Embed Size (px)

Citation preview

Ulster Bank Northern Ireland Purchasing Managers Index (PMI)

Includes analysis of Global, Eurozone, UK, UK Regions, NI & Republic of Ireland economic performance by sector

April 2017 Survey Update

Issued 16th May 2017

Richard RamseyChief Economist Northern Ireland

Twitter @UB_Economics

PMI SurveysPurchasing Managers’ Indexes (PMIs) are monthly surveys of private sector companies which provide an advance indication of what is happening in the private sector economy by tracking variables such as output, new orders, employment and prices across different sectors.

Index numbers are calculated from the percentages of respondents reporting an improvement, no change or decline on the previous month. These indices vary from 0 to 100 with readings of 50.0 signalling no change on the previous month. Readings above 50.0 signal an increase or improvement; readings below 50.0 signal a decline or deterioration. The greater the divergence from 50.0 the greater the rate of change (expansion or contraction). The indices are seasonally adjusted to take into consideration expected variations for the time of year, such as summer shutdowns or holidays.

< 50.0 = Contraction 50.0 = No Change > 50.0 = Expansion

Data at a sector level are more volatile and 3-month moving averages have been used to more accurately identify the broad trends.

• Global output growth (53.7) just shy of January’s 13-mth high• Growth accelerates in UK, EZ & the Republic of Ireland• Chinese composite PMI slows to a 7-month low (51.2)• Emerging Markets Composite PMI eases from 31-mth high• Eurozone composite PMI (56.8) hits a 6-yr high • Italian & Spanish PMIs hit their highest levels since Jul-07 &

Aug-15 respectively• Developed Market manufacturing PMI just shy of recent 35-

mth high with Emerging Markets slipping back to 3-mth low• UK composite PMI (56.0) accelerates to a 4-mth high with

the West Midlands (60.3) the fastest growing region• RoI business activity accelerates to a 3-mth high (58.7)• NI firms’ output growth accelerates to 54.3 – its fastest rate of

growth this year

April 2017 PMIs – Key highlights

Global output growth rate remains unchanged for services but manufacturing eases to a 3-month low

Growth accelerates in the EZ, UK & US (marginally). While Japan & China post slower rates of growth in April

Developed Markets PMI growth rate quickens to 3-mth high & Emerging Markets eases to a 3-mth low

Emerging Markets’ growth rate eases due to China, India & Russia. Brazil expands for 1st time in 26 months

Chinese services PMI hits a 11-month low with manufacturing activity slowing to a 7-month low

Italy reports its fastest rate of growth since Jul-07 with strong rates of growth recorded elsewhere

Growth in EZ services, manufacturing & construction output at or close to 6-year highs

Early indications from the PMI suggests EZ may see an acceleration in Q2 economic growth

Ireland, Spain & France top the service sector growth league with Brazil back in expansion mode too

Euro-zone & Japanese manufacturing bucks the wider trend with activity accelerating in April

Developed Markets continue to outperform the Emerging Markets

NI & UK firms report faster rates of growth in April. NI firms reporting strongest rate of growth so far in 2017

PMI suggests private sector growth stalls in Q3, rebounds in Q4 with momentum retained into Q1/Q2

2014 was the 1st year in 7 years that the 4 main indicators recorded expansion, repeated in 2015 & 2016 (& Q1* 2017)

Output, export orders & employment growth rates quicken in Q2* (April) relative to Q1

NI firms report a pick-up in output & jobs growth while the rate of growth new orders remains unchanged

RoI firms’ orders growing at a robust rate with UK growth accelerating. NI orders growth remains at a 5-mth low

NI firms no longer report rising backlogs

NI export orders growth accelerates to a 3-month high

NI’s rate of employment growth exceeds the UK for 3rd

month in a row. Both NI & UK lag behind the RoI

Input and output cost inflation eases from their recent multi-year highs

Regional Comparisons

The West & East Midlands topped the regional growth table in April with Scotland & the North East at the bottom

Scotland, the North East & NI post the weakest growth rates of all the UK regions in the 3 months to April

The RoI reported the fastest growth rate in business activity over the last year with Scotland stagnating

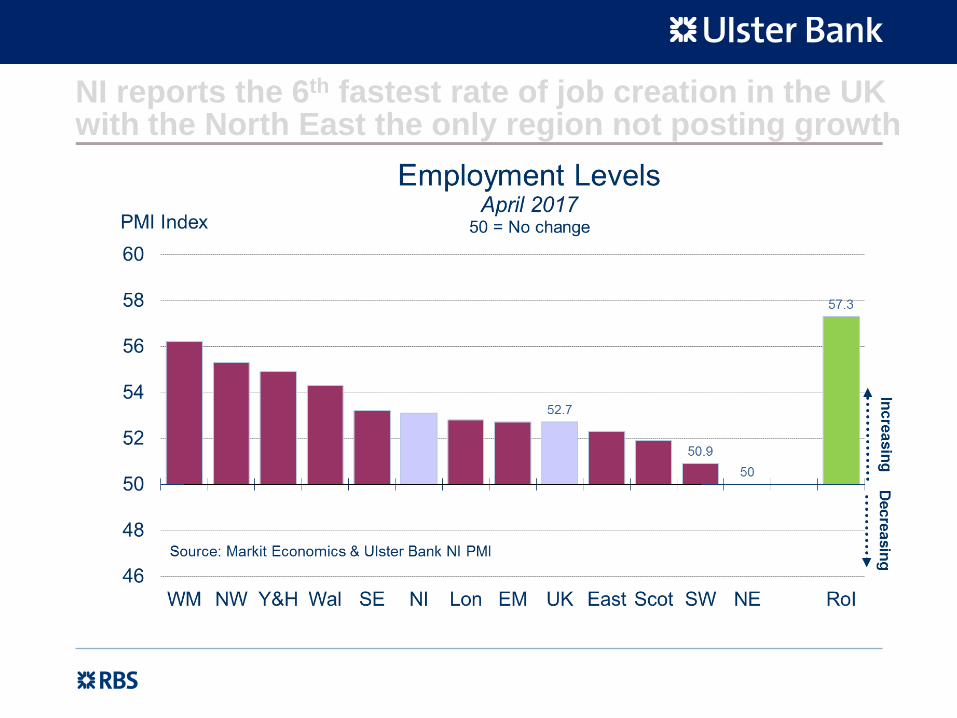

NI reports the 6th fastest rate of job creation in the UK with the North East the only region not posting growth

NI private sector employment growth outperforming the UK average over the last 3 months

Scotland & the North East (job losses) have reported the weakest rates of jobs growth over the last year

SectoralComparisons

UK output growth rates accelerate for all sectors in April

PMI suggests that UK economic growth could rebound in Q2 following a disappointing Q1

All sectors within the RoI reported faster rates of growth in April

Unlike retail & construction, NI manufacturing & services post faster rates of growth in Q2*

Service sector growth accelerates with retail slowing. Construction recovering & manufacturing slowing

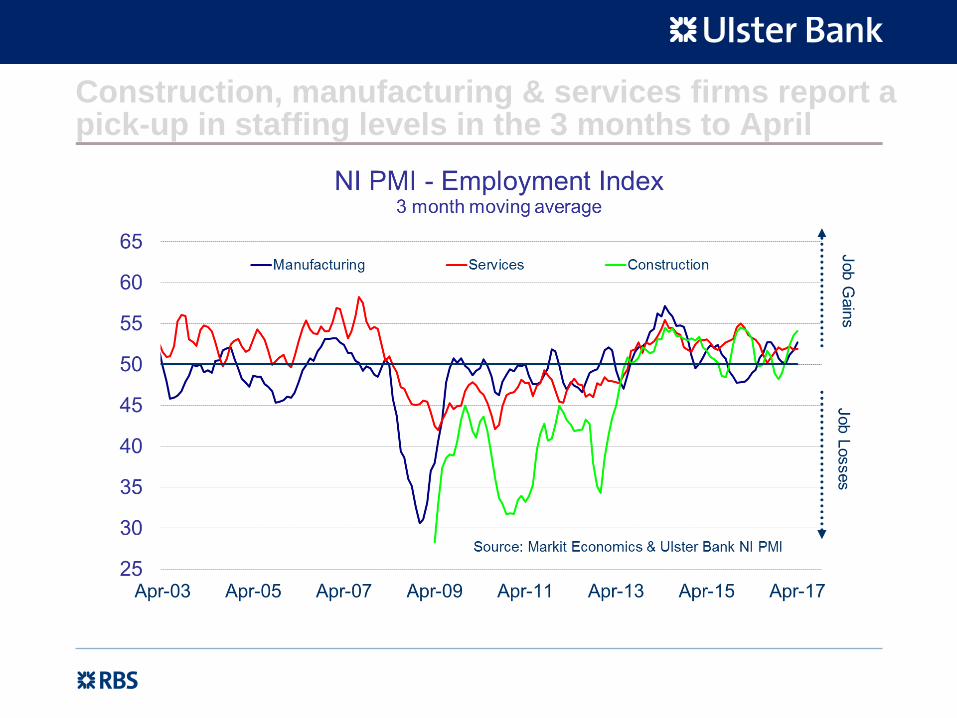

Construction, manufacturing & services firms report a pick-up in staffing levels in the 3 months to April

NI’s manufacturing firms report faster rates of growth in output, employment & new orders in the 3-mths to April

NI manufacturing output growth accelerates following its recent slowdown. UK & RoI output growth slows

NI manufacturing output growth below its pre-downturn long-term average after recent Q4 high

Rate of growth in NI & UK new orders accelerates while pace of expansion eases for RoI firms

French & Italian manufacturing output growth at a 6-year high with Greece still contracting

Sterling weakness exacerbating input cost inflation in NI & UK relative to elsewhere

Input cost inflation hits a record high in Q1 with firms also raising prices at a record rate. Some easing in April

NI & UK manufacturing firms report similar rates of growth in employment but well below those of the RoI

Output and new orders growth rates across NI’s services sector accelerates over the last 3 months

NI & UK’s services sector output growth accelerates in April but still lags behind the RoI

The growth rate in NI’s services sector remains relatively subdued & well below its pre-downturn long-term average

New orders growth rate plateaus for NI services firms and still lags well behind RoI and UK

Input cost inflation accelerates to a near 6-year high with output prices inflation more subdued

NI & UK firms report similar rates of service sector jobs growth but lagging well behind the RoI

NI retailers are still recruiting staff at a significant rate with sales and orders growth slowing rapidly

NI retailers report elevated rates of input cost inflation while output price inflation hits a record high in Q1

NI’s construction firms increasing their staffing levels but new orders are contracting again

Input cost inflation remains high with firms increasing prices at a much weaker rate

NI firms report their 2nd consecutive month of growth in March but stagnation in April

NI firms report falling orders whilst growth continues (albeit slowing) for UK & RoI firms

UK firms report increased activity for civil engineering & housing but commercial activity slows

Construction sector still reporting a shortage of sub-contractors

Optimism amongst UK construction firms is broadly in line with its long-term average

RoI housing and commercial construction activity has been improving while engineering output stagnates

RoI’s construction industry still reporting a decrease in the availability of sub-contractors & rising rates of pay

RoI construction firms still remain very optimistic about the year ahead and well above the long-term average

Slide 65

Disclaimer

This document is intended for clients of Ulster Bank Limited and Ulster Bank Ireland Limited (together and separately, "Ulster Bank") and is not intended for any other person. It does not constitute an offer or invitation to purchase or sell any instrument or to provide any service in any jurisdiction where the required authorisation is not held. Ulster Bank and/or its associates and/or its employees may have a position or engage in transactions in any of the instruments mentioned.

The information including any opinions expressed and the pricing given, is indicative, and constitute our judgement at time of publication and are subject to change without notice. The information contained herein should not be construed as advice, and is not intended to be construed as such.

This publication provides only a brief review of the complex issues discussed and recipients should not rely on information contained here without seeking specific advice on matters that concern them. Ulster Bank make no representations or warranties with respect to the information and disclaim all liability for use the recipient or their advisors make of the information.

Over-the-counter (OTC) derivatives can involve a number of significant and complex risks which are dependent on the terms of the particular transaction and your circumstances. In the event the market has moved against the transaction you have undertaken, you may incursubstantial costs if you wish to close out your position.

Calls may be recorded.