Embed Size (px)

Citation preview

CONTENTS

GOVERNOR’S FOREWORD ..................................................................................................................... 5

DIRECTOR’S FOREWORD ........................................................................................................................ 7

CHAPTER 1 INTRODUCTION ............................................................................................................. 9

CHAPTER 2 REGULATORY FRAMEWORK ......................................................................................... 13

CHAPTER 4 CONDITION AND PERFORMANCE OF THE MICROFINANCE SECTOR.............................. 19

CHAPTER 5 RESPONSES TO CHALLENGES IN THE MICROFINANCE SECTOR ................................... 27

CHAPTER 6 ROLE OF MICROFINANCE IN FINANCIAL INCLUSION ................................................... 29

CHAPTER 7 OUTLOOK ......................................................................................................................... 35

APPENDICES 39

MISSION STATEMENT

MIMISSIO N STATEMENT

Vision

To become a transformative and responsive Central Bank.

Mission

Maintaining financial stability and financial inclusion through credible policies and risk

based supervision of banks, supported by a skilled human resource base and a

modern integrated ICT system.

Values

Trust

Integrity

Passion

Transparency

Accountability

Efficiency

Creativity

PURPOSE OF THE REPORT

The purpose of this microfinance annual report is to provide an analysis of the status

and performance of the microfinance sector in Zimbabwe for the year ended 31

December 2015. This report presents an overview of the microfinance activities

during the period under review.

GOVERNOR’S FOREWORD

1. This inaugural Microfinance Annual Report comes at

a time when microfinance has enjoyed

unprecedented growth in the past decade to

become an important subsector of the global

financial system. Policy makers and regulators

worldwide recognize the vital role of microfinance

as an important tool in economic development and

poverty alleviation through facilitating access to

financial services.

2. In Sub-Saharan Africa microfinance has continued to register impressive growth

particularly in East Africa on the backdrop of the expansion of mobile technology

driven solutions.

3. Since the adoption of the multicurrency regime in 2009, the Zimbabwe microfinance

sector has enjoyed steady growth as reflected by an expansion in branch outreach and

number of clients accessing financial services from microfinance institutions.

4. Notwithstanding the noted positive growth, the microfinance sector has not been

spared from the challenges affecting the domestic economy which include market

illiquidity, absence of affordable wholesale funds, and non-performing credit.

5. Cognisant of the role of microfinance in channelling financial services to low income

groups, and the challenges hindering the sector from reaching its full potential, the

Reserve Bank spearheaded the development of the National Financial Inclusion

Strategy (NFIS) which was launched on 11 March 2016. Microfinance occupies a

prominent role in the NFIS as one of the four key pillars and is expected to play a

critical role in facilitating access to financial services by the unbanked particularly

small to medium enterprises (SMEs) which are recognised globally as the engine for

growth.

6. The Reserve Bank remains resolute in the execution of its mandate to maintain the

safety and soundness of the financial sector through proactive supervision and

enhancement of its supervisory tools and techniques to provide a more supportive

and efficient regulatory and supervisory framework for the microfinance sector in line

with international best practice.

7. To this end, the key stakeholders in the microfinance sector drafted a Microfinance

Policy to guide the sector’s development. The policy awaits requisite Government

approval.

8. The provisions of the Microfinance Act [Chapter 24:29] which was gazetted in 2013,

have promoted strengthened risk management and corporate governance systems

and practices in microfinance institutions. The introduction of the deposit-taking

microfinance licence has provided the long awaited avenue for funding through

authorized deposit mobilization. In the past some errant microfinance institutions

(credit-only) have ventured into illegal deposit-taking resulting in members of the

public losing their money.

9. The Reserve Bank and other stakeholders have since proposed amendments to the

Microfinance Act to further refine the legal framework. The amendments seek to

address, inter alia, tenure of the microfinance licence, the confusing categorization of

the microfinance institutions and liability of directors.

10. I wish to thank all our stakeholders for their dedication and invaluable support to the

Reserve Bank in its endeavours to create a strong, sustainable and inclusive financial

system that is supportive of economic growth.

Dr. J. P. Mangudya

Governor

DIRECTOR’S FOREWORD

1. Microfinance plays a critical role in providing access to

finance by the low-income groups and micro, small and

medium enterprises who cannot access the same from

the formal banking system, due to the absence of

collateral acceptable to banking institutions.

Microfinance is used as a tool to reach out to remote areas that are shunned by banking

institutions.

2. In view of its importance in economic development and poverty alleviation in Zimbabwe,

the microfinance sector has assumed an important role in the National Financial

Inclusion Strategy alongside other pillars namely financial literacy, financial innovation

and financial consumer protection. To promote the growth of the microfinance sector,

the Reserve Bank embarked on initiatives which include establishment of the credit

reference system and collateral registry, licensing of deposit-taking microfinance

institutions (DTMFIs), capacity building workshops and consumer financial literacy

awareness campaigns.

3. The above measures are expected to reduce information asymmetry in the sector,

facilitate effective management of credit risk and promote access to microfinance

products and services by segments previously excluded from formal financial services.

4. Further, the enactment of the Microfinance Act [Chapter 24:29] in 2013 which

incorporated a Code of Conduct also enhanced the consumer protection framework for

consumers of microfinance products and services.

5. The microfinance sector grew at an average of 32.61% in the last five years, in spite of

the constraints in the operating environment. Total loans increased from $63.43 million

as at 31 December 2011 to $187.16 million as at 31 December 2015. The number of

licensed microfinance institutions and branches increased from 95 and 106 to 152 and

571 from 2009 to 2015, respectively. Over the years, microfinance branch network has

also expanded to cover all the ten provinces of the country, while the proportion of

women accessing funding from microfinance institutions increased from 32.90% in 2014

to 42.10% in 2015.

6. Despite funding and capitalisation challenges the microfinance institutions have been

able to raise local and offshore funding to finance productive sectors of the economy,

particularly small and medium enterprises and small scale farmers.

7. In 2013 the Reserve Bank in conjunction with other key stakeholders constituted the

Microfinance Advisory Council (MAC) to promote the development of the microfinance

industry and expansion of financial inclusion. MAC has been instrumental in raising

awareness of the legal and regulatory provisions among the microfinance institutions.

8. In 2015 the Reserve Bank licensed three deposit-taking microfinance institutions which

are expected to play a major role in the development of the microfinance sector by

facilitating the mobilisation of savings from the unbanked segments of the population.

9. The Reserve Bank extends its sincere appreciation to all the stakeholders in the

microfinance sector, including the Zimbabwe Association of Microfinance Institutions,

microfinance institutions, and development partners for their continued support and

cooperation towards achievement of an inclusive, safe and sound financial system.

N. Mataruka

Director – Bank Supervision

CHAPTER 1 INTRODUCTION

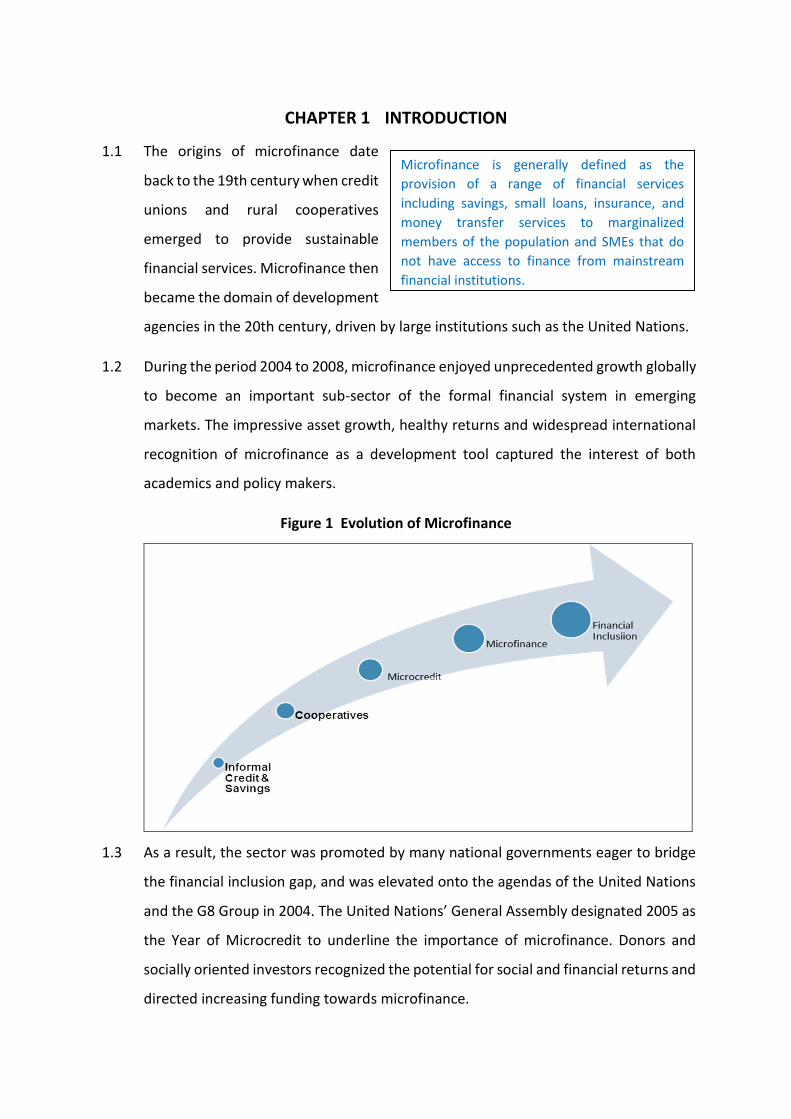

1.1 The origins of microfinance date

back to the 19th century when credit

unions and rural cooperatives

emerged to provide sustainable

financial services. Microfinance then

became the domain of development

agencies in the 20th century, driven by large institutions such as the United Nations.

1.2 During the period 2004 to 2008, microfinance enjoyed unprecedented growth globally

to become an important sub-sector of the formal financial system in emerging

markets. The impressive asset growth, healthy returns and widespread international

recognition of microfinance as a development tool captured the interest of both

academics and policy makers.

Figure 1 Evolution of Microfinance

1.3 As a result, the sector was promoted by many national governments eager to bridge

the financial inclusion gap, and was elevated onto the agendas of the United Nations

and the G8 Group in 2004. The United Nations’ General Assembly designated 2005 as

the Year of Microcredit to underline the importance of microfinance. Donors and

socially oriented investors recognized the potential for social and financial returns and

directed increasing funding towards microfinance.

Microfinance is generally defined as the

provision of a range of financial services

including savings, small loans, insurance, and

money transfer services to marginalized

members of the population and SMEs that do

not have access to finance from mainstream

financial institutions.

Global Microfinance Outlook

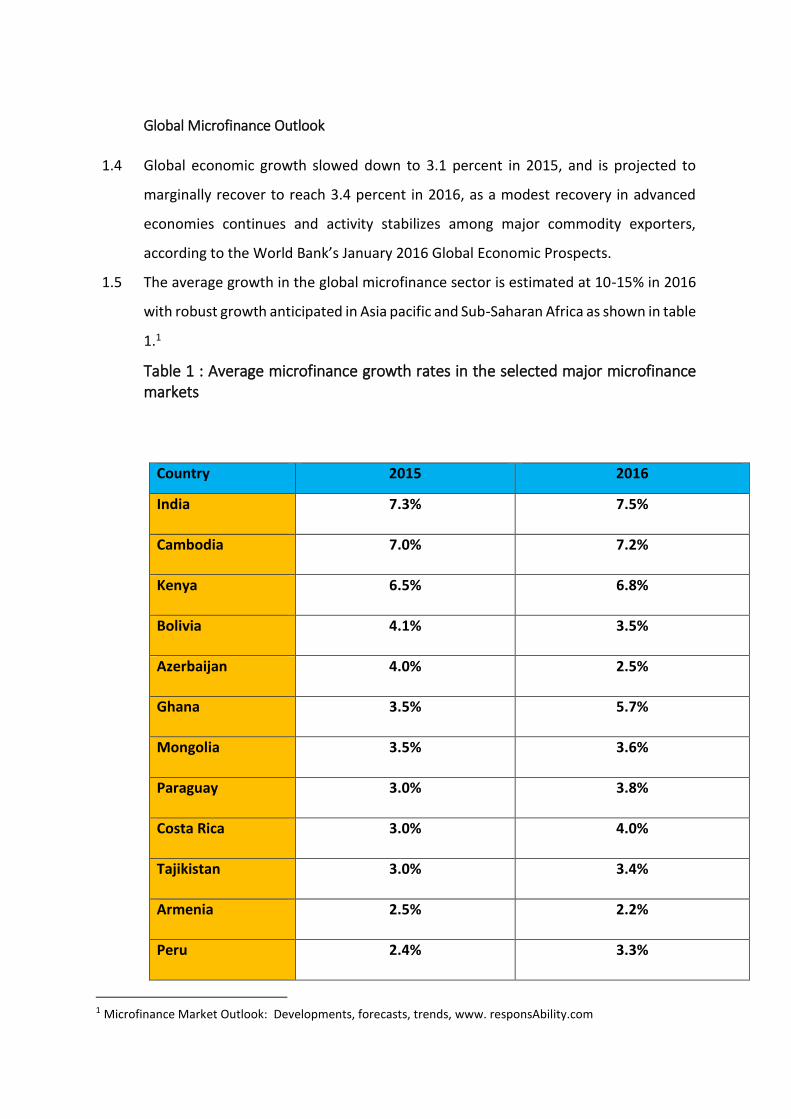

1.4 Global economic growth slowed down to 3.1 percent in 2015, and is projected to

marginally recover to reach 3.4 percent in 2016, as a modest recovery in advanced

economies continues and activity stabilizes among major commodity exporters,

according to the World Bank’s January 2016 Global Economic Prospects.

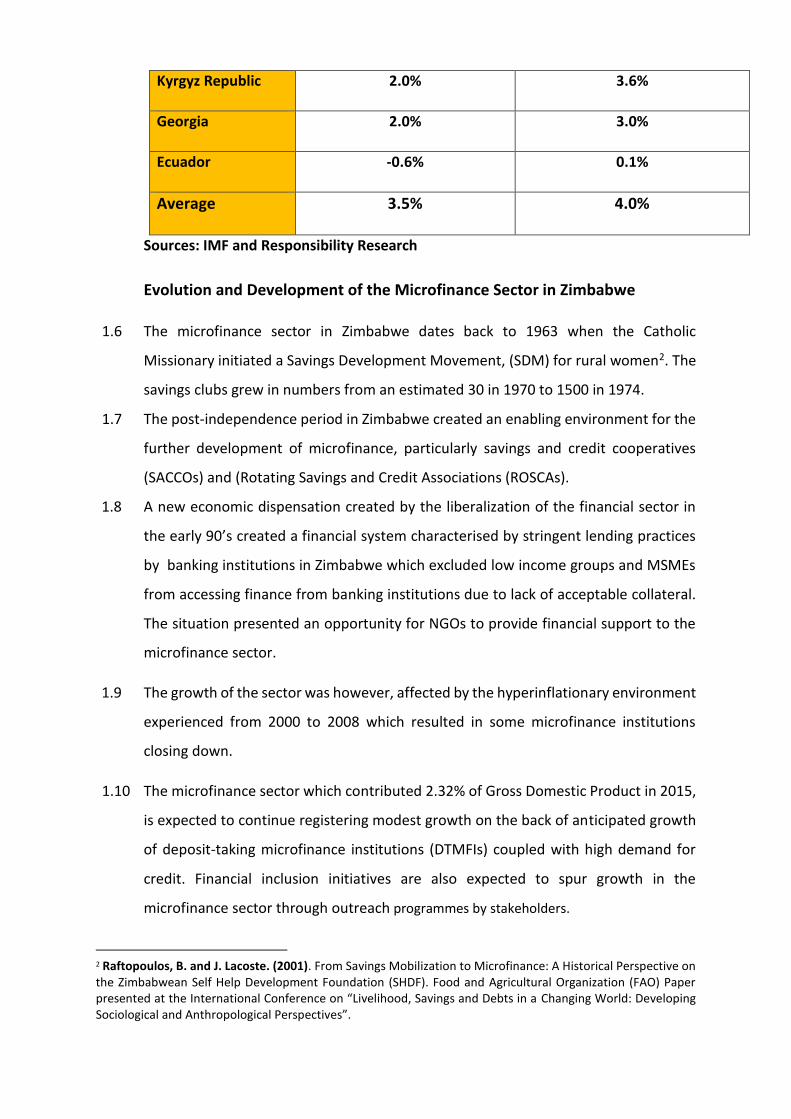

1.5 The average growth in the global microfinance sector is estimated at 10-15% in 2016

with robust growth anticipated in Asia pacific and Sub-Saharan Africa as shown in table

1.1

Table 1 : Average microfinance growth rates in the selected major microfinance

markets

1 Microfinance Market Outlook: Developments, forecasts, trends, www. responsAbility.com

Country 2015 2016

India 7.3% 7.5%

Cambodia 7.0% 7.2%

Kenya 6.5% 6.8%

Bolivia 4.1% 3.5%

Azerbaijan 4.0% 2.5%

Ghana 3.5% 5.7%

Mongolia 3.5% 3.6%

Paraguay 3.0% 3.8%

Costa Rica 3.0% 4.0%

Tajikistan 3.0% 3.4%

Armenia 2.5% 2.2%

Peru 2.4% 3.3%

Sources: IMF and Responsibility Research

Evolution and Development of the Microfinance Sector in Zimbabwe

1.6 The microfinance sector in Zimbabwe dates back to 1963 when the Catholic

Missionary initiated a Savings Development Movement, (SDM) for rural women2. The

savings clubs grew in numbers from an estimated 30 in 1970 to 1500 in 1974.

1.7 The post-independence period in Zimbabwe created an enabling environment for the

further development of microfinance, particularly savings and credit cooperatives

(SACCOs) and (Rotating Savings and Credit Associations (ROSCAs).

1.8 A new economic dispensation created by the liberalization of the financial sector in

the early 90’s created a financial system characterised by stringent lending practices

by banking institutions in Zimbabwe which excluded low income groups and MSMEs

from accessing finance from banking institutions due to lack of acceptable collateral.

The situation presented an opportunity for NGOs to provide financial support to the

microfinance sector.

1.9 The growth of the sector was however, affected by the hyperinflationary environment

experienced from 2000 to 2008 which resulted in some microfinance institutions

closing down.

1.10 The microfinance sector which contributed 2.32% of Gross Domestic Product in 2015,

is expected to continue registering modest growth on the back of anticipated growth

of deposit-taking microfinance institutions (DTMFIs) coupled with high demand for

credit. Financial inclusion initiatives are also expected to spur growth in the

microfinance sector through outreach programmes by stakeholders.

2 Raftopoulos, B. and J. Lacoste. (2001). From Savings Mobilization to Microfinance: A Historical Perspective on the Zimbabwean Self Help Development Foundation (SHDF). Food and Agricultural Organization (FAO) Paper presented at the International Conference on “Livelihood, Savings and Debts in a Changing World: Developing Sociological and Anthropological Perspectives”.

Kyrgyz Republic 2.0% 3.6%

Georgia 2.0% 3.0%

Ecuador -0.6% 0.1%

Average 3.5% 4.0%

1.11 Microfinance as one of the key pillars of NFIS is expected to play a key role in

promoting access to financial services in Zimbabwe. It can offer a wide variety of

financial services to the unbanked particularly at the bottom of the pyramid.

1.12 Digital financial services continue to gain popularity and provide opportunities to not

only expand outreach and reduce costs but also expand the menu of financial services.

From allowing MFIs to access micro-entrepreneurs in remote areas, to enabling the

implementation of more robust ICT and risk assessment tools, technology represents

a huge opportunity for microfinance institutions across the world.

CHAPTER 2 REGULATORY FRAMEWORK

2.1 Prior to August 2013, microfinance institutions were regulated under the Moneylending

and Rates of Interest Act [Chapter 14:14] and the Banking Act [Chapter 24:20].

2.2 The legal and regulatory framework for the microfinance sector in Zimbabwe was largely

inadequate. The legislation for the sector was a notable constraint to the deepening and

broadening of microfinance services and the participation of foreign investors.

2.3 The Moneylending and Rates of Interest Act [Chapter 14:14] was deficient in that it did

not sufficiently provide for important issues such as consumer protection, corporate

governance and was now out of sync with market developments.

Microfinance Act [Chapter 24:29]…

2.4 In recognition of the need for a more supportive and efficient regulatory and supervisory

legislative framework for the microfinance sector, the Microfinance Act [Chapter 24:29]

(the Act) was gazetted in 2013.

2.5 The Act provides for registration and deregistration of microfinance institutions,

including deposit-taking microfinance institutions and expectations for the standard

loan agreement, administrative, accounting, and risk management and corporate

governance practices.

Code of Conduct

2.6 The Act is also customer–centric and has strengthened the consumer protection

framework for microfinance clients through embracing the Core Client Protection

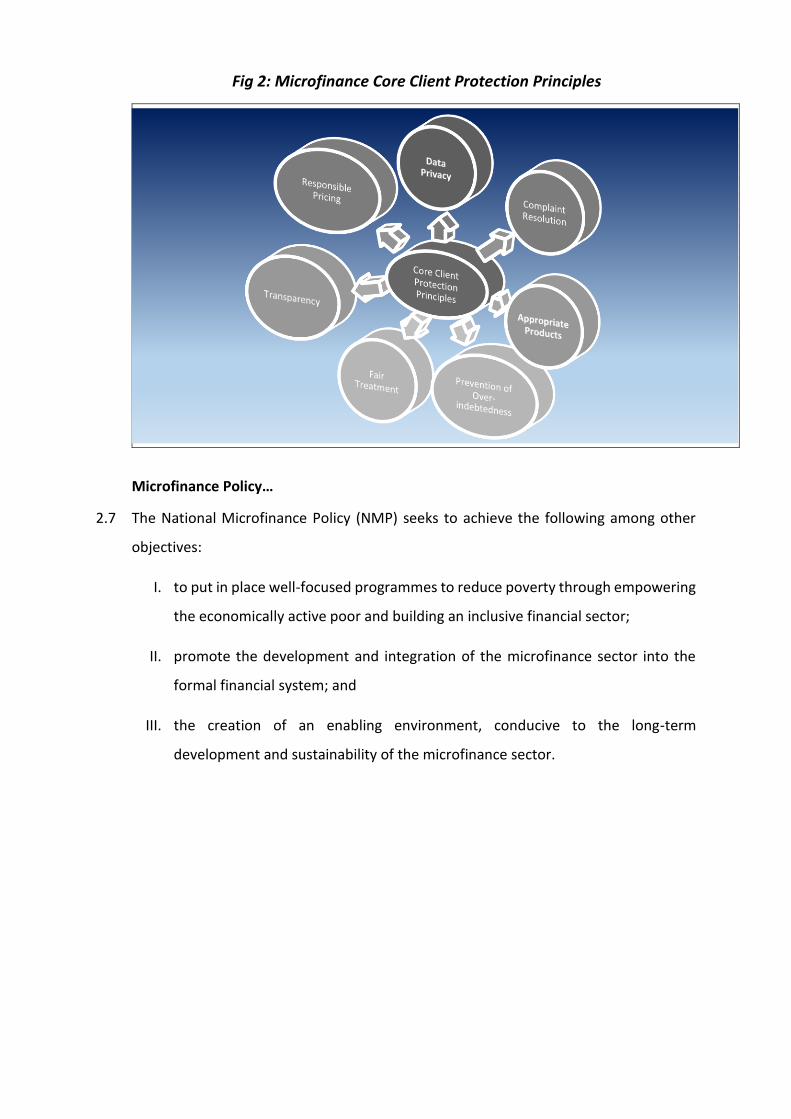

Principles shown in Fig 2 below which are enshrined in the Code of Conduct which is in

the Act.

Fig 2: Microfinance Core Client Protection Principles

Microfinance Policy…

2.7 The National Microfinance Policy (NMP) seeks to achieve the following among other

objectives:

I. to put in place well-focused programmes to reduce poverty through empowering

the economically active poor and building an inclusive financial sector;

II. promote the development and integration of the microfinance sector into the

formal financial system; and

III. the creation of an enabling environment, conducive to the long-term

development and sustainability of the microfinance sector.

CHAPTER 3 ARCHITECTURE OF THE MICROFINANCE SECTOR

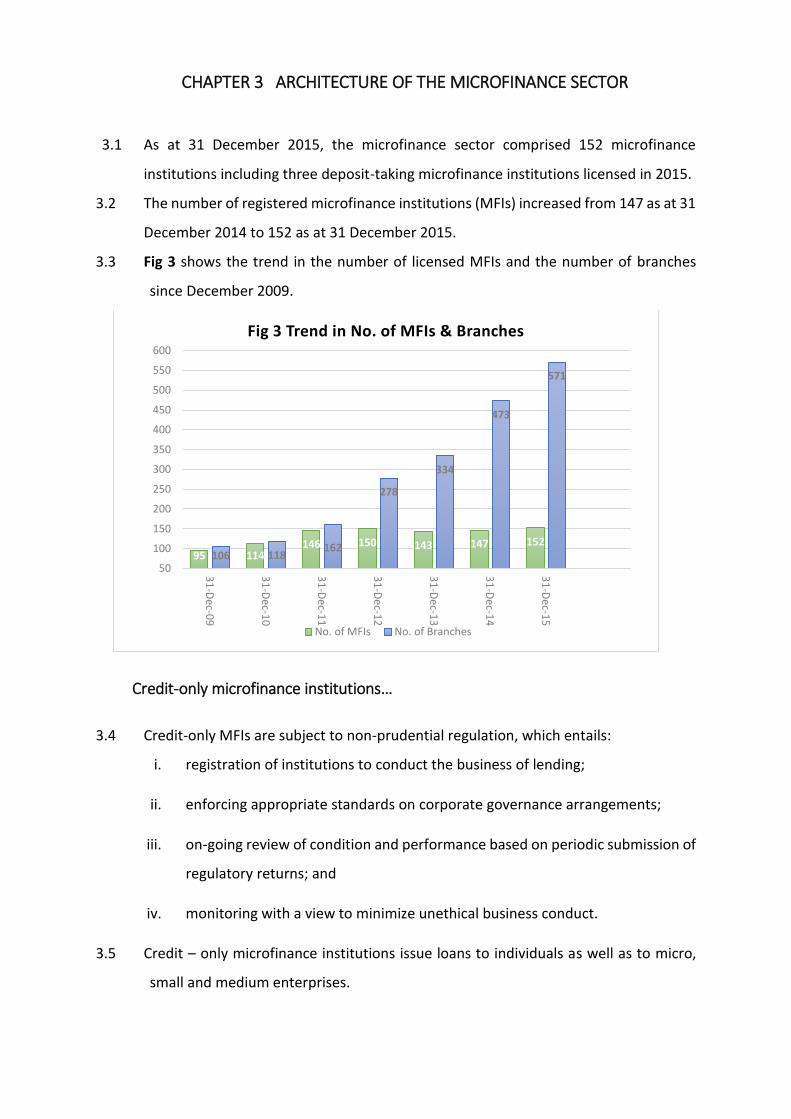

3.1 As at 31 December 2015, the microfinance sector comprised 152 microfinance

institutions including three deposit-taking microfinance institutions licensed in 2015.

3.2 The number of registered microfinance institutions (MFIs) increased from 147 as at 31

December 2014 to 152 as at 31 December 2015.

3.3 Fig 3 shows the trend in the number of licensed MFIs and the number of branches

since December 2009.

Credit-only microfinance institutions…

3.4 Credit-only MFIs are subject to non-prudential regulation, which entails:

i. registration of institutions to conduct the business of lending;

ii. enforcing appropriate standards on corporate governance arrangements;

iii. on-going review of condition and performance based on periodic submission of

regulatory returns; and

iv. monitoring with a view to minimize unethical business conduct.

3.5 Credit – only microfinance institutions issue loans to individuals as well as to micro,

small and medium enterprises.

95 114146 150 143 147 152

106 118162

278

334

473

571

50

100

150

200

250

300

350

400

450

500

550

600

31

-Dec-0

9

31

-Dec-1

0

31

-Dec-1

1

31

-Dec-1

2

31

-Dec-1

3

31

-Dec-1

4

31

-Dec-1

5

Fig 3 Trend in No. of MFIs & Branches

No. of MFIs No. of Branches

Deposit-taking Microfinance Institutions…

3.6 The first deposit-taking MFIs were registered in 2015. As at 31 December 2015, there

were three registered deposit-taking microfinance institutions namely African Century

Limited, GetBucks Financial Services (Private) Limited and Collarhedge Financial

Services (Private) Limited. All three institutions were licensed in 2015. African Century

Limited and GetBucks Financial Services (Private) Limited commenced operations in

January 2016.

3.7 Deposit-taking microfinance institutions are subjected to prudential regulation which

is achieved through the rigorous application of the following prudential standards,

among others:

i. Minimal capital requirements;

ii. Limits on unsecured lending;

iii. Provisioning requirements;

iv. Limits on lending to a single borrower or related party;

v. Restriction on declaration of dividends;

vi. Liquidity requirements; and

vii. Standard loan documentation requirements.

Other Providers of Microfinance Services…

3.8 In Zimbabwe microfinance is provided by banks, Post Office savings Bank (POSB),

microfinance institutions (MFIs), associations (ROSCAs), Savings and Credit

Cooperatives (SACCOs) and non-governmental organizations (NGOs). The government

is also a supplier of microfinance resources to the rural poor mainly in the form of

agricultural inputs and seasonal loans.

3.9 The majority of banks in Zimbabwe offer microfinance services and have established

dedicated SME divisions or units to provide financial services and capacity building.

Branch Network

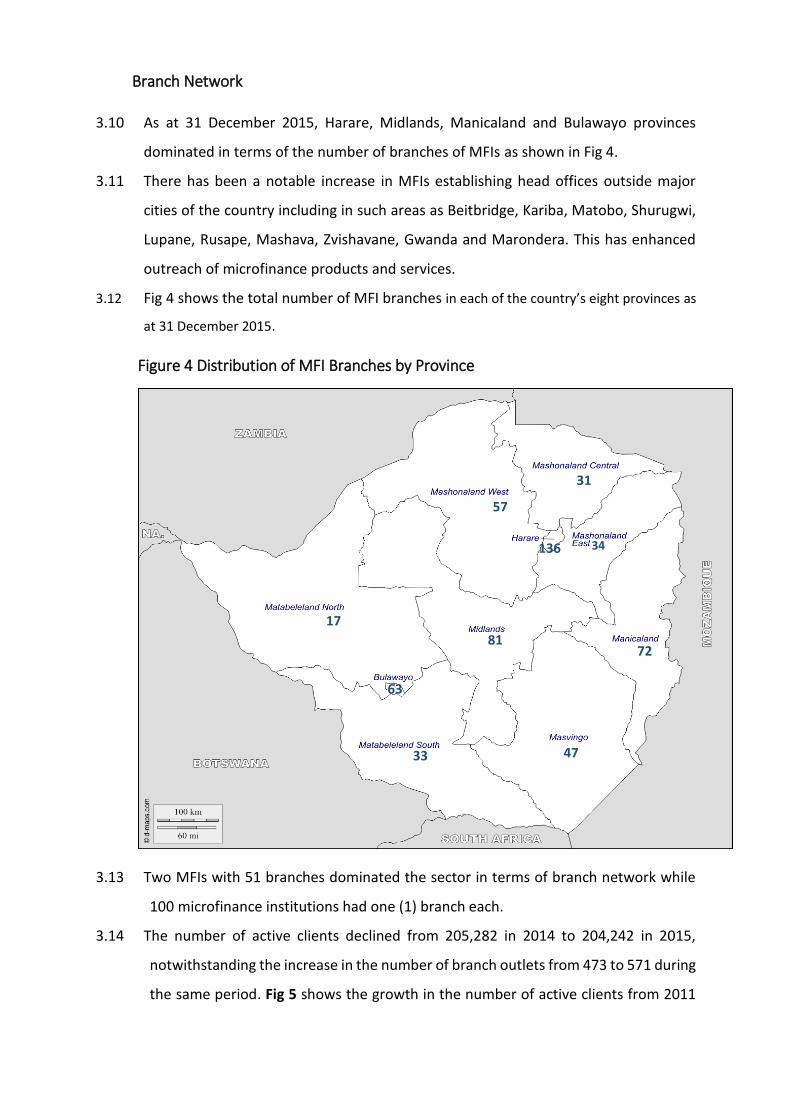

3.10 As at 31 December 2015, Harare, Midlands, Manicaland and Bulawayo provinces

dominated in terms of the number of branches of MFIs as shown in Fig 4.

3.11 There has been a notable increase in MFIs establishing head offices outside major

cities of the country including in such areas as Beitbridge, Kariba, Matobo, Shurugwi,

Lupane, Rusape, Mashava, Zvishavane, Gwanda and Marondera. This has enhanced

outreach of microfinance products and services.

3.12 Fig 4 shows the total number of MFI branches in each of the country’s eight provinces as

at 31 December 2015.

Figure 4 Distribution of MFI Branches by Province

3.13 Two MFIs with 51 branches dominated the sector in terms of branch network while

100 microfinance institutions had one (1) branch each.

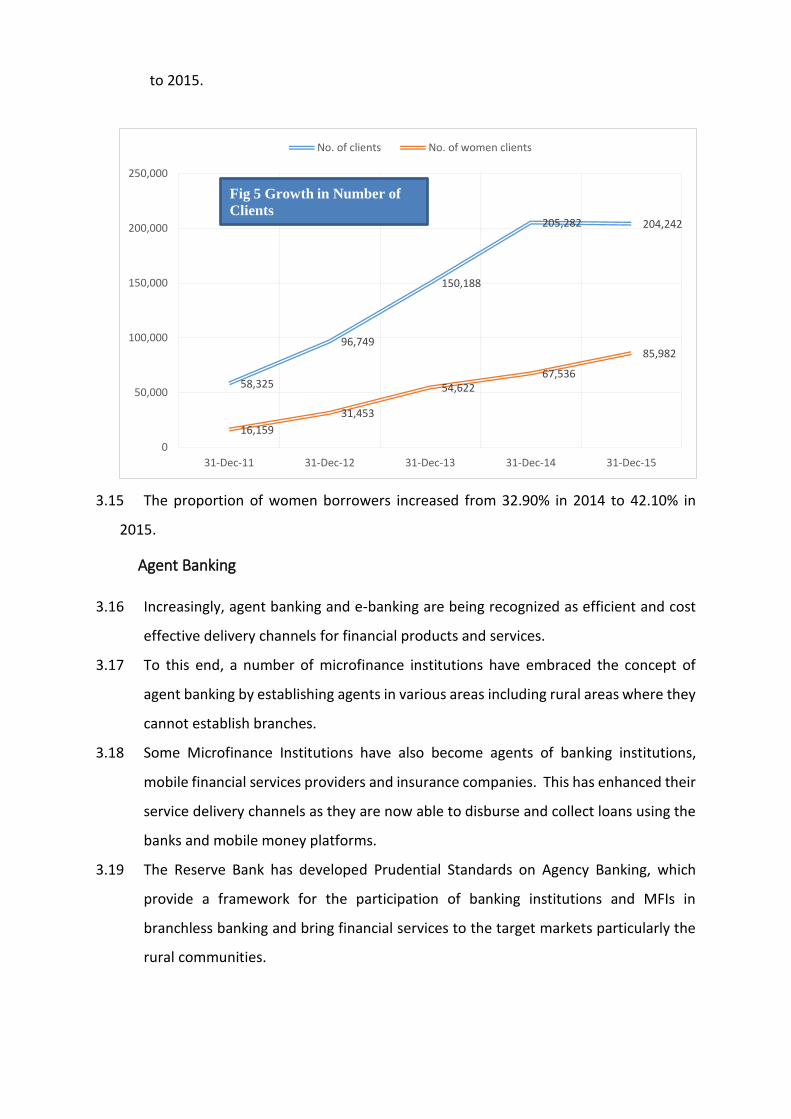

3.14 The number of active clients declined from 205,282 in 2014 to 204,242 in 2015,

notwithstanding the increase in the number of branch outlets from 473 to 571 during

the same period. Fig 5 shows the growth in the number of active clients from 2011

72

47 33

17

136

31

57

81

34

63

to 2015.

3.15 The proportion of women borrowers increased from 32.90% in 2014 to 42.10% in

2015.

Agent Banking

3.16 Increasingly, agent banking and e-banking are being recognized as efficient and cost

effective delivery channels for financial products and services.

3.17 To this end, a number of microfinance institutions have embraced the concept of

agent banking by establishing agents in various areas including rural areas where they

cannot establish branches.

3.18 Some Microfinance Institutions have also become agents of banking institutions,

mobile financial services providers and insurance companies. This has enhanced their

service delivery channels as they are now able to disburse and collect loans using the

banks and mobile money platforms.

3.19 The Reserve Bank has developed Prudential Standards on Agency Banking, which

provide a framework for the participation of banking institutions and MFIs in

branchless banking and bring financial services to the target markets particularly the

rural communities.

58,325

96,749

150,188

205,282 204,242

16,159

31,453

54,62267,536

85,982

0

50,000

100,000

150,000

200,000

250,000

31-Dec-11 31-Dec-12 31-Dec-13 31-Dec-14 31-Dec-15

No. of clients No. of women clients

Fig 5 Growth in Number of

Clients

CHAPTER 4 CONDITION AND PERFORMANCE OF THE MICROFINANCE

SECTOR

Introduction

4.1 The microfinance sector plays a significant role in promoting financial inclusion, self-

sufficiency and economic development particularly among the low income groups and

small to medium enterprises.

Lending Activities

4.2 Loans to the microfinance sector amounted to $187.16 million as at 31 December 2015,

an increase of 19.21% from $156.99 million as at 31 December 2014.

4.3 The top twenty microfinance institutions with a total loan book of $162.79 million

controlled 86.98% of the sector’s total loans as at 31 December 2015. The largest

microfinance institution, with a loan book of $32.50 million, commanded a market

share of 17.37% as at 31 December 2015.

4.4 As at 31 December 2015, loans comprised 83.13% of total microfinance assets of

$225.13 million compared to 77.45% as at 31 December 2014.

4.5 Fig 6 shows the trend in growth of loans in relation to growth in total microfinance

sector assets.

Fig 6: Growth in Total Microfinance Sector Assets and Loans

4.6 The bulk of loans disbursed by microfinance institutions were for consumption

185.73

202.71 202.58208.76 207.74

225.13

164.2156.99 163.53 162.2

173.31187.16

2013 2014 MAR-15 JUN-15 SEP-15 DEC-15

US

D i

n m

ilio

ns

Total Assets Total Loans

purposes constituting 54.26% while loans for productive or income generating

purposes constituted 42.43% as at 31 December 2015.

4.7 Table 2 shows the distribution of loans between productive or income generating

purposes and for consumption purposes.

4.8 There has been a significant shift from consumption lending as reflected by the drop in

the proportion from 70.89% in 2013 to 54.24% in 2015. It has also been established

that some of the individual loan facilities under consumption lending are utilised for

productive purposes.

4.9 MFIs have contributed to the development of

various areas in the country through financing

projects involving activities such as:

i. Banana Plantations in Honde Valley,

Manicaland;

ii. Micro-mortgage facilities to staff of universities, teachers unions and other

tertiary institutions;

iii. Irrigation Projects such as Redwood Irrigation Scheme in Umguza, Matebelenad

North;

iv. Cattle Fattening Schemes such as Masakhane Zihlobo Pen Fattening in Nkayi;

and

29.11%

46.70% 45.76%

70.89%

53.30% 54.24%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

2013 2014 2015

Fig 3: Distribution of Loans : 2013-2016

Productive Consumption

Mhende Irrigation Scheme-

Chirumanzu District, Mvuma

v. Small Scale Dairy projects in Chipinge.

4.10 The funding by MFIs has positively impacted

on the livelihoods of people around the

country. Small scale general dealers who

benefited from working capital increased the

variety of their trading stock and diversified

their businesses as well as introducing credit

facilities.

4.11 Microfinance institutions have also provided value chain financing to smallholder

livestock farmers who managed to increase their fattened cattle throughput. Small

scale horticulture farmers have also benefited immensely from microfinance loans that

have increased their disposable income and assets accumulation.

Portfolio at Risk (PaR)

4.12 The size of the portfolio at risk (PaR) ratio in the microfinance sector increased

marginally from $19.29 million as at 31 December 2014 to $20.06 million as at 31

December 2015. The growth was in line with the growth in the loan portfolio for the

entire sector on a year on year basis.

Small Scale Farmer, Mutoko, Mashonaland East

4.13 Although the level of credit risk in the sector as measured by the Portfolio at Risk (PaR)

ratio has been declining over the years from a peak of 25.52% as at 31 December 2012

to 10.72% as at 31 December 2015, the sector remains vulnerable to credit risk.

4.14 The improvement in the PaR ratio in the sector over the years is largely attributable to

improving credit risk management strategies and strengthening of underwriting

standards employed by microfinance institutions including enhanced credit risk

analysis and increased use of credit references.

4.15 The level of PaR is expected to continue improving in line with the on-going supervisory

initiatives including the capacity building in the areas of credit analysis and delinquency

management and the establishment of a credit reference system by the Reserve Bank.

Earnings…

4.16 Net profit after tax in the sector declined from $24.84 million for the year ended 31

December 2014 to $12.88 million for the year ended 31 December 2015. The decline is

largely attributed to increases in operating costs.

4.17 Fig 8 shows the trend in net income for the sector.

4.18 Consequently return on assets and return on equity declined significantly during the

same period as shown in Fig 11.

0

5

10

15

20

25

2011 2012 2013 2014 2015

2.63

4.91

22.04

24.84

12.88

USD

MIL

LIO

NS

FIG 8 :NET INCOME : 2011-2015

4.19 For the year ended 31 December 2015, eight (8) institutions, recorded net profit in

excess of one million dollars with eighteen (18) institutions posting losses. The losses

recorded by twelve (12) out of the eighteen (18) institutions were largely attributed to

start-up costs while those for the remaining six (6) institutions’ losses were attributed

to increases in provisions for bad & doubtful debts during the year.

Composition of Income

4.20 Total operating income of $100.15 million largely comprised interest income for the

year ended 31 December 2015. Ten microfinance institutions recorded total operating

income of $62.22 million constituting 62.12% of total income for the sector.

Sustainability

4.21 A number of microfinance institutions are considered sustainable3 as reflected by the

average Operational Self Sufficiency (OSS) of 124.57% for the year ended 31 December

2015. OSS is the ratio of an MFI’s operating revenues to its operating expenses

including the financial costs and impairment losses on loans.

4.22 The average OSS ratio is above the break-even point of 100%. Fifteen (15) microfinance

institutions out of 145 recorded OSS ratios of less than 100% largely due to high

3 Sustainability refers to the ability of a microfinance institution (MFI) to cover all its costs through interest and other income paid by its clients independent of external subsidies from donors or the government.

2.66%4.23%

11.87% 12.25%

5.72%

21.09%

6.87%

32.33%34.26%

13.28%

0%

5%

10%

15%

20%

25%

30%

35%

40%

2011 2012 2013 2014 2015

Fig 9 : Profitability Ratios:2011-2015

ROA ROE

employment costs.

4.23 A total of 18 institutions posted losses amounting to $7.65 million, with one

institution’s losses of $7.01 million contributing 91.67% of the total loss figure which

significantly weighed down the sector’s average OSS ratio.

4.24 The sector’s top twenty MFIs (total loans) had operating expenses ratio of less than

70% for the year ended 31 December 2015, indicating that the larger MFIs are striving

to enhance their operational efficiency.

Capitalisation…

4.25 Microfinance institutions’ funding mix for their operations include debt and equity.

Aggregate equity infusion in MFIs increased by 25.94% from $72.49 million in

December 2014 to $95.71 million in December 2015. Microfinance institutions also

accessed a total of $127.52 in debt financing for the period ended 31 December 2015.

4.26 The trend in the sector capital levels from 2011 to 2015 is shown in Fig 10.

Social Performance

4.27 Although a few microfinance institutions have embraced social performance

measurement, there is still more work to be done in this area as Zimbabwe is lagging

0

10

20

30

40

50

60

70

80

90

100

2011 2012 2013 2014 2015

12.46

29.08

68.1772.49

97.01

USD

Mill

ion

s

Fig 10: Total Sector Capital Levels: 2011 – 2015

behind. To accelerate this, the Zimbabwe Association of Microfinance Institutions

(ZAMFI) together with other stakeholders convened a Social Performance

Management workshop in April 2015. The workshop was facilitated by the Grameen

Foundation Southern Africa office based in Uganda.

4.28 Initiatives are underway to adopt the Progress out of Poverty Index (PPI) for

Zimbabwe. The PPI will scientifically measure progress out of poverty which all MFIs

can use going forward.

Challenges in the Microfinance Sector

4.29 The performance of the sector has been constrained by the challenges discussed

below.

Funding…

4.30 MFIs are primarily funded through equity, loans and credit lines. Since the adoption of

the multi-currency system in February 2009, these traditional sources have been

limited. The microfinance sector has operated under a constricted liquidity

environment which has manifested through constrained funding ability, limited credit

creation and high lending rates.

4.31 A number of microfinance institutions continue to struggle to build financial capacity

to underwrite meaningful business. Weak capitalisation is constraining the organic

growth of microfinance institutions.

4.32 The liquidity constraints and limited availability of wholesale funds in the economy has

adversely hampered the provision of financial services to the low income groups and

micro, small and medium enterprises.

4.33 Inadequate funding has also affected microfinance institutions’ capacity to acquire

robust ICT and risk management systems to support their operations and facilitate

impact and financial stability assessments. Weak management information systems

(MIS) have also affected institutions’ ability to submit regulatory returns therefore

hampering performance monitoring of the industry.

Shortage of Relevant Microfinance Skills…

4.34 The sector continues to experience shortage of critical and relevant skills in

microfinance in the areas of micro-credit analysis, risk management and

administration, largely due to funding constraints and inability to train and retain skills.

The shortage of relevant microfinance skills has negatively affected the institutions’

capacity to manage risks emanating from their activities.

Absence of a Comprehensive Credit Reference System…

4.35 The absence of a comprehensive credit reference system for use by MFIs operating in

Zimbabwe has affected the quality of MFIs’ credit risk management systems resulting

in multiple borrowings among the low income groups which leads to over-

indebtedness.

4.36 Information asymmetry in the sector is hampering access to financial services by the

low-income groups as the microfinance institutions do not have access to credit

information for the prospect borrowers.

Illegal Deposit-Taking by Some Microfinance Institutions…

4.37 In 2012, the Reserve Bank cancelled the operating licences of a number of credit-only

microfinance institutions which were boosting their funding bases by illegally

mobilizing deposits, and quoting fictitiously high deposit rates which were meant to

entice members of the public.

Customer Complaints…

4.38 The Reserve Bank has been inundated with complaints from the members of the public

regarding unsustainably high lending rates which have contributed to high levels of

indebtedness. The institutions, given the target market, have failed to aligning their

cost structures to reflect the obtaining operating environment.

4.39 In addition, the nature of complaints also reflect that some MFIs are not fully and

clearly explaining the terms and conditions of their loan facilities.

CHAPTER 5 RESPONSES TO CHALLENGES IN THE MICROFINANCE SECTOR

5.1 Cognisant of the need to create profitable and sustainable microfinance institutions

that offer affordable financial services, the Reserve Bank has taken initiatives

discussed below to eliminate the impediments to the growth of the microfinance

sector.

Capacity Building Initiatives

5.2 The Reserve Bank in conjunction with other stakeholders including ZAMFI has

facilitated a number of capacity building programs including training workshops and

attachment programs for Reserve Bank officers to share supervisory experience in the

area of regulation and supervision of deposit-taking microfinance institutions.

5.3 The Harare Institute of Technology (HIT) in collaboration with ZAMFI and the Reserve

Bank developed and introduced a professional training programme in microfinance

which leads to a Professional Certificate and Diploma in Microfinance.

Membership of Industry Association

5.4 The Reserve Bank continues to encourage microfinance institutions to be members of

a recognised industry association. Membership of an industry association enables

microfinance institutions to tap into industry best practices and standards and

facilitates access to technical assistance, information, training and tools, and funding.

Microfinance Advisory Council

5.5 In 2013 the Reserve Bank in conjunction with the Ministry of Finance & Economic

Development, ZAMFI, other financial sector regulatory authorities and other

stakeholders formed the Microfinance Advisory Council (MAC) to spearhead the

development of the microfinance industry and promoting financial inclusion.

5.6 The terms of reference of MAC include:

i. advise the government on strategies and policies for the development of the

microfinance sector;

ii. promote and facilitate capacity building in the microfinance sector;

iii. promote professionalism, integrity, accountability and dissemination of best

practices in the microfinance sector; and

iv. promote financial inclusion through encouraging and facilitating the

development of innovative microfinance products and delivery channels;

5.7 MAC has reviewed the Zimbabwe Microfinance Policy and organised workshops to

educate microfinance institutions on their duties and responsibilities in terms of the

Microfinance Act [Chapter 24:29].

Initiatives to Enhance Financial Capability Levels

5.8 The World Bank Consumer Protection and Financial Literacy Diagnostic Review and

the FinScope Consumer Survey of 2014 revealed that although Zimbabwe has a high

rate of general literacy, there is low financial literacy. As a result, consumers do not

understand some financial concepts particularly the financial language used in loan

applications and loan agreements which results in over indebtedness and high default

rates.

5.9 In this regard, the Reserve Bank issued Consumer Education and Awareness Bulletins

to educate the public on financial terminologies, financial services and responsible

financial management.

5.10 Further, the Reserve Bank engaged civil organisations and associations including the

Zimbabwe Teachers Association, Progressive Teachers’ Union and Consumer Council

of Zimbabwe as important stakeholders in financial consumer education and

protection.

Establishment of Credit Information System

5.11 The Reserve Bank with the technical support of experts from the World Bank is

working towards the establishment of a credit information system which will

alleviate the information asymmetry in the financial sector.

Establishment of a Collateral Registry

5.12 The Reserve Bank has also accessed financial and technical support of the World Bank

to establish a collateral registry which will enhance access to finance for lower income

groups on the back of movable assets as collateral.

CHAPTER 6 ROLE OF MICROFINANCE IN FINANCIAL INCLUSION

6.1 The FinScope Survey of 2014, revealed that only 23% of the rural population is formally

banked compared to 46% of the urban population, and only 14% of MSMEs owners

are banked. In addition there are low levels of financial literacy and capability, and a

decline in the actual usage of banking services between 2011 and 2014.

6.2 Empirical evidence has demonstrated that microfinance can be a catalyst in economic

development and eradication of poverty through engagement of previously excluded

sections of the community, particularly the youth and women. The scope of

microfinance emerged from humble beginnings of provision of micro-credit to the low

income groups to become a key pillar of financial inclusion through provision of a

wider range of financial products and services including insurance, savings and

remittances.

Access to Financial Services…

6.3 The role of microfinance in financial inclusion manifests itself through the creation of

facilities that enable the low income groups and MSMEs, which are affected by

comparatively higher levels of financial exclusion, to access a variety of financial

services including microcredit, micro-savings, remittances, payments, micro-

insurance and pensions, delivered through an extensive branch network in

partnership with banking institutions and mobile network operators.

6.4 Microfinance institutions are undoubtedly best-placed to address some of the

demand-side barriers to access to finance by MSMEs as, among other attributes, they

possess vast experience in MSME financing. In this respect, the microfinance sector

is expected to be instrumental in the implementation of the SME Financing Policy.

6.5 With adequate and appropriate funding, microfinance institutions can be the main

source of funding for the MSMEs that cannot access funding from the banking

institutions due to lack of collateral usually demanded by the banks.

A young businesswoman running a wire meshing business at Hauna Growth Point, Manicaland

Women

6.6 Notwithstanding the fact that 57% of the

business owners in Zimbabwe are women

(Finscope Survey, 2012), and that women

constitute the majority of the Zimbabwean

population, women remain highly

excluded from the formal financial services

sector.

6.7 The microfinance institutions have

recognised this opportunity and have in

the past year increased their lending to women owned enterprises from 32.90% in

2014 to 42.10% in 2015 of the aggregate loan portfolio of the sector.

Small-Scale Agriculture Financing

6.8 In recognition of the fact that Zimbabwe is an agro-economy with agriculture

contributing about 12% of the country’s GDP in 2014 and more than 60% of inputs to

the manufacturing sector, the microfinance institutions have made inroads in

broadening of access to financial services particularly by smallholder farmers. A

number of microfinance institutions have provided financial support to smallholder

farmers for the production of groundnuts, paprika, bananas and livestock.

A General Dealer Store run by a woman at Siphambi Businesss Centre, Masvingo

6.9 The role of microfinance institutions in the financing of agriculture is expected to be

bolstered by the implementation of an Agricultural & Rural Finance Policy which is

being developed as part of the implementation of the NFIS.

Youth

6.10 Youth in Zimbabwe are excluded from formal financial services largely due to high

levels of unemployment, negative stereotypes about youth who are considered high

risk-takers, lack of collateral, limited business and life experience, and lack of track

record or credit history. This is in addition to the other demand side constraints

affecting all consumers of financial services.

Small Scale Banana Planation owned by a woman in Honde Valley, Manicaland

6.11 Microfinance Institutions are expected to be instrumental in implementing financial

inclusion strategies for the participation of the youth in some or all of the following

measures proposed in the National Financial Inclusion Strategy:

i. Design and implementation of financial literacy programs for the youth;

ii. Establishment of a youth empowerment window by all financial institutions;

iii. Development of appropriate collateral substitutes in order to address the

challenge of security among youth borrowers;

iv. Capacitation of vocational training centres across the country to ensure well

trained graduates are in a position to apply their knowledge on start-ups; and

v. Ensuring that regulatory frameworks and policies are youth friendly and

protective of youth rights in order to increase youth financial inclusion.

Savings mobilisation

6.12 The registration of deposit-taking microfinance institutions will go a long way in

mobilisation of deposits from the historically marginalised segments of the

population, through the development and introduction of innovative and tailor-made

savings accounts which suite the size and level of their cashflows. By providing

savings opportunities for households and MSMEs, deposit-taking microfinance

institutions reduce the vulnerability of their clients to natural disasters, and

A young farmer attending to a Horticulture project .

unexpected illnesses, while enabling them to smoothen their consumption

expenditures with their savings.

Reaching Out to the Remote Areas…

6.13 One of the impediments to financial inclusion is the absence of suppliers of formal

financial products and services in the remote and rural areas of the country, largely

due to inadequate financial and poor physical infrastructure.

6.14 Microfinance institutions play a significant role in facilitating financial inclusion as

they are uniquely positioned in reaching out to the rural communities. Many of them

operate in a limited geographical area, have a greater understanding of the unique

and specific needs of local communities, and are flexible in their operations providing

a level of comfort to their clients.

6.15 Microfinance institutions have managed to reach out to remote areas shunned by

other formal financial institutions. Over the years, microfinance institutions have

expanded their branch network from predominantly urban centres like Harare and

Bulawayo to all the ten provinces of the country. The spread of microfinance into

these predominantly agriculture-based regions has opened more opportunities for

the growth not only of the microfinance institutions themselves but also of

smallholder farmers and MSMEs at Growth Points and Rural Business Centres who

are now able to access working capital finance.

6.16 Microfinance institutions have partnered with other providers of financial services

and mobile finance to ensure that households in remote locations can benefit from

financial services including remittances and payment services at greatly reduced

transaction costs and in time to meet a range of financial obligations.

6.17 The implementation of the NFIS is expected to result in the roll out of micro-insurance

services including crop and livestock insurance, weather index insurance and micro-

health insurance to the rural communities.

CHAPTER 7 OUTLOOK

7.1 The microfinance industry is poised for further growth through the implementation of

the National Financial Inclusion Strategy (NFIS) which was launched on 11 March 2016.

Microfinance, as one of the key pillars of NFIS, is expected to drive the national

inclusion agenda.

7.2 Going forward, the roll out of the NFIS will see increased focus by stakeholders in the

provision of formal financial services to the unbanked segments of society through

delivery channels such as agent banking.

7.3 The Reserve Bank will continue to enhance the regulatory environment to ensure that

the legal framework is supportive of financial inclusion initiatives including mobile

technological innovation and agent banking.

Credit Growth…

7.4 The re-engagement of the international community by the Government of Zimbabwe

coupled with a raft of macro-economic reforms is expected to improve the general

macro-economic environment in Zimbabwe. The resultant effect will see improved

inflows in foreign investments and off-shore lines of credit which is expected to spur

credit growth in the sector.

7.5 The establishment of deposit-taking microfinance institutions is expected to further

boost credit growth in the microfinance sector through mobilization of savings

deposits.

7.6 Measures put in place to resolve non-performing loans in the main stream banking

sector which include setting up a credit reference system and collateral registry are

expected to spur micro-credit growth and enhance credit risk management.

Risk Management…

7.7 In view of capacity building initiatives by the Reserve Bank and other stakeholders,

microfinance institutions are envisaged to implement prudent risk management

systems to improve loan portfolio quality.

Financial Inclusion…

7.8 The microfinance sector is expected to play a

pivotal role in achieving financial inclusion

through extension of credit for productive

purposes and other financial services such as

micro-leasing, micro-insurance, savings and

agricultural loans for small scale farmers.

7.9 The Reserve Bank, in collaboration with other key

stakeholders such as microfinance practitioners, mobile network operators and

Government will continue to explore ways of promoting sustainable financial

inclusion.

7.10 Financial inclusion initiatives are expected to be boosted by the entrance of more

deposit-taking microfinance institutions in the market which in turn promotes the

deepening of financial markets.

Technology and Innovation in Microfinance…

7.11 The adoption of mobile technology, which had a

transformative impact on the banking sector in

the past years is expected to transcend to the

microfinance sector.

7.12 From allowing MFIs to access micro-entrepreneurs in remote areas to enabling the

implementation of more robust ICT and risk assessment tools, technology represents

a huge opportunity for microfinance institutions in Zimbabwe.

7.13 Technology is expected to play an important role in building and managing large loan

portfolios which are typical for MFIs, and help in adopting efficient delivery channels

and putting in place robust MIS. The microfinance sector is expected to gradually

embrace technology and become a technology driven industry.

7.14 Efforts by the umbrella body, ZAMFI to ensure microfinance institutions acquire

affordable information technology systems are expected to gather pace in the next

twelve months.

Compliance…

7.15 Regulatory compliance levels are expected to improve in the sector following Reserve

Bank efforts to enforce compliance and the microfinance institutions embracing the

microfinance code of conduct.

Consumer Protection and Financial Literacy Programmes…

7.16 In view of the target market served by microfinance institutions, the adoption of

sound pro-consumer principles and practices is expected to buttress public confidence

in the financial system as well as stimulating healthy competition and responsible

pricing amongst the players in the sector.

7.17 The rolling out of a consumer protection framework for the microfinance sector in the

next twelve (12) months is a critical component for the growth of an inclusive financial

system in Zimbabwe.

7.18 In view of the anticipated growth in microfinance in the coming year, the need for

financial literacy becomes paramount. The challenge is more pronounced among MFI

clients who are poor and have limited experience and interaction with the formal

financial sector. Microfinance institutions are expected to spearhead use of a variety

of channels to deliver financial literacy programmes to such clients.

7.19 The microfinance sector is envisaged to increase public awareness campaigns in rural

and urban areas, make use of mass media platforms, face-to-face communications

with clients, personal counselling on debt management and embracing of innovative

channels aimed at improving financial literacy among microfinance clients.

Financial Literacy Framework…

7.20 The Reserve Bank, in conjunction with other

stakeholders, is developing a financial

literacy framework which is aimed at

enhancing financial education among

consumers of financial services. The scope of

the financial literacy framework includes:

i. knowledge and awareness on the various types of financial products and services;

ii. knowledge and awareness on risks related to financial products;

iii. consumer protection; and

iv. financial management skill.

APPENDICES

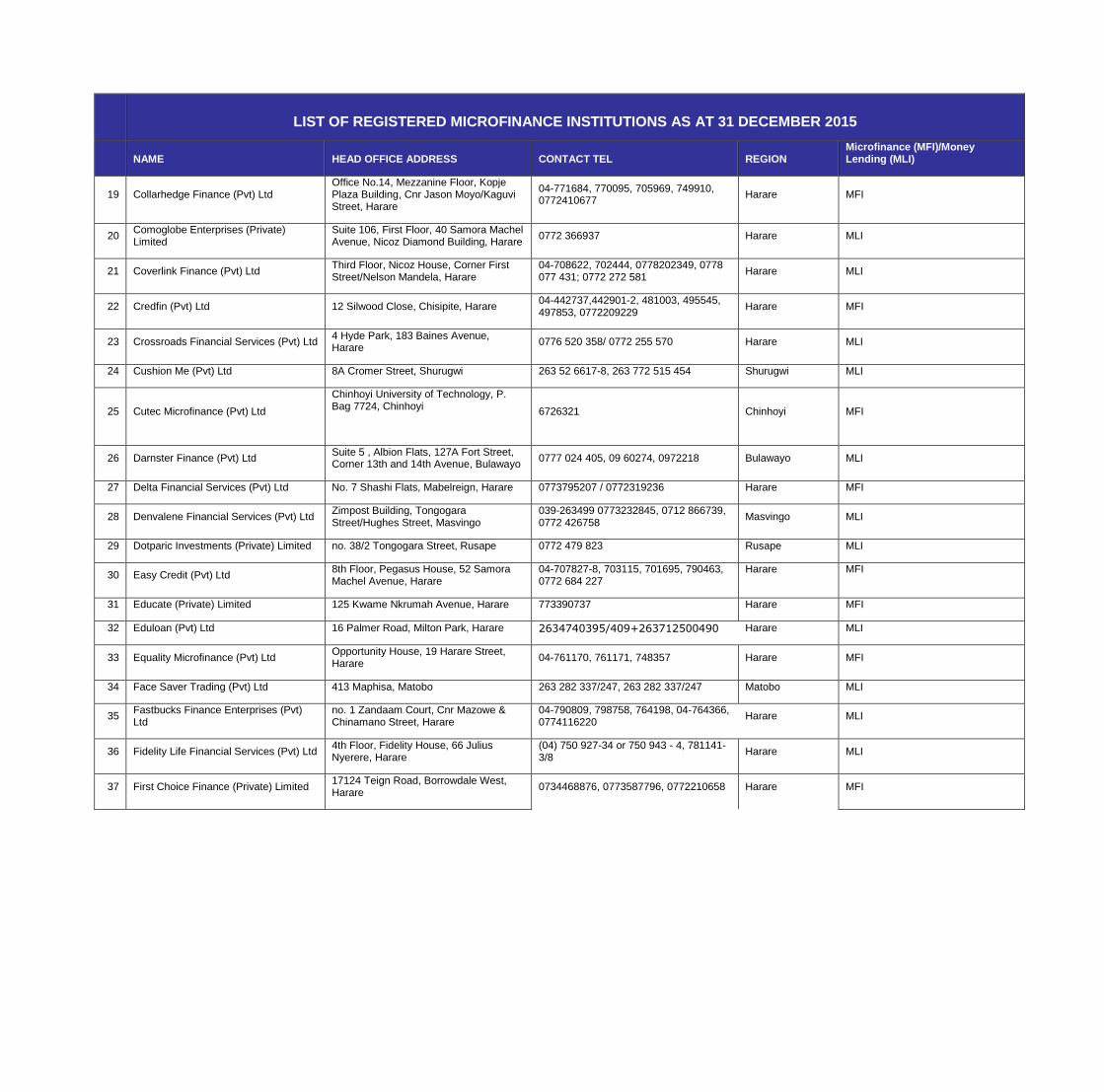

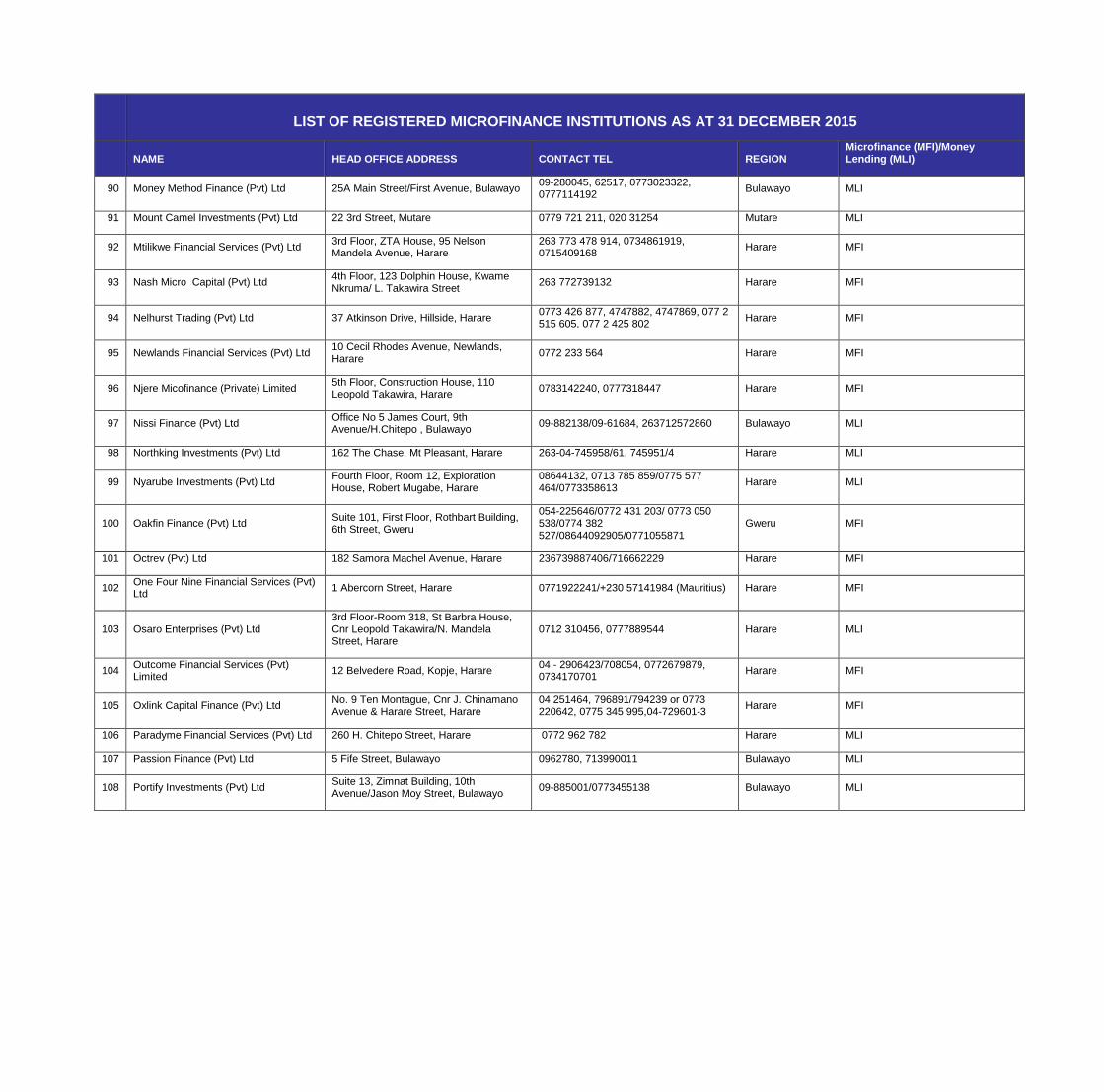

LIST OF REGISTERED MICROFINANCE INSTITUTIONS AS AT 31 DECEMBER 2015

NAME HEAD OFFICE ADDRESS CONTACT TEL REGION Microfinance (MFI)/Money Lending (MLI)

1 ABC Easy Loans t/a BancEasy Loans (Private) Ltd

4th Floor, Heritage House, 67 Samora Machel Avenue, Harare

781046-7, 781715-7, 780270/7 Harare MFI

2 ABC Moneylenders (Pvt) Ltd Hatfield House, Seke Road, Graniteside, Harare

04-751904/751906 Harare MLI

3 African Century (Pvt) Limited African Century Gardens, 153 Josiah Chinamano Avenue, Harare

04-705503, 341 Harare Deposit- Taking MFI

4 Airmode Investments (Pvt) Ltd 9 Essex Avenue, Fitchlea, Kwekwe 055 25100, 0771 966 664, 0778 508 161 Kwekwe MLI

5 Aquapave Investments (Pvt) Ltd 135 Kwame Nkrumah Ave, Harare 772722029 Harare MLI

6 ANF Microfinance (Pvt) Ltd Block 2, Office 12, Longchen Plaza, Harare

778005293, 08644004199 Harare MFI

7 Ashlene Investments (Private) Limited 3rd Floor, West Wing, Construction House, 108-110 Leopold Takawira Street, Harare

04-793202/9, 8644058493-4 Harare MLI

8 Baardy Micro Capital (Pvt) Ltd Office 400, 4th Floor, Conctruction House, 108-110 Leopold Takawira Street, Harare

0772-550189, 777254 Harare MLI

9 Transport & Equpment Finance Company (Pvt) Ltd

30001 Dagenham Road, Willowvale, Harare

04-621551-5, 0772232072 Harare MFI

10 Big Grape Financial Services (Private) Limited

4 Maiden Drive, Newlands, Harare 04-781007-8, 0735495239 Harare MFI

11 Bizlink Finance (Pvt) Ltd 6th Floor, Bard House, 69 S. Machel Avenue, Harare

772380731 Harare MLI

12 Campion Capital (Pvt) Ltd 12 Lomagundi Road, Mount Pleasant, Harare

263777 010185, 4-302819/20, 253793 Harare MLI

13 Cablefin Finance (Pvt) Ltd No. 1 Armagh Avenue, Eastlea, Harare 04-782872/869/0772295077/0777 657 558

Harare MLI

14 Cash Connect Finance (Pvt) Ltd Suite 7, Third Floor, Mass Media House, 19 Selous Avenue, Harare

774452856, 797245 Harare MFI

15 Cash Dial Finance (Pvt) Ltd 48 Joshua Nkomo Street, Bulawayo 0776760080, 09230104 MLI

16 Cash Twentyfour (Pvt) Ltd Jalyd House, 87 Chinhoyi Street, Harare 0773055016, 0772283761 Harare MFI

17 Clarion Financial Services (Private) Limited

7 Bates Street, Milton Park, Harare 731002013 Harare MFI

18 Credit Plus Loans (Pvt) Ltd Stand No 411/2, Office No. 3 New Market Centre, R. Mugabe St, Masvingo

263 773 249 825 Masvingo MLI

LIST OF REGISTERED MICROFINANCE INSTITUTIONS AS AT 31 DECEMBER 2015

NAME HEAD OFFICE ADDRESS CONTACT TEL REGION Microfinance (MFI)/Money Lending (MLI)

19 Collarhedge Finance (Pvt) Ltd Office No.14, Mezzanine Floor, Kopje Plaza Building, Cnr Jason Moyo/Kaguvi Street, Harare

04-771684, 770095, 705969, 749910, 0772410677

Harare MFI

20 Comoglobe Enterprises (Private) Limited

Suite 106, First Floor, 40 Samora Machel Avenue, Nicoz Diamond Building, Harare

0772 366937 Harare MLI

21 Coverlink Finance (Pvt) Ltd Third Floor, Nicoz House, Corner First Street/Nelson Mandela, Harare

04-708622, 702444, 0778202349, 0778 077 431; 0772 272 581

Harare MLI

22 Credfin (Pvt) Ltd 12 Silwood Close, Chisipite, Harare 04-442737,442901-2, 481003, 495545, 497853, 0772209229

Harare MFI

23 Crossroads Financial Services (Pvt) Ltd 4 Hyde Park, 183 Baines Avenue, Harare

0776 520 358/ 0772 255 570 Harare MLI

24 Cushion Me (Pvt) Ltd 8A Cromer Street, Shurugwi 263 52 6617-8, 263 772 515 454 Shurugwi MLI

25 Cutec Microfinance (Pvt) Ltd

Chinhoyi University of Technology, P. Bag 7724, Chinhoyi

6726321 Chinhoyi MFI

26 Darnster Finance (Pvt) Ltd Suite 5 , Albion Flats, 127A Fort Street, Corner 13th and 14th Avenue, Bulawayo

0777 024 405, 09 60274, 0972218 Bulawayo MLI

27 Delta Financial Services (Pvt) Ltd No. 7 Shashi Flats, Mabelreign, Harare 0773795207 / 0772319236 Harare MFI

28 Denvalene Financial Services (Pvt) Ltd Zimpost Building, Tongogara Street/Hughes Street, Masvingo

039-263499 0773232845, 0712 866739, 0772 426758

Masvingo MLI

29 Dotparic Investments (Private) Limited no. 38/2 Tongogara Street, Rusape 0772 479 823 Rusape MLI

30 Easy Credit (Pvt) Ltd 8th Floor, Pegasus House, 52 Samora Machel Avenue, Harare

04-707827-8, 703115, 701695, 790463, 0772 684 227

Harare MFI

31 Educate (Private) Limited 125 Kwame Nkrumah Avenue, Harare 773390737 Harare MFI

32 Eduloan (Pvt) Ltd 16 Palmer Road, Milton Park, Harare 2634740395/409+263712500490 Harare MLI

33 Equality Microfinance (Pvt) Ltd Opportunity House, 19 Harare Street, Harare

04-761170, 761171, 748357 Harare MFI

34 Face Saver Trading (Pvt) Ltd 413 Maphisa, Matobo 263 282 337/247, 263 282 337/247 Matobo MLI

35 Fastbucks Finance Enterprises (Pvt) Ltd

no. 1 Zandaam Court, Cnr Mazowe & Chinamano Street, Harare

04-790809, 798758, 764198, 04-764366, 0774116220

Harare MLI

36 Fidelity Life Financial Services (Pvt) Ltd 4th Floor, Fidelity House, 66 Julius Nyerere, Harare

(04) 750 927-34 or 750 943 - 4, 781141-3/8

Harare MLI

37 First Choice Finance (Private) Limited 17124 Teign Road, Borrowdale West, Harare

0734468876, 0773587796, 0772210658 Harare MFI

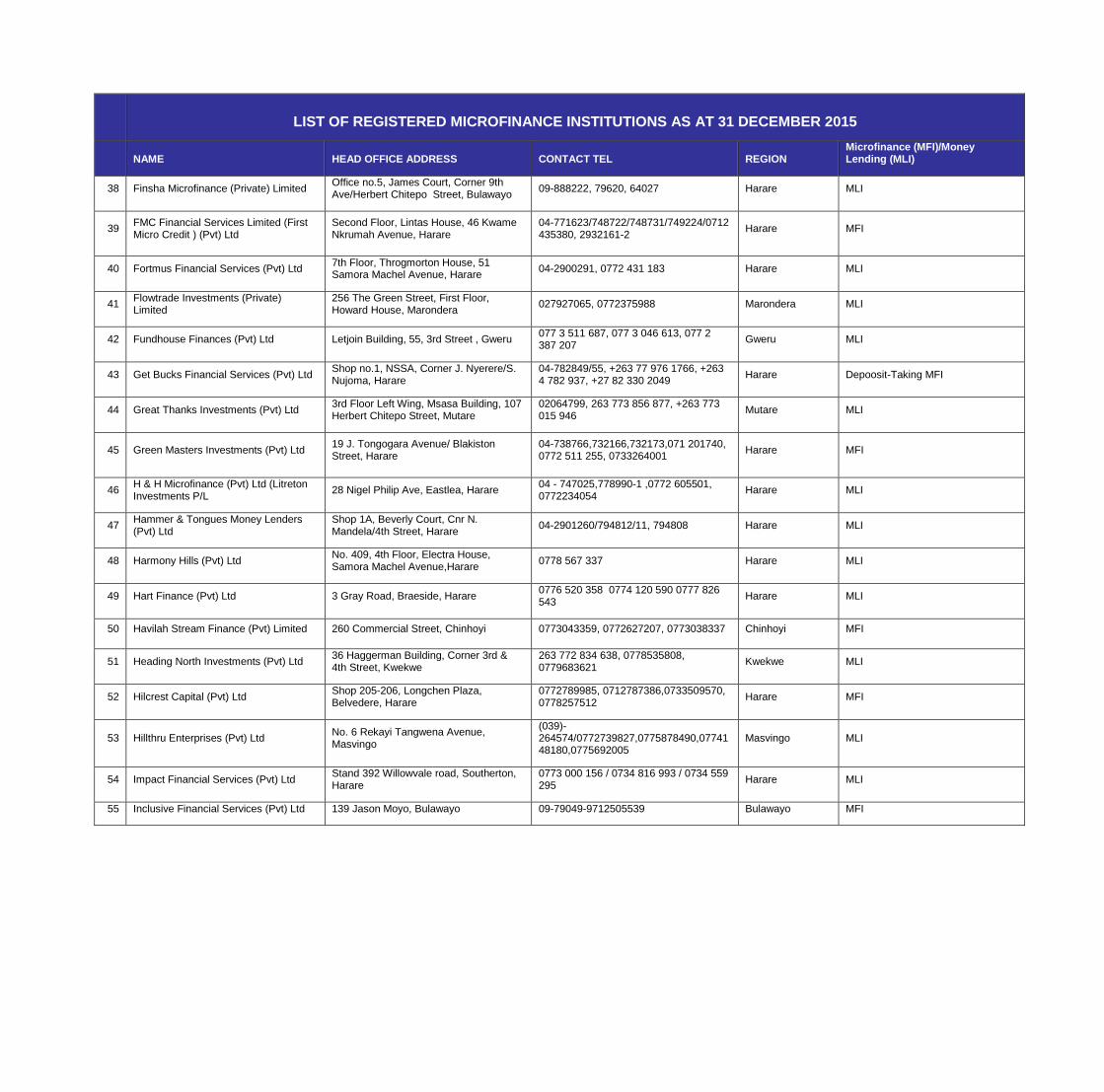

LIST OF REGISTERED MICROFINANCE INSTITUTIONS AS AT 31 DECEMBER 2015

NAME HEAD OFFICE ADDRESS CONTACT TEL REGION Microfinance (MFI)/Money Lending (MLI)

38 Finsha Microfinance (Private) Limited Office no.5, James Court, Corner 9th Ave/Herbert Chitepo Street, Bulawayo

09-888222, 79620, 64027 Harare MLI

39 FMC Financial Services Limited (First Micro Credit ) (Pvt) Ltd

Second Floor, Lintas House, 46 Kwame Nkrumah Avenue, Harare

04-771623/748722/748731/749224/0712 435380, 2932161-2

Harare MFI

40 Fortmus Financial Services (Pvt) Ltd 7th Floor, Throgmorton House, 51 Samora Machel Avenue, Harare

04-2900291, 0772 431 183 Harare MLI

41 Flowtrade Investments (Private) Limited

256 The Green Street, First Floor, Howard House, Marondera

027927065, 0772375988 Marondera MLI

42 Fundhouse Finances (Pvt) Ltd Letjoin Building, 55, 3rd Street , Gweru 077 3 511 687, 077 3 046 613, 077 2 387 207

Gweru MLI

43 Get Bucks Financial Services (Pvt) Ltd Shop no.1, NSSA, Corner J. Nyerere/S. Nujoma, Harare

04-782849/55, +263 77 976 1766, +263 4 782 937, +27 82 330 2049

Harare Depoosit-Taking MFI

44 Great Thanks Investments (Pvt) Ltd 3rd Floor Left Wing, Msasa Building, 107 Herbert Chitepo Street, Mutare

02064799, 263 773 856 877, +263 773 015 946

Mutare MLI

45 Green Masters Investments (Pvt) Ltd 19 J. Tongogara Avenue/ Blakiston Street, Harare

04-738766,732166,732173,071 201740, 0772 511 255, 0733264001

Harare MFI

46 H & H Microfinance (Pvt) Ltd (Litreton Investments P/L

28 Nigel Philip Ave, Eastlea, Harare 04 - 747025,778990-1 ,0772 605501, 0772234054

Harare MLI

47 Hammer & Tongues Money Lenders (Pvt) Ltd

Shop 1A, Beverly Court, Cnr N. Mandela/4th Street, Harare

04-2901260/794812/11, 794808 Harare MLI

48 Harmony Hills (Pvt) Ltd No. 409, 4th Floor, Electra House, Samora Machel Avenue,Harare

0778 567 337 Harare MLI

49 Hart Finance (Pvt) Ltd 3 Gray Road, Braeside, Harare 0776 520 358 0774 120 590 0777 826 543

Harare MLI

50 Havilah Stream Finance (Pvt) Limited 260 Commercial Street, Chinhoyi 0773043359, 0772627207, 0773038337 Chinhoyi MFI

51 Heading North Investments (Pvt) Ltd 36 Haggerman Building, Corner 3rd & 4th Street, Kwekwe

263 772 834 638, 0778535808, 0779683621

Kwekwe MLI

52 Hilcrest Capital (Pvt) Ltd Shop 205-206, Longchen Plaza, Belvedere, Harare

0772789985, 0712787386,0733509570, 0778257512

Harare MFI

53 Hillthru Enterprises (Pvt) Ltd No. 6 Rekayi Tangwena Avenue, Masvingo

(039)-264574/0772739827,0775878490,0774148180,0775692005

Masvingo MLI

54 Impact Financial Services (Pvt) Ltd Stand 392 Willowvale road, Southerton, Harare

0773 000 156 / 0734 816 993 / 0734 559 295

Harare MLI

55 Inclusive Financial Services (Pvt) Ltd 139 Jason Moyo, Bulawayo 09-79049-9712505539 Bulawayo MFI

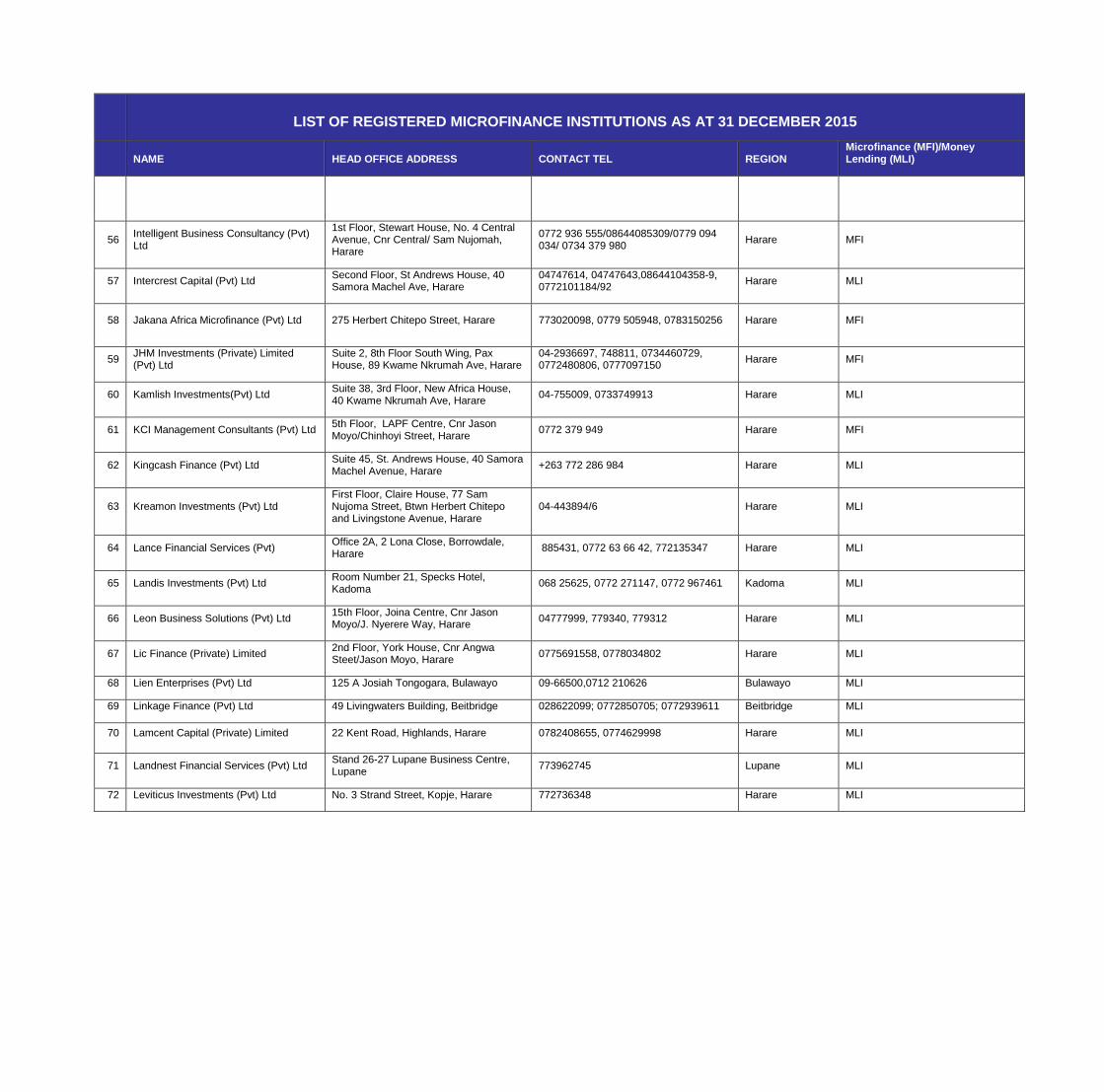

LIST OF REGISTERED MICROFINANCE INSTITUTIONS AS AT 31 DECEMBER 2015

NAME HEAD OFFICE ADDRESS CONTACT TEL REGION Microfinance (MFI)/Money Lending (MLI)

56 Intelligent Business Consultancy (Pvt) Ltd

1st Floor, Stewart House, No. 4 Central Avenue, Cnr Central/ Sam Nujomah, Harare

0772 936 555/08644085309/0779 094 034/ 0734 379 980

Harare MFI

57 Intercrest Capital (Pvt) Ltd Second Floor, St Andrews House, 40 Samora Machel Ave, Harare

04747614, 04747643,08644104358-9, 0772101184/92

Harare MLI

58 Jakana Africa Microfinance (Pvt) Ltd 275 Herbert Chitepo Street, Harare 773020098, 0779 505948, 0783150256 Harare MFI

59 JHM Investments (Private) Limited (Pvt) Ltd

Suite 2, 8th Floor South Wing, Pax House, 89 Kwame Nkrumah Ave, Harare

04-2936697, 748811, 0734460729, 0772480806, 0777097150

Harare MFI

60 Kamlish Investments(Pvt) Ltd Suite 38, 3rd Floor, New Africa House, 40 Kwame Nkrumah Ave, Harare

04-755009, 0733749913 Harare MLI

61 KCI Management Consultants (Pvt) Ltd 5th Floor, LAPF Centre, Cnr Jason Moyo/Chinhoyi Street, Harare

0772 379 949 Harare MFI

62 Kingcash Finance (Pvt) Ltd Suite 45, St. Andrews House, 40 Samora Machel Avenue, Harare

+263 772 286 984 Harare MLI

63 Kreamon Investments (Pvt) Ltd First Floor, Claire House, 77 Sam Nujoma Street, Btwn Herbert Chitepo and Livingstone Avenue, Harare

04-443894/6 Harare MLI

64 Lance Financial Services (Pvt) Office 2A, 2 Lona Close, Borrowdale, Harare

885431, 0772 63 66 42, 772135347 Harare MLI

65 Landis Investments (Pvt) Ltd Room Number 21, Specks Hotel, Kadoma

068 25625, 0772 271147, 0772 967461 Kadoma MLI

66 Leon Business Solutions (Pvt) Ltd 15th Floor, Joina Centre, Cnr Jason Moyo/J. Nyerere Way, Harare

04777999, 779340, 779312 Harare MLI

67 Lic Finance (Private) Limited 2nd Floor, York House, Cnr Angwa Steet/Jason Moyo, Harare

0775691558, 0778034802 Harare MLI

68 Lien Enterprises (Pvt) Ltd 125 A Josiah Tongogara, Bulawayo 09-66500,0712 210626 Bulawayo MLI

69 Linkage Finance (Pvt) Ltd 49 Livingwaters Building, Beitbridge 028622099; 0772850705; 0772939611 Beitbridge MLI

70 Lamcent Capital (Private) Limited 22 Kent Road, Highlands, Harare 0782408655, 0774629998 Harare MLI

71 Landnest Financial Services (Pvt) Ltd Stand 26-27 Lupane Business Centre, Lupane

773962745 Lupane MLI

72 Leviticus Investments (Pvt) Ltd No. 3 Strand Street, Kopje, Harare 772736348 Harare MLI

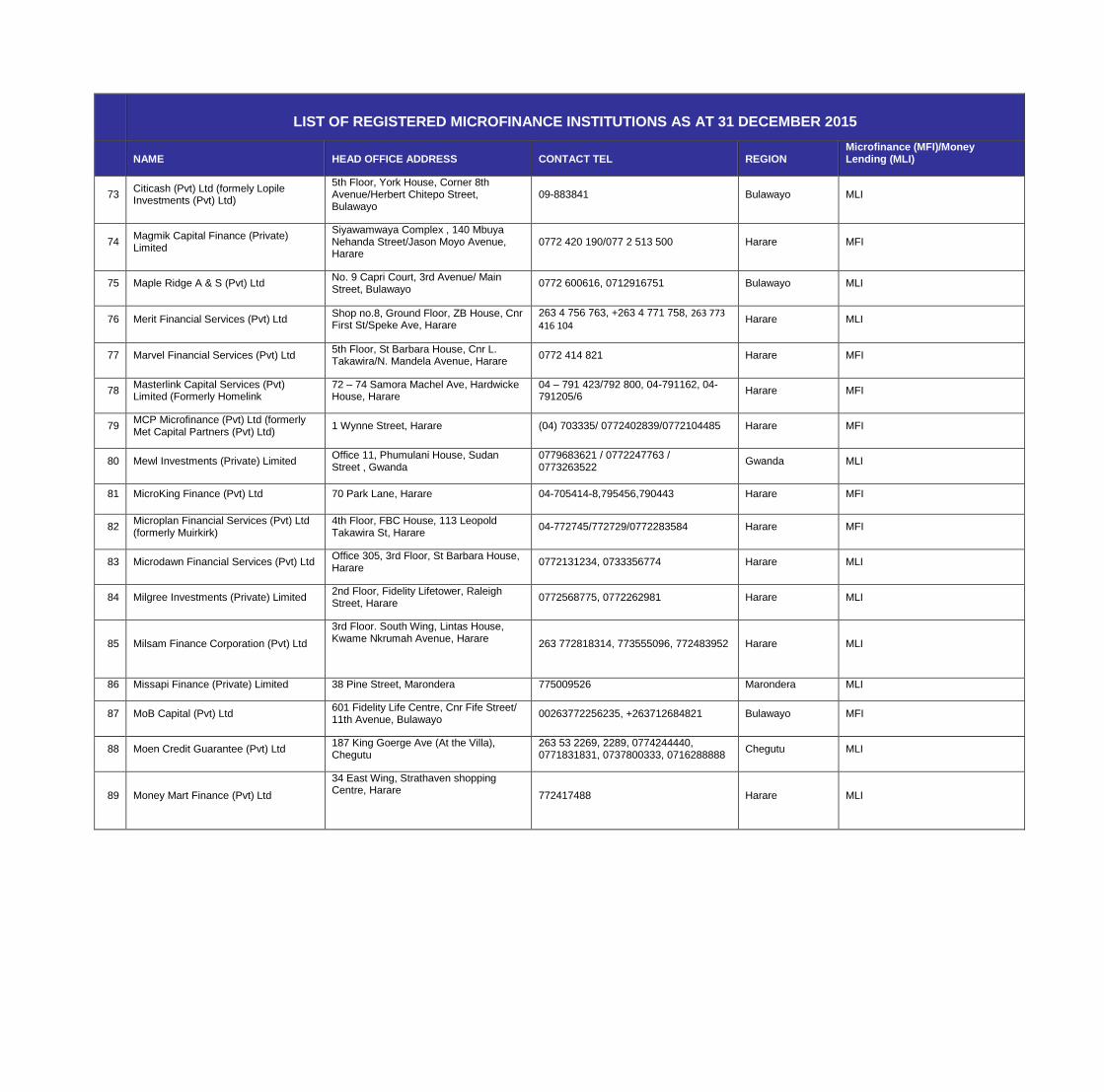

LIST OF REGISTERED MICROFINANCE INSTITUTIONS AS AT 31 DECEMBER 2015

NAME HEAD OFFICE ADDRESS CONTACT TEL REGION Microfinance (MFI)/Money Lending (MLI)

73 Citicash (Pvt) Ltd (formely Lopile Investments (Pvt) Ltd)

5th Floor, York House, Corner 8th Avenue/Herbert Chitepo Street, Bulawayo

09-883841 Bulawayo MLI

74 Magmik Capital Finance (Private) Limited

Siyawamwaya Complex , 140 Mbuya Nehanda Street/Jason Moyo Avenue, Harare

0772 420 190/077 2 513 500 Harare MFI

75 Maple Ridge A & S (Pvt) Ltd No. 9 Capri Court, 3rd Avenue/ Main Street, Bulawayo

0772 600616, 0712916751 Bulawayo MLI

76 Merit Financial Services (Pvt) Ltd Shop no.8, Ground Floor, ZB House, Cnr First St/Speke Ave, Harare

263 4 756 763, +263 4 771 758, 263 773 416 104

Harare MLI

77 Marvel Financial Services (Pvt) Ltd 5th Floor, St Barbara House, Cnr L. Takawira/N. Mandela Avenue, Harare

0772 414 821 Harare MFI

78 Masterlink Capital Services (Pvt) Limited (Formerly Homelink

72 – 74 Samora Machel Ave, Hardwicke House, Harare

04 – 791 423/792 800, 04-791162, 04-791205/6

Harare MFI

79 MCP Microfinance (Pvt) Ltd (formerly Met Capital Partners (Pvt) Ltd)

1 Wynne Street, Harare (04) 703335/ 0772402839/0772104485 Harare MFI

80 Mewl Investments (Private) Limited Office 11, Phumulani House, Sudan Street , Gwanda

0779683621 / 0772247763 / 0773263522

Gwanda MLI

81 MicroKing Finance (Pvt) Ltd 70 Park Lane, Harare 04-705414-8,795456,790443 Harare MFI

82 Microplan Financial Services (Pvt) Ltd (formerly Muirkirk)

4th Floor, FBC House, 113 Leopold Takawira St, Harare

04-772745/772729/0772283584 Harare MFI

83 Microdawn Financial Services (Pvt) Ltd Office 305, 3rd Floor, St Barbara House, Harare

0772131234, 0733356774 Harare MLI

84 Milgree Investments (Private) Limited 2nd Floor, Fidelity Lifetower, Raleigh Street, Harare

0772568775, 0772262981 Harare MLI

85 Milsam Finance Corporation (Pvt) Ltd

3rd Floor. South Wing, Lintas House, Kwame Nkrumah Avenue, Harare

263 772818314, 773555096, 772483952 Harare MLI

86 Missapi Finance (Private) Limited 38 Pine Street, Marondera 775009526 Marondera MLI

87 MoB Capital (Pvt) Ltd 601 Fidelity Life Centre, Cnr Fife Street/ 11th Avenue, Bulawayo

00263772256235, +263712684821 Bulawayo MFI

88 Moen Credit Guarantee (Pvt) Ltd 187 King Goerge Ave (At the Villa), Chegutu

263 53 2269, 2289, 0774244440, 0771831831, 0737800333, 0716288888

Chegutu MLI

89 Money Mart Finance (Pvt) Ltd

34 East Wing, Strathaven shopping Centre, Harare

772417488 Harare MLI

LIST OF REGISTERED MICROFINANCE INSTITUTIONS AS AT 31 DECEMBER 2015

NAME HEAD OFFICE ADDRESS CONTACT TEL REGION Microfinance (MFI)/Money Lending (MLI)

90 Money Method Finance (Pvt) Ltd 25A Main Street/First Avenue, Bulawayo 09-280045, 62517, 0773023322, 0777114192

Bulawayo MLI

91 Mount Camel Investments (Pvt) Ltd 22 3rd Street, Mutare 0779 721 211, 020 31254 Mutare MLI

92 Mtilikwe Financial Services (Pvt) Ltd 3rd Floor, ZTA House, 95 Nelson Mandela Avenue, Harare

263 773 478 914, 0734861919, 0715409168

Harare MFI

93 Nash Micro Capital (Pvt) Ltd 4th Floor, 123 Dolphin House, Kwame Nkruma/ L. Takawira Street

263 772739132 Harare MFI

94 Nelhurst Trading (Pvt) Ltd 37 Atkinson Drive, Hillside, Harare 0773 426 877, 4747882, 4747869, 077 2 515 605, 077 2 425 802

Harare MFI

95 Newlands Financial Services (Pvt) Ltd 10 Cecil Rhodes Avenue, Newlands, Harare

0772 233 564 Harare MFI

96 Njere Micofinance (Private) Limited 5th Floor, Construction House, 110 Leopold Takawira, Harare

0783142240, 0777318447 Harare MFI

97 Nissi Finance (Pvt) Ltd Office No 5 James Court, 9th Avenue/H.Chitepo , Bulawayo

09-882138/09-61684, 263712572860 Bulawayo MLI

98 Northking Investments (Pvt) Ltd 162 The Chase, Mt Pleasant, Harare 263-04-745958/61, 745951/4 Harare MLI

99 Nyarube Investments (Pvt) Ltd Fourth Floor, Room 12, Exploration House, Robert Mugabe, Harare

08644132, 0713 785 859/0775 577 464/0773358613

Harare MLI

100 Oakfin Finance (Pvt) Ltd Suite 101, First Floor, Rothbart Building, 6th Street, Gweru

054-225646/0772 431 203/ 0773 050 538/0774 382 527/08644092905/0771055871

Gweru MFI

101 Octrev (Pvt) Ltd 182 Samora Machel Avenue, Harare 236739887406/716662229 Harare MFI

102 One Four Nine Financial Services (Pvt) Ltd

1 Abercorn Street, Harare 0771922241/+230 57141984 (Mauritius) Harare MFI

103 Osaro Enterprises (Pvt) Ltd 3rd Floor-Room 318, St Barbra House, Cnr Leopold Takawira/N. Mandela Street, Harare

0712 310456, 0777889544 Harare MLI

104 Outcome Financial Services (Pvt) Limited

12 Belvedere Road, Kopje, Harare 04 - 2906423/708054, 0772679879, 0734170701

Harare MFI

105 Oxlink Capital Finance (Pvt) Ltd No. 9 Ten Montague, Cnr J. Chinamano Avenue & Harare Street, Harare

04 251464, 796891/794239 or 0773 220642, 0775 345 995,04-729601-3

Harare MFI

106 Paradyme Financial Services (Pvt) Ltd 260 H. Chitepo Street, Harare 0772 962 782 Harare MLI

107 Passion Finance (Pvt) Ltd 5 Fife Street, Bulawayo 0962780, 713990011 Bulawayo MLI

108 Portify Investments (Pvt) Ltd Suite 13, Zimnat Building, 10th Avenue/Jason Moy Street, Bulawayo

09-885001/0773455138 Bulawayo MLI

LIST OF REGISTERED MICROFINANCE INSTITUTIONS AS AT 31 DECEMBER 2015

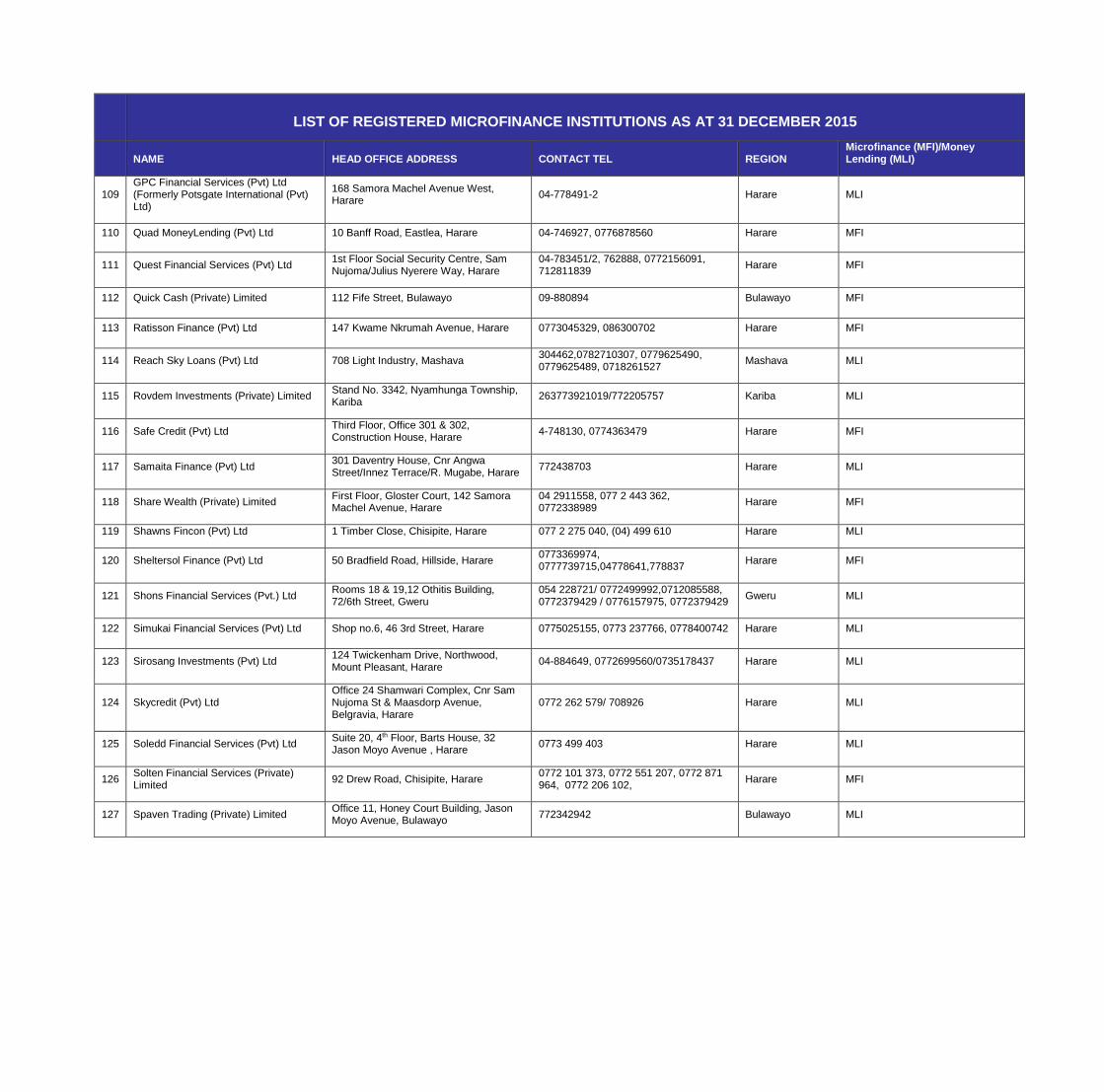

NAME HEAD OFFICE ADDRESS CONTACT TEL REGION Microfinance (MFI)/Money Lending (MLI)

109 GPC Financial Services (Pvt) Ltd (Formerly Potsgate International (Pvt) Ltd)

168 Samora Machel Avenue West, Harare

04-778491-2 Harare MLI

110 Quad MoneyLending (Pvt) Ltd 10 Banff Road, Eastlea, Harare 04-746927, 0776878560 Harare MFI

111 Quest Financial Services (Pvt) Ltd 1st Floor Social Security Centre, Sam Nujoma/Julius Nyerere Way, Harare

04-783451/2, 762888, 0772156091, 712811839

Harare MFI

112 Quick Cash (Private) Limited 112 Fife Street, Bulawayo 09-880894 Bulawayo MFI

113 Ratisson Finance (Pvt) Ltd 147 Kwame Nkrumah Avenue, Harare 0773045329, 086300702 Harare MFI

114 Reach Sky Loans (Pvt) Ltd 708 Light Industry, Mashava 304462,0782710307, 0779625490, 0779625489, 0718261527

Mashava MLI

115 Rovdem Investments (Private) Limited Stand No. 3342, Nyamhunga Township, Kariba

263773921019/772205757 Kariba MLI

116 Safe Credit (Pvt) Ltd Third Floor, Office 301 & 302, Construction House, Harare

4-748130, 0774363479 Harare MFI

117 Samaita Finance (Pvt) Ltd 301 Daventry House, Cnr Angwa Street/Innez Terrace/R. Mugabe, Harare

772438703 Harare MLI

118 Share Wealth (Private) Limited First Floor, Gloster Court, 142 Samora Machel Avenue, Harare

04 2911558, 077 2 443 362, 0772338989

Harare MFI

119 Shawns Fincon (Pvt) Ltd 1 Timber Close, Chisipite, Harare 077 2 275 040, (04) 499 610 Harare MLI

120 Sheltersol Finance (Pvt) Ltd 50 Bradfield Road, Hillside, Harare 0773369974, 0777739715,04778641,778837

Harare MFI

121 Shons Financial Services (Pvt.) Ltd Rooms 18 & 19,12 Othitis Building, 72/6th Street, Gweru

054 228721/ 0772499992,0712085588, 0772379429 / 0776157975, 0772379429

Gweru MLI

122 Simukai Financial Services (Pvt) Ltd Shop no.6, 46 3rd Street, Harare 0775025155, 0773 237766, 0778400742 Harare MLI

123 Sirosang Investments (Pvt) Ltd 124 Twickenham Drive, Northwood, Mount Pleasant, Harare

04-884649, 0772699560/0735178437 Harare MLI

124 Skycredit (Pvt) Ltd Office 24 Shamwari Complex, Cnr Sam Nujoma St & Maasdorp Avenue, Belgravia, Harare

0772 262 579/ 708926 Harare MLI

125 Soledd Financial Services (Pvt) Ltd Suite 20, 4th Floor, Barts House, 32 Jason Moyo Avenue , Harare

0773 499 403 Harare MLI

126 Solten Financial Services (Private) Limited

92 Drew Road, Chisipite, Harare 0772 101 373, 0772 551 207, 0772 871 964, 0772 206 102,

Harare MFI

127 Spaven Trading (Private) Limited Office 11, Honey Court Building, Jason Moyo Avenue, Bulawayo

772342942 Bulawayo MLI

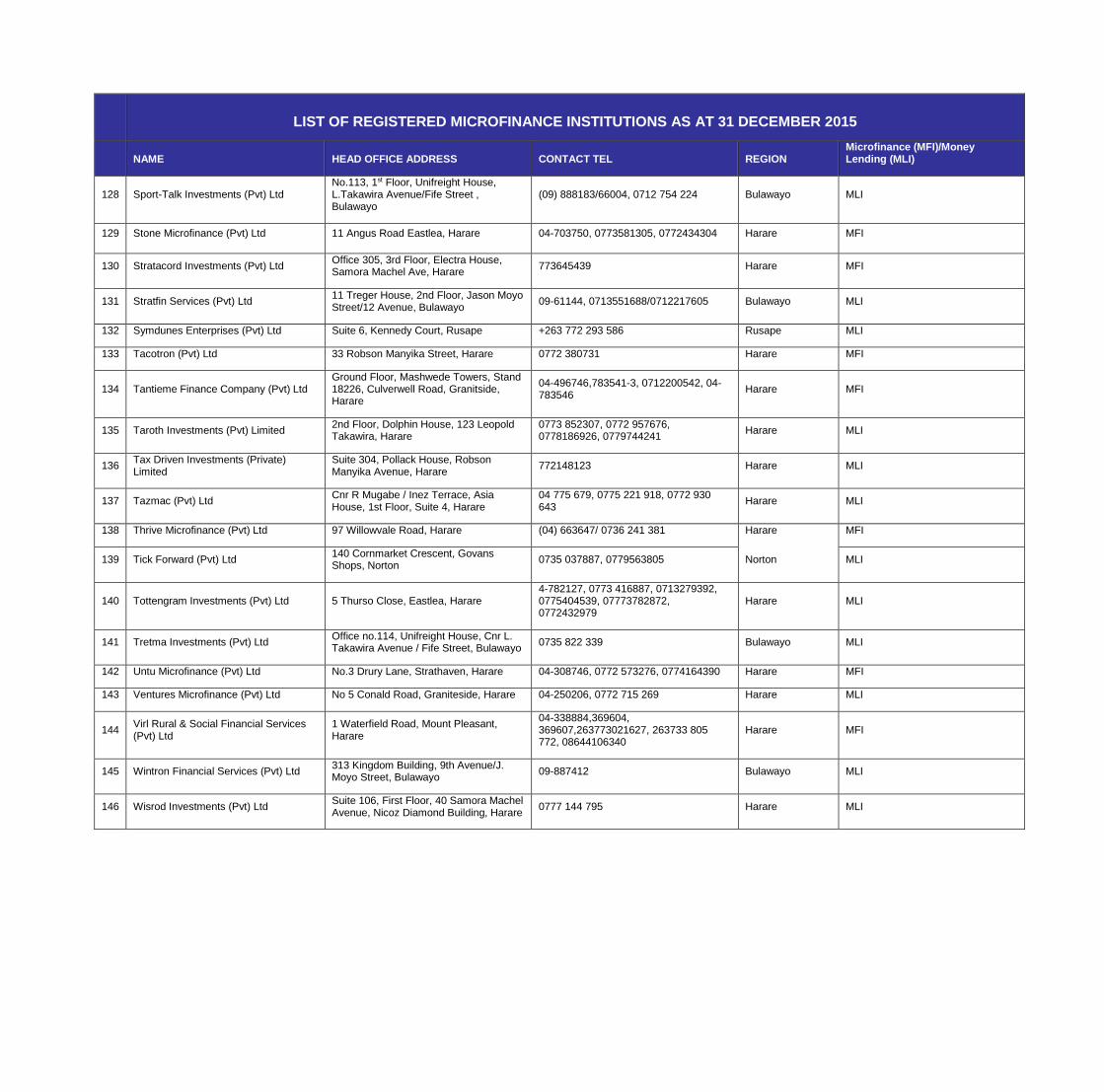

LIST OF REGISTERED MICROFINANCE INSTITUTIONS AS AT 31 DECEMBER 2015

NAME HEAD OFFICE ADDRESS CONTACT TEL REGION Microfinance (MFI)/Money Lending (MLI)

128 Sport-Talk Investments (Pvt) Ltd No.113, 1st Floor, Unifreight House, L.Takawira Avenue/Fife Street , Bulawayo

(09) 888183/66004, 0712 754 224 Bulawayo MLI

129 Stone Microfinance (Pvt) Ltd 11 Angus Road Eastlea, Harare 04-703750, 0773581305, 0772434304 Harare MFI

130 Stratacord Investments (Pvt) Ltd Office 305, 3rd Floor, Electra House, Samora Machel Ave, Harare

773645439 Harare MFI

131 Stratfin Services (Pvt) Ltd 11 Treger House, 2nd Floor, Jason Moyo Street/12 Avenue, Bulawayo

09-61144, 0713551688/0712217605 Bulawayo MLI

132 Symdunes Enterprises (Pvt) Ltd Suite 6, Kennedy Court, Rusape +263 772 293 586 Rusape MLI

133 Tacotron (Pvt) Ltd 33 Robson Manyika Street, Harare 0772 380731 Harare MFI

134 Tantieme Finance Company (Pvt) Ltd Ground Floor, Mashwede Towers, Stand 18226, Culverwell Road, Granitside, Harare

04-496746,783541-3, 0712200542, 04-783546

Harare MFI

135 Taroth Investments (Pvt) Limited 2nd Floor, Dolphin House, 123 Leopold Takawira, Harare

0773 852307, 0772 957676, 0778186926, 0779744241

Harare MLI

136 Tax Driven Investments (Private) Limited

Suite 304, Pollack House, Robson Manyika Avenue, Harare

772148123 Harare MLI

137 Tazmac (Pvt) Ltd Cnr R Mugabe / Inez Terrace, Asia House, 1st Floor, Suite 4, Harare

04 775 679, 0775 221 918, 0772 930 643

Harare MLI

138 Thrive Microfinance (Pvt) Ltd 97 Willowvale Road, Harare (04) 663647/ 0736 241 381 Harare MFI

139 Tick Forward (Pvt) Ltd 140 Cornmarket Crescent, Govans Shops, Norton

0735 037887, 0779563805 Norton MLI

140 Tottengram Investments (Pvt) Ltd 5 Thurso Close, Eastlea, Harare 4-782127, 0773 416887, 0713279392, 0775404539, 07773782872, 0772432979

Harare MLI

141 Tretma Investments (Pvt) Ltd Office no.114, Unifreight House, Cnr L. Takawira Avenue / Fife Street, Bulawayo

0735 822 339 Bulawayo MLI

142 Untu Microfinance (Pvt) Ltd No.3 Drury Lane, Strathaven, Harare 04-308746, 0772 573276, 0774164390 Harare MFI

143 Ventures Microfinance (Pvt) Ltd No 5 Conald Road, Graniteside, Harare 04-250206, 0772 715 269 Harare MLI

144 Virl Rural & Social Financial Services (Pvt) Ltd

1 Waterfield Road, Mount Pleasant, Harare

04-338884,369604, 369607,263773021627, 263733 805 772, 08644106340

Harare MFI

145 Wintron Financial Services (Pvt) Ltd 313 Kingdom Building, 9th Avenue/J. Moyo Street, Bulawayo

09-887412 Bulawayo MLI

146 Wisrod Investments (Pvt) Ltd Suite 106, First Floor, 40 Samora Machel Avenue, Nicoz Diamond Building, Harare

0777 144 795 Harare MLI

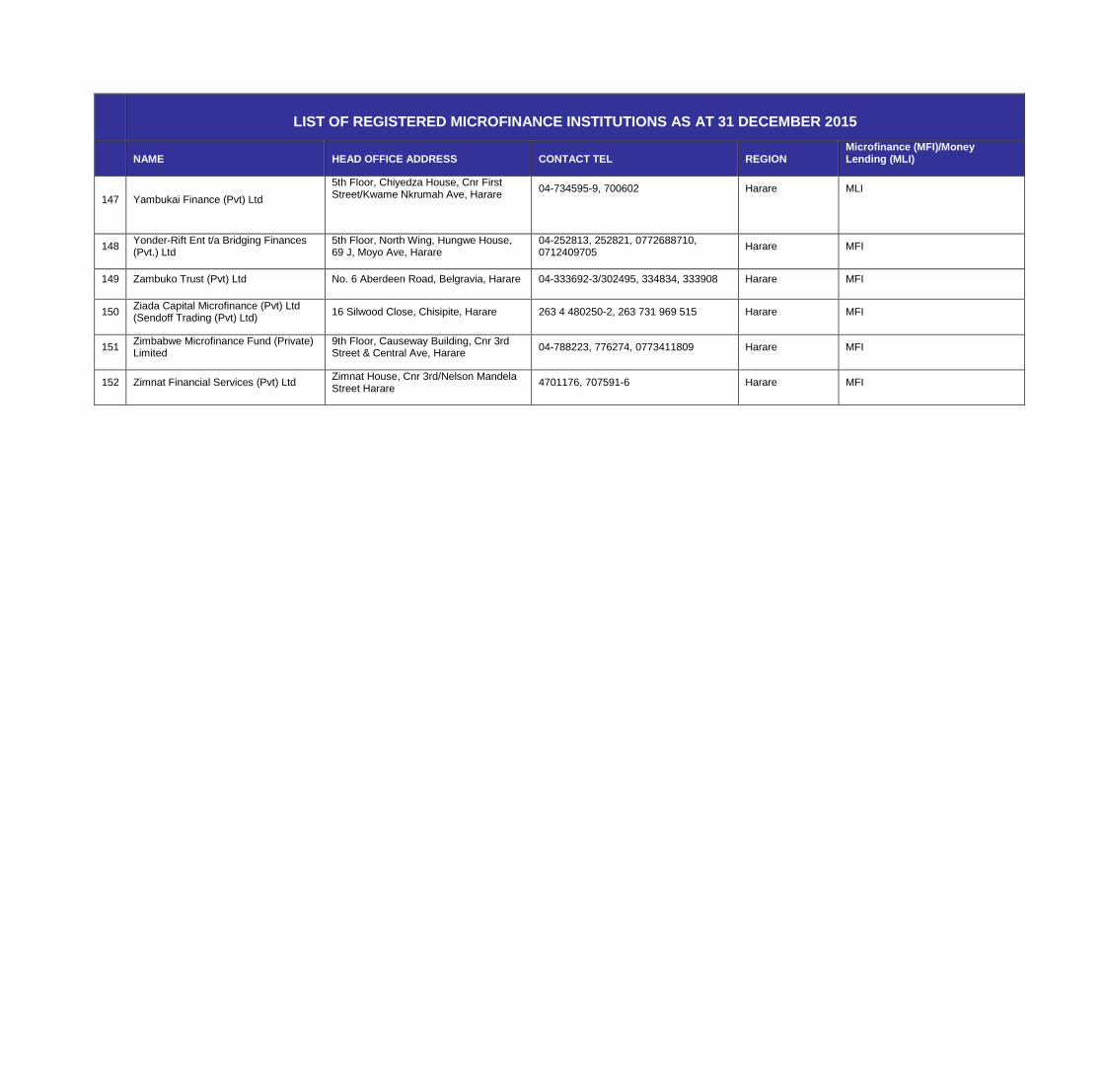

LIST OF REGISTERED MICROFINANCE INSTITUTIONS AS AT 31 DECEMBER 2015

NAME HEAD OFFICE ADDRESS CONTACT TEL REGION Microfinance (MFI)/Money Lending (MLI)

147 Yambukai Finance (Pvt) Ltd

5th Floor, Chiyedza House, Cnr First Street/Kwame Nkrumah Ave, Harare

04-734595-9, 700602

Harare

MLI

148 Yonder-Rift Ent t/a Bridging Finances (Pvt.) Ltd

5th Floor, North Wing, Hungwe House, 69 J, Moyo Ave, Harare

04-252813, 252821, 0772688710, 0712409705

Harare MFI

149 Zambuko Trust (Pvt) Ltd No. 6 Aberdeen Road, Belgravia, Harare 04-333692-3/302495, 334834, 333908 Harare MFI

150 Ziada Capital Microfinance (Pvt) Ltd (Sendoff Trading (Pvt) Ltd)

16 Silwood Close, Chisipite, Harare 263 4 480250-2, 263 731 969 515 Harare MFI

151 Zimbabwe Microfinance Fund (Private) Limited

9th Floor, Causeway Building, Cnr 3rd Street & Central Ave, Harare

04-788223, 776274, 0773411809 Harare MFI

152 Zimnat Financial Services (Pvt) Ltd Zimnat House, Cnr 3rd/Nelson Mandela Street Harare

4701176, 707591-6 Harare MFI