Embed Size (px)

Citation preview

CHAPTER -1

r\

CONSUMER DURABLE

MARKET IN RURAL INDIA

AN OVERVIEW

CHAPTER-I

CONSUMER DURABLE MARKET IN RURAL

INDIA: AN OVERVIEW

INTRODUCTION

The study on Indian rural consumer behavior is aimed at helping marketers to

get a better understanding of the Indian market place thus enabling them to embark on

selected strategies to effectively reach the Indian rural consumers. India is a big

country with 28 states, over one billion people and 120 dialects/languages. Three-

fourths of India’s population lives in rural areas, and contribute one-third of the

national income. This rural population is spread all over India.

From the market perspective, people of India comprise different segments of

consumers, based on class, status, and income. An important and recent development

in India’s consumerism is the emergence of the rural market for several basic

consumer goods. India is a lucrative market even though the per capita income is low

and it remains a huge market, even for expensive products. Among the total 164.8

million households in India, 80.7 million households comes under low income group,

followed by 50.4 million lower middle income households, 19.7 million middle

income group, 8.2 million upper middle income group and 5.8 million high income

group.

The behaviour of all consumers is not identical to that of their urban

counterparts. Behaviour is influenced by various factors like their income, social

1

groupings, and place of their origin. For understanding rural consumer counterparts,

enquiries are to be made about the concepts on what is meant by rural, what criteria

are to be considered for rural-urban differentiation, what studies demographic factors

influencing on rural market in India, how the rural consumers are classified, what

studies have been made to indicate rural market potential, what are the rural demand

and buying habits, what is the hierarchy of rural how rural and urban consumer

behaviour can be differentiated and similar issues. A humble attempt has been made

in this chapter to enquire these issues1.

1.1 MEANING OF RURAL

Rural community has some special features. First, as social interactions are

few, individuals cannot remain unknown among the society; second, division of the

labour is minimum; third, range of occupation is very small; fourth homogenous

beliefs at community level and fifth, social class is identified basically on ascribed

and personal attributes. Achieved attributes of individuals are given less prominence.

Most of the people depend on agriculture or agriculture-related activities.

Above criteria are comprehensive in nature, but all of them are not

operationally measurable. Census Authorities of India2 provides an operationally

measurable definition. Census of India3 provides data on rural and urban population in

India. But it is difficult to make an air-tight divide between the two. Rural and urban

worlds are inseparably inter-linked. “Differences between the two are believed to be

reduced due to interchange of people between the two areas through large-scale

migration, influences of urban-centered mass media, greater interdependence of rural•>

and urban economies and other types increased systematic linkage. ” However, the

2

term ‘urban’ is defined as, ‘All places with a municipality, corporation, cantonment,

or a notified town area; and All other places satisfying the following criteria:

1. Minimum Population of 5,000

2. At least 75 per cent of the male working force in non-agricultural pursuits,

3. A density of population of400 per square kilo metre (1,000 per sq. mile).

Where as, dictionary meaning of the term ‘Rural’ is agricultural and pastoral or some

thing opposite to urban. In the context of the study the meaning of the term used by

the social scientists is noteworthy. According to O.F. Larson4, Rural refers

empirically to populations living in areas of low density and to small settlements.

Rural India, during the colonial period, was more or less isolated from the

mainland civilization. The village economy is known for agrarian society. The present

villages are changing fast and no longer exist as self-sufficient republics. In spite of

the criticism against the development attained by the rural societies it must be

admitted that there has been a considerable change in them.

Traditionally, town and cities are the places where the urban population is

inhabited and ‘rural and ‘village’ is synonymously used. The Census of India does not

provide a comprehensive definition for rural areas. It classifies the regions as urban

areas based on an objective classification of the population residing in that area.

Following this, the regions, which do not belong to the urban regions, are classified as

rural areas of the country. The primary economic classification of the population is

divided into workers and non-workers. The workers are subdivided into nine

categories. All other places are considered rural. They are:

3

1. Cultivators

2. Agricultural laborers

3. In mining and quarrying, livestock, forestry, fishing and hunting, plantation,

orchards and allied activities.

4. In household industry

5. In manufacturing other than household Industry

6. In construction

7. In trade and commerce

8. In transport, storage and communication

9. In other services.

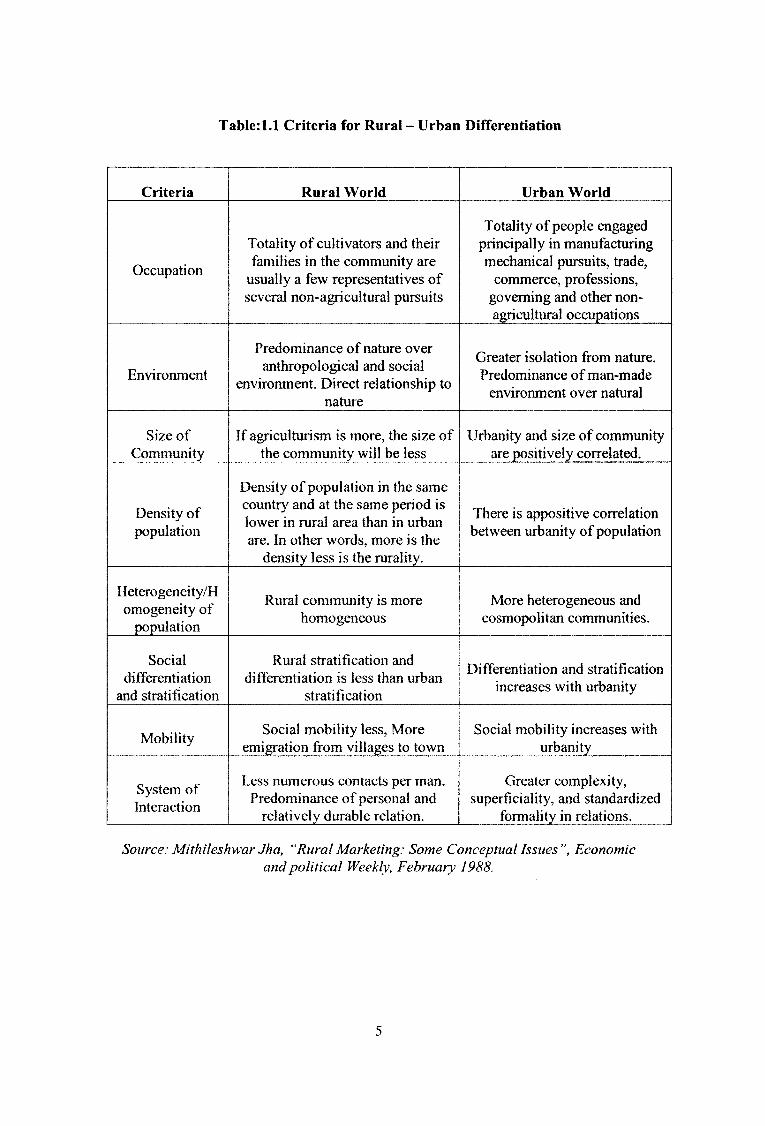

1.2 CRITERIA FOR RURAL - URBAN DIFFERENTIATION

Census of India5, inferred that the rural can be understood better by ‘other-

than-those' of urban. Sociologists distinguished rural and urban world through eight

major criteria. They are:

1. Environment

2. Density of population

3. Size of community

4. Occupation

5. Heterogeneity and Homogeneity of the population in racial and psychological traits

6. Social stratification

7. Mobility

8. Interaction system

With the help of these criteria Sorokin and Zimmerman6 have differentiated

the two. Content of their work is tabulated as follows:

4

Tableil.l Criteria for Rural - Urban Differentiation

Criteria Rural World Urban World

Occupation

Totality of cultivators and their families in the community are

usually a few representatives of several non-agricultural pursuits

Totality of people engaged principally in manufacturing mechanical pursuits, trade,

commerce, professions, governing and other non- agricultural occupations

Environment

Predominance of nature over anthropological and social

environment. Direct relationship to nature

Greater isolation from nature. Predominance of man-made

environment over natural

Size of Community

If agriculturism is more, the size of the community will be less

Urbanity and size of community are positively correlated.

Density of population

Density of population in the same country and at the same period is lower in rural area than in urban are. In other words, more is the

density less is the ruraiity.

There is appositive correlation between urbanity of population

Heterogeneity/H omogeneity of

population

Rural community is more homogeneous

More heterogeneous and cosmopolitan communities.

Socialdifferentiation

and stratification

Rural stratification and differentiation is less than urban

stratification

Differentiation and stratification increases with urbanity

Mobility Social mobility less, More emigration from villages to town

Social mobility increases with urbanity

System of Interaction

Less numerous contacts per man. Predominance of personal and

relatively durable relation.

Greater complexity, superficiality, and standardized

formality in relations.

Source: Mithileshwar Jha, “Rural Marketing: Some Conceptual Issues ”, Economic and political Weekly, February 1988.

5

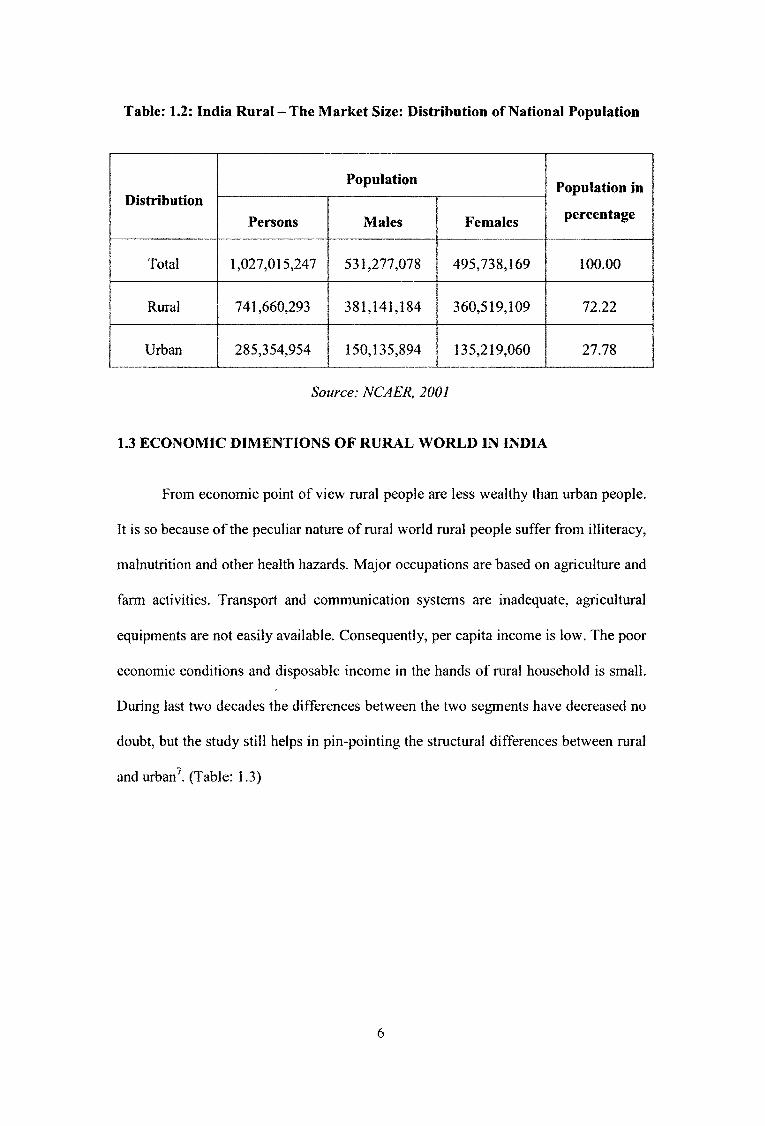

Table: 1.2: India Rural-The Market Size: Distribution of National Population

DistributionPopulation Population in

Persons Males Females percentage

Total 1,027,015,247 531,277,078 495,738,169 100.00

Rural 741,660,293 381,141,184 360,519,109 72.22

Urban 285,354,954 150,135,894 135,219,060 27.78

Source: NCAER, 2001

1.3 ECONOMIC DIMENTIONS OF RURAL WORLD IN INDIA

From economic point of view rural people are less wealthy than urban people.

It is so because of the peculiar nature of rural world rural people suffer from illiteracy,

malnutrition and other health hazards. Major occupations are based on agriculture and

farm activities. Transport and communication systems are inadequate, agricultural

equipments are not easily available. Consequently, per capita income is low. The poor

economic conditions and disposable income in the hands of rural household is small.

During last two decades the differences between the two segments have decreased no

doubt, but the study still helps in pin-pointing the structural differences between rural

and urban7. (Table: 1.3)

6

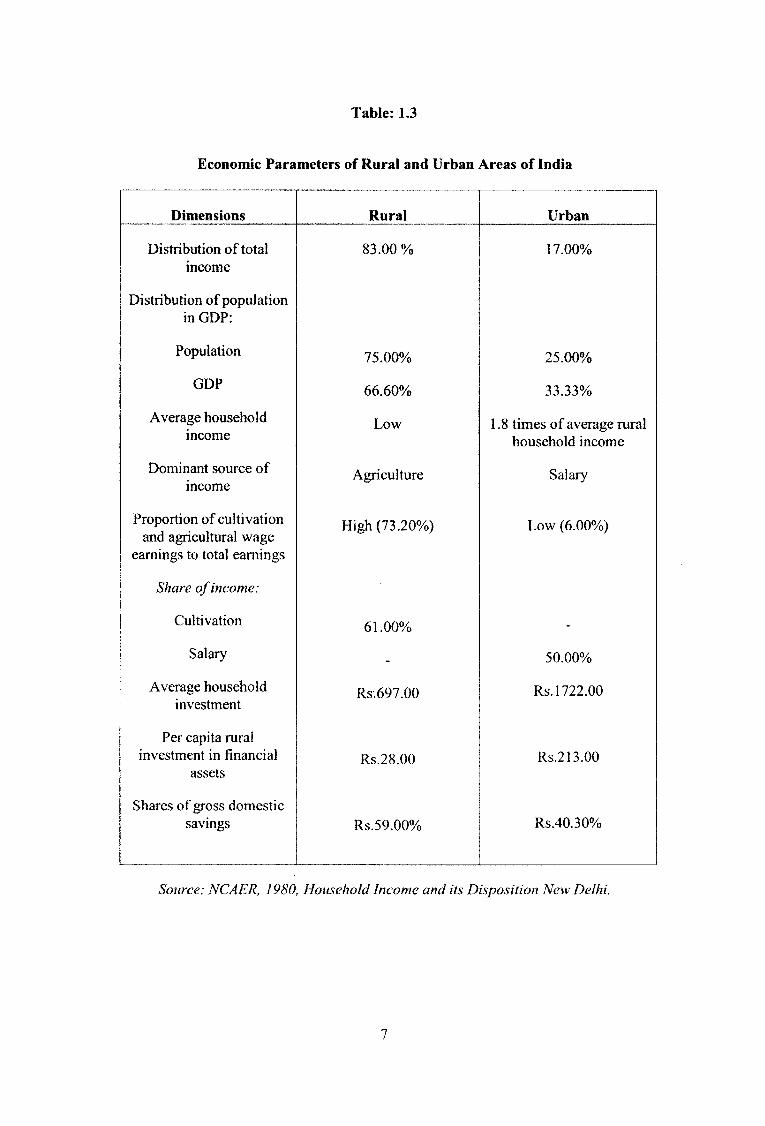

Table: 1.3

Economic Parameters of Rural and Urban Areas of India

Dimensions Rural Urban

Distribution of total 83.00 % 17.00%income

Distribution of population in GDP:

Population 75.00% 25.00%

GDP 66.60% 33.33%

Average household income

Low 1.8 times of average rural household income

Dominant source of income

Agriculture Salary

Proportion of cultivation and agricultural wage

earnings to total earnings

High (73.20%) Low (6.00%)

Share of income:

Cultivation 61.00% -Salary

- 50.00%

Average household investment

Rs',697.00 Rs. 1722.00

Per capita rural investment in financial

assetsRs.28,00 Rs.213.00

Shares of gross domestic savings Rs.59.00% Rs.40.30%

Source: NCAER, 1980, Household Income and its Disposition New Delhi.

7

1.4 RURAL MARKET

Ten years ago, foreign consumer products were scarce in India and only

available to the affluent section. Import restrictions prevented or severely hindered

foreign consumer goods from entrance to India. With the economic liberalization that

ensued, foreign brands are now prevalent across India. Today, multinational

corporations view emerging markets such as India as prime opportunities for growth.

Rural markets are growing twice as fast as the urban markets. With a rural population

equal to just less than 2.5 times the population of the entire United States as of the

2000 census, the potential consumer base is astounding8.

The success in India's rural markets for multinational corporations has been

mediocre at best. This is an opportunity for the multinational corporations seeking to

enter the rural Indian market and can learn how to do so more wisely.With excess

population of one billion people, India has caught the eye of multinational

corporations across the globe as a place of opportunity for exploring new markets.

While India has portions of their population that would be considered wealthy or

middle class by Western standards, a much greater percentage of India’s population is

still low income. As a result, they spend money, and use products differently than the

countries where most multinational corporations originate. Rural areas, in particular,

exemplify these differences9.

The concept of “Rural Market" is very broad one and it is interpreted in many

ways. In Indian context, the word ‘rural’ is so much associated with agriculture and

farmers that rural marketing tends to be seen as a marketing of inputs or outputs

related to agriculture. As the primary occupation of the rural India is agriculture or its

allied activities10.

8

According to 2001 census11 Almost three fourth of the rural population were

dependent on agriculture and its allied activities for their livelihood. With an average

income equivalent to $42 per month ($504 dollars per year), rural Indians have a very

low disposable income. Most rural homes have minimal storage space and no

refrigeration. Very few people own or have access to refrigeration facility. As a result,

rural Indian purchasing habits tend to be of an "earn today, spend today" mentality.

Rather than buying in bulk, which would mean paying more for a large quantity

upfront, rural Indians tend to buy what they need for short span of time. These factors

result in consumers buying products locally, as well as on a daily basis. In addition to

the fact that income levels are low, rural incomes also vary greatly depending on the

monsoons. When a monsoon hits, this devastates the livelihood of most rural

consumers because they are dependent on agricultural work for income. Corporations

are also directly affected because this makes it difficult to predict demand.

Rural marketing can also be identified by three distinct areas . The rural to

urban transactions deal with a wide range of products, which flow from the rural to

the urban sector. Products like oil seeds, cotton, and sugarcane, etc., and finished

products like handlooms, textiles. The rural to rural transactions limit production and

consumption within the rural area itself. Products like tools, baskets, ropes, etc.,

which are produced by artisans like carpenters, and cobblers who cater to the

professional and household needs of the rural people. The urban to rural flow of

manufactured branded goods namely consumables durables and agricultural inputs

etc. as a domain is the concern of this area. As the rural, population is aspiring to

change their lifestyles, with the increasing disposable incomes, the urban

manufacturing and service sectors have entered the rural scene with their

consumables, durables and services.

9

In a survey conducted in the Management Services Pool Division of the

Hindustan Lever Ltd13, it was observed that agricultural prosperity percolates to the

small farmers and the landless laborers also, the future of any company in the country

lies in rural areas. It has a very large market potential as is evident by the Thomson

Rural Market Index14 of 1972.

The rise in rural income, consumption and expenditure are the indicators for the

changing rural market scenario. It is noticed that the change is in terms of increasing

literacy, awareness to improve living standards and modernization in the attitudes,

outlook and life-styles of the rural folk, both male and female. “The estimates

of consumption and income elasticity available for various types of commodities

reveal that the demand response to a change in income and/or expenditure would be

higher in rural markets than the urban markets.

Indian market offers both enormous opportunities and considerable challenges

to marketing men in India. The opportunities lie in the vastness of the market both in

terms of land and population, increasing levels of income and literacy, rising

consumer aspirations, and favorable marketing conditions, although the complex

social organization and cultural setting and the emergence of assertive consumer

movement with the active support of the government pose great challenge to the

Indian marketers. Nevertheless, the opportunities may be exploited and the challenges

met by developing and understanding of the marketing environment and by

cultivating insights into consumer behavior before making marketing decisions.

10

1.4.1 RURAL MARKETS - IMPORTANCE

Rural India has a population of around 742 million in 200 million households.

Agriculture and allied activities are still the means for livelihood for majority of this

population. Although the institutional reforms and economic development

programmes did not have any significant impact on the green revolution and the rural

sector in many parts of India15. The advent of market oriented farming on commercial

lines with the help of improved and advanced technology and mechanization resulted

in appreciable increase in rural income in these and other regions especially for

middle and large farmers.

It is noticed that the 75 per cent of India’s people live in rural areas, market

size of about 750 million people distributed in 400 districts across 600000 villages.

Though 350 million of these people are desperately poor and survive only at

subsistence level, the remaining 400 million are economically better off due to a

combination of favorable monsoon conditions, increased agricultural yields, and a rise

of mini industries in rural markets. It is also estimated that 200 million people have

enough disposable income to purchase a few modem goods and services such as

TV’s, Refrigerators, and motorbikes. Rural purchasing power is apparent in that rural

India accounts for a sizable percentage of the markets for many consumer goods sold

in India. 20 to 30 per cent markets for colour TV’s and refrigerators16.

11

Table; 1.4: Distribution of Villages in India

Population Number of villages % of Total

Less than 200 114267 18%

200-499 155123 24.30%

500-999 159400 25.00%

1000-1999 125758 19.70%

2000-4999 69135 10.80%

5000-9999 11618 1.80%

10,000 & Above 3064 0.50%

Total: 638365 100%

Source: NCAER

The traditional elements about rural markets are associated with their rural

communities and any breakdown of these relations would be the process of

urbanization. There is no meaningful distinction in rural region, rural family or rural

people. The element in rural societies has to be seen in terms of rural - urban

continuum. A rural urban continuum is visible and makes it difficult to trace where

the village starts and the town ends. Related to these processes are the linkages and

interactions between the rural population and the urban world. The migration of rural

laborers to the urban regions increases the exposure to the urban lifestyles, which also

contributes to the changes in consumption pattern17. Rural market is undergoing a

transformation and is luring Multinational Companies to market their products in this

segment. The key success of any marketer lies in understanding the psyche of the

rural consumer, which is completely different from that of their urban counterparts.

Marketers need to reap the benefits of an untapped rural market increased

12

consumption of durables and non durables, increased income level, low competition,

increased literacy levels, and increased brand awareness. In the urban time, they must

overcome the challenges like lack of proper storage facilities, transport and

communication, infrastructure, proper distribution channels and uneven distribution of

purchasing power18.

Today, rural markets are focused by Indian and MNC’s for various reasons. It

is expected that the current and future potential of the national income comes out from

rural population. The rural markets can be classified on the basis of literacy level,

fragmented income levels, different degrees of penetration and geographic

distance from urban markets. Based on classification market size can be decided and

it is scope for future opportunities and challenges to marketers. Government of India

defines rural as ‘Whatever is not urban are rural'19. The significant changes have been

noticed in the buying and consumption pattern of rural consumers after seventies. It is

due to agricultural revolution, rural development programmes, spread of education,

increasing banking facilities, introduction of electricity and increasing communication

with the urban areas, rural consumers are becoming aware for achieving a new and

better standard of living.

The expenditure on non food items is steadily increasing. These are mill-made

clothing, toilet articles, durable consumer goods like, furniture, sewing machines,

bicycles, two-wheelers. Sale of semi-durables like cutlery, hosieries has increased.

Demand for durables like radios, watches, TVs has increased enormously20.

However, the consumption of luxury goods is still low as compared to urban

areas because of the simple life-style and taste of the rural consumers. It has been

noticed that the consumption of consumer durables and other costly items is more in

13

prosperous agricultural districts and the demand is catching up fast with the urban

71districts .

“Rural Marketing” is a dominant theme emerging over the last few years in

Indian Marketing. The increasing penetration of electronic media and advertising into

rural population is also aspiring for better lifestyles, especially with the increasing

disposable incomes accruing to a significant section of them.

The Indian and Multinational Consumer Durable and FMCG Companies

identified the vast potential of the rural markets and attempted to target these markets.

Although the practical constraints in terms of lack of transportation and

communication facilities along with limited rural understanding acted as constraints in

comprehending the rural scenario. Initially the doors to the rural markets remained

closed and it is difficult to understand the strategies of the rural buyers. Today due to

the improved facilities of transportation and infrastructure competitors are

concentrating on rural markets.

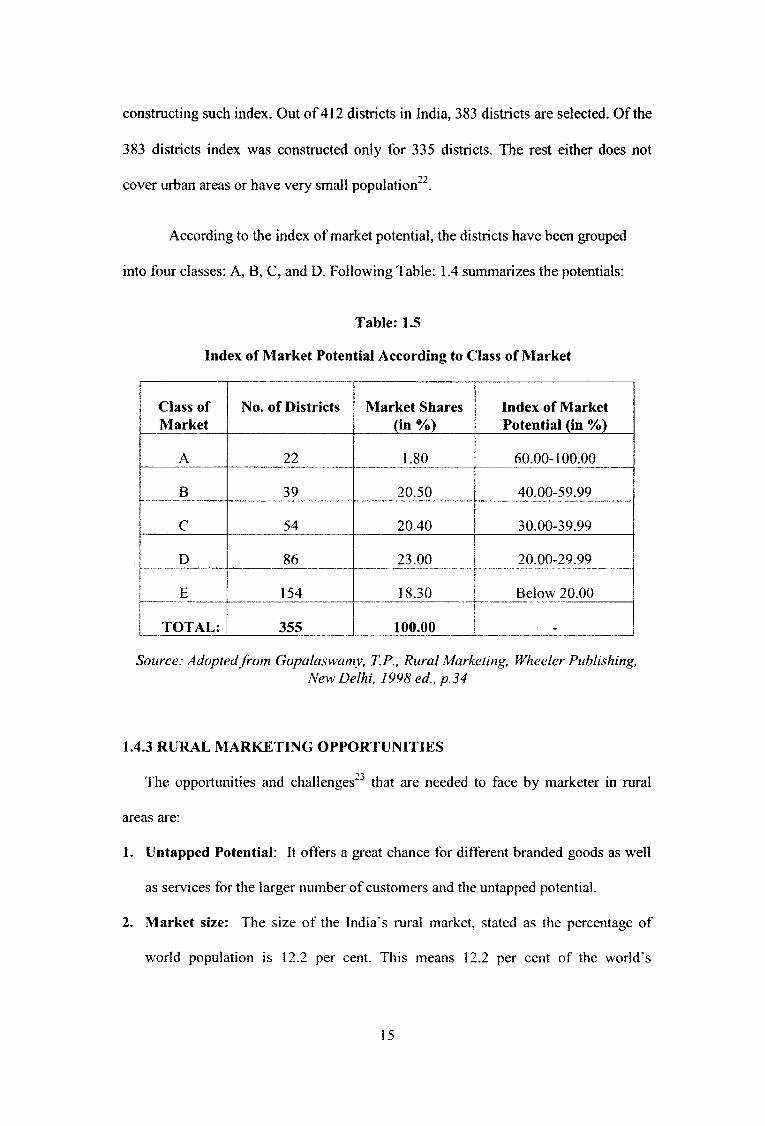

1.4.2 INDEX FOR RURAL MARKET POTENTIAL

Consumers purchasing capacity in a locality depends on their earning abilities

and such abilities in turn depend on various indicators of the locality. These indicators

are: Occupational pattern, agriculture related data, agricultural input data, rural

electrification data and commercial bank data. Better are the indicators, brighter are

the selling potential in the locality. That is why Hindustan Thompson Associates

Limited has developed “Thompson Rural Market Index” with the object of providing

guidance to the marketing people.15 In 1972 the company attempted first factors have

been considered and weights are assigned to each of such factors. The results have not

found satisfactory. Later in 1986, twenty-six factors have been considered for

14

constructing such index. Out of 412 districts in India, 383 districts are selected. Of the

383 districts index was constructed only for 335 districts. The rest either does not

cover urban areas or have very small population22.

According to the index of market potential, the districts have been grouped

into four classes: A, B, C, and D. Following Table: 1.4 summarizes the potentials:

Table: 1.5

Index of Market Potential According to Class of Market

Class of Market

No. of Districts Market Shares (in %)

Index of Market Potential (in %)

A 22 1.80 60.00-100.00

B 39 20.50 40.00-59.99

C 54 20.40 30.00-39.99

D 86 23.00 20.00-29.99

E 154 18.30 Below 20.00

TOTAL: 355 100.00 _

Source: Adopted from Gopalaswamy, T.P., Rural Marketing, Wheeler Publishing,New Delhi, 1998 ed., p.34

1.4.3 RURAL MARKETING OPPORTUNITIES

The opportunities and challenges23 that are needed to face by marketer in rural

areas are:

1. Untapped Potential: It offers a great chance for different branded goods as well

as services for the larger number of customers and the untapped potential.

2. Market size: The size of the India's rural market, stated as the percentage of

world population is 12.2 per cent. This means 12.2 per cent of the world's

15

consumers live in rural India. In India, rural household’s from about 72 per cent of

the total households and this constitutes a huge market by any standard.

3. Current - Growth in Consumption: The purchase and consumption of certain

durables and non-durables by consumes in rural areas is more than that in urban

areas. Some of the products for which the demand is more in rural areas are

wristwatches, bicycles, radios. Etc. It is estimated that for durables the annual

growth has been at a rate of 25 per cent, which is outstanding by any standards.

> According to the National Sample Survey 2000, India22 has witnessed

growth in purchasing power as a consequence of rising rural prosperity. It

is reflected in terms of rising consumption levels of rural masses. The All-

India average per capita household expenditure is Rs.382.

4. Increasing Income: Different programmes undertaken by the government has

helped to improve the economic situation of the rural areas. The increase in

income is seen in both absolute values as well as on the increase in average

number of days of occupation in a year.

5. Accessibility of Markets: Though the road network has not developed to the best

possible extent, a fair amount of development has been made in many regions,

making these regions accessible from the urban region and making it easier for

supplying products to these regions.

6. Competition in Urban Areas: The urban market is getting saturated and thus, is

unable to provide the much needed market to many companies and in search of

greener pastures, many of these companies are now targeting the rural market.

7. Changing Consumer Behaviour: The literacy rate in the villages has increased

considerably, bringing about a shift in the preferences of the people. This change

16

in preference and buying behaviour of the people has led many companies to tap

this new breed of customers.

8. Rising Rural Prosperity: The production index of consumer durables continued

to display impressive year on year growth in April 2004. During the month, index

was up by 17.7 per cent as compared with a negligible 0.4 per cent growth in

April 2003. This impressive production growth of consumer durables in recent

times, has been due to increased demand from rural sector on account of higher

growth in income (Table: 1.5)

Table: 1.6: Rising Rural Prosperity

Income Groups 1994-95 2000-01 2006-07

Above Rs. 1,00000 1.6 3.8 5.6

Rs.77,001 -1,00,000 2.7 4.7 5.8

Rs.50,000-77,000 8.3 13 22.4

Rs.25,000-50,000 2.6 41.1 44.6

25,000-and below 61.4 37.4 20.2

Source: NCEAR, Business world, October 11, 1999 p.28

From the table India is now seeing a dramatic shift towards prosperity in rural

households. The lowest income class (Rs.25, 000 and below) will shrink from more

than 60 per cent in 1994-95 to 20 per cent in 2006-07. The higher income class will be

more than double. The developmental activities were undertaken during 5 year plans

and other special programs such as land reforms, rural electrification, rural

communication network, and rural credit facilities etc.

17

9. Life Cycle Changes:

Many products have achieved near maturity in the urban market, while in rural

markets, they are still the growth phase. The reason for the variations in product

lifecycle stages may be attributed to the different rates of adoption - diffusion process

in urban and rural markets. Popular consumer durable brands in urban areas have

reached maturity stage while in rural markets yet to grow.

1.5.1 CONSUMER BEHAVIOUR

There are two types of resources in nature, namely, human resources, and

physical resource, of the two, the human resources is active. This active resource

(human resource) exploits all the material resources for it survival. For this survival,

there are three fundamental components, viz. Food, clothing and shelter. The urge for

these three components arises in human mind. This urge is the mother of all human

effort. Behaviour gives an answer to “how human beings act as they do”? In the

marketing context, this explanation may be an answer to “why people, behave as they

do as buyers”24.

Consumer behaviour is a subsection of the large fields of human behaviour. It

is the process whereby individuals decide whether, what, when, where how and from

whom to purchase goods and services”25

The comprehensive idea about consumer behaviour as “The act of individuals

directly involved in obtaining and using economic goods and services, including the

decision processes that precede and determine these acts”.26

18

Consumer behaviour involves the purchasing and other consumption related

activities of people in the exchange process. The human mind gets expression through

body and thus consumer behaviour relates to the inner man, i.e. this covert behaviour.

1.5.2 STUDY OF CONSUMER BEHAVIOUR - ITS SIGNIFICANCE

The study of consumer behaviour has assumed growing importance under the

present customer oriented marketing system. Consumer behaviour is a dynamic

concept. Hence, study of consumer behaviour is important for marketers in response

to the question. “How do consumers buy and how will this change, if the marketing

■ynprogram is changed”?

The study of consumer behaviour is useful in the development of more

efficient use of marketing resources and in arriving at solutions to the problems of

marketing management. Now-a-days, greater attention is being paid to consumer

protection. The knowledge and understanding of consumer behaviour can lead to both

consumer protection efforts and to better understanding of consumer behaviour can

lead to both consumer protection efforts and to better understanding of the impact

these efforts have on consumers. An important reason for studying consumer

behaviour is the need for evaluation of consumer groups with unsatisfied needs or

desires28.

The success of any business enterprise depends not only on the ability to

recognize unmet needs, but also to understand whether those needs will be expressed

as economically feasible markets and what organizational response is required for

success in catering to those needs.

19

The study of consumer behaviour is essential for the development of market

strategies and to segment the markets. Individuals significantly vary in terms of

income, occupations, education, ages, tastes, attitudes, interest, residence and so forth.

It would not be possible for the marketer to design an appropriate marketing mix to

appeal and influence all the customers. One of the major contributions of consumer

behaviour to marketers is the identification of meaningful variables upon which to

segment markets29.

The marketing concept envisages a proper and adequate understanding of the

buyer and his behaviour. The buyer behaviour is the one which manifested overtly in

the consumption of a product. A prudent marketer is supposed to learn more what a

buyer is than who the buyer is. The critical understanding of the buyer with this

information should become the essential ingredients of a marketing policy decision.

For the success of business, all the marketing plans and policies should be customer-

oriented. Knowledge of consumer behaviour is, therefore, important for effective

product planning and for efficient execution of a firm's advertising and sales

promotion policies30.

It has been said that change is the life blood of all the marketing activities. The

marketer studies the change continuously and adapts to the change. Further, tries to

create change at the root of all this change is human mind. The marketing concept is a

bye-product of the study of ever changing human mind consistent with the

contemporary marketing thought; consumers are the focal point of all the marketing

activities.

Marketing starts with consumers and ends with consumers. Satisfaction of the

consumer is the ultimate aim of any business activity”.31

20

Behaviour is a mirror in which everyone shows his or her image. Behaviour is

the process of responding to stimuli. Consumer behaviour is to do with the activities

of individuals in obtaining and using the goods and services; it encompasses the

decision making process that precedes and determines purchases. “It is the process

where by individuals decide, whether what, when, where, how and from whom to

purchase goods and services”. Consumer behaviour is all the psychological, social

and physical behaviour of potential customers as they become aware of, evaluate,

purchase, consumer and tell others about the products or services . The consumer is

the focus of marketing efforts. The modem marketing concept spells out the real

significance of buyer behaviour. In the course of operating the concept, the modem

marketing management tries to solve the basic problems of consumers in the area of

consumption.

For Defining of such problems; there is a need for constant effort to

understand the buying process and all the factors influencing consumer behaviour.

Further, consumer’s behaviour is dynamic. The dynamic nature of consumer makes it

more important making the marketing manager to study, analyze and interpret the

ever changing consumer behaviour. It helps in making sound decision in respect of

the Four P’s of the marketing mix.

The study of consumer behaviour has become more complicated in the light of

increasing role of government in consumer movement in all the developing countries.

Comprehending consumer needs, expectations and aspirations coupled with problems

is a must to exploit marketing opportunities and meeting the challenges best along

with the opportunities. Consumer behaviour comprises of individuals in obtaining and

using goods and services. Knowledge of the factors that influence consumer

21

behaviour can help organizations predict how consumers will respond to their

products. Behaviour is determined by both socio-cultural and psychological factors.

Culture encompasses the values, arts, customs, and skills of people in a given

society cultural trends reflect the social values of the population and as much have

important implications for market segmentation, product development, advertising,

and other aspects of marketing strategy. Social-class categories can be identified by

income, education level and occupation. Social class and purchasing patterns are

indicators for marketers in strategy planning.

The family has considerable impact on the formation of values and attitudes

that influence purchasing patterns. Many people favor the same products as their

parents do. Purchase decision tends to be influenced by the family members who use

the product most. The relative influence of husbands and wives in purchasing

decisions varies according to product class and buying stage33.

Reference groups play an important role in purchasing patterns by providing

the individual with a sense of identity. Consumers are more likely to buy a product if

it is used by someone they share common interest with or by someone they admire or

trust. Consumers also look to opinion leaders to set trends by word-of-mouth

communication. Opinion leadership is usually related to a specific product or interest.

The more conspicuous the product, that the consumer more likely will be influenced

by other people in making the purchase decision.

It is important for marketers to understand the motives that lead consumers to

make purchases. Maslow’s theory of motivation is based on five needs; survival,

safety, belongingness and love, esteem, and self-actualization. Motivational analysis

is a highly speculative field which sometimes probes the symbolic realm of the

22

unconscious34. Perception is the process by which the mind takes in and orders

stimuli.

It is important for the marketers to know the impact of stimulus on consumers

behaviour in perceiving a product in terms of brand images, benefits and risks that

might result from its purchase. Marketers view learning primarily as a stimulus -

response mechanism. The components of the stimulus - response have been

formulated in terms of drive, cue, response, and reinforcement.

Marketers are interested in attitudes because they often precede actions. The

cognitive component of attitude is what the individual thinks about the object; the

affective component is what the individual feels about the object, and the co-native

component is how the individual responds to the object.Marketing success is partly

determined by how well a company is able to understand, predict and influence

consumer attitudes. Depending on how a product is doing, the marketer may want to

confirm existing attitudes, change existing attitudes, or create new attitudes35.

Personality is a reflection of individual differences in behaviour. Trait-factor

theories of personality emphasize the personal characteristics that distinguish

consumers from one another and the external situations that cause consumers to

exhibit predictable behaviour patterns. Generalizations about the effects of personality

on consumer behaviour may be over simplifications, but the field of psychographics

can provide a valuable basis for market segmentation.

1,6.1 RURAL CONSUMER

About three quarters of the Indian population are in the rural areas and with

the growing middle class, especially in the Indian cities; the spill over effect of the

23

growing urban middle class is also felt in the rural areas. The Indian rural market has

been growing at 3-4% per annum, adding more than 1 million new consumers every

year and now accounts for close to 50% of the volume consumption of fast-moving

consumer goods (FMCG) in India.

The market size of the fast moving consumer goods sector is projected to more

than double to US$ 23.25 billion by 2010 from the present US$ 11.16 billion. As a

result, it is becoming an important market place for fast moving consumer goods as

well as consumer durables.

Rural market consists of diverse population spread across a vast country,

speaking different languages, with different levels of literacy and composed of big

landlords, traders, small farmers, marginal farmer’s laborers and communities of

different profession. The rural consumer always prefers to live in simple way.

Everyone has his/her own typical standard of living. The rural consumers are less

aware of westernization than urban people. The expectation of self sustaining

economic growth is more important than urban choices. When a rural consumer

intends to buy a product, the product type depends on consumer’s needs, purchasing

capacity, his attitude towards the product and the cost benefit analysis of the product.

Based on this, the manufactures were more focused on price of product and paid less

attention to quality or durability. But the rural consumer has the potential to buy

expensive premium consumer durables like, watches, TVs, mobiles, gas-stove, and

two-wheelers for acquiring social status in a rural society. In rural areas, the decision

making processes is collective. So marketers should address the brand message at

different levels. In this process, the educated rural people act as opinion leaders. Their

decisions matter a lot at the purchasing level.

24

Besides that, some major attitudes of rural consumers are:

• Resistant to change

• Price sensitive

• High brand loyalty

• Influenced by traditions

• Moderate aspirational levels

• Quality conscious

• Low to moderate risk-taking ability

“Trust” is a major factor in rural marketing, which is nothing but a mechanism to

solidify the belief in the product. Once the marketer creates a positive attitude of the

brand/service, then it is very difficult to divert the rural consumers. They not only

seek comfort in their brand but also from the person who is selling them the brand.

The person may be the primary source (the company), the secondary source (the

wholesaler) or the territory source (the retailer). This is applicable for all the brands,

products, services, etc. The seasonal fluctuation also affects the behavior of the rural

consumer up to some extent. But the growing literacy rate and the high penetration of

conventional media changed the perception and attitude of the rural consumer. At the

same time, the consumption habits of rural consumers are also becoming more

modem in an urban sense36.

1.6.2 CHARACTERISTICS OF RURAL CONSUMER BEHAVIOUR

The rural consumers are noted for the high degree of value orientation. Such

orientation to value has labeled Indians as one of the most discerning consumers in

the world. Even, luxury brands have to design a unique pricing strategy in order to get

a foothold in the Indian market.

25

Rural consumers have a high degree of family orientation. This orientation in

fact, extends to the extended family and friends as well. Brands with identities that

support family values tend to be popular and accepted easily in the rural market.

Rural consumers are also associated with values of nurturing, care and

affection. These values are far more dominant than values of ambition and

achievement. Product which communicate feelings and emotions gel with the rural

consumers.

Apart from psychology and economics, the role of history and tradition in

shaping the Indian consumer behavior is quite unique. Perhaps, only in India, one

sees traditional products along side modem products. For example, hair oils and tooth

powder existing with shampoos and toothpaste.

1.6.3 INCREASING AWARENESS OF INDIAN CONSUMER

Over the years, as a result of the increasing literacy in the country, exposure to

the west, satellite television, foreign magazines and newspapers, there is a significant

increase of consumer awareness among the Indians. Today more and more consumers

are selective on the quality of the products/services.

This awareness has made the Indian consumers seek more and more reliable

sources for purchases such as organized retail chains that have a corporate

background and where the accountability is more pronounced. The consumer also

seeks to purchase from a place where his/her feedback is more valued.

Indian consumers are now more aware and discerning, and are knowledgeable

about technology, products and the market and are beginning to demand benefits

beyond just availability of a range of products that came from ‘trusted' manufacturers.

The Indian consumers are price sensitive and prefer to buy value for money products.

26

1.6.4 CHANGING CONSUMER BEHAVIOUR

The study of consumer behaviour is an attempt to understand and predict

human actions in the buying role. It has assumed growing importance under market-

orientated or customer oriented marketing planning and management. Buyers market

for many products and the growth of consumerism and consumer legislation since

1960 have created special interest in buyer behaviour and the formulation of

marketing mixes to respond favorably buyer behaviour in the market place. Buyer

behaviour is defined as “all psychological, social and physical behaviour” of potential

customers as they become aware of, evaluate purchase, consumer, and tell others

about products and services.

Consumer behaviour is not only the study of what people consume but also

“where”, “How often”, and “under what conditions”, the product is consumed. In

view of the dynamic and complex nature of the consumer behaviour many social

scientists of different disciplines have attempted to formulate theories drawn from

peculiarities of their fields. They viewed the consumer behaviour and explained from

different angles. Each observer seemed to view the behaviour, while there is some

justification in all, by itself none is a totally adequate explanation of behaviour.

Decision process approach in understanding consumer behaviour provides that

purchase is an ultimate activity in a course of action taken by the consumer. To

understand that stage, it is necessary to understand what precedes and what follows

that state37.The literacy rates in the villages have increased considerably, bringing

about a shift in the preferences of the people. This change in preference and buying

behaviour of the people has led many companies to tap the new breed of customers.

27

From an overall market size point of view, rural markets look very attractive.

The rural market offers its own set of problems, which include a scant density of

target population, posing a challenge for continuous and effective physical

distribution. The set of intermediaries in rural markets are different from urban

intermediaries, posing challenges of channel management.

Promotion and marketing communications in rural market also poses another

uphill task as target consumers are illiterate and there is hardly any conventional

media available for communication. Problems of physical distribution and channel

management have adverse impact on the quality of services and cost of serving

customers in the markets. The market network has a large set of multipurpose tail

outlets and a large chunk of primary consumers. Marketers need to develop a

distribution structure by developing stock points in feeder towns and serving the small

retailers in village markets. The marketer does not have control over delivery and

-*o

quality of services at the retailer point" .

Companies with relatively fewer resources can come together through

syndicated distribution through co-partnering with non-competitive marketers for the

same market. Companies follow a strategy called “eo-opetition”, in which they come

together to synergize their resources in rural markets for benefit of both the partners

and yet, can compete in the urban markets for market share.

Rural marketing also involves more intensive personal selling compared to

urban marketing. Unavailability of persuasive media and poor level of literacy

demands personal selling to convince consumers to buy a product in the market.

There is need to understand the consumer behaviour and “reason why" of Indian

market and then, design marketing programs in which they need to associate the brand

28

with the life style of rural people. Marketers should try to understand the media habits

of people and use rural folk media for communication39.

They need to be addressed in their own language, by their own hero, and

associate the brand with myriad rituals, celebrations, festivals, melas, and other

activities for enhancing brand’s market presence. Thus, looking at the challenges and

the opportunities that rural markets offer to the marketers, it can be said that the future

is very promising for those who can understand the dynamics of rural markets and

exploit them to their best advantage.

1.6.5 CHANGING RURAL CONSUMER

The increasing disposable income and the per capita consumption of rural

consumer improving their standard of living. Rural consumers prefer to buy the

products with hygienic and reasonably high quality products and simultaneously get

rid of the spurious and sub-standard products being supplied to them. They deserve

quality products, correct information about the product and a door step delivery40.

The rural consumer from one homogeneous group with similar needs, values

and aspirations has similar kind of expectations. With the increasing spread of rural

income, personal care products are expected to make substantial penetration into the

lower income strata by the normal “Percolation effect”41.

The factors contributing to increasing purchasing capacity of rural consumers

are marketable agricultural surplus, remittances, Government expenditure, and

disposal of industry.

Now, the rural market is undergoing a sea change resulting from the multi

pronged activities undertaken for overall development of villages-agricultural

29

revolution, spread of education, increasing banking facilities, introduction of

electricity and increasing communication with the urban areas, etc. All these have led

to the creation of general awareness for achieving a new and a better standard of

living.

This is an indication that the demand for personal care products will be on the

increase. Significant changes have been noticed in the changing buying and

consumption patterns of the rural consumers, imbibing new ideas, attitudes and way

of life. The National Sample Survey42, 17th round has revealed the increase in demand

for non-food consumer products for household consumption. It has been observed

that the consumption of consumer durables and other costly items are more in

prosperous agricultural districts and the demand is catching up fast with that in the

urban districts.

Prosperity in the rural areas has opened up new opportunities and it is seen

that quite a few business houses are on their way for capitalizing this marketing

opportunity. Rural consumer of today is different from the rural consumer of

yesterday. He is very dynamic. He is an enlightened person with new expectations. He

needs a lot of convincing before buying durable products.

1.6.6 SOCIAL AND BEHAVIORAL INFLUENCES ON THE RURAL

CONSUMER OF INDIA

The rural consumer is influenced by the environment and by his wants and

perceptions. Understanding the social and attitudinal influences on rural consumer

behaviour is important to the marketer, as these serve as a guide to decide on product

offering, pricing, distribution, media and its impact, and message in effect. The

following are some of the rural marketing strategies.

30

Cultural Social Practices and Consumer Behaviour The cultural and social

practices have a major influence on the behaviour of rural consumer. The widely

dispersed villages and limited communication helped preserve traditions in rural

markets. Increasing access to urban areas and information dissemination possibly

reduces the influence of traditions. Till such a time, those cultural influences would

persist. Hence, the marketer has to develop products that suit cultural practices.

Identify a suitable target audience and design media and message that reflect social

behaviour. Design the distribution to reach the places where the consumer

traditionally makes his purchase43.

Influence of Perception: The marketer seeks to modify the behaviour of the rural

consumer needs to first influence perception and attitude. It is here that the marketer

has to be careful in designing the product and message for the rural market. The

decision variables of a product and message are critical to marketing effectiveness in

rural markets as the color, shape and action hold meaning for rural consumers that are

different from those held by urban consumers.

1. Attitude to Quality and Price: The marketer who seeks to modify the behaviour

of the rural consumer needs to first influence perception and attitude. It is here

that the marketer has to be careful in designing the product and message for the

rural market. The decision variables of a product and message are critical to

marketing effectiveness in rural markets as the color, shape and action hold

meaning for rural consumers that are different from those held by urban

consumers.

31

2. Attitude to quality and price: Small-pack sizes get acceptance in markets, which

can have only a small price because of the nature of income receipts. A landless

laborer may get a small amount to spend.

3. Brand Preference and Loyalty: There is a need to have a good understanding of

the purchase behaviour of the consumer in order to adopt right marketing strategy.

The attitude of the rural consumer favors quality products and brands, but

brand pricing has to take into account both the income level and the income flow of

the consumers. The rural consumers are not homogenous. There are consumers that

can afford high priced brands. There is a group of consumers who can not only afford,

but are also willing to buy, high priced brands.

1.5.7 Rural demand and buying habits

Demand depends on need and major portion of need is based on income of the

buyers. Earning of most of the rural buyers are seasonal in nature as they are engaged

in agriculture or agriculture based activities, and agricultural products grow

seasonally44.

Needs of the rural buyers may be broadly classified into two groups:

agricultural inputs and consumer goods. Again both the group of goods may be

classified into non-durable and durable agricultural inputs, while pump sets, power

tillers, tractors etc. are durable agricultural inputs. Foods, cosmetics, clothes,

toothpaste are non-durables, while refrigerators, TV sets, two wheelers, Automobiles,

washing machines are durable consumables.

32

Volume of demands, timing of demands and the prices at which demands are

to be made depend on various factors related to the concerned consumer. Some

important factors are: buyer’s income flow, his need perception, and his level of

education, social connection and similar matters45. Enquires on such issues on rural

buyers are very limited. Hence, comparison between rural and urban buyers in these

respects may throw some light on these issues. Such a comparison is as given below:

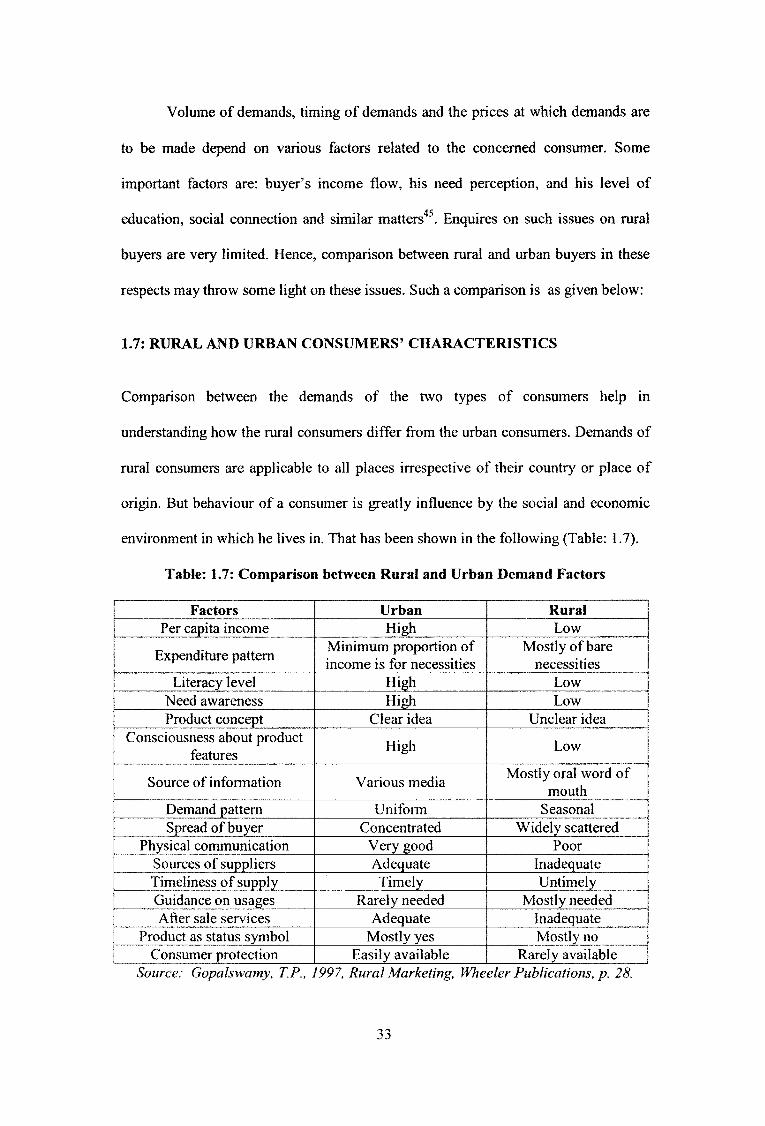

1.7: RURAL AND URBAN CONSUMERS’ CHARACTERISTICS

Comparison between the demands of the two types of consumers help in

understanding how the rural consumers differ from the urban consumers. Demands of

rural consumers are applicable to all places irrespective of their country or place of

origin. But behaviour of a consumer is greatly influence by the social and economic

environment in which he lives in. That has been shown in the following (Table: 1.7).

Table: 1.7: Comparison between Rural and Urban Demand Factors

Factors Urban RuralPer capita income High Low

Expenditure pattern Minimum proportion of income is for necessities

Mostly of bare necessities

Literacy level High LowNeed awareness High LowProduct concept Clear idea Unclear idea

Consciousness about product features High Low

Source of information Various media Mostly oral word of mouth

Demand pattern Uniform SeasonalSpread of buyer Concentrated Widely scattered

Physical communication Very good PoorSources of suppliers Adequate InadequateTimeliness of supply Timely UntimelyGuidance on usages Rarely needed Mostly neededAfter sale services Adequate Inadequate

Product as status symbol Mostly yes Mostly noConsumer protection Easily available Rarely available

Source: Gopalswamy, T.P., 1997, Rural Marketing, Wheeler Publications, p. 28.

33

1.7.1 CHANGING TRENDS IN INDIAN CONSUMER BEHAVIOUR

Bulk Purchasing

Urbanization is taking place in India at a dramatic pace and is influencing the

life style and buying behaviour of the consumers. The working urbanites are

depending more on fast and ready-to-serve food, they take less pain in traditional

method of cooking and cleaning.

Bulk purchases from hyper stores seems to be the trend these days with

purchasing becoming more of a once-a-week affair, rather than frequent visits to the

neighbourhood market/store/vendor. The popular growing shopping trend among

urbanities is purchasing from super markets to hyper stores.

Trendy Life Styles

The current urban middle and upper class Indian consumer buying behaviour

to a large extent has western influence. There is an increase in positive attitude

towards western trends. The Indian consumer has become much more open-minded

and experimental in his/her perspective. There is now an exponential growth of

western trend reaching the Indian consumer by way of the media and Indians working

abroad.

Foreign brands vie increasingly with domestic brands for the growing market

in India. Foreign made furniture is well accepted by the Indian consumers.

Malaysian, Chinese, Italian furniture are growing in popularity in India. Indian

consumers have also developed lifestyles which have emerged from changing

attitudes and mind sets; exposure to western influences and a need for self-

34

gratification. Beauty parlours in cities, eateries, designer wear, watches, hi-tech

products are a few instances which reflect these changes.

The sellers’ market is slowly moving towards becoming the buyers’ market.

Since, India’s economic liberalization policies were initiated in 1991, many new

product offerings have entered the Indian market and product variety has also

increased manifold. Import licensing restrictions are being eliminated and tariffs

significantly reduced and this has led to large range of consumer goods made

available in India. Indian consumers have always preferred foreign goods and with the

liberalization, they now have a choice of foreign products vis-a-vis the local products.

1.7.2 PROBLEMS IN REACHING RURAL CONSUMERS

There are several problems in establishing market in rural areas, though they have

potential to grow46. The problems are:

1. Lack of Retail Infrastructure: Around 60,000 of the approximately 0.6 million

villages in India did not have a retail outlet of any kind.

2. Vast unevenly distributed Purchasing Power: Rural India accounts for a

significant share of the total consumption in a number of categories, the

consumption trends to be geographically dispersed because of the sparse

distribution of populations and unevenness of purchasing power.

In fact, 145,098 villages or 23 per cent of the total number of villages in India

have a population less than 200. Another 21 per cent have population between 200

and 500. Thus for a Route Schedule (RS) type distribution system to work, the RS

would have to cover large geographical areas to achieve break-even volumes.

35

Covering large geographical areas, in turn, would raise the inventory and

transportation costs, thus affecting the viability of the RS operations.

3. Difficulty in Logistics Planning: Determining sales potential of an area in rural

India is a challenging task, considering the sparse population distribution, uneven

distribution of purchasing power, and the relative lack of data availability.

4. Seasonal Demand: Agriculture is the primary source of income in rural India.

Agriculture being a seasonal activity, the demand pattern also tends to be

seasonal. The demand is typically high during the peak crop harvesting and

marketing season. The seasonality of demand implies low sales in the lull months,

which again affects the viability of operations of the members of the distribution

channel.

5. Need for large-scale marketing organization and staff: Large geographical

areas with underdeveloped transportation and communication infrastructure call

for more intensive marketing efforts for direct coverage. This, in turn, raises the

cost of servicing these markets.

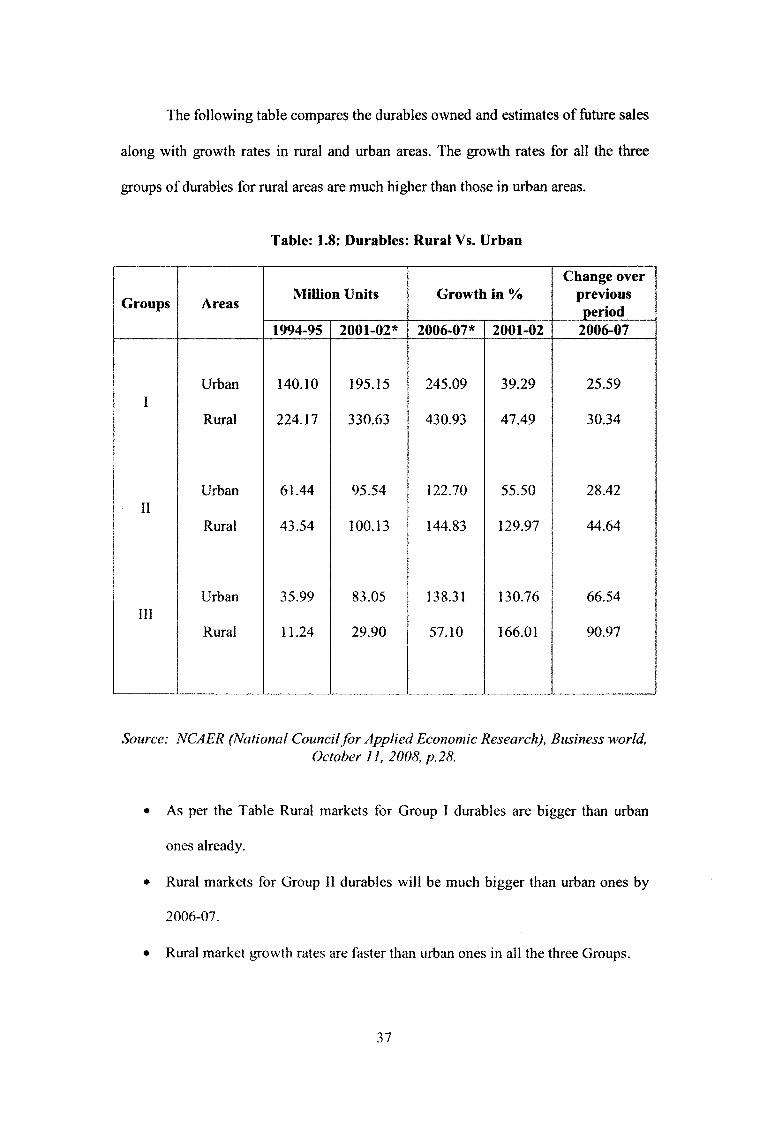

Growth Rates of Rural - Urban for Consumer Durables: The growth rates

of durable market are higher in rural areas for many products. The durable market

offers an excellent proposition47 (Table: 1.7). The durables are classified as under for

analysis:

Group - I Less than Rs. 1,000 in value. Items like transistors, pressure cookers,

wristwatches and bicycles.

Group - II Rs. 1,001 to Rs. 6,000 in value. Items like black and white TV’s sewing

machines, mixers and cassette recorders.

Group-Ill More than Rs. 6,000 in value. Items like color TV’s, refrigerators, two-

wheelers and washing machines.

36

The following table compares the durables owned and estimates of ftiture sales

along with growth rates in rural and urban areas. The growth rates for all the three

groups of durables for rural areas are much higher than those in urban areas.

Table: 1.8: Durables: Rural Vs. Urban

Groups AreasMillion Units Growth in %

Change over previous period

1994-95 2001-02* 2006-07* 2001-02 2006-07

IUrban 140.10 195.15 245.09 39.29 25.59

Rural 224.17 330.63 430.93 47.49 30.34

Urban 61.44 95.54 122.70 55.50 28.42II

Rural 43.54 100.13 144.83 129.97 44.64

Urban 35.99 83.05 138.31 130.76 66.54III

Rural 11.24 29.90 57.10 166.01 90.97

Source: NCAER (National Council for Applied Economic Research), Business world,October 11, 2008, p.28.

• As per the Table Rural markets for Group I durables are bigger than urban

ones already.

• Rural markets for Group II durables will be much bigger than urban ones by

2006-07.

• Rural market growth rates are faster than urban ones in all the three Groups.

37

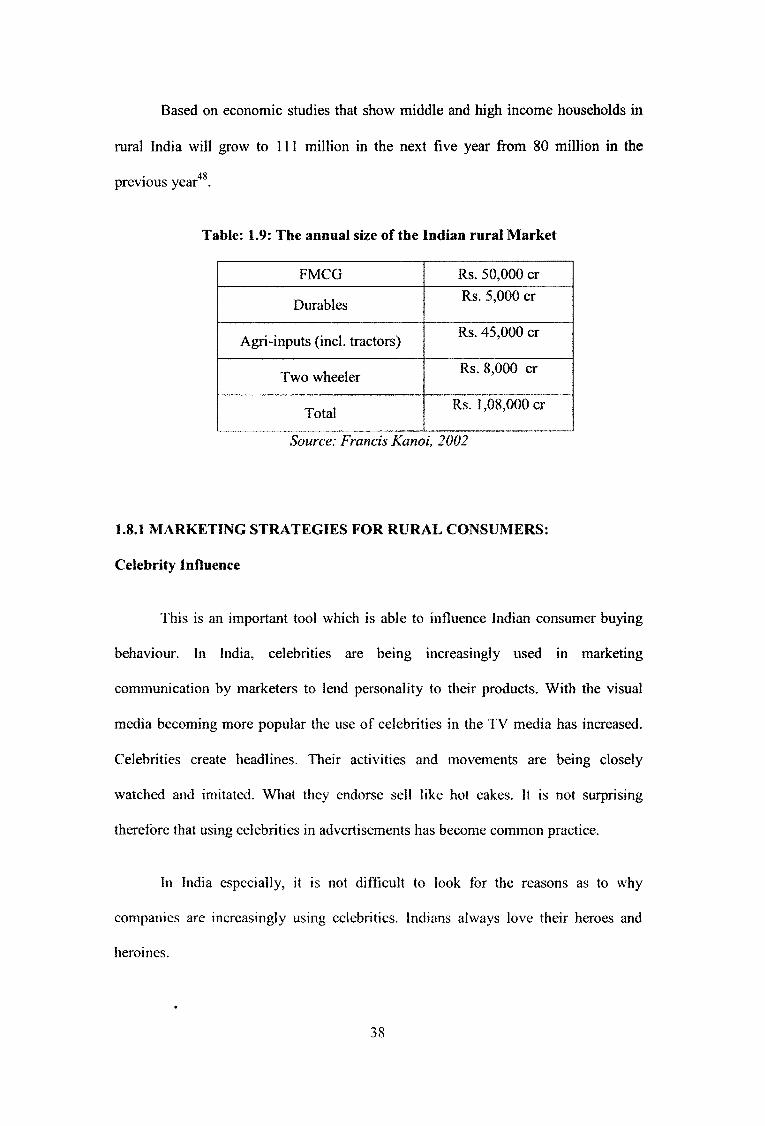

Based on economic studies that show middle and high income households in

rural India will grow to 111 million in the next five year from 80 million in the

previous year48.

Table: 1.9: The annual size of the Indian rural Market

FMCG Rs. 50,000 cr

Durables Rs. 5,000 cr

Agri-inputs (incl. tractors) Rs. 45,000 cr

Two wheeler Rs. 8,000 cr

Total Rs. 1,08,000 cr

Source: Francis Kanoi, 2002

1.8.1 MARKETING STRATEGIES FOR RURAL CONSUMERS:

Celebrity Influence

This is an important tool which is able to influence Indian consumer buying

behaviour. In India, celebrities are being increasingly used in marketing

communication by marketers to lend personality to their products. With the visual

media becoming more popular the use of celebrities in the TV media has increased.

Celebrities create headlines. Their activities and movements are being closely

watched and imitated. What they endorse sell like hot cakes. It is not surprising

therefore that using celebrities in advertisements has become common practice.

In India especially, it is not difficult to look for the reasons as to why

companies are increasingly using celebrities. Indians always love their heroes and

heroines.

38

Consumers like advertisements more if they are admirers of the celebrities in

the advertisements. When a consumer likes the celebrity in the advertisement, he or

she is more likely to accept what the celebrity says about the advertised product and

therefore will develop more positive feelings toward the advertisement and the brand

itself. Famous celebrities are able to attract attention and retain attention by their mere

presence in the advertisements. In the midst of the advertisement clutter, the

advertisements that celebrities endorse also achieve high recall rates. When people see

their favoured reference group members or celebrities in the advertisements, they pay

more attention to them. Celebrities may also help reposition products. Products with

sagging sales needs some boosting and in these Indian celebrities can help by way of

they endorsing the product concerned.

Quality Oriented Outlets

Indian consumers looking for quality choose expensive brands as they feel that

price is an indicator of quality. However, in the absence of well known brands in

selected product range, consumers are likely to take cues from well established retail

outlets hoping that these outlets carry quality products. Businessmen who prefer not

to go for high-visibility, costly campaigns may embark on the strategy to engage well

known retail outlets to capture the segment of rural consumers looking for quality

products.

Freebies

Indian consumer buying behaviour is influenced by freebies. Freebies are

consumer products given free of charge as gifts to purchases of selected products

above a certain value. TVs, washing machines, refrigerators, and ready made clothes

39

are some of the product categories in which freebies are given to Indian consumers.

Freebies generally comprise tooth paste, soaps, detergent, cooking oil etc.

Indian companies intending to penetrate the Indian market, perhaps should

consider giving freebies for the purchases made by the Indian consumers. Malaysians

can work with the local business partners to attract the consumers by way of such

promotion campaigns.

Eco-friendly Products

The environmental awareness in India has started affecting marketing of

products based upon their eco-friendliness. In general, Indian consumers are likely to

buy environmentally responsible products and packs. The future key for marketing

could be to select more ethical and ecological responsible products and packaging,

which is also convenient for consumers, thus, balancing environmental concerns with

commercial considerations. Consumers in India are taking lead in prompting

manufacturers to adopt technologies to produce eco-friendly products.

40

1.10.1CONSUMER DURABLE INDUSTRY

The study of Consumer Durable market will be helpful in understanding the

key aspects of the consumer behaviour with respect to consumer durables in rural

areas. To take a deep insight of consumer behaviour with regard to consumer

durables, the study has been taken up to know the status of durable market in recent

times.

Indian economy is one of the fastest growing economy in the world with the

GDP rate of 9.2 per cent (177000 crore) which is fourth largest in the world. In terms

of foreign exchange, India stands at 12th largest economy with foreign reserve of USD

177.00 billion 49. During post liberalization Indian government encouraging industries

like consumer electronics, automobile, textiles, transportation etc. For a long period

rural markets were not concentrated either by government or organization. Rural

markets were most unexplored markets of the country50.

In India, 70 per cent of the population lives in villages. As the urban market is

reaching to saturation, rural market is giving wide scope for durables, as rural

people’s purchasing power parity is increasing substantially. Their penetration level is

at two percent to 0.5 per cent for durables. The rural market is growing faster than the

urban market. Where as urban market has more of product replacement market.

However, rural market is still unexplored for consumer durables51.

The pre liberalization era saw foreign direct investment being discouraged

with the enactment of FERA in 1974. The Act proved to be a major obstacle to the

growth of the durable industry. As a result, the economies of the scale could not be

achieved through the mass production.S.K.U.L IBRARYAcc.Gall.No

by any foreign company in Indian companies. It is regulated only up to 40 per cent

equity is allowed by FDI in Indian companies. Some other hurdles are like, imports

discouraged by heavy import duties, licensing policies, Government policies, etc.

Before the liberalization in Indian economy only a few companies like

Kelvinator, Godrej, Allwyn, and Voltas were the major players, accounting for not

less than 90 per cent of the market. Post liberalization is the period for foreign players

like LG, Sony, Samsung, Daewoo, and Aiwa to enter in Indian market. Today these

players are holding major market share. Durable market is one of the fastest growing

sectors in the country. It is due to the rise in living standards, easy access to consumer

finance and wide range of choice and increased number of foreign players. Durables

like watches, TVs, mobile phones, refrigerators, washing machines and air coolers,

gas-stove and two-wheelers are no longer considered luxury items. Exchange offers,

discounts, and intense competition are also increasing the growth of consumer durable

market in India. The Indian market is prospecting for durables due to increase in

income levels.

42

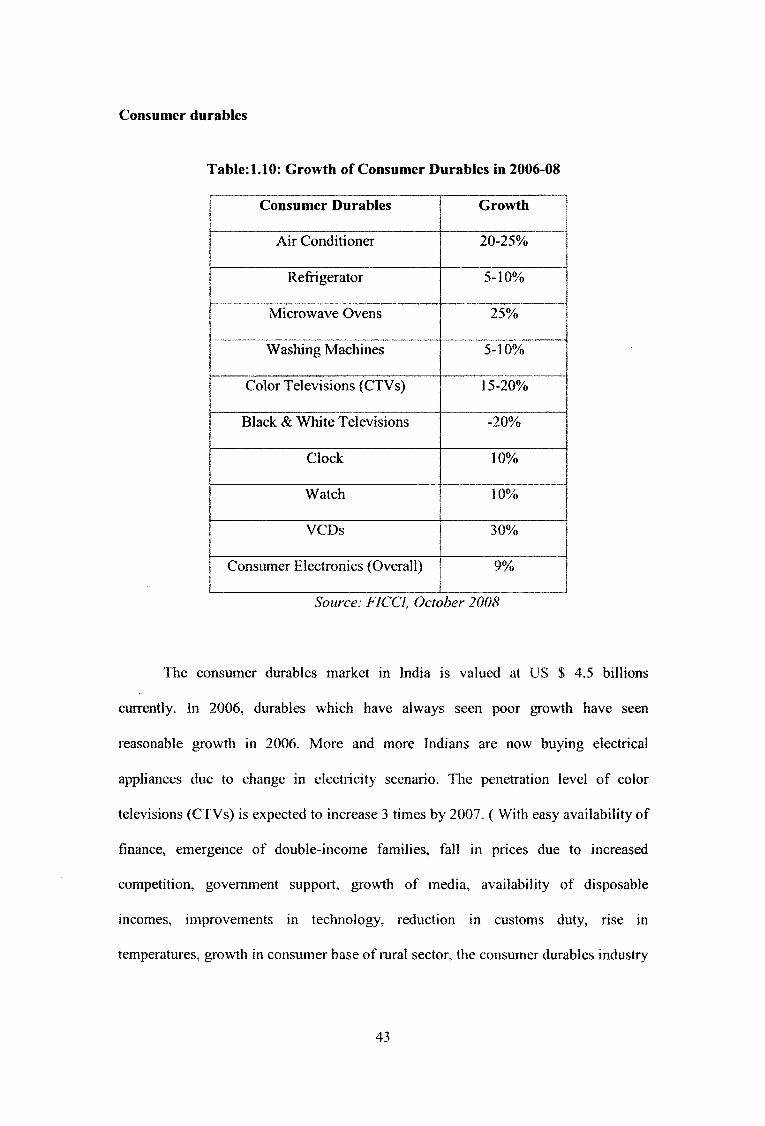

Consumer durables

Table: 1.10: Growth of Consumer Durables in 2006-08

Consumer Durables Growth

Air Conditioner 20-25%

Refrigerator 5-10%

Microwave Ovens 25%

Washing Machines 5-10%

Color Televisions (CTVs) 15-20%

Black & White Televisions -20%

Clock 10%

Watch 10%

VCDs 30%

Consumer Electronics (Overall) 9%

Source: FICCI, October 2008

The consumer durables market in India is valued at US $ 4.5 billions

currently. In 2006, durables which have always seen poor growth have seen

reasonable growth in 2006. More and more Indians are now buying electrical

appliances due to change in electricity scenario. The penetration level of color

televisions (CTVs) is expected to increase 3 times by 2007. ( With easy availability of

finance, emergence of double-income families, fall in prices due to increased

competition, government support, growth of media, availability of disposable

incomes, improvements in technology, reduction in customs duty, rise in

temperatures, growth in consumer base of rural sector, the consumer durables industry

43

is growing at a fast pace. Given these factors, a good growth is projected in the future,

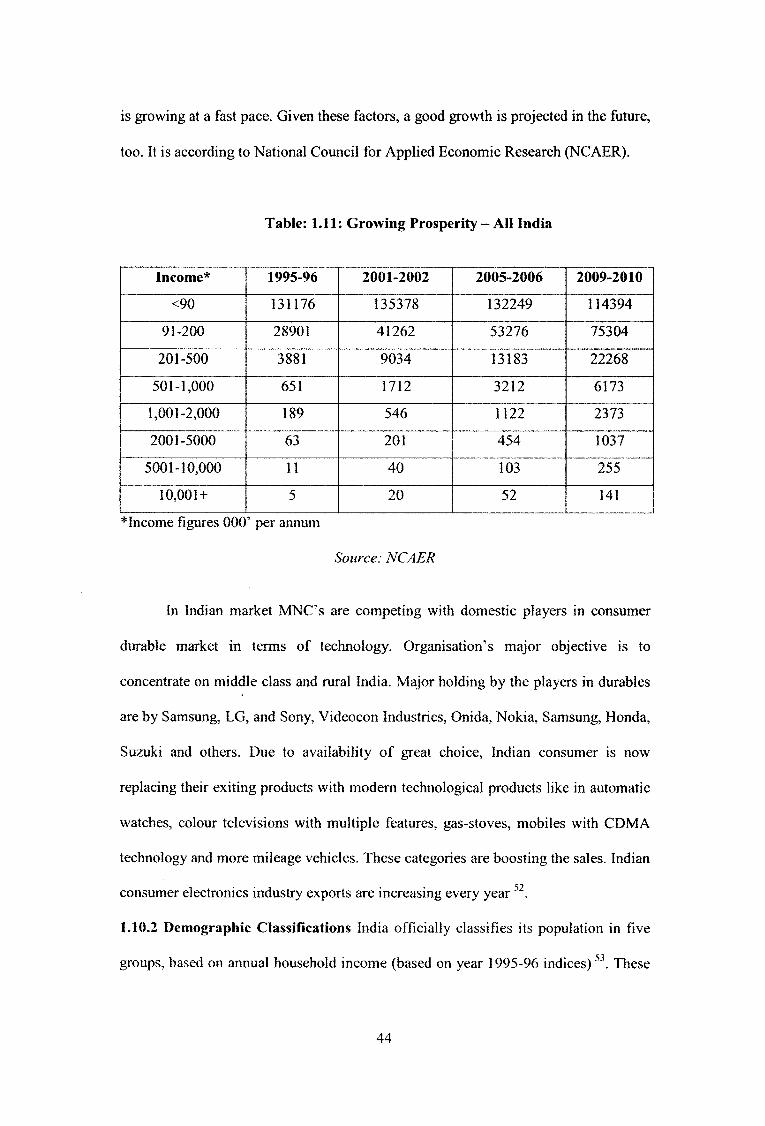

too. It is according to National Council for Applied Economic Research (NCAER).

Table: 1.11: Growing Prosperity - AH India

Income* 1995-96 2001-2002 2005-2006 2009-2010

<90 131176 135378 132249 114394

91-200 28901 41262 53276 75304

201-500 3881 9034 13183 22268

501-1,000 651 1712 3212 6173

1,001-2,000 189 546 1122 2373

2001-5000 63 201 454 1037

5001-10,000 11 40 103 255

10,001+ 5 20 52 141

* Income figures 000’ per annum

Source: NCAER

In Indian market MNC’s are competing with domestic players in consumer

durable market in terms of technology. Organisation’s major objective is to

concentrate on middle class and rural India. Major holding by the players in durables

are by Samsung, LG, and Sony, Videocon Industries, Onida, Nokia, Samsung, Honda,

Suzuki and others. Due to availability of great choice, Indian consumer is now

replacing their exiting products with modem technological products like in automatic

watches, colour televisions with multiple features, gas-stoves, mobiles with CDMA

technology and more mileage vehicles. These categories are boosting the sales. Indian

consumer electronics industry exports are increasing every year 52.

1.10.2 Demographic Classifications India officially classifies its population in five

groups, based on annual household income (based on year 1995-96 indices)53. These

44

groups are: Lower Income; three subgroups of Middle Income; and Higher Income.

However, the rupee income classifications by themselves do not present a realistic

picture of market potential for a foreign business enterprise, because of significant

differences in purchase power from the parities of various groups. In fact, the Indian

rupee has a very high purchase power parity compared to its international exchange

value. For instance, value for the money, the domestic purchasing power of a rural

consumer is low, where as the consumption for equivalent needs and services. As a

result, India ranks fifth in the world, on purchase power parity terms, despite having

low per capita national income (US$ 340 per capita).

1.10.3Consumer Classes

Even discounting the purchase power parity factor, income classifications do not

serve as an effective indicator of ownership and consumption trends in the economy.

NCAER, has released an alternative classification system based on consumption

indicators, which is more relevant for ascertaining consumption patterns of various

classes of goods in rural markets.

There are five classes of consumer households, ranging from the destitute to the

highly affluent, which differ considerably in their consumption behavior and

ownership patterns across various categories of goods. These classes exist in urban as

well as rural households both, and consumption trends may differ significantly

between similar income households in urban and rural areas.

45

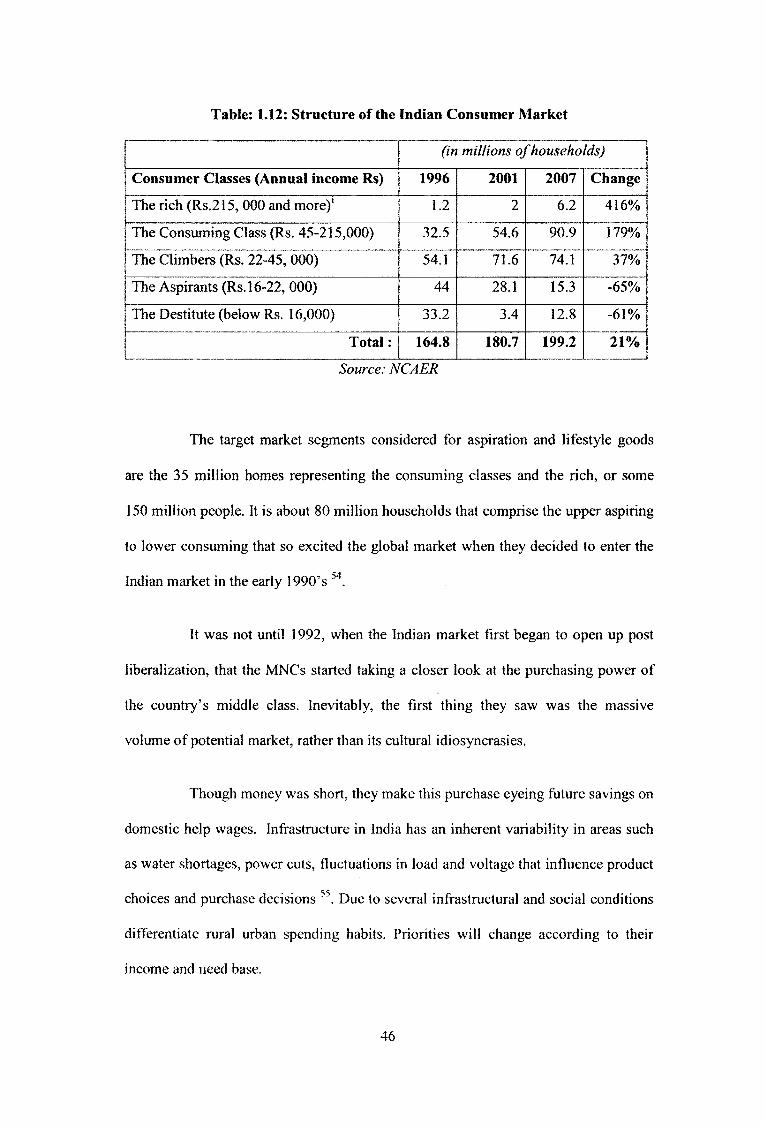

Table: 1.12: Structure of the Indian Consumer Market

(in millions of households)

Consumer Classes (Annual income Rs) 1996 2001 2007 Change

The rich (Rs.215, 000 and more)1 1.2 2 6.2 416%

The Consuming Class (Rs. 45-215,000) 32.5 54.6 90.9 179%

The Climbers (Rs. 22-45, 000) 54.1 71.6 74.1 37%

The Aspirants (Rs. 16-22, 000) 44 28.1 15.3 -65%

The Destitute (below Rs. 16,000) 33.2 3.4 12.8 -61%

Total: 164.8 180.7 199.2 21%

Source: NCAER

The target market segments considered for aspiration and lifestyle goods

are the 35 million homes representing the consuming classes and the rich, or some

150 million people. It is about 80 million households that comprise the upper aspiring

to lower consuming that so excited the global market when they decided to enter the

Indian market in the early 1990's 54.

It was not until 1992, when the Indian market first began to open up post

liberalization, that the MNCs started taking a closer look at the purchasing power of

the country’s middle class. Inevitably, the first thing they saw was the massive

volume of potential market, rather than its cultural idiosyncrasies.

Though money was short, they make this purchase eyeing future savings on

domestic help wages. Infrastructure in India has an inherent variability in areas such

as water shortages, power cuts, fluctuations in load and voltage that influence product

choices and purchase decisions 55. Due to several infrastructural and social conditions

differentiate rural urban spending habits. Priorities will change according to their

income and need base.

46

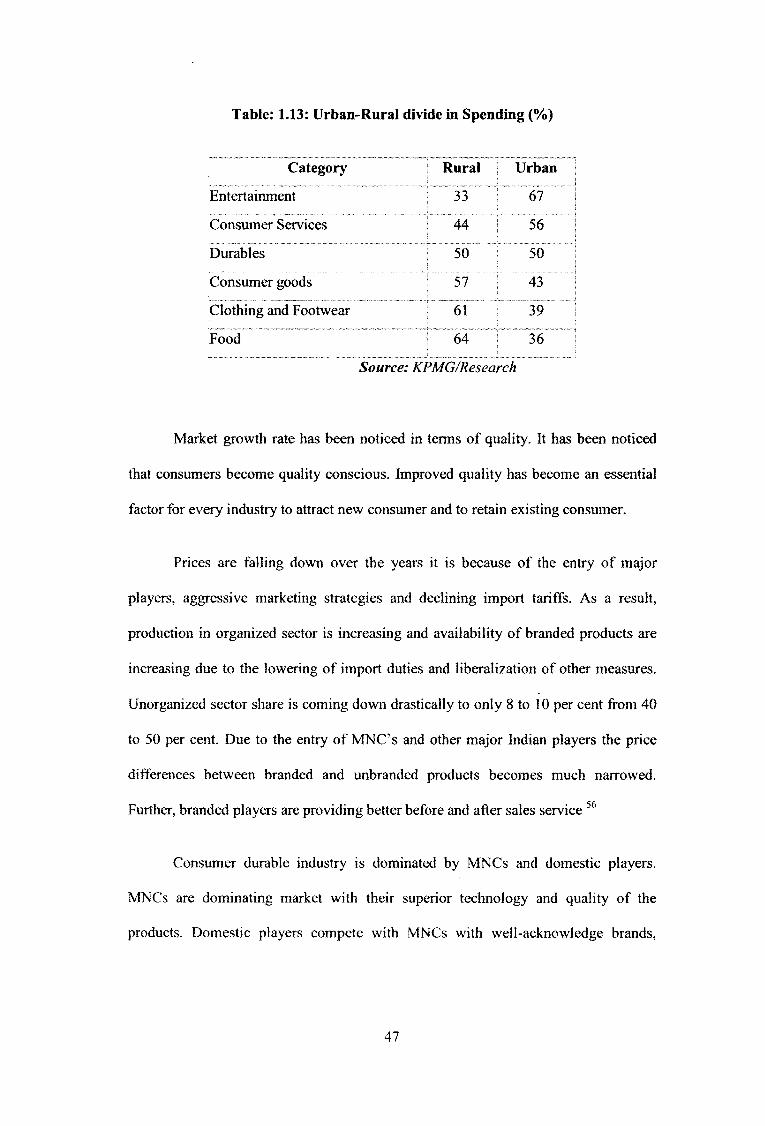

Table: 1.13: Urban-Rural divide in Spending (%)

Category | Rural Urban

Entertainment ............r 33......1 ...... 67.....

Consumer Services j 44 j... . 56....

Durables 50 50

Consumer goods ........... |........57....... .........43....

Clothing and Footwear ............[...... 61 ...... ] '.... ....39....

Food ... T.....64.. ... ] ....“"36”

Source: KPMG/Research

Market growth rate has been noticed in terms of quality. It has been noticed

that consumers become quality conscious. Improved quality has become an essential

factor for every industry to attract new consumer and to retain existing consumer.

Prices are falling down over the years it is because of the entry of major

players, aggressive marketing strategies and declining import tariffs. As a result,

production in organized sector is increasing and availability of branded products are

increasing due to the lowering of import duties and liberalization of other measures.

Unorganized sector share is coming down drastically to only 8 to 10 per cent from 40

to 50 per cent. Due to the entry of MNC’s and other major Indian players the price

differences between branded and unbranded products becomes much narrowed.

Further, branded players are providing better before and after sales service 56

Consumer durable industry is dominated by MNCs and domestic players.

MNCs are dominating market with their superior technology and quality of the

products. Domestic players compete with MNCs with well-acknowledge brands,

47

extensive distribution network by understanding local market conditions. Both the

players are formulating different marketing strategies with differentiating prices.

1.10.4 Opportunities and Potentialities for Future Growth

The growth of GDP, rising purchasing power of people with higher propensity

to consume with preference for sophisticated brands would provide constant impetus

to growth of white goods industry. Penetration of consumer durables would be deeper

in rural India due to the promotional strategies by the organizations. Organizations are

providing better schemes for rural poor in terms of financial assistance and incentive

schemes to attract towards white goods industry 57.

Consumer durable industry is facing lower growth due to the saturation in the

urban markets. This leads wide scope for rural markets. Rural consumers can be

attracted by providing easy payable consumer finance schemes and basic services,

after sales service to suit the infrastructure and existing amenities. Generally, rural

consumers buy durables form nearest towns.