Embed Size (px)

Citation preview

join the Future now

Power Distribution Tariffs in India 2016 – Discom Wise & Consumer Wise Comprehensive Track

E-REP Fact Factor Series

March 2016

© ENINCON LLP 2016, All rights reserved

Research Base Power Distribution Tariffs in India 2016| 2

CERC Final tariff

Regulations for 2014-

19 tightens power

plant’s operating

norms

ILLUSTRATIVE

join the Future now

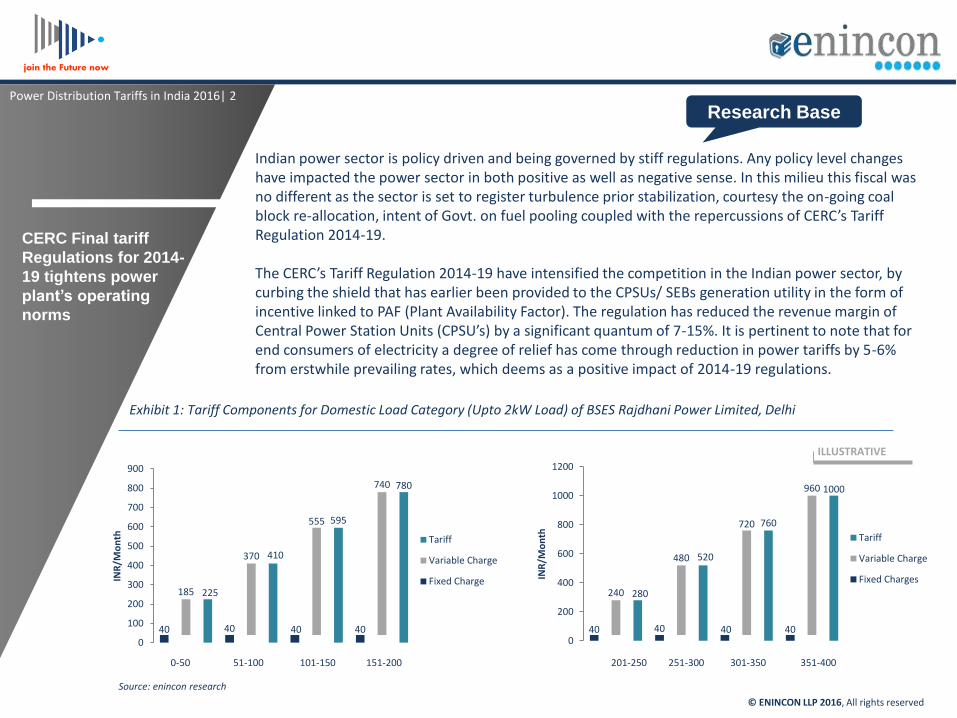

Indian power sector is policy driven and being governed by stiff regulations. Any policy level changes have impacted the power sector in both positive as well as negative sense. In this milieu this fiscal was no different as the sector is set to register turbulence prior stabilization, courtesy the on-going coal block re-allocation, intent of Govt. on fuel pooling coupled with the repercussions of CERC’s Tariff Regulation 2014-19. The CERC’s Tariff Regulation 2014-19 have intensified the competition in the Indian power sector, by curbing the shield that has earlier been provided to the CPSUs/ SEBs generation utility in the form of incentive linked to PAF (Plant Availability Factor). The regulation has reduced the revenue margin of Central Power Station Units (CPSU’s) by a significant quantum of 7-15%. It is pertinent to note that for end consumers of electricity a degree of relief has come through reduction in power tariffs by 5-6% from erstwhile prevailing rates, which deems as a positive impact of 2014-19 regulations.

40 40 40 40

185

370

555

740

225

410

595

780

0

100

200

300

400

500

600

700

800

900

INR

/Mo

nth

Tariff

Variable Charge

Fixed Charge

40 40 40 40

240

480

720

960

280

520

760

1000

0

200

400

600

800

1000

1200

INR

/Mo

nth

Tariff

Variable Charge

Fixed Charges

Exhibit 1: Tariff Components for Domestic Load Category (Upto 2kW Load) of BSES Rajdhani Power Limited, Delhi

Source: enincon research

0-50 51-100 101-150 151-200 201-250 251-300 301-350 351-400

© ENINCON LLP 2016, All rights reserved

© ENINCON LLP 2016, All rights reserved

Power Distribution Tariffs in India 2016 | 3

Research Base

join the Future now

ILLUSTRATIVE Fuel pooling has seen partial acceptance, as coal pooling is still under consideration. Gas pooling will help in reviving up 16 GW of stranded capacity and as Government of India is providing subsidy to check the tariff at INR 5.50. Only future will unveil the extent of benefit to the gas based power plants. The coal pooling would be positive for the stranded capacity, but it would be negative for the government run power generation utilities or the ones having FSA (Fuel Supply Agreement) with CIL. The coal pooling was anticipated to increase the power tariff by INR 0.40- 0.50 per unit during FY 2015-16, but the same would be much lower during this fiscal, ie- FY 2016-17. Such happenings when clubbed generates an imperative need for a dossier which would examine the tariffs as per end consumers. Hence, by meticulously examining the regulation, the latest trends governing the key fuel resources and deeply analysing the possible impacts on all the stakeholders, enincon llp attempts to blend the factual power tariff data and present a dossier which would be first of its kind and would enable clients with reliable insights and better understanding of the power tariff dynamics in the country.

Exhibit 3: Consumer Category Classification

25%

20%

20%

10%

25%

Domestic

Non-domestic

Industrial

Agricultural

Others

Key Highlights of CERC Final Tariff Regulation for 2014-19: New Formula for calculation of Fuel Cost Tightening of Operating Efficiency Norms Actual PLF Linked Incentives Tax Payment on Actual Basis Instead of Gross-up at

Applicable Tax Rate Lower NAPAF for recovery of Fixed Charges Lower Fuel Stock Allowed for Normative Working

Capital

Source: enincon research

“Power Distribution

Tariff in India-2016” gives better understanding

and reliable insights of

power tariff dynamics in the

country

© ENINCON LLP 2016, All rights reserved

ENINCON Research &

Services Framework

Research Reports

ENINCON Research

Desk

Business Stakeholders/Partic

ipants

Experts Insights/ Market view

Validated data & analysis

Opportunity mapping

& Market sizing

First hand sector

knowledge & inputs

Gist of the report in .pdf

format for ready use

Free Author

support on report & Competitive

cost

Customized Research Solution

Primary research

inputs from F2F

interviews

Germinates from minds that think fresh to evolve path finding guide for all stake holders through quality information & analyses

ENINCON’S Service Difference

Exhibit 4: ENINCON’s Difference

Emanates from seamless integration of domain expertise with first hand industry knowledge and customized research solutions at a very competitive cost

ENINCON’S Research Difference

ENINCON’s Difference

ENINCON

The Report gives

a comprehensive

track of all

existing and

upcoming Captive

Power Plants of

India, bifurcated

as per fuel used

Power Distribution Tariffs in India 2016| 4

ILLUSTRATIVE

join the Future now

Re

sear

ch O

bje

ctiv

e

Re

sear

ch R

esu

lts

1. To tabulate New tariff Structure for 2014

2. To analyze the pressure on power generating utilities with incentives linked to PLF instead of PAF

3. To study the impact on the various stakeholders of the supply chain due to these regulations

4. To analyse cost of supply and cost of procurement of power from the perspective of distribution utility

Research Objective

Exhibit 5: ENINCON Research Objective & Key Queries Resolved

© ENINCON LLP 2016, All rights reserved

ENINCON Research reports

delivering domain

knowledge, market

insights & future

outlook

Power Distribution Tariff in India 2016 | 5

• What is likely rationale behind tariff calculations followed in India for 2014-19?

• What are the key impacts on the

stakeholders due to these regulations?

• What would be the cost of power

supply and cost of procurement vis-à-vis from power distribution utility’s perspective?

• How this tariff regime impacted the

generating utilities?

Key

Qu

eri

es

Re

solv

ed

ILLUSTRATIVE

join the Future now

© ENINCON LLP 2016, All rights reserved

Exhibit 6: Key Queries Resolved will be helpful for

Power Generating Companies, Power Distribution Utilities

Research agencies, FI institutions

Bulk Consumers

Govt. & Regulatory

Bodies

Industries

ENINCON Research reports

delivering domain

knowledge, market

insights & future

outlook

Power Distribution Tariff in India 2016 | 6

ILLUSTRATIVE

join the Future now

Mu

st B

uy

For

Mu

st B

uy

For

Power Generating Companies

Power Distribution Companies

EPC Companies

Fuel Supplying Companies

Energy Sector Professionals

Energy Trading Companies

Equipment Manufacturers

FII’s/Banks

Government bodies

Educational Institutions

NGOs

IT Service Providers

Consultants

Research firms

Research Bodies/Institutes

Industry associations

Engineering Firms

Must Buy For

Exhibit 7: Must Buy For

© ENINCON LLP 2016, All rights reserved

ENINCON Research reports

delivering domain

knowledge, market

insights & future

outlook

Power Distribution Tariff in India 2016 | 7

ILLUSTRATIVE

join the Future now

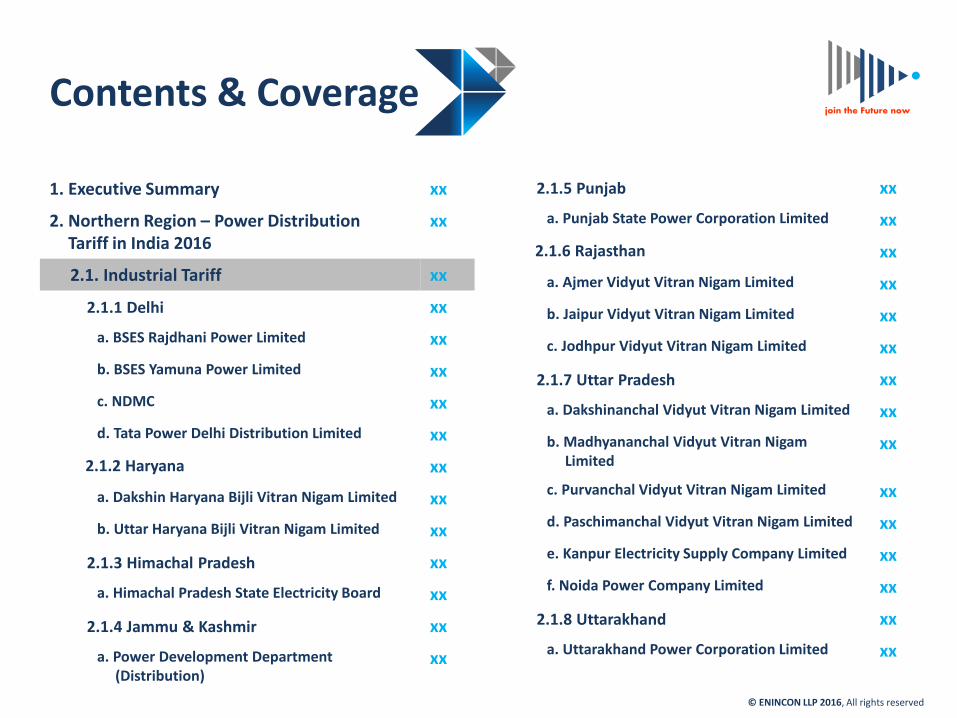

Contents & Coverage

© ENINCON LLP 2016, All rights reserved

join the Future now

1. Executive Summary xx

2. Northern Region – Power Distribution Tariff in India 2016

xx

2.1. Industrial Tariff xx

2.1.1 Delhi xx

a. BSES Rajdhani Power Limited xx

b. BSES Yamuna Power Limited xx

c. NDMC xx

d. Tata Power Delhi Distribution Limited xx

2.1.2 Haryana xx

a. Dakshin Haryana Bijli Vitran Nigam Limited xx

b. Uttar Haryana Bijli Vitran Nigam Limited xx

2.1.3 Himachal Pradesh xx

a. Himachal Pradesh State Electricity Board xx

2.1.4 Jammu & Kashmir xx

a. Power Development Department (Distribution)

xx

2.1.5 Punjab xx

a. Punjab State Power Corporation Limited xx

2.1.6 Rajasthan xx

a. Ajmer Vidyut Vitran Nigam Limited xx

b. Jaipur Vidyut Vitran Nigam Limited xx

c. Jodhpur Vidyut Vitran Nigam Limited xx

2.1.7 Uttar Pradesh xx

a. Dakshinanchal Vidyut Vitran Nigam Limited xx

b. Madhyananchal Vidyut Vitran Nigam Limited

xx

c. Purvanchal Vidyut Vitran Nigam Limited xx

d. Paschimanchal Vidyut Vitran Nigam Limited xx

e. Kanpur Electricity Supply Company Limited xx

f. Noida Power Company Limited xx

2.1.8 Uttarakhand xx

a. Uttarakhand Power Corporation Limited xx

Contents & Coverage

© ENINCON LLP 2016, All rights reserved

join the Future now

2.2. Commercial Tariff xx

2.2.1 Delhi xx

a. BSES Rajdhani Power Limited xx

b. BSES Yamuna Power Limited xx

c. NDMC xx

d. Tata Power Delhi Distribution Limited xx

2.2.2 Haryana xx

a. Dakshin Haryana Bijli Vitran Nigam Limited xx

b. Uttar Haryana Bijli Vitran Nigam Limited xx

2.2.3 Himachal Pradesh xx

a. Himachal Pradesh State Electricity Board xx

2.2.4 Jammu & Kashmir xx

a. Power Development Department (Distribution)

xx

2.2.5 Punjab xx

a. Punjab State Power Corporation Limited xx

2.2.6 Rajasthan xx

a. Ajmer Vidyut Vitran Nigam Limited xx

b. Jaipur Vidyut Vitran Nigam Limited xx

c. Jodhpur Vidyut Vitran Nigam Limited xx

2.2.7 Uttar Pradesh xx

a. Dakshinanchal Vidyut Vitran Nigam Limited xx

b. Madhyananchal Vidyut Vitran Nigam Limited

xx

c. Purvanchal Vidyut Vitran Nigam Limited xx

d. Paschimanchal Vidyut Vitran Nigam Limited xx

e. Kanpur Electricity Supply Company Limited xx

f. Noida Power Company Limited xx

2.2.8 Uttarakhand xx

a. Uttarakhand Power Corporation Limited xx

2.3. Agricultural Tariff xx

Contents & Coverage

© ENINCON LLP 2016, All rights reserved

join the Future now

2.3.1 Delhi xx

a. BSES Rajdhani Power Limited xx

b. BSES Yamuna Power Limited xx

c. NDMC xx

d. Tata Power Delhi Distribution Limited xx

2.3.2 Haryana xx

a. Dakshin Haryana Bijli Vitran Nigam Limited xx

b. Uttar Haryana Bijli Vitran Nigam Limited xx

2.3.3 Himachal Pradesh xx

a. Himachal Pradesh State Electricity Board xx

2.3.4 Jammu & Kashmir xx

a. Power Development Department (Distribution)

xx

2.3.5 Punjab xx

a. Punjab State Power Corporation Limited xx

2.3.6 Rajasthan xx

a. Ajmer Vidyut Vitran Nigam Limited xx

b. Jaipur Vidyut Vitran Nigam Limited xx

c. Jodhpur Vidyut Vitran Nigam Limited xx

2.3.7 Uttar Pradesh xx

a. Dakshinanchal Vidyut Vitran Nigam Limited xx

b. Madhyananchal Vidyut Vitran Nigam Limited

xx

c. Purvanchal Vidyut Vitran Nigam Limited xx

d. Paschimanchal Vidyut Vitran Nigam Limited xx

e. Kanpur Electricity Supply Company Limited xx

f. Noida Power Company Limited xx

2.3.8 Uttarakhand xx

a. Uttarakhand Power Corporation Limited xx

Contents & Coverage

© ENINCON LLP 2016, All rights reserved

join the Future now

2.4. Domestic Tariff xx

2.4.1 Delhi xx

a. BSES Rajdhani Power Limited xx

b. BSES Yamuna Power Limited xx

c. NDMC xx

d. Tata Power Delhi Distribution Limited xx

2.4.2 Haryana xx

a. Dakshin Haryana Bijli Vitran Nigam Limited xx

b. Uttar Haryana Bijli Vitran Nigam Limited xx

2.4.3 Himachal Pradesh xx

a. Himachal Pradesh State Electricity Board xx

2.4.4 Jammu & Kashmir xx

a. Power Development Department (Distribution)

xx

2.4.5 Punjab xx

a. Punjab State Power Corporation Limited xx

2.4.6 Rajasthan xx

a. Ajmer Vidyut Vitran Nigam Limited xx

b. Jaipur Vidyut Vitran Nigam Limited xx

c. Jodhpur Vidyut Vitran Nigam Limited xx

2.4.7 Uttar Pradesh xx

a. Dakshinanchal Vidyut Vitran Nigam Limited xx

b. Madhyananchal Vidyut Vitran Nigam Limited

xx

c. Purvanchal Vidyut Vitran Nigam Limited xx

d. Paschimanchal Vidyut Vitran Nigam Limited xx

e. Kanpur Electricity Supply Company Limited xx

f. Noida Power Company Limited xx

2.4.8 Uttarakhand xx

a. Uttarakhand Power Corporation Limited xx

2.5. Temporary Tariff xx

Contents & Coverage

© ENINCON LLP 2016, All rights reserved

join the Future now

2.5.1 Delhi xx

a. BSES Rajdhani Power Limited xx

b. BSES Yamuna Power Limited xx

c. NDMC xx

d. Tata Power Delhi Distribution Limited xx

2.5.2 Haryana xx

a. Dakshin Haryana Bijli Vitran Nigam Limited xx

b. Uttar Haryana Bijli Vitran Nigam Limited xx

2.5.3 Himachal Pradesh xx

a. Himachal Pradesh State Electricity Board xx

2.5.4 Jammu & Kashmir xx

a. Power Development Department (Distribution)

xx

2.5.5 Punjab xx

a. Punjab State Power Corporation Limited xx

2.5.6 Rajasthan xx

a. Ajmer Vidyut Vitran Nigam Limited xx

b. Jaipur Vidyut Vitran Nigam Limited xx

c. Jodhpur Vidyut Vitran Nigam Limited xx

2.5.7 Uttar Pradesh xx

a. Dakshinanchal Vidyut Vitran Nigam Limited xx

b. Madhyananchal Vidyut Vitran Nigam Limited

xx

c. Purvanchal Vidyut Vitran Nigam Limited xx

d. Paschimanchal Vidyut Vitran Nigam Limited xx

e. Kanpur Electricity Supply Company Limited xx

f. Noida Power Company Limited xx

2.5.8 Uttarakhand xx

a. Uttarakhand Power Corporation Limited xx

Contents & Coverage

© ENINCON LLP 2016, All rights reserved

join the Future now

3. Western Region – Power Distribution Tariff in India 2016

xx

3.1. Industrial Tariff xx

3.1.1 Chhattisgarh xx

a. Chhattisgarh State Power Distribution Company Ltd.

xx

3.1.2 Gujarat xx

a. Dakshin Gujarat Vij Company Ltd. xx

b. Madhya Gujarat Vij Company Ltd. xx

c. Paschim Gujarat Vij Company Ltd. xx

d. Uttar Gujarat Vij Company Ltd. xx

e. Torrent Power Ltd. xx

f. Torrent Power Ltd. xx

3.1.3 Madhya Pradesh xx

a. Madhya Pradesh Paschim Kshetra Vidyut Vitaran Company Ltd.

xx

b. Madhya Pradesh Poorv Kshetra Vidyut Vitaran Company Ltd.

xx

c. Madhya Pradesh Madhya Kshetra Vidyut Vitaran Company Ltd.

xx

3.1.4 Maharashtra xx

a. BEST Undertaking xx

b. Maharashtra State Electricity Distribution Co. Ltd.

xx

c. Reliance Energy Ltd. xx

d. TATA Power Ltd. xx

3.1.5 Goa xx

a. Electricity Department, Goa xx

3.2. Commercial Tariff xx

3.2.1 Chhattisgarh xx

a. Chhattisgarh State Power Distribution Company Ltd.

xx

Contents & Coverage

© ENINCON LLP 2016, All rights reserved

join the Future now

3.2.2 Gujarat xx

a. Dakshin Gujarat Vij Company Ltd. xx

b. Madhya Gujarat Vij Company Ltd. xx

c. Paschim Gujarat Vij Company Ltd. xx

d. Uttar Gujarat Vij Company Ltd. xx

e. Torrent Power Ltd. xx

f. Torrent Power Ltd. xx

3.2.3 Madhya Pradesh xx

a. Madhya Pradesh Paschim Kshetra Vidyut Vitaran Company Ltd.

xx

b. Madhya Pradesh Poorv Kshetra Vidyut Vitaran Company Ltd.

xx

c. Madhya Pradesh Madhya Kshetra Vidyut Vitaran Company Ltd.

xx

3.2.4 Maharashtra xx

a. BEST Undertaking xx

b. Maharashtra State Electricity Distribution Co. Ltd.

xx

c. Reliance Energy Ltd. xx

d. TATA Power Ltd. xx

3.2.5 Goa xx

a. Electricity Department, Goa xx

3.3. Agricultural Tariff xx

3.3.1 Chhattisgarh xx

a. Chhattisgarh State Power Distribution Company Ltd.

xx

3.3.2 Gujarat xx

a. Dakshin Gujarat Vij Company Ltd. xx

b. Madhya Gujarat Vij Company Ltd. xx

c. Paschim Gujarat Vij Company Ltd. xx

d. Uttar Gujarat Vij Company Ltd. xx

e. Torrent Power Ltd. xx

Contents & Coverage

© ENINCON LLP 2016, All rights reserved

join the Future now

f. Torrent Power Ltd. xx

3.3.3 Madhya Pradesh xx

a. Madhya Pradesh Paschim Kshetra Vidyut Vitaran Company Ltd.

xx

b. Madhya Pradesh Poorv Kshetra Vidyut

Vitaran Company Ltd.

xx

c. Madhya Pradesh Madhya Kshetra Vidyut Vitaran Company Ltd.

xx

3.3.4 Maharashtra xx

a. BEST Undertaking xx

b. Maharashtra State Electricity Distribution Co. Ltd.

xx

c. Reliance Energy Ltd. xx

d. TATA Power Ltd. xx

3.3.5 Goa xx

a. Electricity Department, Goa xx

3.4. Domestic Tariff xx

3.4.1 Chhattisgarh xx

a. Chhattisgarh State Power Distribution Company Ltd.

xx

3.4.2 Gujarat xx

a. Dakshin Gujarat Vij Company Ltd. xx

b. Madhya Gujarat Vij Company Ltd. xx

c. Paschim Gujarat Vij Company Ltd. xx

d. Uttar Gujarat Vij Company Ltd. xx

e. Torrent Power Ltd. xx

3.4.3 Madhya Pradesh xx

a. Madhya Pradesh Paschim Kshetra Vidyut Vitaran Company Ltd.

xx

b. Madhya Pradesh Poorv Kshetra Vidyut Vitaran Company Ltd.

xx

c. Madhya Pradesh Madhya Kshetra Vidyut Vitaran Company Ltd.

xx

3.4.4 Maharashtra xx

Contents & Coverage

© ENINCON LLP 2016, All rights reserved

join the Future now

a. BEST Undertaking xx

b. Maharashtra State Electricity Distribution Co. Ltd.

xx

c. Reliance Energy Ltd. xx

d. TATA Power Ltd. xx

3.4.5 Goa xx

a. Electricity Department, Goa xx

3.5. Temporary Tariff xx

3.5.1 Chhattisgarh xx

a. Chhattisgarh State Power Distribution Company Ltd.

xx

3.5.2 Gujarat xx

a. Dakshin Gujarat Vij Company Ltd. xx

b. Madhya Gujarat Vij Company Ltd. xx

c. Paschim Gujarat Vij Company Ltd. xx

d. Uttar Gujarat Vij Company Ltd. xx

e. Torrent Power Ltd. xx

f. Torrent Power Ltd. xx

3.5.3 Madhya Pradesh xx

a. Madhya Pradesh Paschim Kshetra Vidyut Vitaran Company Ltd.

xx

b. Madhya Pradesh Poorv Kshetra Vidyut Vitaran Company Ltd.

xx

c. Madhya Pradesh Madhya Kshetra Vidyut

Vitaran Company Ltd.

xx

3.5.4 Maharashtra xx

a. BEST Undertaking xx

b. Maharashtra State Electricity Distribution Co. Ltd.

xx

c. Reliance Energy Ltd. xx

d. TATA Power Ltd. xx

3.5.5 Goa xx

Contents & Coverage

© ENINCON LLP 2016, All rights reserved

join the Future now

a. Electricity Department, Goa xx

4. Eastern Region – Power Distribution Tariff in India 2016

xx

4.1. Industrial Tariff xx

4.1.1 Bihar xx

a. Bihar State Electricity Board xx

4.1.2 Jharkhand xx

a. Damodar Valley Corporation xx

b. Jamshedpur Utility & Services Company xx

c. Bokaro Power Supply Company Pvt. Ltd. xx

d. TATA Steel Ltd. xx

4.1.3 Odisha xx

a. Central Electricity Supply Company of Orissa Ltd.

xx

b. North Eastern Electricity Supply Company of Orissa Ltd.

xx

c. Southern Electricity Supply Company of Orissa Ltd.

xx

d. Western Electricity Supply Company of Orissa Ltd.

xx

4.1.4 West Bengal xx

a. Calcutta Electricity Supply Company Ltd. xx

b. DPSC Ltd.. xx

c. Durgapur Projects Ltd. xx

d. West Bengal State Electricity Distribution Company Ltd.

xx

4.1.5 Sikkim xx

a. Energy & Power Department, Govt. of Sikkim

xx

4.2. Commercial Tariff xx

4.2.1 Bihar xx

a. Bihar State Electricity Board xx

4.2.2 Jharkhand xx

Contents & Coverage

© ENINCON LLP 2016, All rights reserved

join the Future now

a. Damodar Valley Corporation xx

b. Jamshedpur Utility & Services Company xx

c. Bokaro Power Supply Company Pvt. Ltd. xx

d. TATA Steel Ltd. xx

4.2.3 Odisha xx

a. Central Electricity Supply Company of Orissa Ltd.

xx

b. North Eastern Electricity Supply Company of Orissa Ltd.

xx

c. Southern Electricity Supply Company of Orissa Ltd.

xx

d. Western Electricity Supply Company of Orissa Ltd.

xx

4.2.4 West Bengal xx

a. Calcutta Electricity Supply Company Ltd. xx

b. DPSC Ltd.. xx

c. Durgapur Projects Ltd. xx

d. West Bengal State Electricity Distribution Company Ltd.

xx

4.2.5 Sikkim xx

a. Energy & Power Department, Govt. of Sikkim

xx

4.3. Agricultural Tariff xx

4.3.1 Bihar xx

a. Bihar State Electricity Board xx

4.3.2 Jharkhand xx

a. Damodar Valley Corporation xx

b. Jamshedpur Utility & Services Company xx

c. Bokaro Power Supply Company Pvt. Ltd. xx

d. TATA Steel Ltd. xx

4.3.3 Odisha xx

a. Central Electricity Supply Company of Orissa Ltd.

xx

Contents & Coverage

© ENINCON LLP 2016, All rights reserved

join the Future now

b. North Eastern Electricity Supply Company of Orissa Ltd.

xx

c. Southern Electricity Supply Company of Orissa Ltd.

xx

d. Western Electricity Supply Company of Orissa Ltd.

xx

4.3.4 West Bengal xx

a. Calcutta Electricity Supply Company Ltd. xx

b. DPSC Ltd.. xx

c. Durgapur Projects Ltd. xx

d. West Bengal State Electricity Distribution Company Ltd.

xx

4.3.5 Sikkim xx

a. Energy & Power Department, Govt. of Sikkim

xx

4.4. Domestic Tariff xx

4.4.1 Bihar xx

a. Bihar State Electricity Board xx

4.4.2 Jharkhand xx

a. Damodar Valley Corporation xx

b. Jamshedpur Utility & Services Company xx

c. Bokaro Power Supply Company Pvt. Ltd. xx

d. TATA Steel Ltd. xx

4.4.3 Odisha xx

a. Central Electricity Supply Company of Orissa Ltd.

xx

b. North Eastern Electricity Supply Company of Orissa Ltd.

xx

c. Southern Electricity Supply Company of Orissa Ltd.

xx

d. Western Electricity Supply Company of Orissa Ltd.

xx

4.4.4 West Bengal xx

Contents & Coverage

© ENINCON LLP 2016, All rights reserved

join the Future now

a. Calcutta Electricity Supply Company Ltd. xx

b. DPSC Ltd.. xx

c. Durgapur Projects Ltd. xx

d. West Bengal State Electricity Distribution Company Ltd.

xx

4.4.5 Sikkim xx

a. Energy & Power Department, Govt. of Sikkim

xx

4.5. Temporary Tariff xx

4.5.1 Bihar xx

a. Bihar State Electricity Board xx

4.5.2 Jharkhand xx

a. Damodar Valley Corporation xx

b. Jamshedpur Utility & Services Company xx

c. Bokaro Power Supply Company Pvt. Ltd. xx

d. TATA Steel Ltd. xx

4.5.3 Odisha xx

a. Central Electricity Supply Company of Orissa Ltd.

xx

b. North Eastern Electricity Supply Company of Orissa Ltd.

xx

c. Southern Electricity Supply Company of Orissa Ltd.

xx

d. Western Electricity Supply Company of Orissa Ltd.

xx

4.5.4 West Bengal xx

a. Calcutta Electricity Supply Company Ltd. xx

b. DPSC Ltd.. xx

c. Durgapur Projects Ltd. xx

d. West Bengal State Electricity Distribution Company Ltd.

xx

4.5.5 Sikkim xx

a. Energy & Power Department, Govt. of Sikkim

xx

Contents & Coverage

© ENINCON LLP 2016, All rights reserved

join the Future now

5. Southern Region – Power Distribution Tariff in India 2016

xx

5.1. Industrial Tariff xx

5.1.1 Andhra Pradesh xx

a. Central Power Distribution Company of A.P. Ltd.

xx

b. Eastern Power Distribution Company of A.P. Ltd.

xx

c. Northern Power Distribution Company of A.P. Ltd.

xx

d. Southern Power Distribution Company of A.P. Ltd.

xx

5.1.2 Karnataka xx

a. Bangalore Electricity Supply Company Ltd. xx

b. Chamundeshwari Electricity Supply Company Ltd.

xx

c. Gulbarga Electricity Supply Company Ltd. xx

d. Hubli Electricity Supply Company Ltd. xx

e. Mangalore Electricity Supply Company Ltd. xx

5.1.3 Tamil Nadu xx

a. Tamil Nadu Electricity Generation & Distribution Co. Ltd.

xx

5.1.4 Kerala xx

a. Kerala State Electricity Board xx

5.2. Commercial Tariff xx

5.2.1 Andhra Pradesh xx

a. Central Power Distribution Company of A.P. Ltd.

xx

b. Eastern Power Distribution Company of A.P. Ltd.

xx

c. Northern Power Distribution Company of A.P. Ltd.

xx

d. Southern Power Distribution Company of A.P. Ltd.

xx

5.2.2 Karnataka xx

Contents & Coverage

© ENINCON LLP 2016, All rights reserved

join the Future now

a. Bangalore Electricity Supply Company Ltd. xx

b. Chamundeshwari Electricity Supply Company Ltd.

xx

c. Gulbarga Electricity Supply Company Ltd. xx

d. Hubli Electricity Supply Company Ltd. xx

e. Mangalore Electricity Supply Company Ltd. xx

5.2.3 Tamil Nadu xx

a. Tamil Nadu Electricity Generation & Distribution Co. Ltd.

xx

5.2.4 Kerala xx

a. Kerala State Electricity Board xx

5.3. Agricultural Tariff xx

5.3.1 Andhra Pradesh xx

a. Central Power Distribution Company of A.P. Ltd.

xx

b. Eastern Power Distribution Company of A.P. Ltd.

xx

c. Northern Power Distribution Company of A.P. Ltd.

xx

d. Southern Power Distribution Company of A.P. Ltd.

xx

5.3.2 Karnataka xx

a. Bangalore Electricity Supply Company Ltd. xx

b. Chamundeshwari Electricity Supply Company Ltd.

xx

c. Gulbarga Electricity Supply Company Ltd. xx

d. Hubli Electricity Supply Company Ltd. xx

e. Mangalore Electricity Supply Company Ltd. xx

5.3.3 Tamil Nadu xx

a. Tamil Nadu Electricity Generation & Distribution Co. Ltd.

xx

5.3.4 Kerala xx

a. Kerala State Electricity Board xx

Contents & Coverage

© ENINCON LLP 2016, All rights reserved

join the Future now

5.4. Domestic Tariff xx

5.4.1 Andhra Pradesh xx

a. Central Power Distribution Company of A.P. Ltd.

xx

b. Eastern Power Distribution Company of A.P. Ltd.

xx

c. Northern Power Distribution Company of A.P. Ltd.

xx

d. Southern Power Distribution Company of A.P. Ltd.

xx

5.4.2 Karnataka xx

a. Bangalore Electricity Supply Company Ltd. xx

b. Chamundeshwari Electricity Supply Company Ltd.

xx

c. Gulbarga Electricity Supply Company Ltd. xx

d. Hubli Electricity Supply Company Ltd. xx

e. Mangalore Electricity Supply Company Ltd. xx

5.4.3 Tamil Nadu xx

a. Tamil Nadu Electricity Generation & Distribution Co. Ltd.

xx

5.4.4 Kerala xx

a. Kerala State Electricity Board xx

5.5. Temporary Tariff xx

5.5.1 Andhra Pradesh xx

a. Central Power Distribution Company of A.P. Ltd.

xx

b. Eastern Power Distribution Company of A.P. Ltd.

xx

c. Northern Power Distribution Company of A.P. Ltd.

xx

d. Southern Power Distribution Company of A.P. Ltd.

xx

5.5.2 Karnataka xx

a. Bangalore Electricity Supply Company Ltd. xx

Contents & Coverage

© ENINCON LLP 2016, All rights reserved

join the Future now

b. Chamundeshwari Electricity Supply Company Ltd.

xx

c. Gulbarga Electricity Supply Company Ltd. xx

d. Hubli Electricity Supply Company Ltd. xx

e. Mangalore Electricity Supply Company Ltd. xx

5.5.3 Tamil Nadu xx

a. Tamil Nadu Electricity Generation & Distribution Co. Ltd.

xx

5.5.4 Kerala xx

a. Kerala State Electricity Board xx

6. ENINCON’s Analysis xx

6.1 Intra State Discom’s Analysis xx

6.1.1 Zones with Highest Revenues xx

6.1.2 Circles with Highest Revenues xx

6.1.3 AT&C Losses xx

a. Losses Within Different Circles xx

b. Metering Efficiency of Discoms xx

c. Collection Efficiency of Discoms xx

6.1.4 Standard Operating Procedures (SOP) xx

6.1.5 Discom with Highest Degree of Automation

xx

6.1.6 Truing Up Schedule 2014-15 xx

6.2 Inter State Discom’s Analysis xx

6.2.1 Best Performing Discoms xx

6.2.2 Best Practices followed amongst Discoms

xx

6.3 CERC Tariff Regulation 2014-19 Analysis xx

6.4 Tariff Comparison 2015-16 xx

6.5 New Tariff Policy/Regulation Analysis xx

7. ENINCON’s Recommendations xx