

© NCEL

Should You Trade Commodity Futures?

Trading commodity futures is not for everyone. It can be a volatile and risky business. Before you invest any money in futures contracts, you should:

– Consider your financial experience, goals, and financial resources

– Understand commodity futures contracts and your obligations before entering the market

– Be aware that you can lose more than your initial investment

– Only take risk for the amount that you can afford to lose

– Understand your exposure to risk and other aspects of trading by thoroughly reviewing the risk disclosure documents your broker is required to provide you

© NCEL

Can I lose Money Trading Futures?

• Yes, if you are reckless– Lax controls, poor corporate governance, over confidence,

hoping to recover through taking an even bigger position, etc.

• But it is not Rocket Science– Proper Understanding and Respect of Risk can ensure losses

are contained and gains are preserved

© NCEL

Introduction to Derivatives

© NCEL

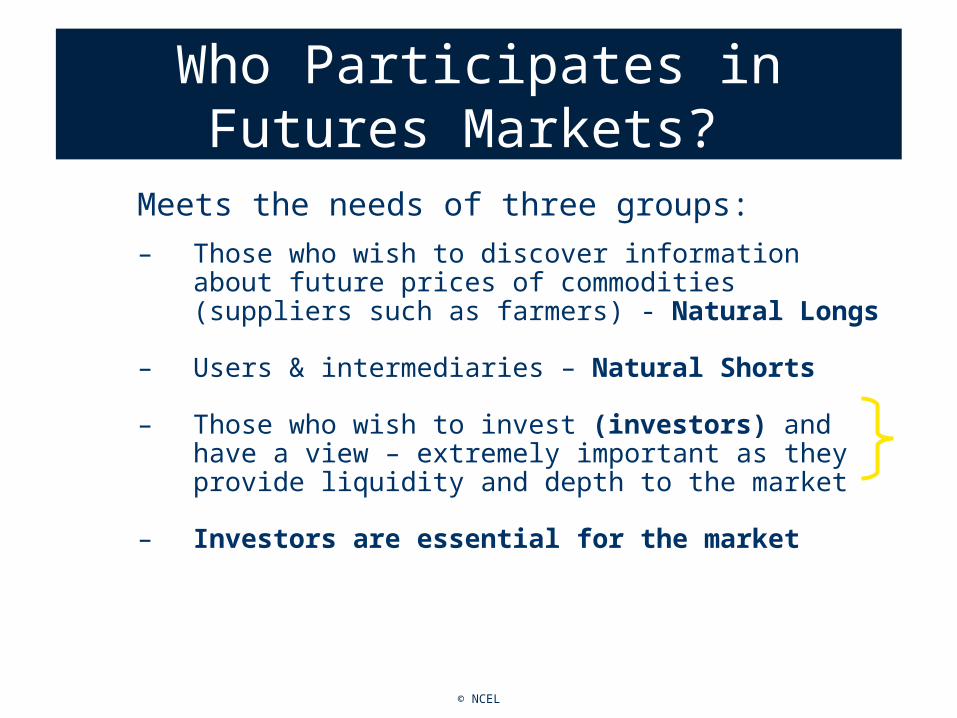

Who Participates in Futures Markets?

Meets the needs of three groups:

– Those who wish to discover information about future prices of commodities (suppliers such as farmers) - Natural Longs

– Users & intermediaries – Natural Shorts

– Those who wish to invest (investors) and have a view – extremely important as they provide liquidity and depth to the market

– Investors are essential for the market

© NCEL

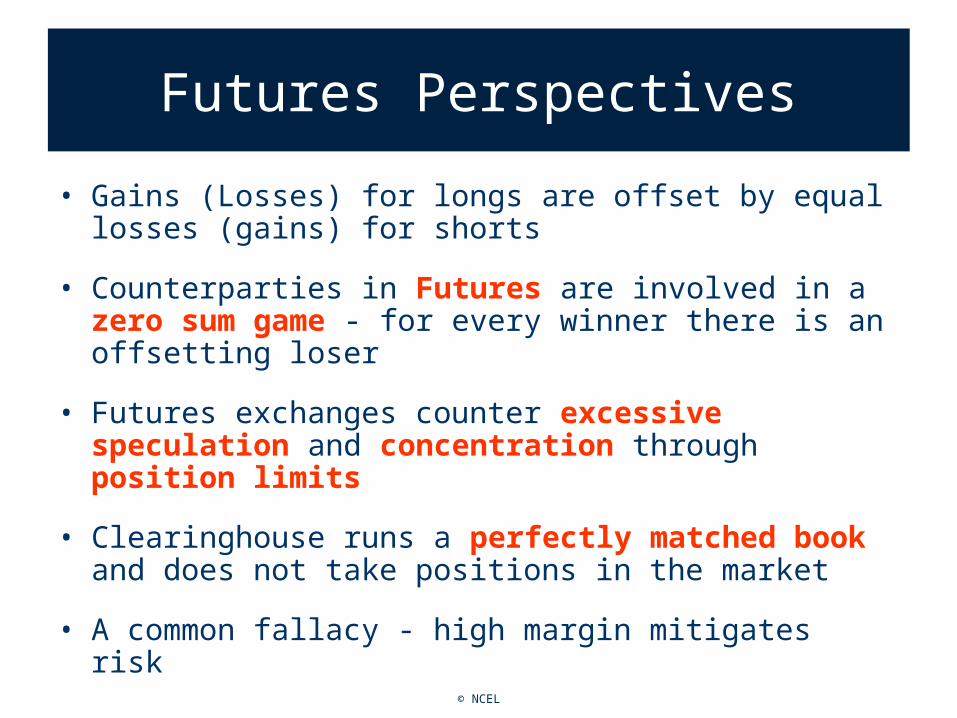

Futures Perspectives

• Gains (Losses) for longs are offset by equal losses (gains) for shorts

• Counterparties in Futures are involved in a zero sum game - for every winner there is an offsetting loser

• Futures exchanges counter excessive speculation and concentration through position limits

• Clearinghouse runs a perfectly matched book and does not take positions in the market

• A common fallacy - high margin mitigates risk

© NCEL

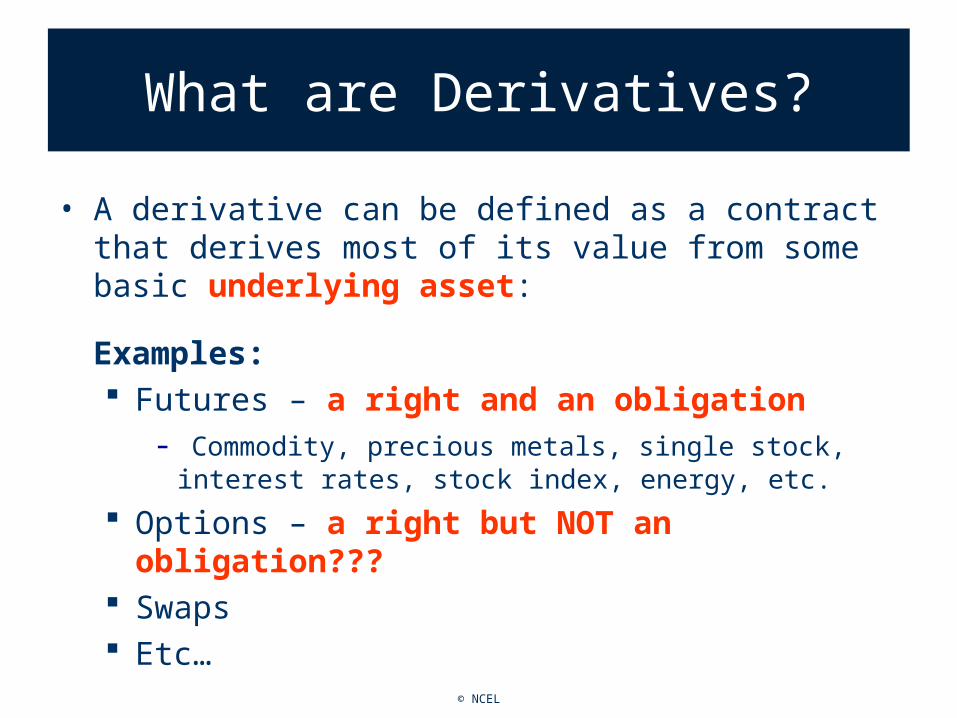

What are Derivatives?

• A derivative can be defined as a contract that derives most of its value from some basic underlying asset:

Examples: Futures – a right and an obligation

- Commodity, precious metals, single stock, interest rates, stock index, energy, etc.

Options – a right but NOT an obligation??? Swaps Etc…

© NCEL

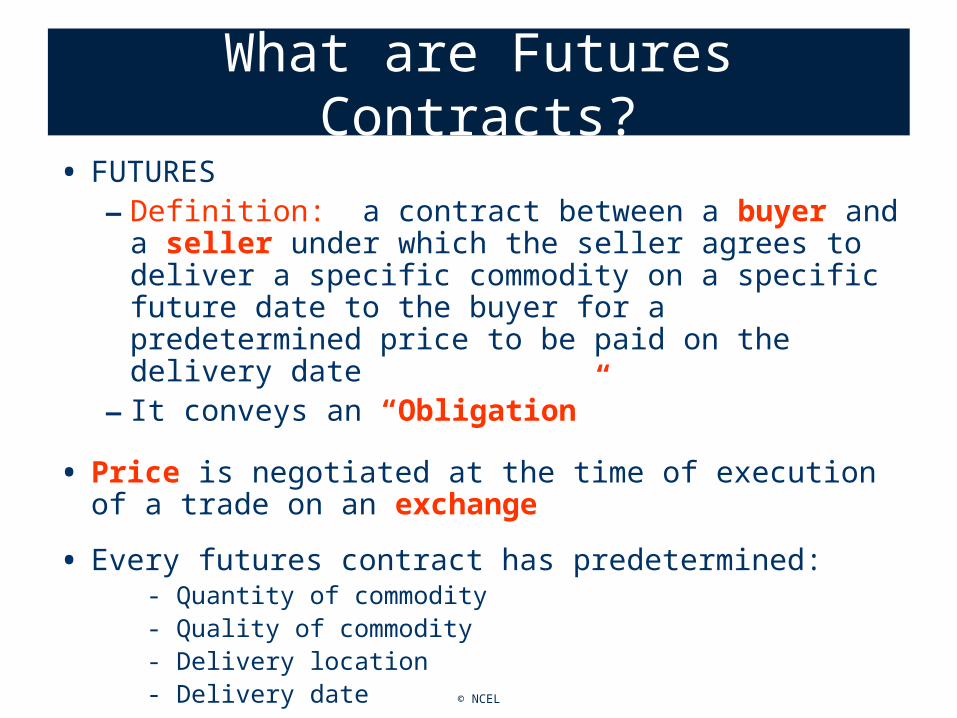

What are Futures Contracts?

• FUTURES– Definition: a contract between a buyer and a seller

under which the seller agrees to deliver a specific commodity on a specific future date to the buyer for a predetermined price to be paid on the delivery date

– It conveys an “Obligation”

• Price is negotiated at the time of execution of a trade on an exchange

• Every futures contract has predetermined:- Quantity of commodity- Quality of commodity- Delivery location- Delivery date

© NCEL

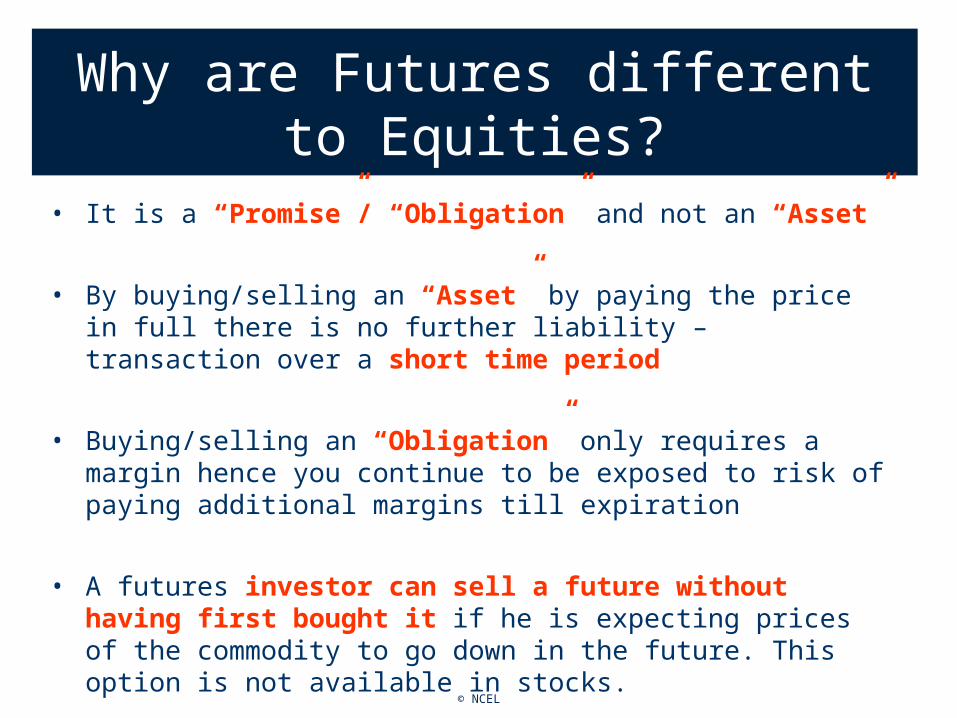

Why are Futures different to Equities?

• It is a “Promise”/ “Obligation” and not an “Asset”

• By buying/selling an “Asset” by paying the price in full there is no further liability – transaction over a short time period

• Buying/selling an “Obligation” only requires a margin hence you continue to be exposed to risk of paying additional margins till expiration

• A futures investor can sell a future without having first bought it if he is expecting prices of the commodity to go down in the future. This option is not available in stocks.

© NCEL

Why are Futures different to Equities?

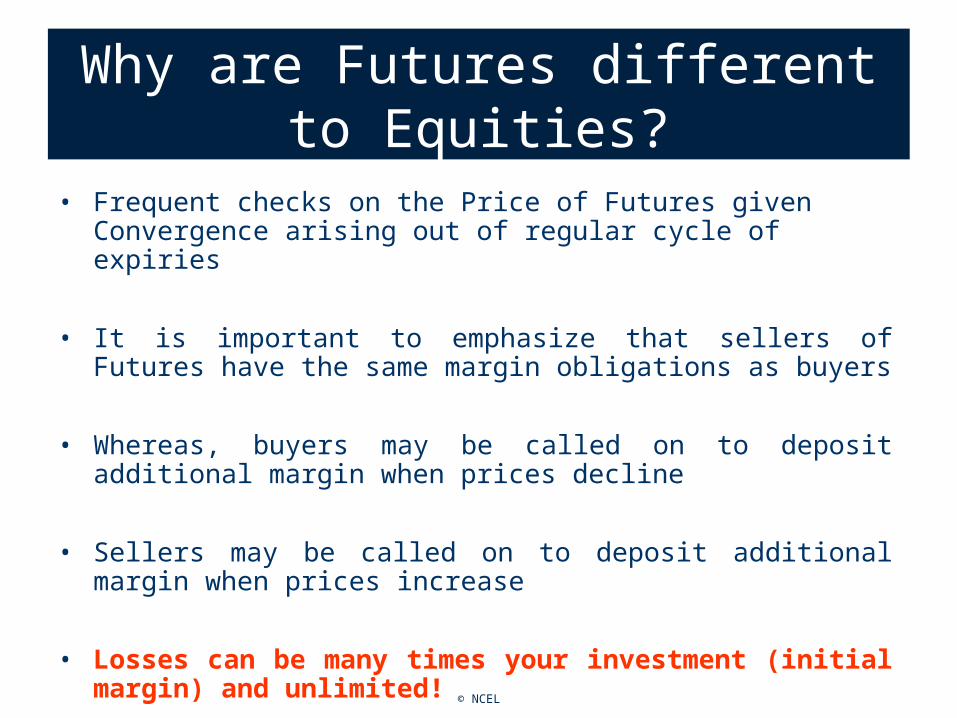

• Frequent checks on the Price of Futures given Convergence arising out of regular cycle of expiries

• It is important to emphasize that sellers of Futures have the same margin obligations as buyers

• Whereas, buyers may be called on to deposit additional margin when prices decline

• Sellers may be called on to deposit additional margin when prices increase

• Losses can be many times your investment (initial margin) and unlimited!

© NCEL

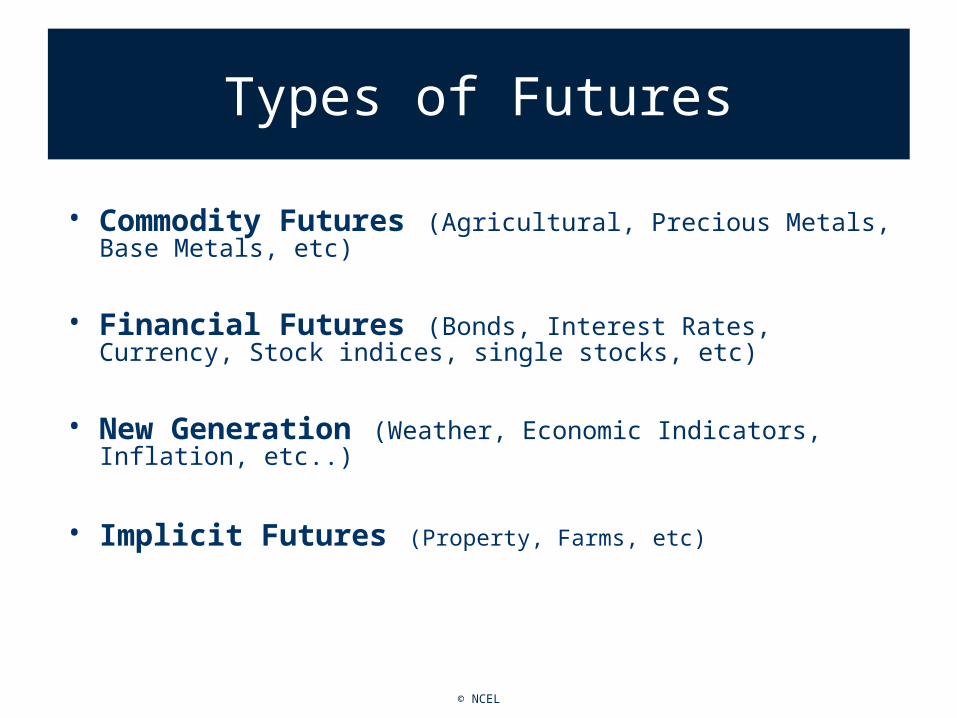

Types of Futures

• Commodity Futures (Agricultural, Precious Metals, Base Metals, etc)

• Financial Futures (Bonds, Interest Rates, Currency, Stock indices, single stocks, etc)

• New Generation (Weather, Economic Indicators, Inflation, etc..)

• Implicit Futures (Property, Farms, etc)

© NCEL

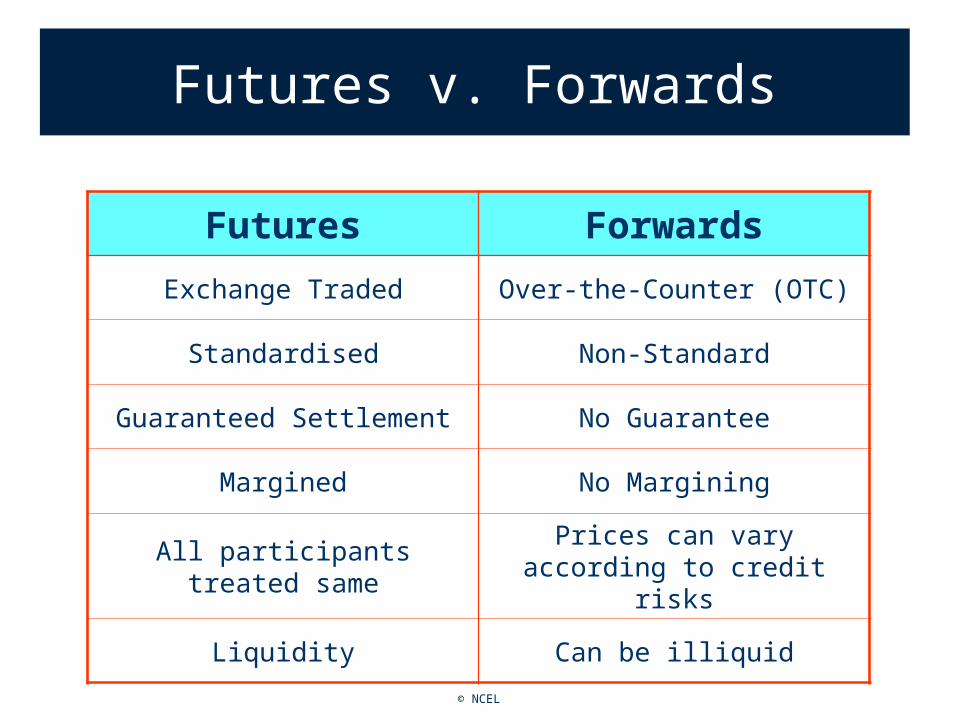

Futures v. Forwards

Futures Forwards

Exchange Traded Over-the-Counter (OTC)

Standardised Non-Standard

Guaranteed Settlement No Guarantee

Margined No Margining

All participants treated samePrices can vary according to

credit risks

Liquidity Can be illiquid

© NCEL

History

• Implied Futures have been traded historically

• Japanese Rice Futures – 17th Century

• Chicago first example of modern futures exchange – Mid 19th Century

• Commodity Futures - first products

• Commodity Exchanges trade contracts on commodities and not commodities themselves

© NCEL

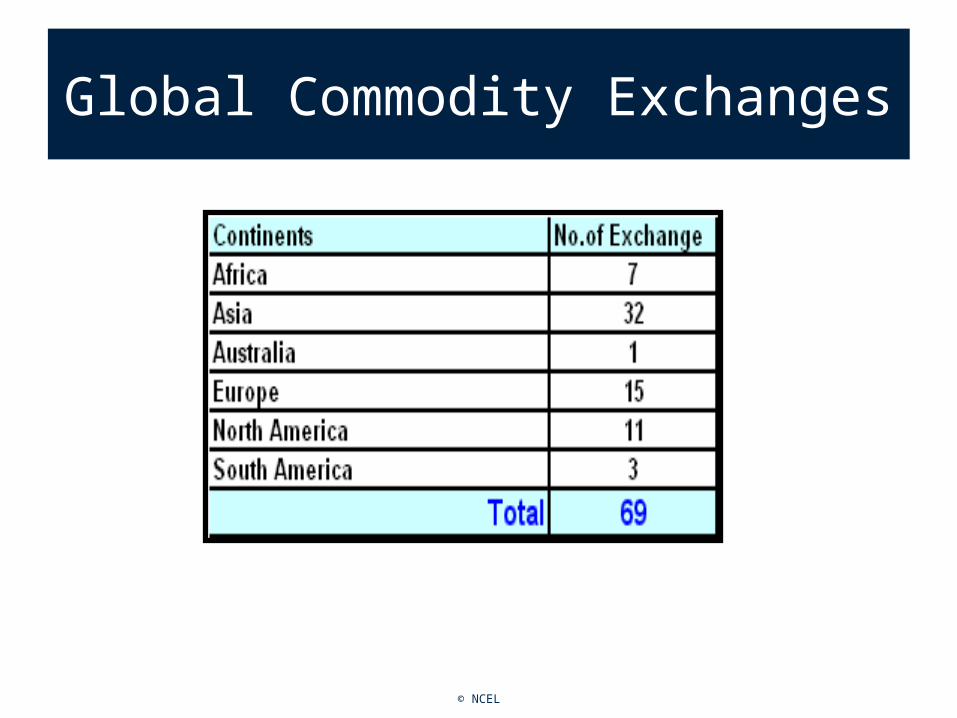

Global Commodity Exchanges

© NCEL

PMEX

© NCEL

Highlights

• Demutualised, all-electronic commodity futures exchange

• Provide secure “Client Level” online access via the Internet with a unique id for each and every Client

• Broker/Client & Client/Client segregation of funds

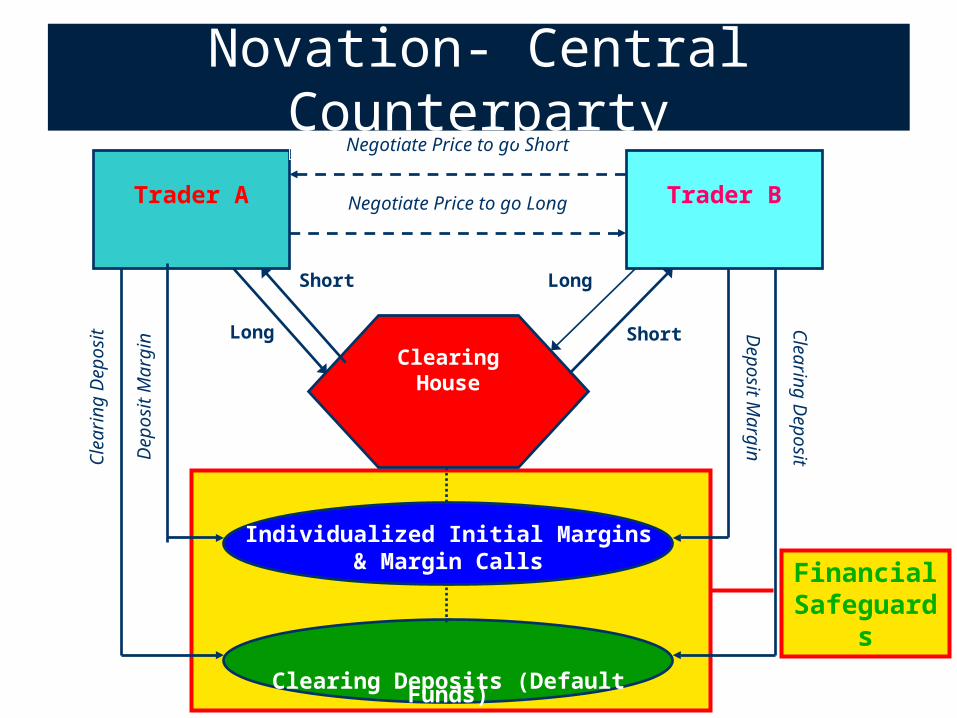

• NCEL Clearing House will provide complete “Novation” – act as the Central Counterparty

• Settlement Guarantee Fund to provide complete protection for all open positions

• Investor Protection Fund to cover losses in case of closed positions and idle balances with Brokers

• Daily Marking-to-market of Open positions and collection of variation margin on T+0 basis, electronically

• Use of analytics for De-Risking NCEL and new product development

© NCEL

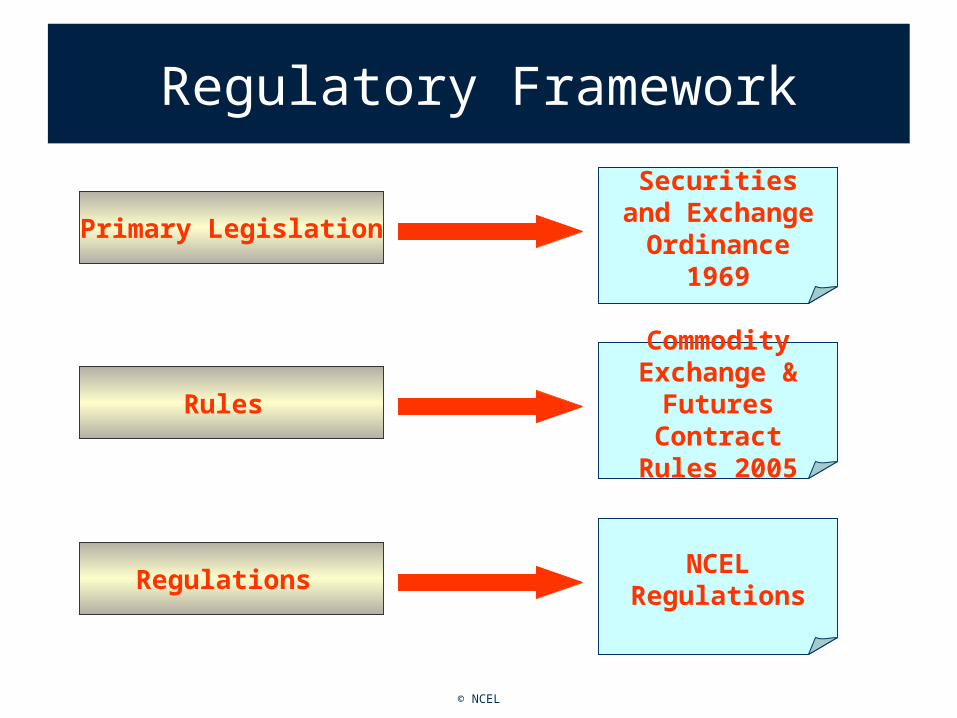

Regulatory Framework

Primary LegislationSecurities and

Exchange Ordinance 1969

Rules

Commodity Exchange &

Futures Contract Rules 2005

NCEL Regulations

Regulations

© NCEL

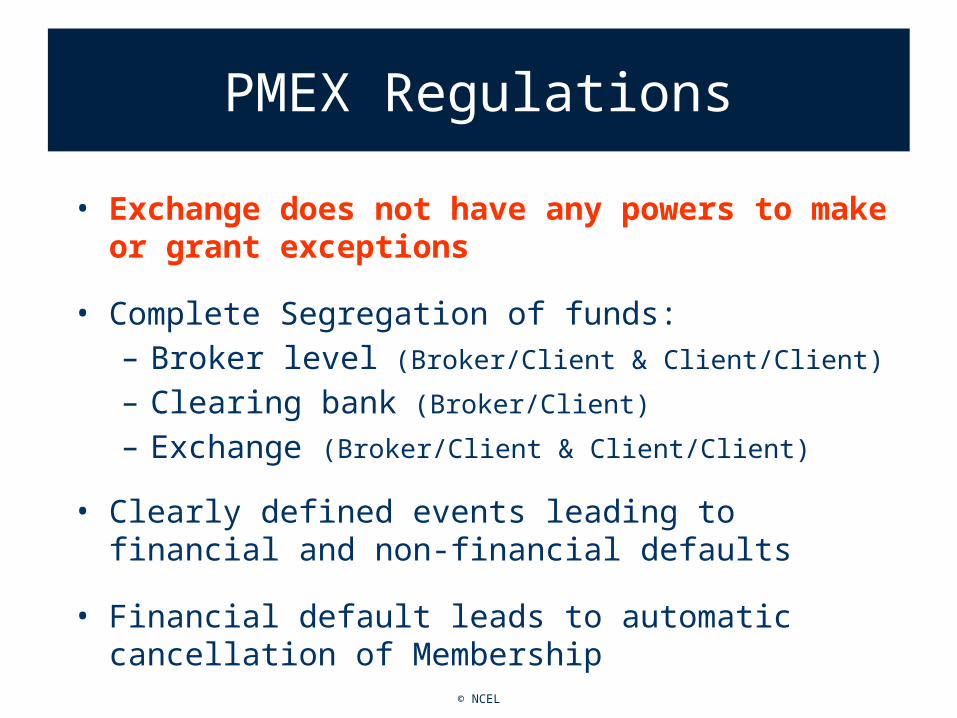

PMEX Regulations

• Exchange does not have any powers to make or grant exceptions

• Complete Segregation of funds:– Broker level (Broker/Client & Client/Client)

– Clearing bank (Broker/Client)

– Exchange (Broker/Client & Client/Client)

• Clearly defined events leading to financial and non-financial defaults

• Financial default leads to automatic cancellation of Membership

© NCEL

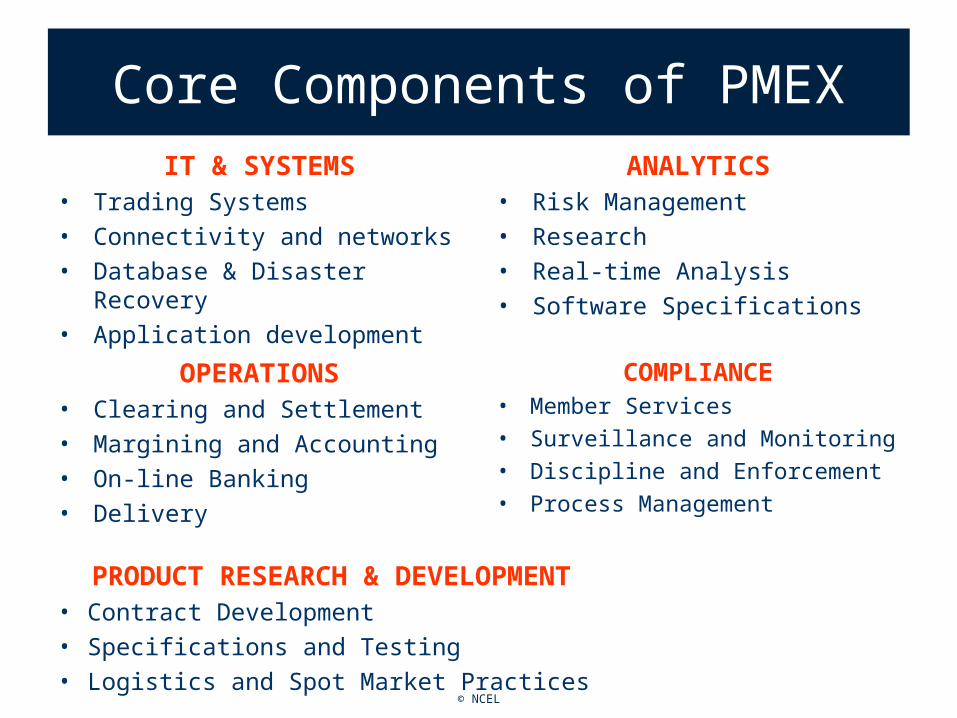

Core Components of PMEXIT & SYSTEMS

• Trading Systems

• Connectivity and networks

• Database & Disaster Recovery

• Application development

ANALYTICS• Risk Management

• Research

• Real-time Analysis

• Software Specifications

OPERATIONS• Clearing and Settlement

• Margining and Accounting

• On-line Banking

• Delivery

COMPLIANCE• Member Services

• Surveillance and Monitoring

• Discipline and Enforcement

• Process Management

PRODUCT RESEARCH & DEVELOPMENT• Contract Development

• Specifications and Testing

• Logistics and Spot Market Practices

© NCEL

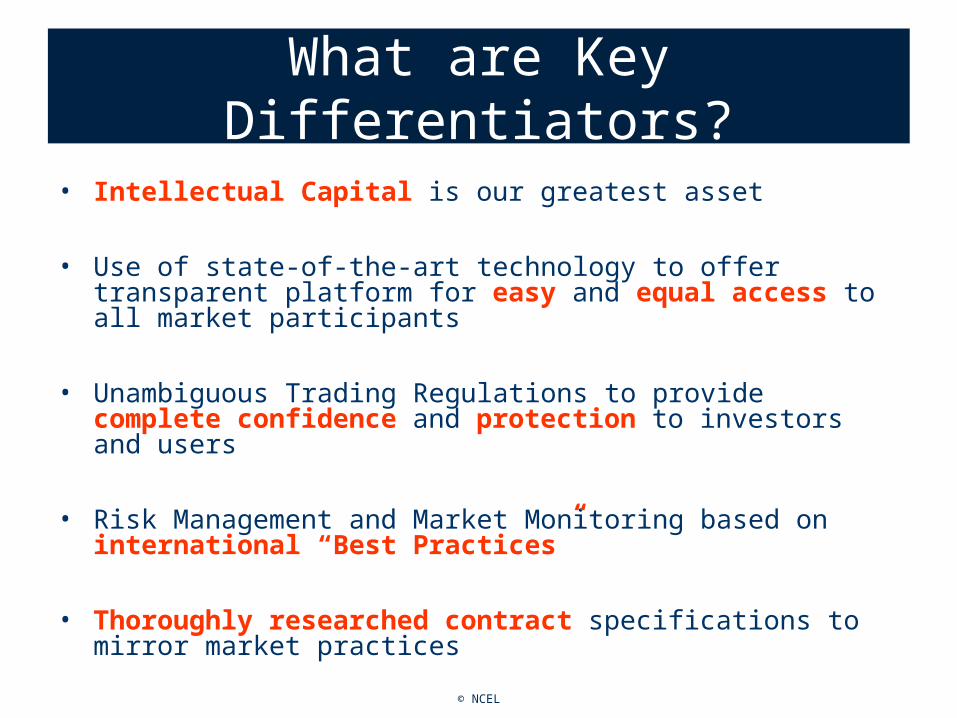

What are Key Differentiators?

• Intellectual Capital is our greatest asset

• Use of state-of-the-art technology to offer transparent platform for easy and equal access to all market participants

• Unambiguous Trading Regulations to provide complete confidence and protection to investors and users

• Risk Management and Market Monitoring based on international “Best Practices”

• Thoroughly researched contract specifications to mirror market practices

© NCEL

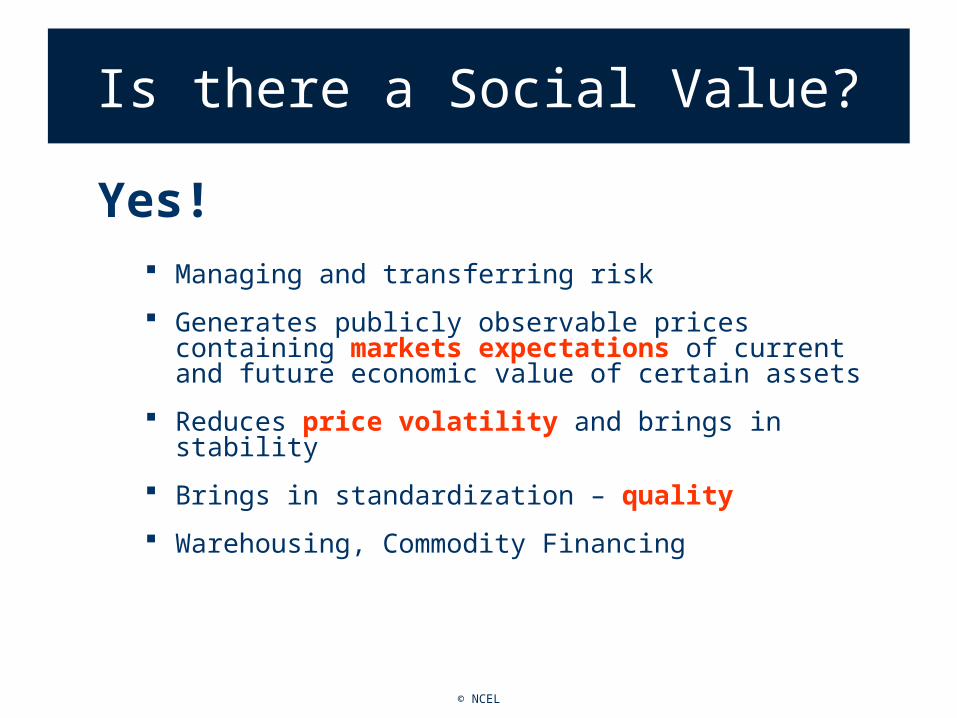

Is there a Social Value?

Yes! Managing and transferring risk

Generates publicly observable prices containing markets expectations of current and future economic value of certain assets

Reduces price volatility and brings in stability

Brings in standardization – quality

Warehousing, Commodity Financing

© NCEL

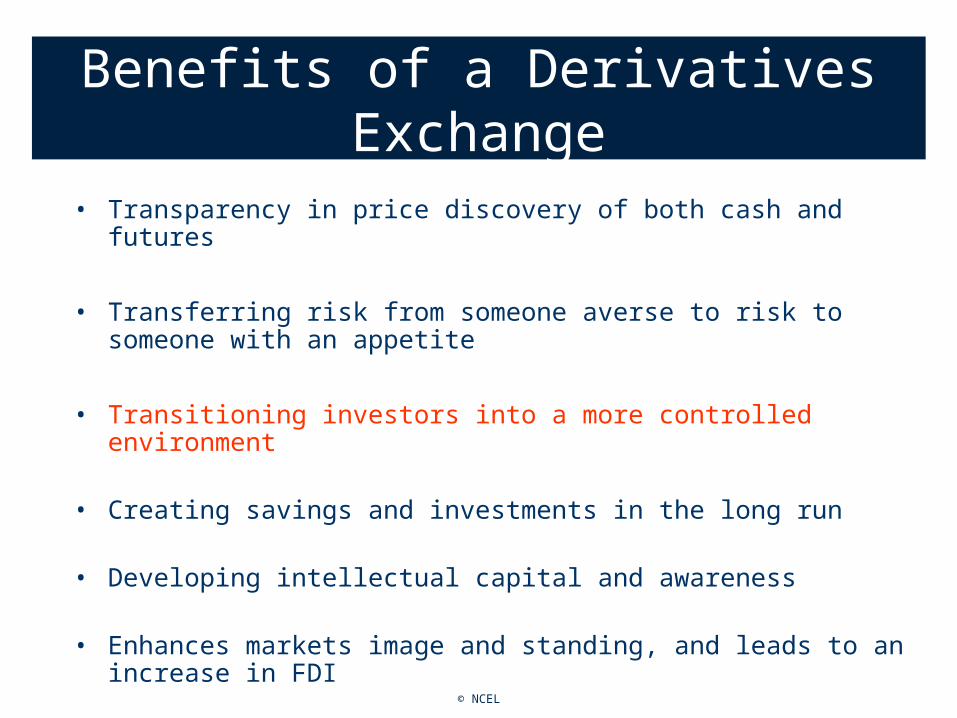

Benefits of a Derivatives Exchange

• Transparency in price discovery of both cash and futures

• Transferring risk from someone averse to risk to someone with an appetite

• Transitioning investors into a more controlled environment

• Creating savings and investments in the long run

• Developing intellectual capital and awareness

• Enhances markets image and standing, and leads to an increase in FDI

© NCEL

Trader A

Negotiate Price to go Short

Negotiate Price to go Long

Long

Short Long

ShortClearing House

Individualized Initial Margins & Margin Calls

Clearing Deposits (Default Funds)

Trader B

Deposi

t M

arg

in

Deposit M

arg

in

Cle

ari

ng D

ep

osi

t Cle

arin

g D

ep

osit

Financial Safeguar

ds

Novation- Central Counterparty

© NCEL

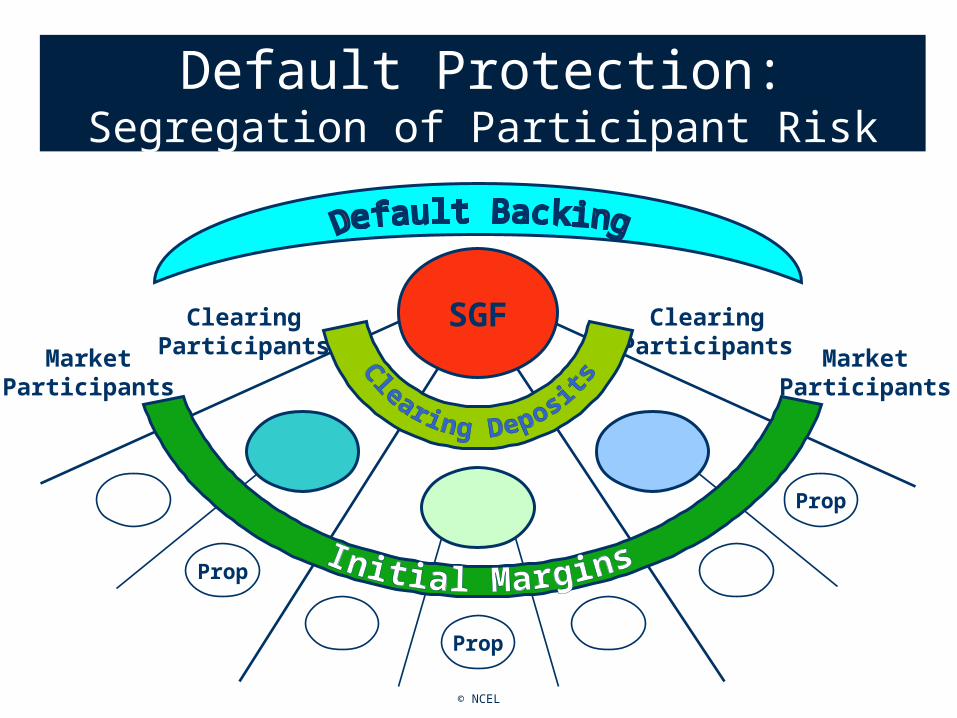

Default Protection: Segregation of Participant Risk

ClearingParticipants

ClearingParticipantsMarket

ParticipantsMarket

Participants

Prop

Prop

Prop

SGF

© NCEL

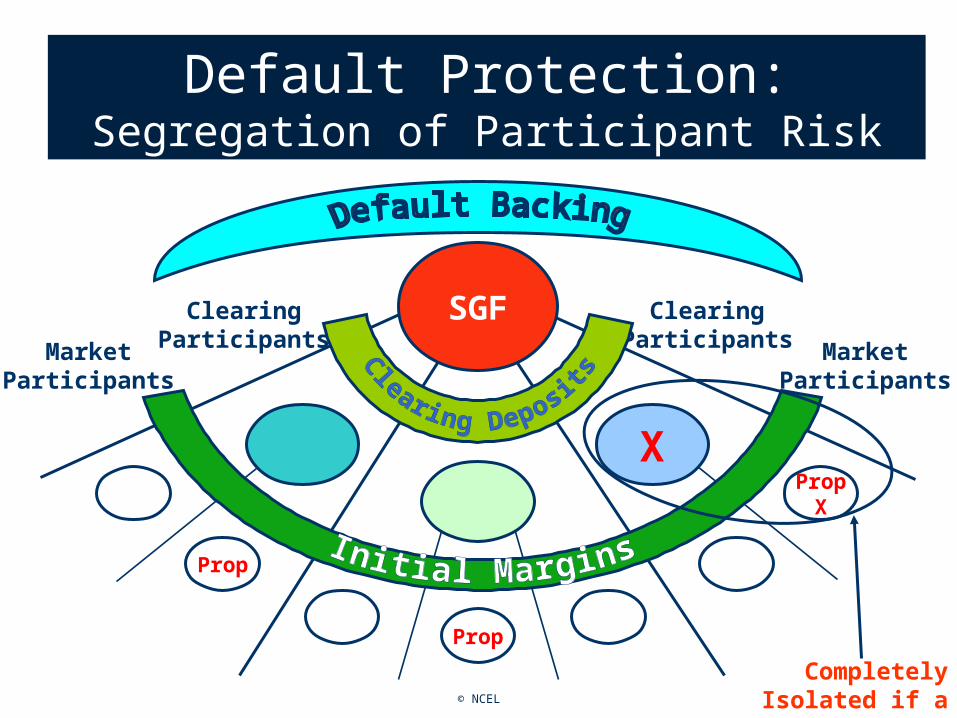

Default Protection: Segregation of Participant Risk

ClearingParticipants

ClearingParticipantsMarket

ParticipantsMarket

Participants

X

Prop

Prop

PropX

SGF

Completely Isolated if a default takes place

© NCEL

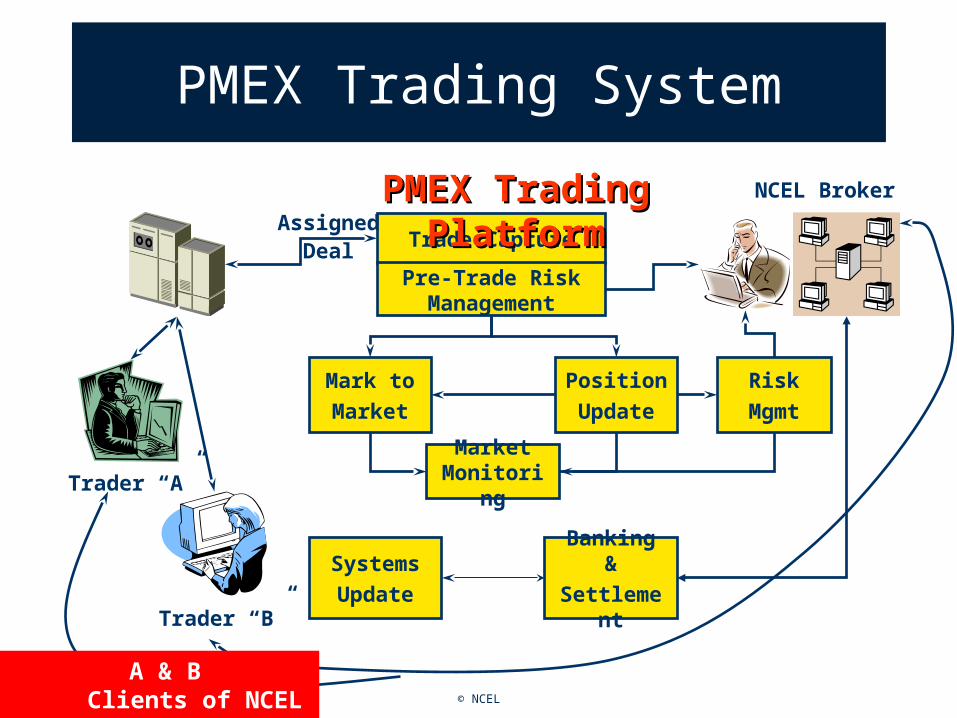

PMEX Trading System

Trade Capture

Pre-Trade Risk Management

Mark toMarket

PositionUpdate

Market Monitori

ng

RiskMgmt

Banking &

Settlement

SystemsUpdate

PMEX Trading PMEX Trading PlatformPlatform

NCEL Broker

Trader “A”

Trader “B”

AssignedDeal

A & B Clients of NCEL Broker

© NCEL

Contract Choice and Design

• Four out of Five new futures contracts fail and are de-listed within the first three years of trading

• Two possible reasons:– Lack of demand for the contract itself– Poor contract design

• Of course these two reasons are related to one another

© NCEL

How do you Design a Contract?

• Research is critical to the success of a contract

• Interaction with market participants

• Simplicity

• Designed for industry to mirror industry practice

• Minimal entry/exit costs

• Ensure Price Convergence through credible threat of

delivery

• Tracking of Basis - Responsibility of Market Oversight

Dept.

© NCEL

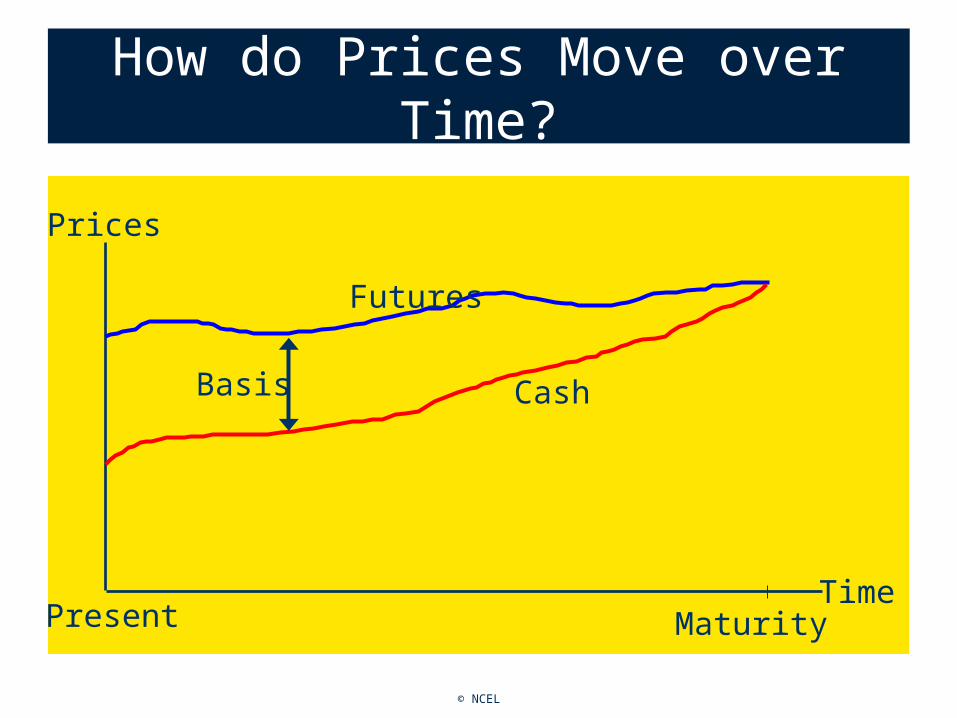

How do Prices Move over Time?

Basis

Prices

Present MaturityTime

Cash

Futures

© NCEL

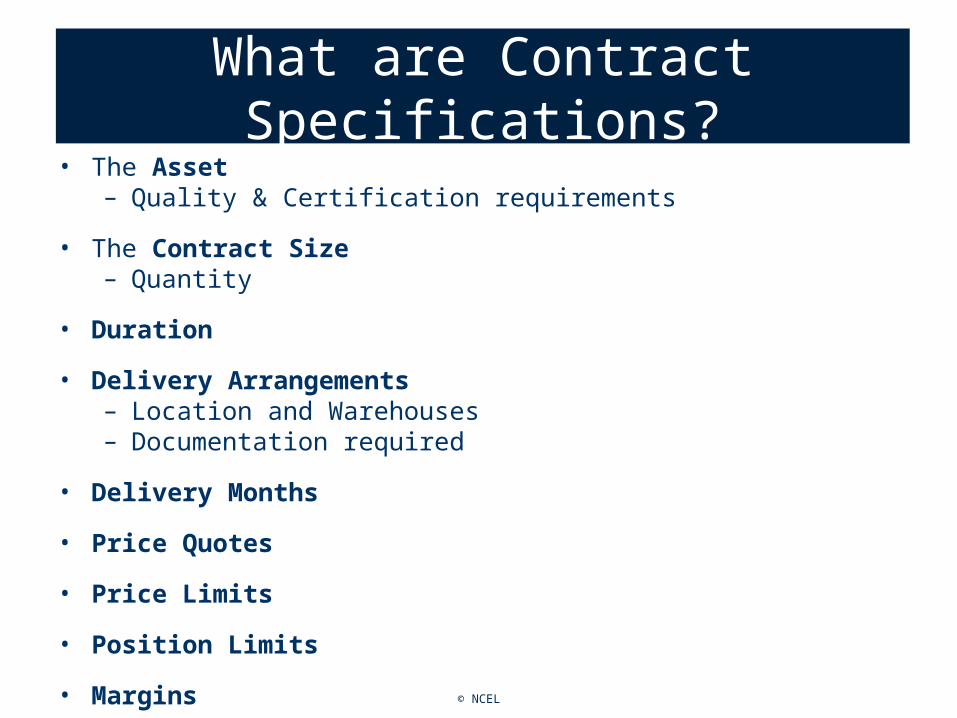

What are Contract Specifications?• The Asset

– Quality & Certification requirements

• The Contract Size– Quantity

• Duration

• Delivery Arrangements– Location and Warehouses– Documentation required

• Delivery Months

• Price Quotes

• Price Limits

• Position Limits

• Margins

© NCEL

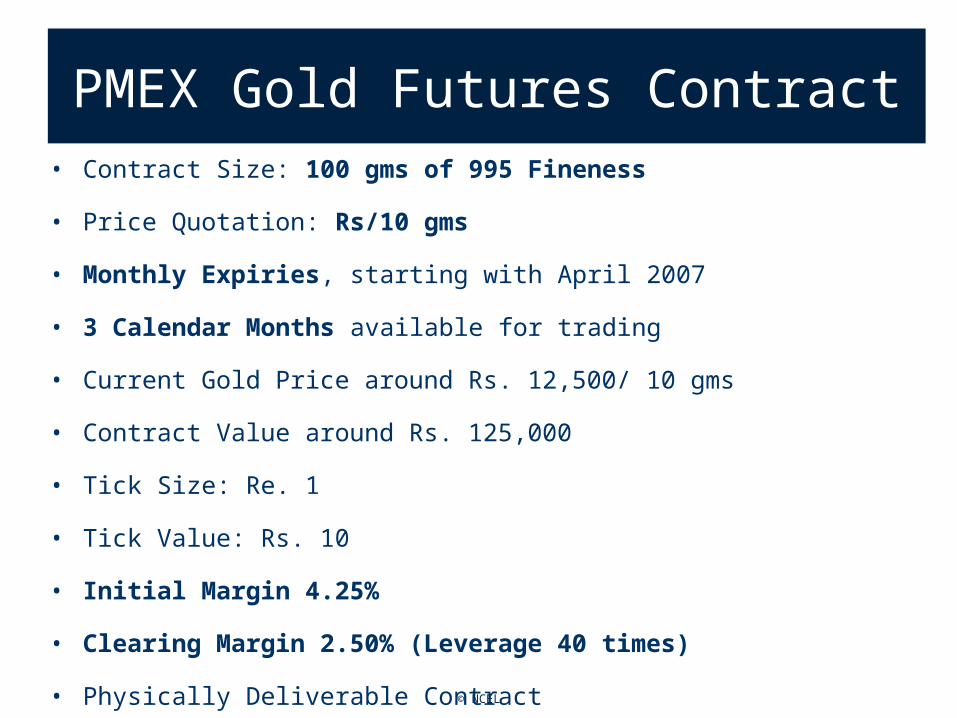

PMEX Gold Futures Contract• Contract Size: 100 gms of 995 Fineness

• Price Quotation: Rs/10 gms

• Monthly Expiries, starting with April 2007

• 3 Calendar Months available for trading

• Current Gold Price around Rs. 12,500/ 10 gms

• Contract Value around Rs. 125,000

• Tick Size: Re. 1

• Tick Value: Rs. 10

• Initial Margin 4.25%

• Clearing Margin 2.50% (Leverage 40 times)

• Physically Deliverable Contract

© NCEL

Risk Management

© NCEL

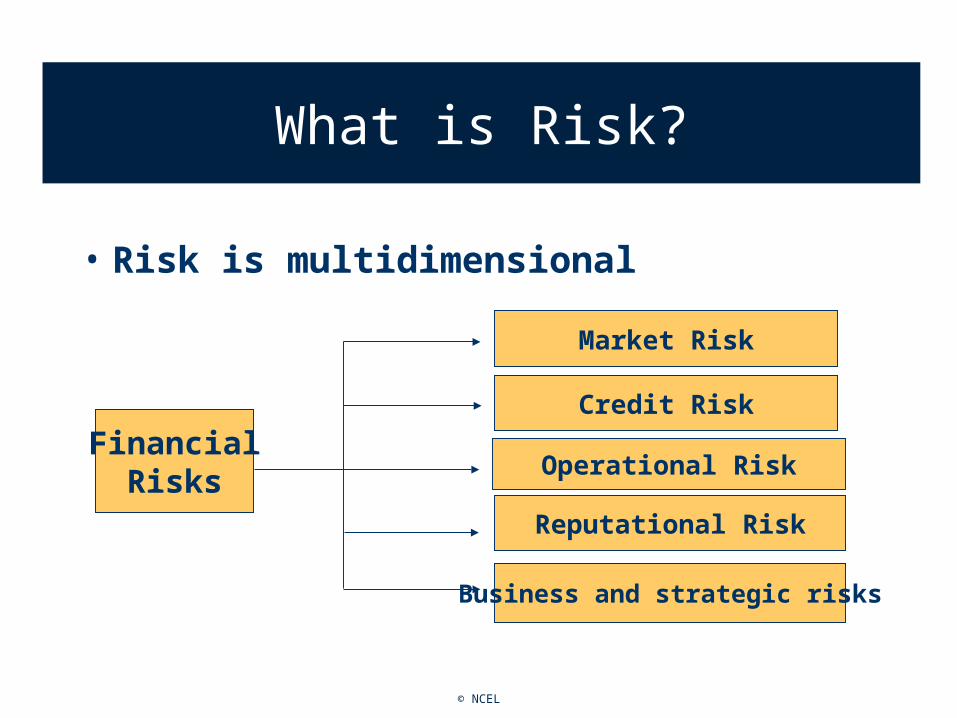

FinancialRisks

Operational Risk

Reputational Risk

Business and strategic risks

Market Risk

Credit Risk

What is Risk?

• Risk is multidimensional

© NCEL

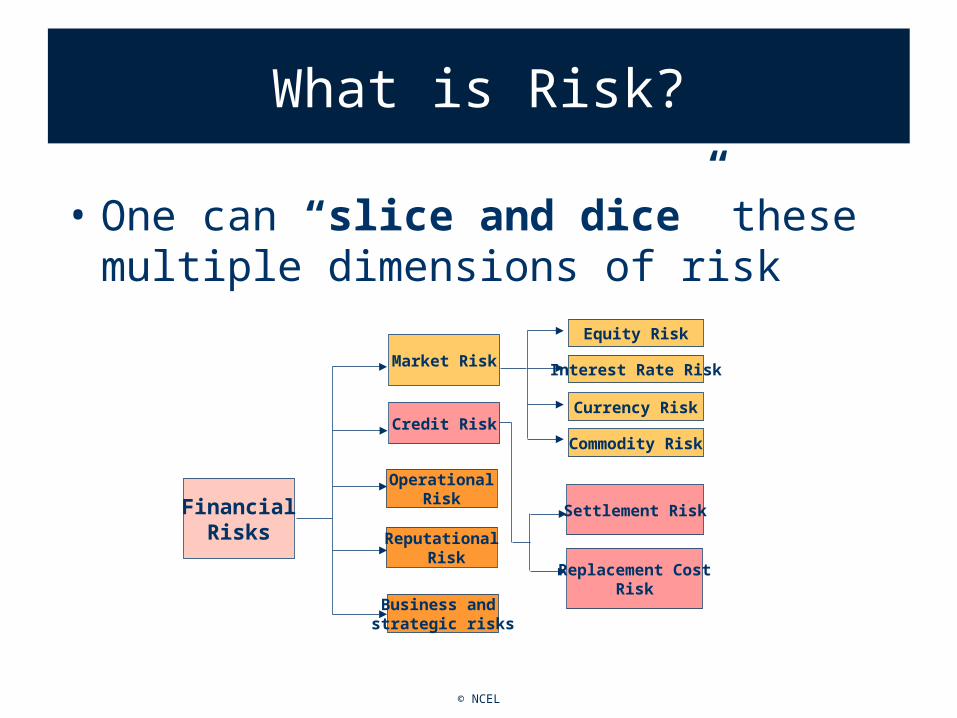

What is Risk?

• One can “slice and dice” these multiple dimensions of risk

Replacement CostRisk

Settlement Risk

Equity Risk

Interest Rate Risk

Currency Risk

Commodity Risk

FinancialRisks

OperationalRisk

Reputational Risk

Business and strategic risks

Market Risk

Credit Risk

© NCEL

What is Risk?

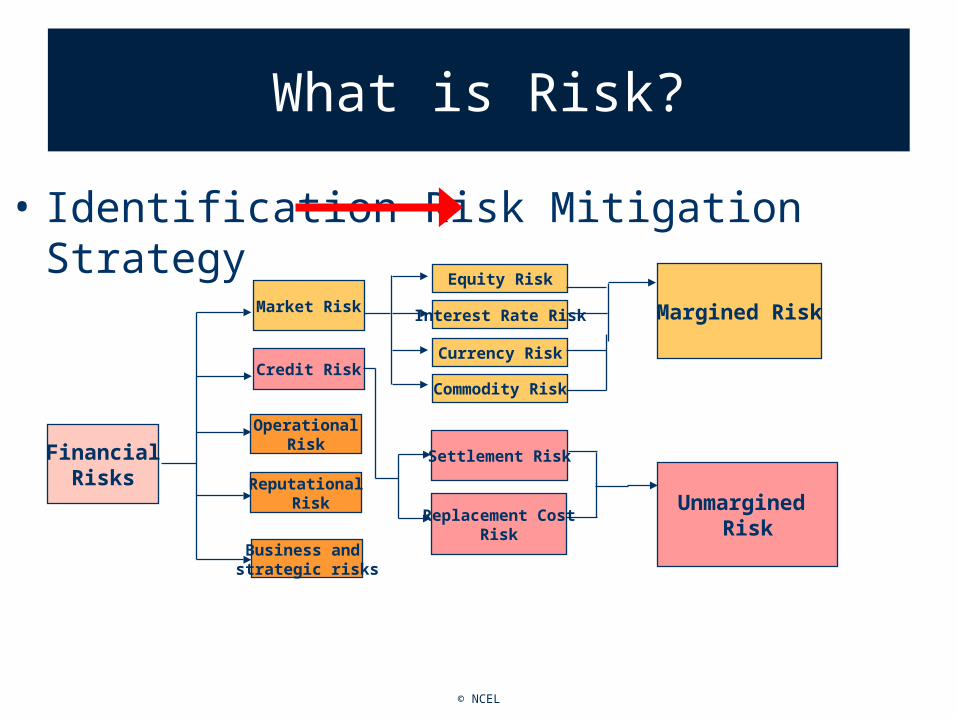

• Identification Risk Mitigation Strategy

Replacement CostRisk

Settlement Risk

Unmargined Risk

Margined Risk

Equity Risk

Interest Rate Risk

Currency Risk

Commodity Risk

FinancialRisks

OperationalRisk

Reputational Risk

Business and strategic risks

Market Risk

Credit Risk

© NCEL

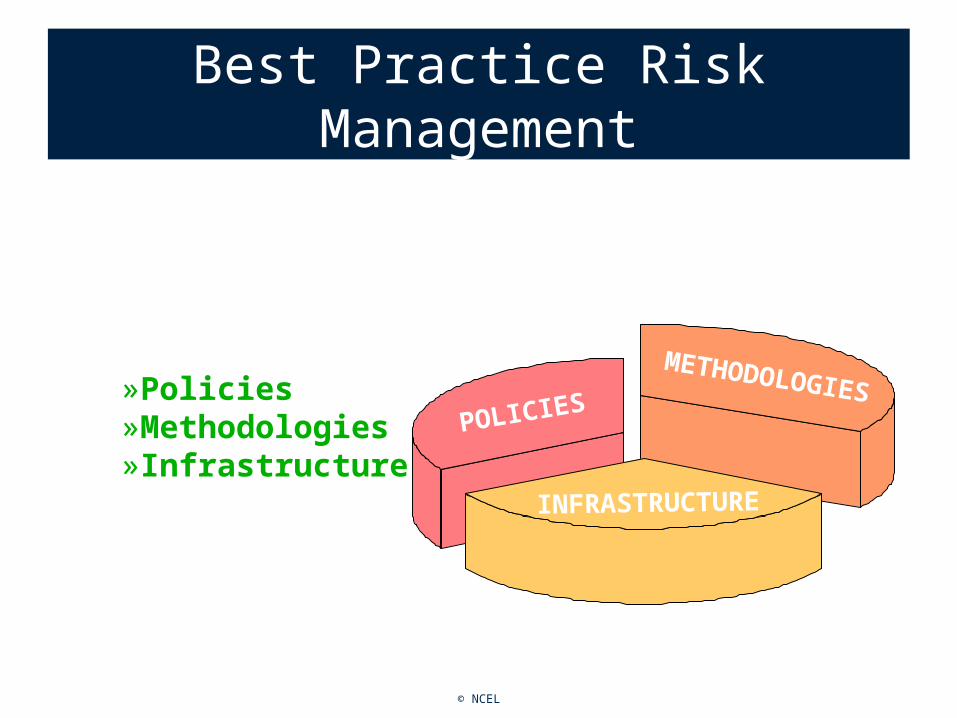

• Framework for Risk Management can be benchmarked in terms of:

POLICIES

METHODOLOGIES

INFRASTRUCTURE

Best Practice Risk Management

»Policies»Methodologies»Infrastructure

© NCEL

• Framework for Risk Management can be benchmarked in terms of:

POLICIES

METHODOLOGIES

INFRASTRUCTURE

Best Practice Risk Management

»Policies»Methodologies»Infrastructure

ProactiveRisk

Management

© NCEL

Risk Management@

PMEX

© NCEL

Market Risk Mitigants

• Complete segregation – cornerstone • Initial Margins determined using VaR

– No netting-off between clients• Pre-Trade Check• Spot Month • Delivery Margin• Credits

– Intra commodity spreads– Inter commodity spreads

• Daily Mark-to-Market of Positions• Variation Margin in Cash only• Daily Settlement Price Process

© NCEL

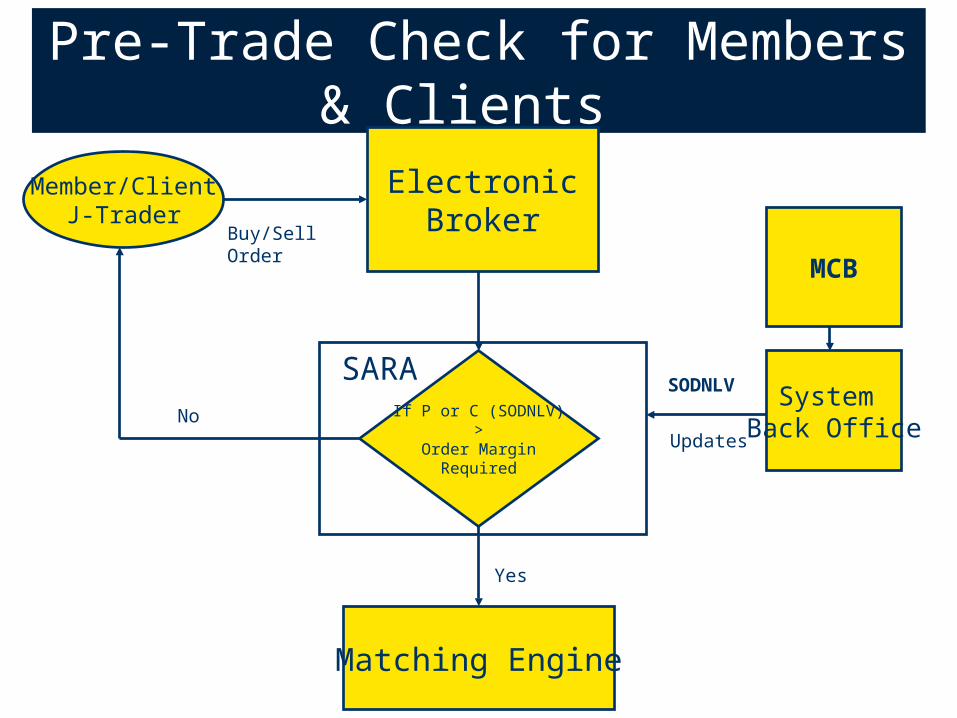

Pre-Trade Check for Members & Clients

Member/ClientJ-Trader

ElectronicBrokerBuy/Sell

Order

If P or C (SODNLV)>

Order MarginRequired

SARA

Matching Engine

Yes

NoSystem

Back Office

MCB

SODNLV

Updates

© NCEL

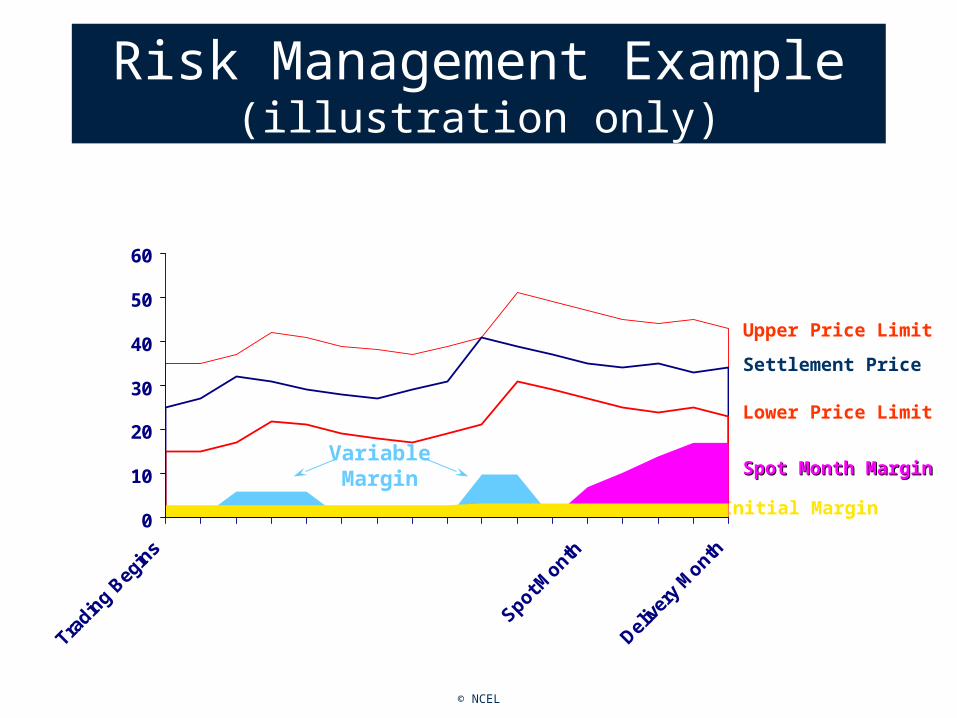

Risk Management Example(illustration only)

Settlement Price

Lower Price Limit

Upper Price Limit

Spot Month MarginSpot Month Margin

Initial Margin0

10

20

30

40

50

60

Tradin

g Beg

ins

Spot Month

Deliv

ery

Month

VariableMargin

© NCEL

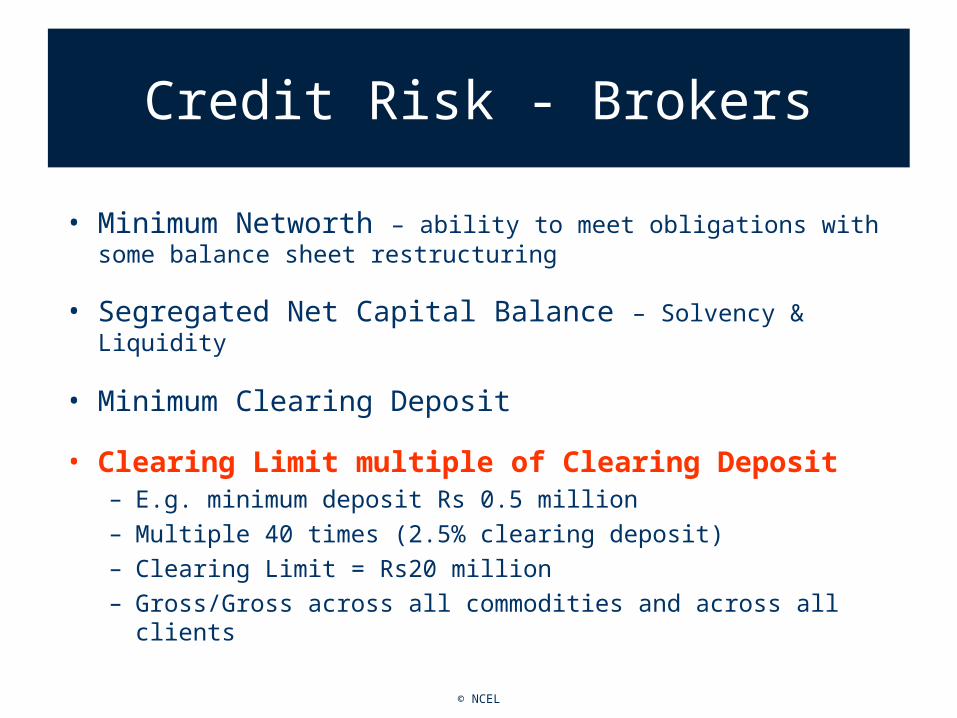

Credit Risk - Brokers

• Minimum Networth – ability to meet obligations with some balance sheet restructuring

• Segregated Net Capital Balance – Solvency & Liquidity

• Minimum Clearing Deposit

• Clearing Limit multiple of Clearing Deposit– E.g. minimum deposit Rs 0.5 million– Multiple 40 times (2.5% clearing deposit)– Clearing Limit = Rs20 million– Gross/Gross across all commodities and across all clients

© NCEL

Other Tools & Measures

• Market Monitoring up to Client Level in real-time– To counter front running, wash trading, trading opposites, etc

• Unambiguous default provisions

• Misconduct, un-business like conduct and unprofessional conduct clearly defined

• Each and every participant has to follow the Regulations, Circulars, Notices and Guidelines

• Granting Exemptions or making exceptions not in PMEX’s vocabulary

© NCEL

Position Limits

• Position Limits – Members & Clients

• To counter excessive speculation and manipulation– Limits the number of contracts that can be entered

into:• Gross across all clients• Gross across all contracts• Grossed up to the Member level

• Open contracts held by one individual investor with different brokers are combined using Client ID’s

© NCEL

NCEL Trading System

One of the costs for brokers is investment in client management and back office system

However, NCEL being an equal opportunity provider offers this to its brokers for free

• PMEX will provide a complete end-to-end online trading & Client Management system to brokers:

– Risk Management (pre-trade check), Electronic Fund Transfer, Margin Call generation, online 24/7 access to daily ledgers and accounting, secure access (USB key and personal digital certificates), access to historical data, etc.

• Margin calls with online bank transfers facility

• Pre-trade check and daily mark-to-market protects brokers from client defaults

© NCEL

PMEX Technology

• Focus on availability , strong security, and ease of use

• State-of-the-art data center with biometric access control and fire protection system

• Redundant network both internal and external, multiple ISP links

• 100% Internet driven exchange• Strong two factor authentication of traders using

USB Keys (smart cards)• Authentication based on Digital Certificate

credentials• Disaster recovery based on Veritas clustering,

remote replication and tape library backup solutions• Separate Disaster Recovery site for business

continuity

USB Key

© NCEL

Trading on PMEX

© NCEL

Trading on PMEX

• Investors have two methods of trading on PMEX:1. Direct access to the market2. Traditional route of placing orders through brokers

• In both cases, Broker is the Obligor to the Exchange

• Broker responsible for ensuring all Client Margins are paid

• Broker responsible for ensuring Clients comply with PMEX Regulations

• Broker responsible for Exposure/Margin/Position monitoring of all clients

• Broker earns commissions from both types of Clients

• Less Overheads if Clients allowed direct access

© NCEL

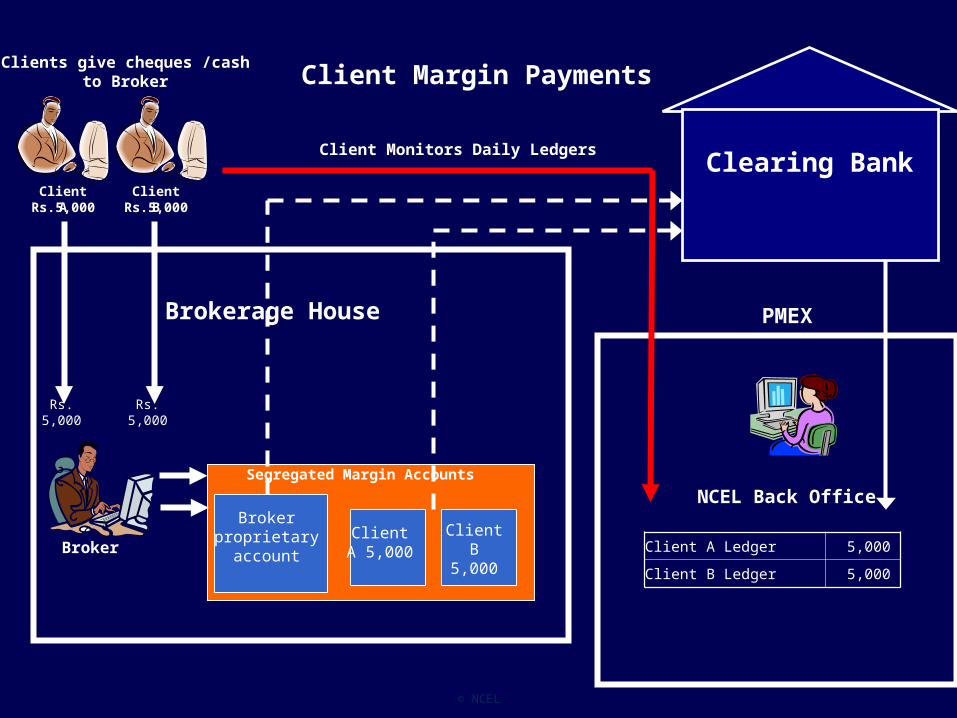

NCEL Back Office

Broker

Brokerage House

Segregated Margin Accounts

Client Margin Payments

Client ARs.5,000

Client BRs.5,000

Rs. 5,000Rs. 5,000

PMEX

Client A Ledger 5,000

Client B Ledger 5,000

Client Monitors Daily Ledgers

Client A 5,000

Client B 5,000

Broker proprietary

account

Clearing Bank

Clients give cheques /cash to Broker

© NCEL

How to Start Trading?Contact an PMEX Registered Broker

Enter Orders, Monitor Position, Pay Margins

Ask for training, if using Direct Terminal

Verify that Margins have been paid to PMEX

Insist on Account Statements from Broker

Payment of Initial Margin to Broker

Broker Opens Trading Account

If required, ask for Direct Trading Terminal

Read and Sign Risk Disclosure Documents

Step 1

Step 4

Step 5

Step 6

Step 7

Step 8

Step 9

Step 3

Step 2

© NCEL

www.pmex.com.pk