Embed Size (px)

Citation preview

Financial InstitutionsDepository Institutions

Presented by S. Cox

Objectives

Describe the various types of depository institutions

Discuss types of deposit insurance

Financial Institutions

A financial institution is any organization or business that provides services related to money.› Banks, credit unions, savings associations

are known as depository institutions A deposit is money placed or

transferred into a bank account. A customer who makes a deposit is

considered a depositor.

Financial Institutions

Banks are businesses…they are supposed to make money.

They use deposits to make loans to other customers…charging interest…and in turn generating revenue.› Also make money from ATM-usage fees,

overdraft fees, monthly account-maintenance fees, and other fees.

Financial Institutions

Depository institutions are one of the most important parts of the US economy …responsible for most of the money circulating in the country.

Paying bills or buying items using a debit or credit card are done through depository institutions as well as borrowing money.

Without depository institutions our economy would not function well.

Commercial Banks

Commercial banks are owned by stockholders (an investor who expects to make a return from his or her investment in stock).

Functions› Transfer funds, accept deposits, and make

loans to individuals, businesses, and governments

About 6,500 commercial banks in the US

Commercial Banks

Transfer funds - Every time you pay for something you are transferring money from yourself to another party› A transaction account allows the owner

to use it to pay a third party Checking accounts are the most common

type of transaction account

Commercial Banks

Accept deposits – can also save money at a bank› Savings accounts are deposit accounts that

provide a safe place to store your money. Do not have check writing privileges Banks pay interest on savings accounts Money market accounts are a type of

savings account that pays more interest than an average savings account, requires a larger initial deposit, and a minimum balance…usually $500

Commercial Banks

Make loans – make more loans than other depository institutions› Cars› Houses› Sometimes higher education

Other services – vary from bank to bank› Safe-deposit box› Sell securities and insurance

Savings and Loan Associations

Savings and loan association (S & L) are a type of financial institution that helped customers save money by allowing small deposits and home loans; also known as a savings association or thrift institution (encouraged people to be thrifty and save).

Originally savings associations only provided savings accounts and home loans because many banks didn’t offer home loans.

Today savings associations offer other types of loans as well

Savings and Loan Associations

Operate for a profit Usually owned by stockholders but can

be owned by an individual, a group of people, or a corporation

Credit Unions

A credit union is a financial institution that provides many of the same services as banks and S & Ls, but owned by its members and run on a nonprofit basis.› Known as a cooperative or co-op (a business or

organization that is owned by its members who cooperate to run the organization)

› Not-for-profit means instead of paying profits to shareholders, money made by not-for-profit credit unions is returned to members in the form of higher interest rates on savings accounts and lower interest rates on loans.

Credit Unions

Share accounts are savings accounts at a credit union.

Share draft accounts are checking accounts at a credit union.

To open a credit union account you must meet membership criteria…most common relate to employer, occupation, and geography› Once enrolled as a member you can stay

member, even if you no longer meet the membership requirement

Credit Unions

Currently there are more credit unions (8,000) than banks in the US but banks tend to be larger…have more deposits, assets, and profits compared to credit unions

Federal Deposit Insurance

Deposit insurance covers the deposits of customers in the case of a bank failure.

Depository institutions pool their money and share risk to pay premiums to the deposit insurance fund (DIF) so that depositors can maintain their insured funds in the case of bank failure. › In most years, there are few bank failures and the fund

balance grows, but as a result of the financial crisis and resulting economic downturn in the early 21st century…the growth of this fund was affected.

Banks – Federal Deposit Insurance Corporation (FDIC) Credit unions – National Credit Union Administration

(NCUA)

Federal Deposit Insurance Corporation

Federal Deposit Insurance Corporation (FDIC) is an independent federal agency established in 1933 that provides deposit insurance up to $250,000 for depositors in insured banks and thrifts in the case of bank failure.› Since thousands of banks failed during the Great

Depression, the FDIC was created to promote public confidence in the banks.

› Since it was started, no depositor has lost a cent of insured funds due to the failure of an FDIC-insured institution.

Federal Deposit Insurance Corporation

Initially it covered each customer’s deposits up to $100,000 but in 2008 to improve confidence, it was raised to $250,000 for interest bearing accounts.› Was meant to be temporary but made

permanent in 2010› Non-interest bearing transaction accounts

(checking accounts) are covered regardless of the amount

Federal Deposit Insurance Corporation

Deposits are insured per ownership category per depository institution:› Single accounts› Joint accounts› Certain retirement accounts› Certain trust accounts› Employee-benefit plan accounts› Government accounts

Federal Deposit Insurance Corporation

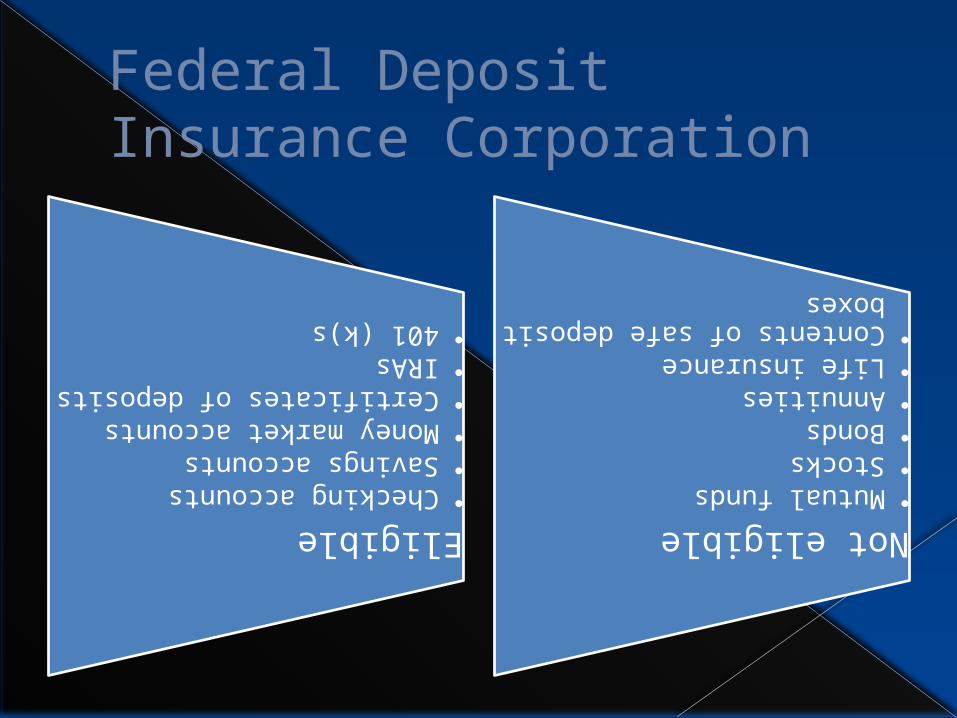

Eligible•Checking accounts•Savings accounts•Money market accounts•Certificates of deposits•IRAs•401 (k)s

Not eligible•Mutual funds•Stocks•Bonds•Annuities•Life insurance•Contents of safe deposit boxes

Federal Deposit Insurance Corporation

Banks must disclose the risks of purchasing non-deposit investment products that they sell

FDIC also monitors banks to help ensure that they do things by the book

Also manages banks that are failing

National Credit Union Share Insurance Fund

National Credit Union Share Insurance Fund (NCUSIF) was established in 1970 to insure credit union deposits up to $250,000.

NCUSIF is administered by the National Credit Union Administration (NCUA).

FDIC and NCUA are virtually Identical…› insure accounts up to $250,000› Pay insurance premiums› Backed by the government› Have examiners who determine financial soundness

of insured institutions› Insure state as well as federally chartered

depository institutions

Financial InstitutionsNon-Depository Institutions

Objectives

Define non-depository institutions Describe the role of investment banks

in raising capital Explain the purpose of securities Describe the function of finance

companies Explain how insurance companies

provide risk-management and investment options to their clients

Other Financial Institutions

Non-depository institutions – do not accept deposits although many make loans› Accept money from their customers to

invest in business deals, which spreads the risk and provides a way for customers to invest

› Examples: Investment banks, securities firms, finance companies, and insurance companies

Investment Banks

Investment Banks provide services for business…specialists in the securities markets› Help businesses raise capital…money…

through securities (financial instruments such as bonds and stocks)

› Help organizations issue bonds and find investors to buy them Bonds are debt issued by a government or

company For example, if you buy a bond you are loaning money

to that organization

Investment Banks

› Act as assist companies raise capital by acting as an agent to sell stock Stock is a security that gives the purchaser

part ownership in the company called equity Stockholders may receive dividends (payments)

from the issuing company

Securities Firms

Securities Firms are financial institutions involved in the trading of securities in financial markets also called brokerage firms, stockbrokers, or bondbrokers› If you wanted to buy Google stock, you would go

to a stockbroker, the stockbroker would place the order and charge a fee (commission)

› Full-service brokerage firms advise customers on which securities to buy and help manage their investments

› Discount brokers place orders for customers too but other services may be limited…fees are less

Finance Companies

Finance Companies make profits by issuing loans to businesses and individuals…only service provided to customers

Two major types1. Consumer financial companies – provide

personal loans to individuals…generally to those with poor credit and usually have a higher interest rates than a bank or credit union Payday lenders – short-term loans designed to

cover expenses until the borrower’s next payday…very expensive…interest rates can be 300% or higher

Finance Companies

2. Business financial companies – provide loans to businesses, such as retail stores…arranges with the business to provide loans on site to customers For example, a customer wants to buy a

computer but doesn't have the cash. The computer store can offer a loan. The computer store isn’t really issuing the loan, the business finance company issues the loan.

Some large manufacturers form their own finance company called captive finance companies, to provide loans so the manufacturer can easily sell its goods.

Insurance Companies

Insurance Companies are for-profit businesses that primarily sell insurance and may sell other products

Two primary ways insurance companies make money: Selling insurance policies and selling investment products

Insurance Companies

Insurance protects us against financial loss› Consumers buy an insurance policy by

making periodic payments, known as premiums and in return the insurance carrier agrees to cover losses according to the terms in the policy The person or thing covered by the policy is

called the insured

![Models and Exploration Methods for Major Gold Deposit Types · Models and Exploration Methods for Major Gold Deposit Types Robert, F. [1] , ... epithermal deposits has been more firmly](https://img.dokumen.tips/doc/110x75/5c9df1c488c993c6368bc9ef/models-and-exploration-methods-for-major-gold-deposit-types-models-and-exploration.jpg)