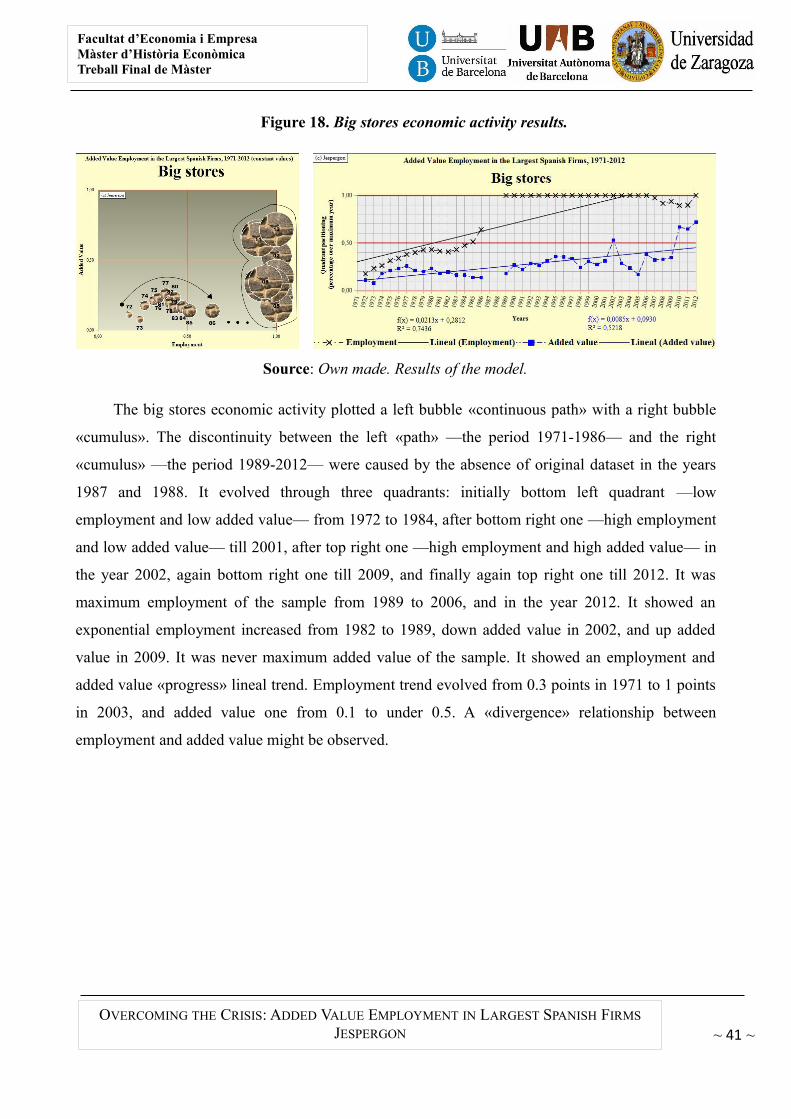

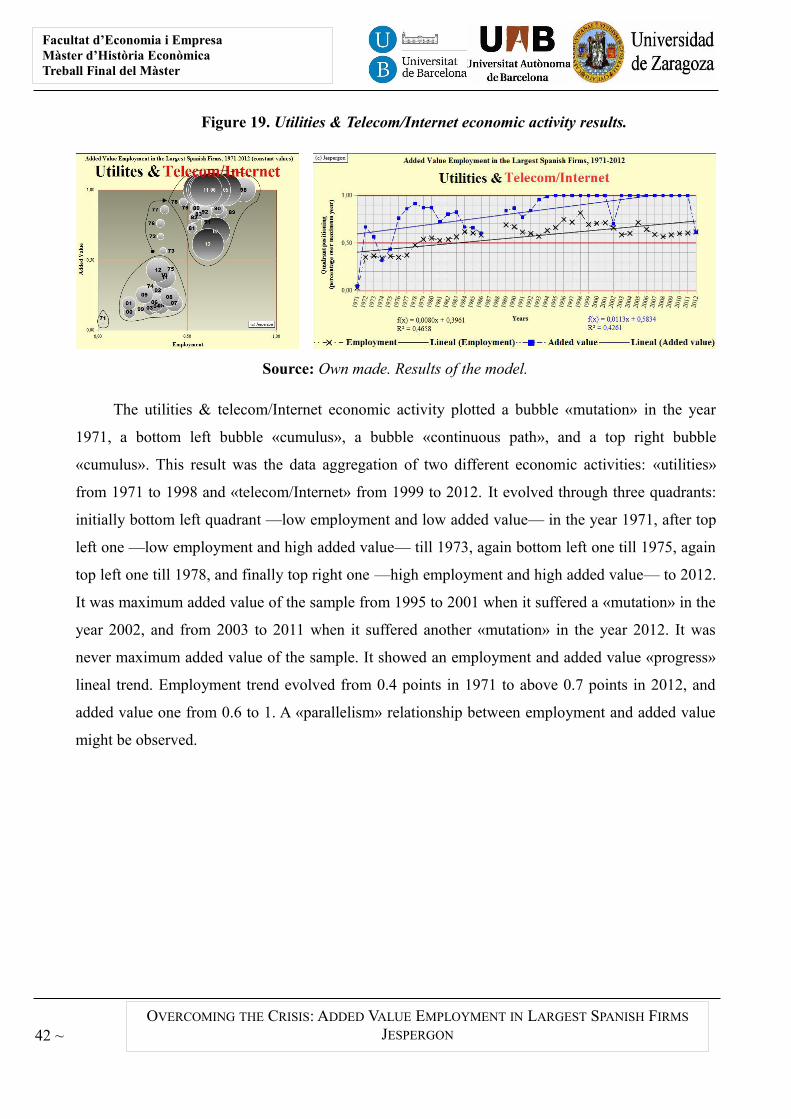

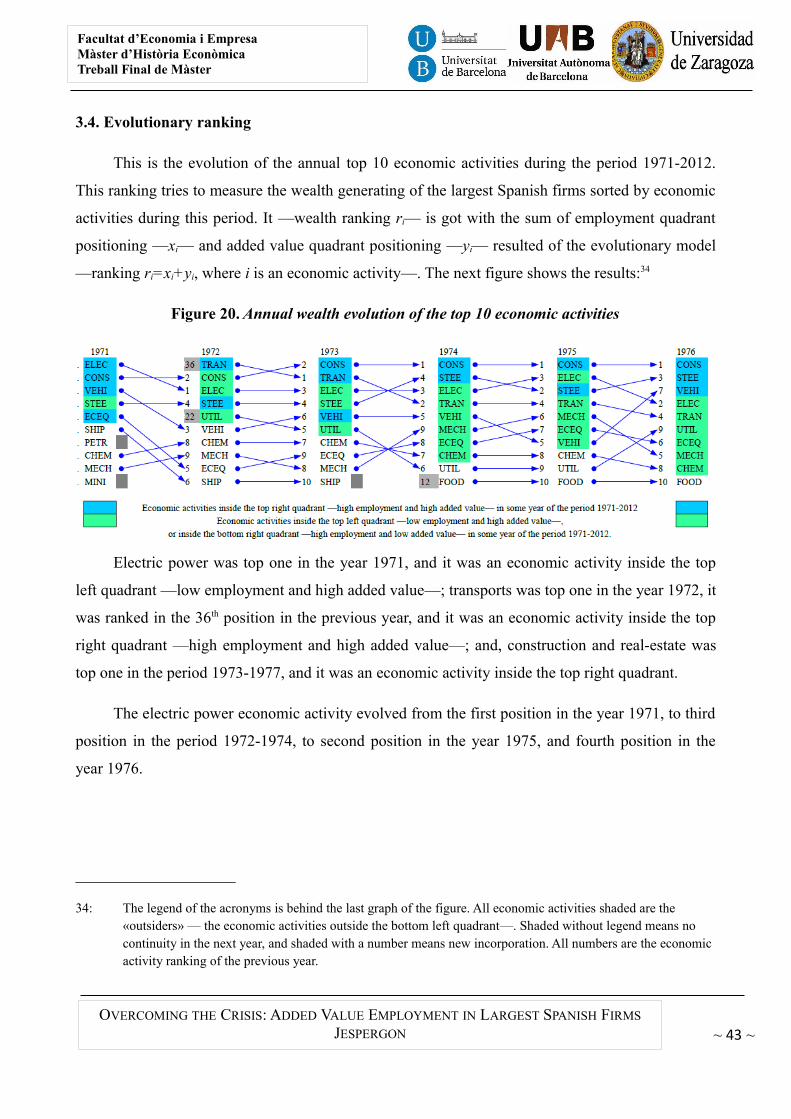

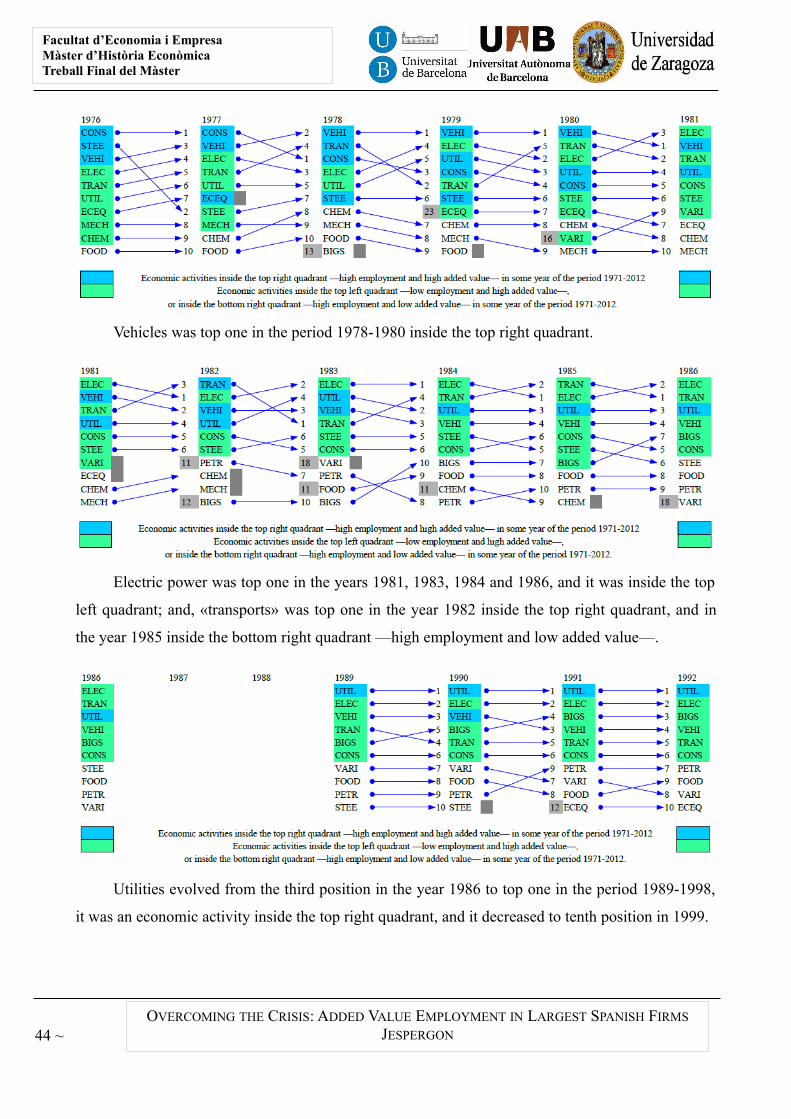

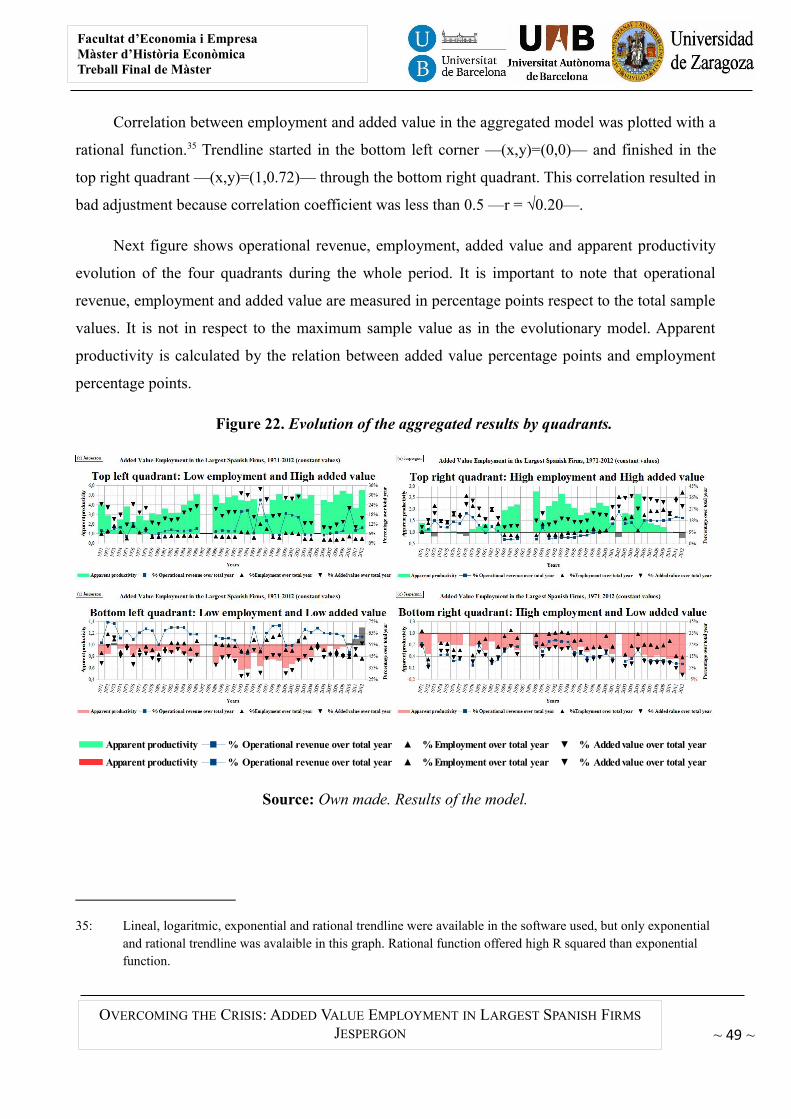

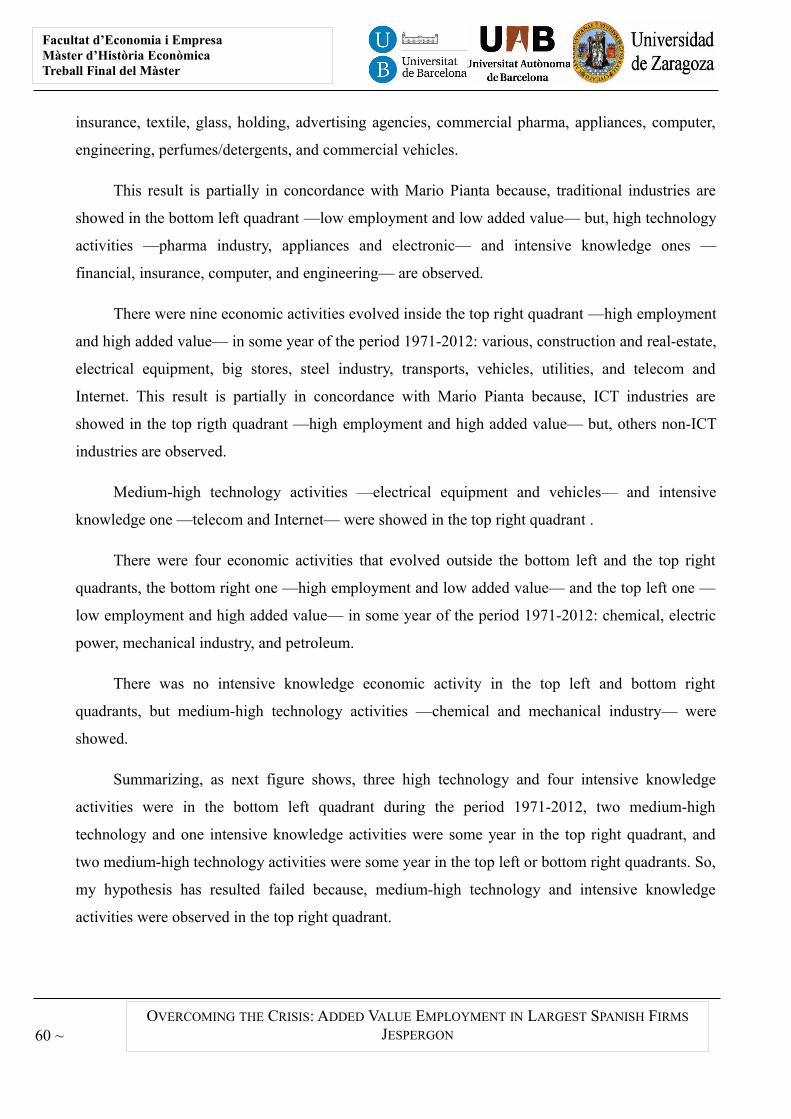

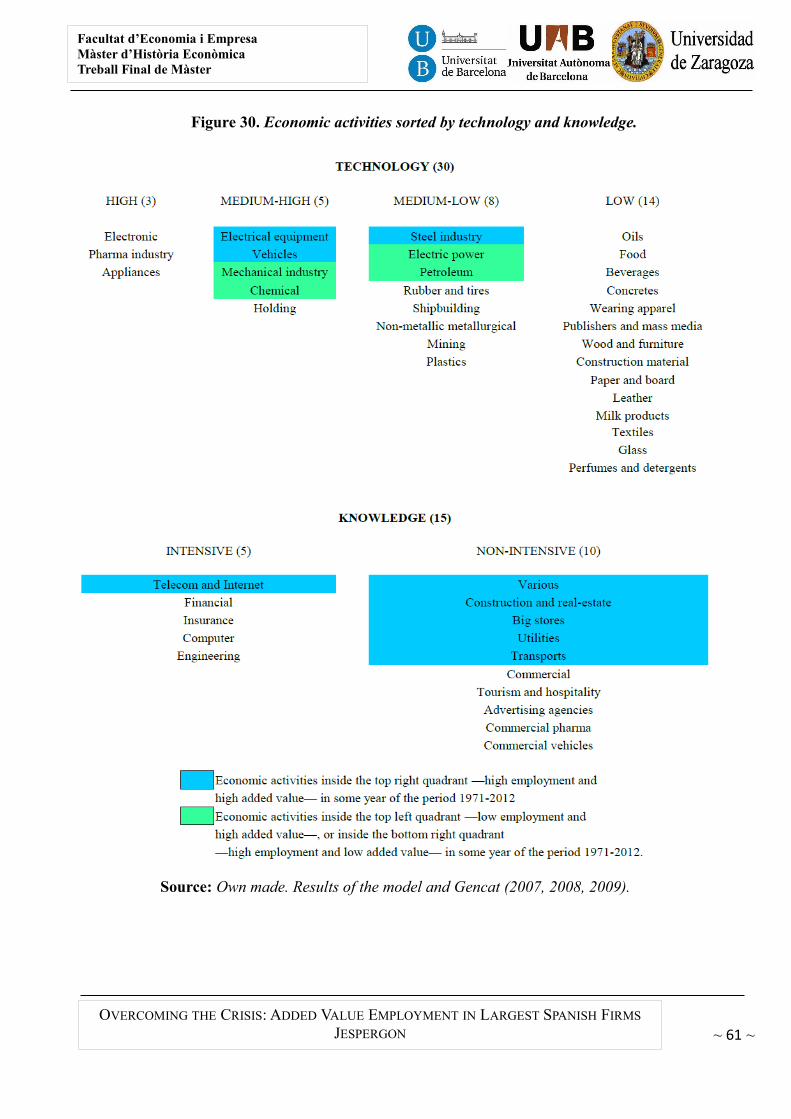

Embed Size (px)

Citation preview

570455 – Treball Final de Màster

Jesús Pérez González01/09/2014

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final del Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON 2 ~

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final de Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON

Overcoming the Crisis:

Added Value Employment in the Largest Spanish Firms, 1971-2012.

A Study of Economic Activities.

Jespergon

Final Job of the Economic History Interdisciplinary UB-UAB-UZ Master's Degree.

Supervised by Dr. Anna Mª Aubanell Jubany, UAB Professor.

Barcelona, September 1, 2014.

® Jespergon: Jesús Pérez González, 2014.

® UB: University of Barcelona, 2014.<http://www.ub.edu/histeco/cat/inici.htm>

® UAB: Autonomous University of Barcelona, 2014.<http://www.ub.edu/histeco/cat/inici.htm>

® UZ: University of Zaragoza, 2014.<http://www.unizar.es/departamentos/estructura_economica/presentacion.html>

~ 3 ~

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final del Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON 4 ~

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final de Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON

Al meu fill Vicenç

perquè el papa t'estima molt.

~ 5 ~

Cited in the page 15 of the Spanish version book

Reinvent. Your Second Chance.Dr. Mario Alonso Puig (2010).

Barcelona. Book Club.

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final del Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON 6 ~

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final de Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON

Overcoming the Crisis:

Added Value Employment in the Largest Spanish Firms, 1971-2012.

A Study of Economic Activities.

Jespergon.1 Supervised by Dr. Anna Aubanell. September 1, 2014

RESEARCH JOB IN ECONOMIC HISTORY MASTER'S (UB-UAB-UZ)

Abstract

This study describes results of the evolutionary dynamic of the economic activities, and added

value and employment trends, of the largest non-financial Spanish firms. The innovation of this

study is the performance of a longitudinal cross from 1971 to 2012. The goal is to determine which

Spanish economic activities have generated largest wealth: bigger added value and higher

employment. To carry out this mission, this study uses an evolutionary model. It is an annual

scatterplot that correlates employment, measured by quantity of jobs, and added value, measured by

monetary value, of the largest non-financial Spanish firms, measured by operational revenues. The

originality of this study is the division of the dispersion diagram into four quadrants: bottom left

one of low employment and low added value, bottom right one of high employment and low added

value, top left one of low employment and high added value, and top right one of high employment

and high added value.

Keywords: Added Value, Employment, Wealth, Spanish Economic Activities, largest Spanish

firms, Dispersion Diagram, Evolutionary Model.

JEL classification codes: A13, B52, C25, D31, E01, J21, L11, M40.

Resumen

Este estudio describe los resultados de la dinámica evolutiva de las actividades económicas y,

las tendencias de valor añadido y empleo, de las mayores empresas no financieras de España. La

innovación de este estudio es la realización de un corte longitudinal desde 1971 hasta 2012. El

1 Jespergon ©: Jesús Pérez González. <[email protected]>. Graduado en ADE por la UOC.

~ 7 ~

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final del Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON

objetivo es determinar qué actividades económicas españolas han generado mayor riqueza: mayor

valor añadido y mayor empleo. Para lleva a cabo esta misión, este estudio usa un modelo evolutivo.

Es un diagrama de dispersión annual que correlaciona empleo, medido por la cantidad de puestos de

trabajo, y valor añadido, medido por el valor monetario, de las mayores empresas españolas no

financieras, medidas por los ingresos de explotación. La originalidad de este estudio es la división

del diagrama de dispersión en cuatro cuadrantes: el inferior izquierdo de bajo empleo y bajo valor

añadido, el inferior derecho de alto empleo y bajo valor añadido, el superior izquierdo de bajo

empleo y alto valor añadido y el superior derecho de alto empleo y alto valor añadido.

Palabras clave: Valor añadido, Empleo, Riqueza, Actividades económicas españolas, mayores

empresas españolas, Diagrama de dispersión, Modelo evolucionario.

JEL classification codes: A13, B52, C25, D31, E01, J21, L11, M40.

Introduction

The major consequence of the Great Recession for Spain has been the spectacular rise of

unemployment rate. According to ILO,2 Spain scored top 5 major unemployment harmonized rate

countries in the World —behind Macedonia, Kosovo, Bosnia and Herzegovina, and South Africa

sorted from highest to lowest— in the year 2012. Unemployment harmonized annual rate in Spain

was 25.6 over Spanish active population according to EU statistics 3 or 26.4 according to OECD

database 4 at the end of the year 2013. These data was maximum Spanish unemployment rate from

1987 to 2013. According to euroindicators in January 2014,5 the EU28 and Spanish seasonally-

2: ILO. Ilostat. International Labour Organization. <http://www.ilo.org/ilostat/faces/home/statisticaldata>. [Accessed May 3, 2014].

3: EU. Eurostat. European Commission. <http://epp.eurostat.ec.europa.eu/portal/page/portal/statistics/search_database>. [Accessed April 18, 2014].

4: OECD. StatExtracts. Organisation for Economic co-Operation and Development. <http://stats.oecd.org/>. [Accessed March 2, 2014].

5: Eurostat (2014). Euro area unemployment rate at 12.0% [online open access]. European Commission. News Release Euroindicators, (30/2014 – 28 February 2014). <http://epp.eurostat.ec.europa.eu/cache/ITY_PUBLIC/3-28022014-AP/EN/3-28022014-AP-EN.PDF>. [Accessed April 2, 2014].

8 ~

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final de Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON

adjusted unemployment rate was 10.8 and 25.8 percentage points, respectively. This data have

scored Spain in the second position —behind Greece— in the ranking of major countries in the

European Union unemployment rate, and fifteen percentage points over the EU28 average.

In this context, value-added economic activities and economic growth without net

employment creation are in discussion in the Spanish society. According to Laborda,6 “the data

appear to assert greater survivability of large companies, especially those of 5,000 workers or

more”. Relevance of this study is largest Spanish firms evolution sorted by economic activities, and

its employment and added value projection in short-term.

The main question of this study is: Which Spanish economic activities had high employment

and high added value in the largest Spanish firms during the period 1971-2012? The secondary

questions are: What was the evolutionary dynamic of these economic activities? What was the

employment and added value trends of these economic activities? What were economic activities

bigger wealth generating during the period 1971-2012? Which was correlation between

employment and added value? Does data aggregation changes results of this study? Can be drawn

some projection of this study in the short-term?

For answering these questions this study is divided in seven chapters without including this

introduction and the appendices. The first chapter is the state of the art about the recent literature of

the Spanish economic activities of the big business in the last forty years. The second chapter is

about the data-set source, methodology description used in the evolutionary model, and discussion

about validity of this study. The third chapter shows results of the evolutionary model of this study,

the «microresults» of the economic activities outside the bottom left quadrant, evolutionary wealth

ranking, and the «macroresults» of the aggregation by quadrants of all economic activities. The

fourth are the answer to the questions. The fifth chapter expose conclusions may be extracted of the

results of this study. The sixth chapter are the extensions about the theme Overcoming the Crisis

that I would wish to investigate in future research with European Funds in a short time. The seventh

chapter are references. And, finally, appendix that it shows the annual results —plotted in the form

of graphics— of the evolutionary model.

6: Laborda, Anna (2012). ¿Cuántas empresas se ha llevado la crisis? Informe Económico ESADE, 12 (January, 2012), 54-63.

~ 9 ~

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final del Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON

1. Literature review

The majority of experts viewed added value as a multidimensional construct. “There is no one

definition of added value”. “There are a lot of things that could be in there and you could call all of

those added value”. “There are many ways of measuring what it means”. These views reflect the

diversity of perspectives uncovered in the literature review (de Chernatony, Harris & Dall'Olmo,

2000: 46). While some speak of «added value», others talk about «adding value» or «value-added»

(De Chernatony, Harris & Dall'Olmo, 2000: 42). In this study I use the term «added value» and it is

related to an accounting definition.

According to Gallizo (2000a), «value added» is defined by the increase of wealth generated

by the activities of a company in a given period, which is measured by the difference between the

production value reached in the period —sold, stored, and immobilized— and the procurement

related to that volume of activity. Therefore, it is a «value added production». It is also a «gross

value added» —GVA— because it does not compute depreciation and provisions in the section on

operating costs, but such provisions are considered an assignment in the distribution of value added.

It is also a «business value added» directly linked with the GVA of the National Accounts, by

obtaining a classification of income and expenses by nature. In this study the largest Spanish firms

are those who declare higher operational revenue in their annual accounts.

The production approach, which is also called the output approach, measures GDP as the

difference between the aggregation of business GVA less the value of goods and services used in

producing these outputs during an accounting period (Viet, 2009: 4-14). The total economy

comprises the following institutional sectors in the System of National Accounts:

a) Non-financial corporations (divided into public, national private, and foreign controlled);

b) Financial corporations (divided into public, national private, and foreign controlled);

c) General government;

10 ~

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final de Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON

d) Non-profit institutions serving households; and

e) Households.

The subject of this study are the largest non-financial Spanish firms.

Daems (1987: 73-91)7 developed a test to analyze the underlying factors to the growth of big

firms. He provided some puzzling facts, such as the astonishingly high level of large U.K. firms in

real per capita terms among the European countries or, on the contrary, the surprisingly low level of

Spanish large firms in the same terms. Possible explanations were low R&D levels and the revealed

comparative advantage of a country against the set of sectors more conducive to giant firms. The

comparative advantage of Spain was not conducive to the developing of trademarks, at least until

1970. Oranges and fruits, iron ore, lead, pyrites, wine, and oil were unlikely candidates for

trademarks. Even the late growth of industrial exports was linked to non trademark sectors:

shoemaking and shipbuilding. During the period 1974-1990 Spain begun to show a very

competitive profile in one particular sector typically trademark led: vehicles. Spain was one of the

major world cars exporter in 1990 (Carreras & Tafunell, 1999: 303-304).

Carreras & Tafunell (1999: 281-283) analyzed the sectoral composition of the 200 largest

Spanish firms from 1917 to 1990. In the years 1974 and 1990, ordered by the number of firms, top

five economic sectors were manufacturing, finance, utilities —electricity, gas, water, and telephone

—, construction and public works, and transports. They also showed the distribution of the fifty

largest Spanish manufacturing enterprises sorted by the SIC American sectoral breakdown.8 In the

years 1974 and 1990, the group with greater number of firms is transportation equipment in both

years, followed by chemicals in the year 1974 and electrical machinery in 1990.

This current study is conducted from the point of view of the Spanish economic activities,

rather than an industrial sector study, because service firms —the tertiary sector— are included. In

the same way, this study is not a sectoral economic study because agriculture, livestock and

fisheries —the primary sector— is not included. Summarizing, this study focuses on the largest

non-financial Spanish firms engaged in economic activities of the secondary and tertiary sectors.

7: Work cited in Carreras & Tafunell (1999: 303).

8: SIC: Standard Industrial Classification. A SIC list is online available in the Department of Labor of the United States. <https://www.osha.gov/pls/imis/sic_manual.html>. [Accessed July 17, 2014].

~ 11 ~

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final del Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON

The most important literature for this study is the Spanish book The Big Firm in Spain. A

process of concentration and dependence (Sánchez, 1998). Joan-Eugeni Sánchez 9 argued that a

double process of concentration and dependence had occurred with the largest firms that were

operating in Spain, considering these as fundamentals in the economic activity. He analyzed the

general features of the largest firms in Spain through the evolution of variables provided by the

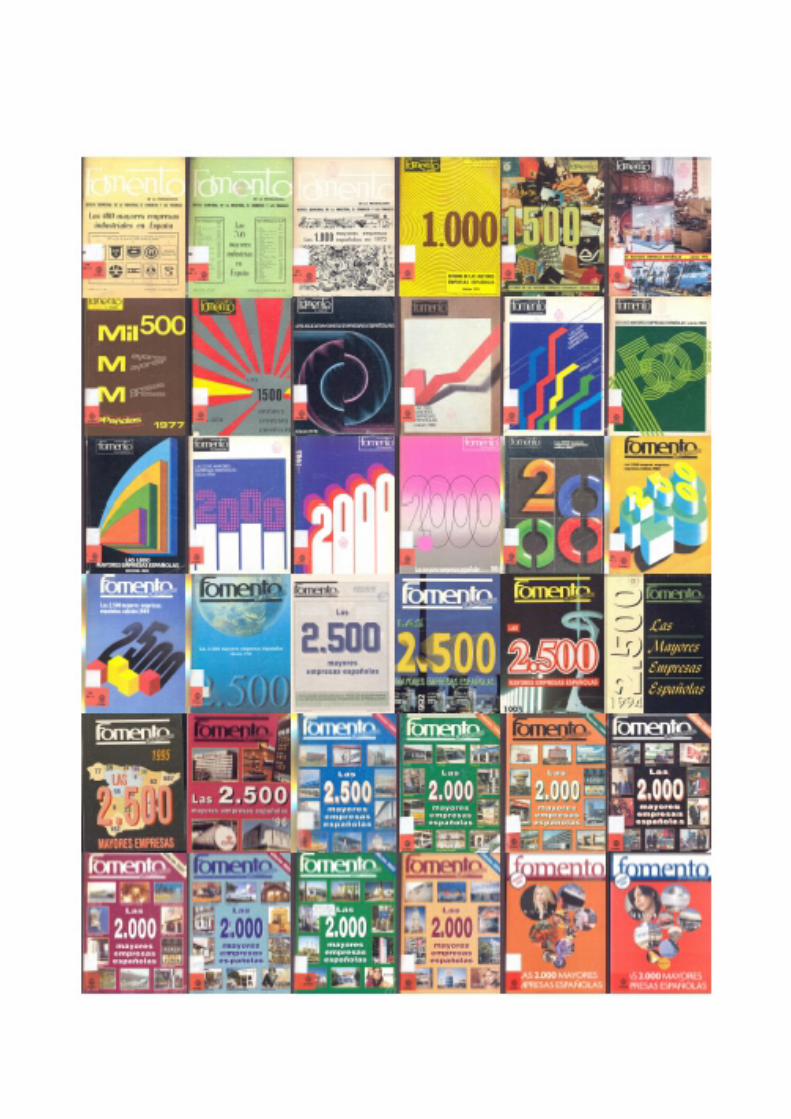

annual special issues —The (…) largest Spanish firms— of the Spanish journal Fomento de la

producción, the same dataset I have used for this study. He restricted the sample to the 1,000 largest

Spanish firms, measured by their operational revenue, so do this study but only 711 firms on

average in the period 1971-2012. He wrote an entire chapter to contextualize the structural and

cyclical trends of the Spanish economy during the period 1973-1994. He realized six cross-sections:

1973, 1976, 1981, 1986, 1991, and 1994. The innovation of this study is that I realize a longitudinal

section from 1971 to 2012 of the largest Spanish firms.

Sánchez analyzed changes in the structure of Spanish largest firms through the evolution of

the number of enterprises, operational revenue, added value, own resources, profit or loss, and

apparent and real productivity by sectors —industry, construction, and services— and by economic

activities —the first two digits of the NACE firm—. His results showed that the higher economic

activity by number of firms (table IV.2: 76) and by relative operational revenue (table IV.4: 82) was

big stores. The higher economic activity by relative added value per operational revenue was

communications (table IV.6: 88). The higher economic activity by total people employed was

construction, and by average employment per firm were rail transport in the year 1973 and

communications in 1994 (table V.2: 102). The higher economic activity by apparent productivity,

measured by added value per employee, was energy and water (table V.3: 109). The data source of

this study ends in 2006 and my desire was to get to the present, I have supplemented it with other data

source that has forced me to convert NACE 10 in the economic activities code of the first source.

There is an interesting study of Rodríguez (2011: 7) that analyzed the impact of the current

Economic Recession had on Spanish employment and GVA in 2009 through the correlation of

9: Joan-Eugeni Sánzchez is Professor of Human Geography at the University of Barcelona and scientific consultant to the Center for European Initiatives and Research Foundation in the Mediterranean —CIREM—.

10: NACE: Statistical Classification of Economic Activities in the European Community. <http://ec.europa.eu/eurostat/ramon/nomenclatures/index.cfm?TargetUrl=LST_NOM_DTL&StrNom=NACE_REV2>. [Accessed July 21, 2014]. A Spanish NACE list is online available in CNAE. <http://www.cnae.com.es/lista-actividades.php>. [Accessed July 17, 2014].

12 ~

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final de Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON

annual variation in real GVA and employment from 2008 to 2009 plotted in four quadrants. It

showed that there were 11 industries in the top right quadrant —GVA and employment growth rates

above the national average—: health, veterinary and social services; public administration;

education; personal services; domestic staff; agriculture, livestock and hunting; hospitality;11

transports and communications; real-estate and business services; food, beverages and tobacco; and,

trade and repair. There were 2 industries in the top left quadrant —GVA growth rate above the

national average and employment growth rate below the national average—: fishing and chemical.

There were 7 industries in the bottom right quadrant —GVA growth rate below the national average

and employment growth rate above the national average—: electric power, gas and water;

manufacture of coke, refined petroleum products and nuclear fuel; financial intermediation; paper,

publishing and printing; rubber and plastics; extraction of energy products; and, machinery and

equipment. Finally, there were 9 industries in the bottom left quadrant —GVA and employment

growth rates below the national average—: transport material; electrical, electronic and optical

equipment; miscellaneous articles; other mineral extraction; leather and footwear; metallurgy and

metal products; textile and confection; other non-metallic mineral products; and, wood and cork.

The originality of this study is because I analyze the correlation between added value and

employment of the secondary and tertiary economic activities of the largest non-financial Spanish

firms during the period 1971-2012 through four quadrants whose meanings are: high added value

and high employment —economic activities located in the top right quadrant—, high added value

and low employment —the top left quadrant—, low added value and high employment —the

bottom right quadrant—, and low added value and low employment —the bottom left quadrant—. I

have not found literature review with this idea.

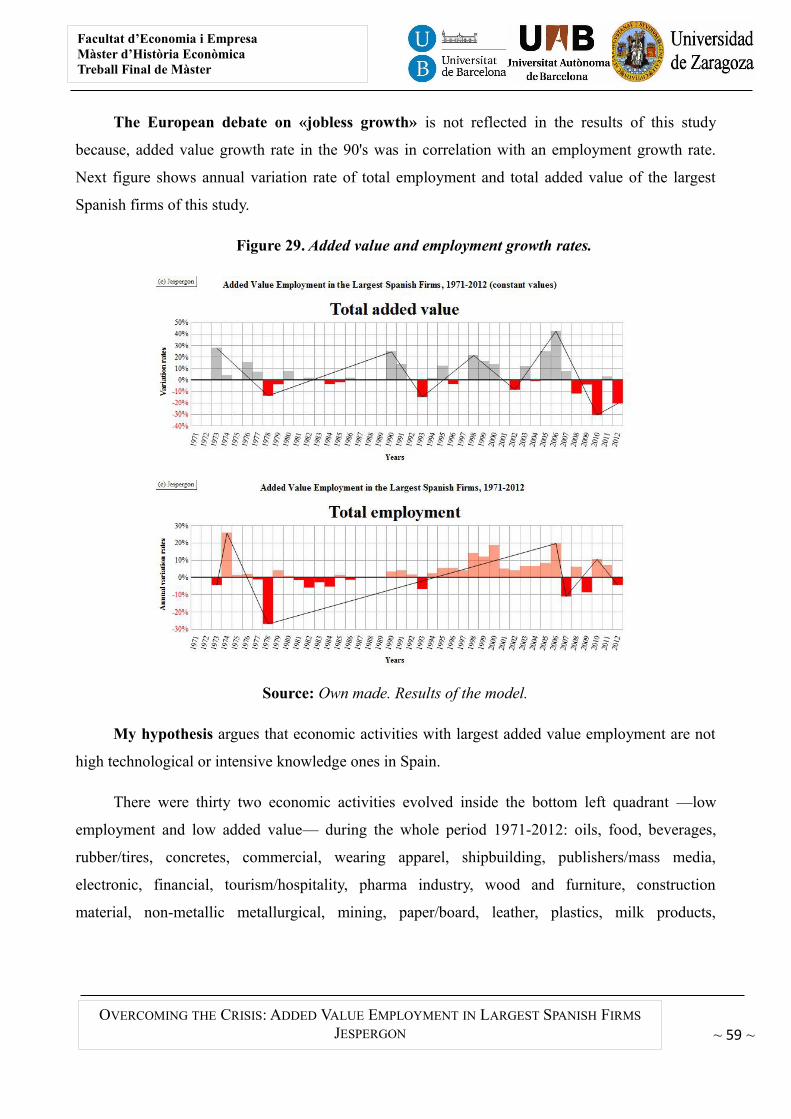

In the context of the European debate on «jobless growth» in the 1990s, Pianta (2003: 9)

explained that the evidence points to an extensive process of restructuring in many manufacturing

sectors where the growth of value added is not matched anymore by increases in jobs . The idea of

relating employment and added value emerged from Pianta (2003: 6) that related “[...] the most

accurate description of the economic relevance of innovations [measured by share of new products

in sales] to the employment performance [measured by percentage change in employment] of 20

11: Hospitality is referred to the Spanish word hostelería that means: set of services, companies and establishmentsproviding accommodation and food to travelers.

~ 13 ~

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final del Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON

manufacturing industries in four EU countries [...]” where “ICT industries (computing,

telecommunications, precision instruments and other transport, including aerospace) are generally

in the top right quadrant [...]” and “Traditional industries (textiles, wearing apparel, leather and a

few others) tend to concentrate in the bottom left quadrant [...]”. My hypothesis is that largest added

value employment economic activities would must be high technological or intensive knowledge

ones (Gencat, 2007, 2008, 2009), and these activities would be —or not— bigger employment

generating. I expect that for Spain it will not be so.

Finally, I want to point out that the idea of modeling the evolution of the economic activities

represented by the largest Spanish firms in a dispersion diagram emerged from Hans Rosling,12 and

I believe that this study is the first time Rosling evolutionary model is applied in the correlation of

added value and employment.

Summarizing, this study analyzes evolutionary dynamic of the economic activities, and added

value and employment trends, of the largest non-financial Spanish firms, measured by their

operational revenue, engaged in economic activities of the secondary and tertiary sectors during the

period 1971-2012. The goal is to determine which Spanish economic activities have generated the

largest wealth: bigger added value and higher employment.

12: Rosling, Hans (2006). “The best stats you've ever seen” [open access online]. TED. Filmed on February 2006. <http://www.ted.com/talks/hans_rosling_shows_the_best_stats_you_ve_ever_seen>. [Accessed on June 28, 2014].See also YouTube video: “Hans Rosling's 200 Countries, 200 Years, 4 Minutes – The Joy of Stats – BBC Four”. Updated on November 26, 2010. <http://www.youtube.com/watch?v=jbkSRLYSojo>. [Accessed on November 3, 2012].

14 ~

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final de Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON

2. Methodology

2.1. The source of the dataset

According to Sánchez (1998: 21), Fomento de la producción dataset is a homogeneous series,

not very common in the landscape of social and statistical information in Spain, and widely

accepted and disseminated in the Spanish business and academic fields. The availability of a series

of about 40 years and collected under the same homogeneous criteria open the option of a

diachronic analysis of great interest.

However, it is important to clarify that business data published by Fomento de la producción

are a voluntary response of the major Spanish companies at the request of the journal, and its

accuracy and veracity is understood due to the objective of social transparency in all

entrepreneurship. The authors of Fomento de la producción have supplemented the missing data

where it has been possible with other information sources, often in very few occasions for self-

esteem. Also these authors want to point out that in any case their work aims to achieve the

infallible qualification because the objective was just to get a guidance document. I subscribe all

these constraints for this study.

The idea of publishing the Spanish journal Fomento de la producción about industry,

commerce and finance in Barcelona was thanks to a journalist from Huesca called Feliciano

Baratech.13 The first exemplar published of this journal was in the year 1945 with fortnightly

appearance. Actually, this journal has a web page where is possible to consult the Spain 25,000

database.14 The query of this online database, and electronic ones —Spain 25,000, Spain 27,000 and

Spain 30,000 (Fomento de la producción, 1988-2011)—, did not produce the expected results

because added value data was not available. Of course, other database were consulted but with

13: Martí Michelena, A. (1990). “Recuerdos de un periodista”. Fomento de la producción, 1002 (Oct. 1, 1990), 8.

14: Fomento de la producción. España 25.000. Online database. <http://www.fomentodigital.com/busqueda/empresa/espana25000.jsp>. [Accessed May 3, 2014].

~ 15 ~

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final del Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON

failed results because there were not available added value data of the largest Spanish firms.15 More

over, other databases exist but with restricted access.16

So, the next step was consult the availability of the journal Fomento de la producción in the

common catalogue of the universities of Catalonia. The results of this consultation showed that

from 1970 there was a Spanish annual special issue called The (…) largest Spanish firms (Fomento

de la Producción, 1970-2006). The consult in situ of available annual special issues —the whole

collection were available in the National Library of Catalonia— show me the possibility of a

longitudinal section of the largest Spanish firms because operational revenue, quantity of

employment, added value, and economic activity classification of the largest Spanish firms were

available from 1971 to 2006. A further problem was low coverage of the variable added value.

My desire from the beginning was to finish this study closest the current year for analyzing

the involvement of the Economic Recession in Spain —from 2009 to 2013—17 on the employment

and added value of the largest non-financial firms. To meet this objective was necessary to expand

the dataset. Beyond 2006, I only found a dossier within the journal entitled “The first Spanish

15: Dun & Bradstreet (1990). Duns 15.000. Principales empresas españolas. Dun & Bradstreet España, S.A.—— (1992, 1993). Duns 30.000. Principales empresas españolas. Dun & Bradstreet España, S.A. —— (1998). Duns 50.000. Principales empresas españolas. Volumenes 1 y 2. Dun & Bradstreet España, S.A.INE. Encuesta Industrial de Empresas. <http://www.ine.es/jaxi/menu.do?

type=pcaxis&path=/t05/p048/&file=inebase&L=0>. [Accessed July 24, 2014].Banco de España. Central de Balances. <http://www.bde.es/bde/es/areas/cenbal/>. [Accessed July 17, 2014].(2002). Las 1.000 mayores empresas españolas [recurso electrónico]: contiene 6.000 balances de las 1.000

mayores empresas de los ejercicios 1996-2001. La Gaceta de los Negocios with the collaboration of Banco Santander Central Hispano.

(2004). 1.000 mayores empresas españolas [recurso electrónico]: contiene los datos del último ejercicio de las 1.000 mayores empresas españolas. La Gaceta de los Negocios.

(2003, 2005, 2007). “5.000 mayores empresas”. Revista Actualidad Económica. Madrid: Recoletos medios digitales.

16: The empirical study of Besteiro (1991) that took as reference Account 80, "Operations", of the General Accounting Plan of Spain of the year 1973, and consisted in the analyses of the components of the Added Value of Spanish companies in 1979 and 1980, investigating fifty and three sectors in the two-digit level according to NACE with a sample of 102,233 companies in 1979 and 62,545 in 1980. The database was provided by the Center for Data Processing of the State Secretary of Treasury of the Ministry of Economy and Finance of Spain, without which collaboration would have been impossible to carry out her ambitious work.Besteiro Varela, María Avelina (1991). Estudio empírico referido a los años 1979 y 1980 de los componentes

del Valor Añadido de las empresas españolas realizado con datos de la cuenta 80, «Explotación», del PlanGeneral de Contabilidad [open access in Google Scholar]. Revista Española de Financiación y Contabilidad, XXI(66), 67-193.

17: According to Eurostat, Spain had negative real GDP growth rates in the years 2009, 2010, 2012, and 2013. <http://epp.eurostat.ec.europa.eu/tgm/table.do? tab=table&init=1&plugin=1&language=en&pcode=tec00115>.[Accessed, August 5, 2014]. According to the IMF, the Spanish forecast GDP growth rate for 2014 has moved to the positive 1.2 percentagepoints, and 1.6 for 2015. [News published in Spain on July 10, 2014].

16 ~

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final de Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON

companies to (...)” (Fomento de la producción, 2008-2012) of around 200 companies. So, I

supplemented these data with the online Iberian Analysis System Balances database, called SABI.18

This database has restricted access for students, stores financial company information and

business intelligence for 2,000,000 Spanish firms from 1989 to the current date, and all the

necessary data for this study —NACE 2009 primary code, operational revenue, number of

employees, and added value— were available and exportable. The problems encountered were that

the drop-down menu on the main page did not select the years prior to 2002, the reclassification of

the NACE according to the economic sector classification of the journal, and the faster consumption

of available financial credit for exporting data.19 Finally, I got to export top 500 Spanish firms by

operational revenue from 2006 to 2012.

According to Sánchez (1998: 21-22), simultaneity of two different data sources —Fomento

de la producción and SABI— can break the continuity of the serial homogeneity of this study. The

value of time series to establish the trends is know. It may be questionable in its absolute validity as

timely and quantitative information, but it allows to detect trends in the processes, even the values

may be questionable. This is the case in this methodology. However, this study can be considered

that provides information of interest, especially from an evolutionary point of view.

So, I had the data necessary for my study. The problem was the labor cost of this job. The

solution left was to scan the data; to write all data for each year in a spreadsheet —name of the firm,

name of the economic activity classification, nominal monetary operational revenue, quantity of

employment, and nominal monetary added value—; to order firms by economic activities when the

data source was the journal, or to reclassify firms by economic activities when the data source was

SABI; and, to add the totals. Lack of time has restricted sample size of this study of a total of 67,125

available companies to 28,461 firms, 711 per year on average,20 a coverage on average of 42.4

percentage points for the periods 1971-1986 and 1989-2012. Next table shows the annual coverage

of this study:

18: SABI. Sistema de Análisis de Balances Ibéricos. <http://www.bvdinfo.com/en-gb/products/company-information/national/sabi>. [Accessed on June 6, 2014].

19: Ten days' work in different Universities in two months —when financial credit was restored— were required.20: The constraint of around 660's firms used in this study is because it was the equivalent to four hours of my job.

~ 17 ~

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final del Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON

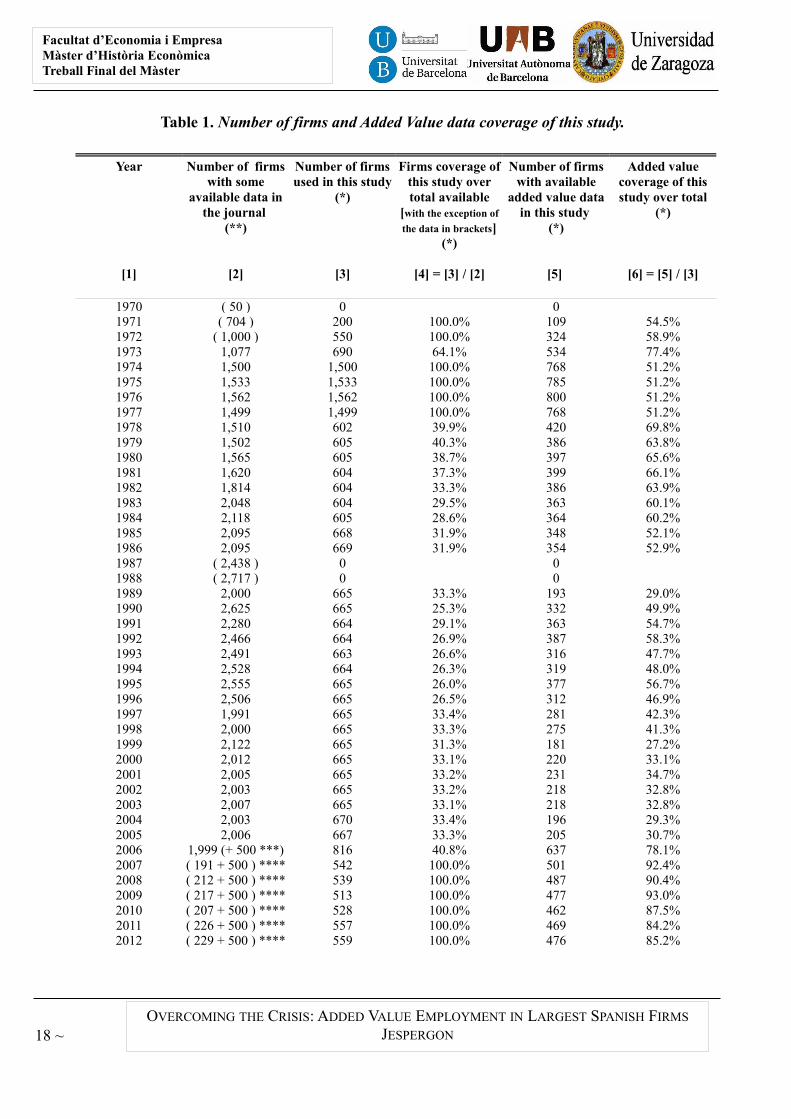

Table 1. Number of firms and Added Value data coverage of this study.

Year

[1]

Number of firmswith some

available data inthe journal

(**)

[2]

Number of firmsused in this study

(*)

[3]

Firms coverage ofthis study overtotal available

[with the exception of

the data in brackets](*)

[4] = [3] / [2]

Number of firmswith available

added value datain this study

(*)

[5]

Added valuecoverage of thisstudy over total

(*)

[6] = [5] / [3]

1970 ( 50 ) 0 01971 ( 704 ) 200 100.0% 109 54.5%1972 ( 1,000 ) 550 100.0% 324 58.9%1973 1,077 690 64.1% 534 77.4%1974 1,500 1,500 100.0% 768 51.2%1975 1,533 1,533 100.0% 785 51.2%1976 1,562 1,562 100.0% 800 51.2%1977 1,499 1,499 100.0% 768 51.2%1978 1,510 602 39.9% 420 69.8%1979 1,502 605 40.3% 386 63.8%1980 1,565 605 38.7% 397 65.6%1981 1,620 604 37.3% 399 66.1%1982 1,814 604 33.3% 386 63.9%1983 2,048 604 29.5% 363 60.1%1984 2,118 605 28.6% 364 60.2%1985 2,095 668 31.9% 348 52.1%1986 2,095 669 31.9% 354 52.9%1987 ( 2,438 ) 0 01988 ( 2,717 ) 0 01989 2,000 665 33.3% 193 29.0%1990 2,625 665 25.3% 332 49.9%1991 2,280 664 29.1% 363 54.7%1992 2,466 664 26.9% 387 58.3%1993 2,491 663 26.6% 316 47.7%1994 2,528 664 26.3% 319 48.0%1995 2,555 665 26.0% 377 56.7%1996 2,506 665 26.5% 312 46.9%1997 1,991 665 33.4% 281 42.3%1998 2,000 665 33.3% 275 41.3%1999 2,122 665 31.3% 181 27.2%2000 2,012 665 33.1% 220 33.1%2001 2,005 665 33.2% 231 34.7%2002 2,003 665 33.2% 218 32.8%2003 2,007 665 33.1% 218 32.8%2004 2,003 670 33.4% 196 29.3%2005 2,006 667 33.3% 205 30.7%2006 1,999 (+ 500 ***) 816 40.8% 637 78.1%2007 ( 191 + 500 ) **** 542 100.0% 501 92.4%2008 ( 212 + 500 ) **** 539 100.0% 487 90.4%2009 ( 217 + 500 ) **** 513 100.0% 477 93.0%2010 ( 207 + 500 ) **** 528 100.0% 462 87.5%2011 ( 226 + 500 ) **** 557 100.0% 469 84.2%2012 ( 229 + 500 ) **** 559 100.0% 476 85.2%

18 ~

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final de Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON

TOTAL 67,125 28,461 42.4% 15,638 54.9%

Source: (*) Own made. Results of the model.(**) Fomento de la producción (1971-2006).

(***) SABI. TOP500 Spanish firms by operational revenue.(****) Fomento de la producción (2008-2012) & SABI. TOP500.

Notes: The years 1970, 1987 and 1988 have not been included in the total because added value data were not available.The total firms included in the years 1971 and 1972 are the number of firms used in this study —200 and 550 instead of704 and 1,000, respectively— because original source did not offer any added value data for the others companies —504 and 450, respectively—, for this reason the study has full coverage in these years. For the years 1974, 1975, 1976and 1977 the data of this study was in correspondence with the aggregate results of the economic activities carried outby the authors of Fomento de la producción. It was a pity this practice did not continue in subsequent years. The data ofthe year 1974 was available in Fomento de la producción (1975). For the period 2006-2012 the simultaneous use of twodatasets —Fomento de la producción and SABI— causes the existence of duplications. The total firms included in theperiod 2007-2012 are the number of firms used in this study, for this reason the study has full coverage in this period.The journal data override SABI data for all replicas. The year 2007 was available in Fomento de la producción (2008).The dossiers “The first Spanish companies to (...)” of the years 2010, 2011 and 2012 (Fomento de la producción, 2010-2012) offer own resources data instead of the added value data of the firms.

The added values are not available for all the firms because, or there are enterprises that do

not provide some of the components for calculating their added value —SABI has not this problem

because it has full added value coverage—, or there are companies that belong a business group and

the added value is registered in the main firm —the Fomento de la producción dataset showed

results in the form of consolidated accounts—, or firms do not want to show negative added value

in their annual income statement —this is the case of the Fomento de la producción dataset but not

of the SABI dataset—, or there are subsidiary foreign firms deriving added value to their

headquarters. In previously table you can observe that on average the added value coverage of this

study is 54.9 percentage points over total. Obviously, complete coverage exchanges the results of

this study, and it requires that absolute results should be interpreted with caution. However, this

study may be useful to establish trends from the point of view of the evolutionary dynamic of the

economic activities of the largest non-financial Spanish firms. Following, relative added value and

employment calculations are necessary for modelling this study.

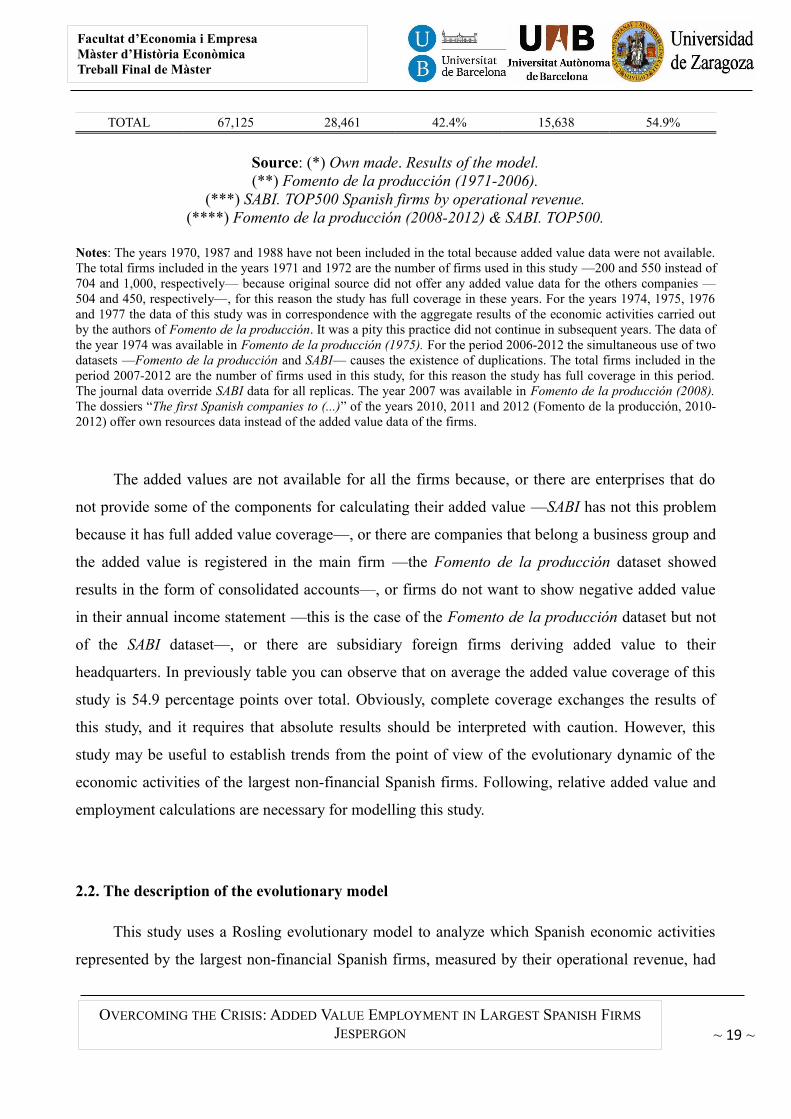

2.2. The description of the evolutionary model

This study uses a Rosling evolutionary model to analyze which Spanish economic activities

represented by the largest non-financial Spanish firms, measured by their operational revenue, had

~ 19 ~

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final del Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON

higher added value and bigger employment from 1971 to 2012. The evolutionary model is an

annual 2D-plotted dispersion diagram. The dispersion diagram correlates two variables:

employment and added value. Employment is represented in the horizontal axis and added value in

the vertical axis. Both axis are segmented into two divisions. The first division includes the range

values from 0 to 0.5 and the second one from 0.5 to 1. So, this model presents four quadrants. The

bottom left quadrant indicates low added value and low employment economic activities, the

bottom right one low added value and high employment, the top left one high added value and low

employment, and the top right one high added value and high employment.

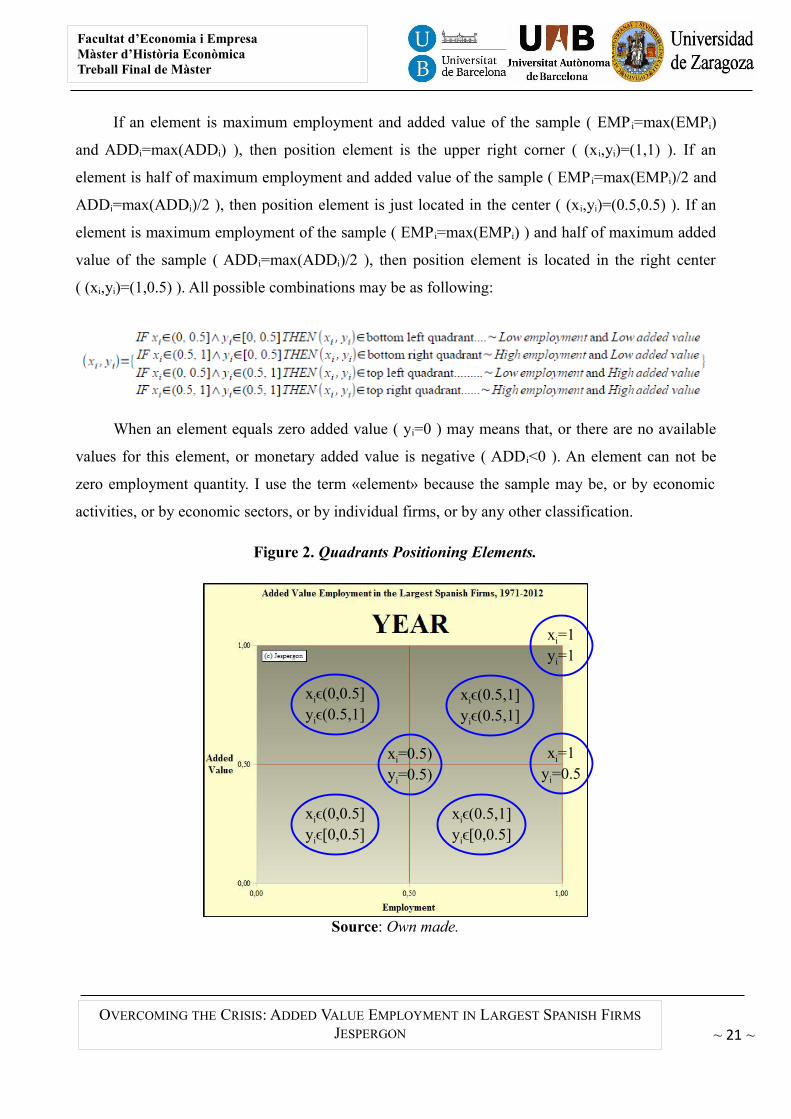

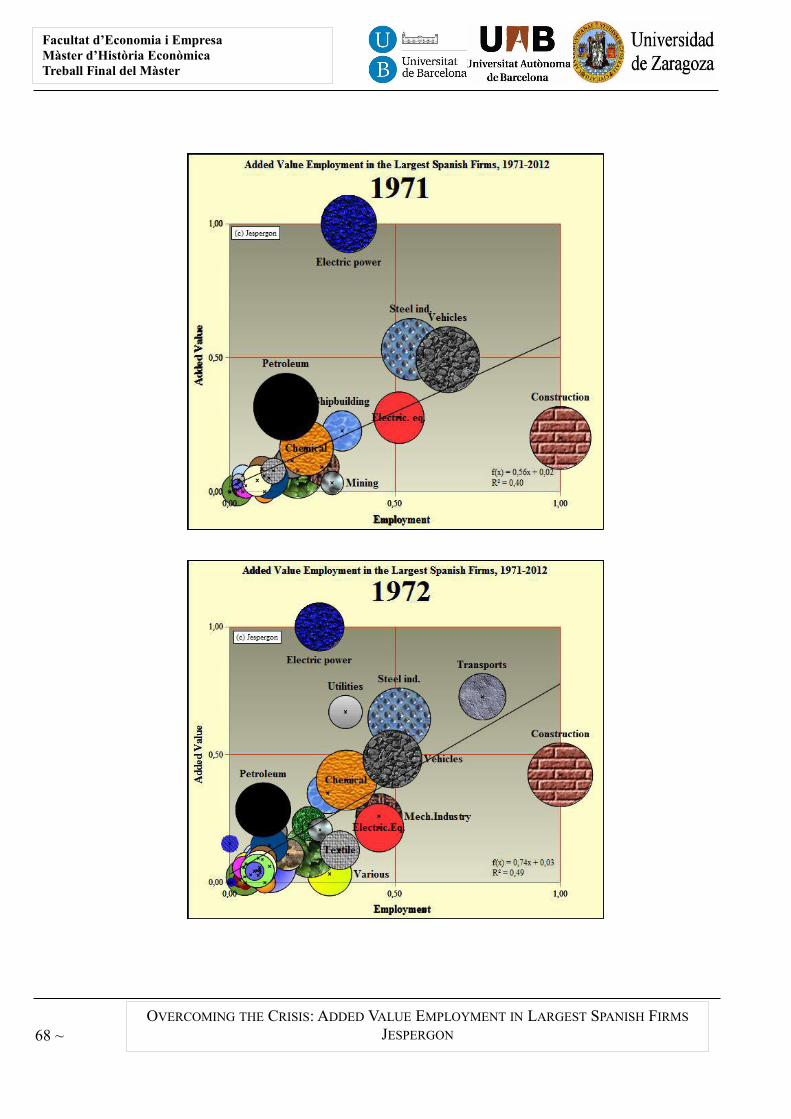

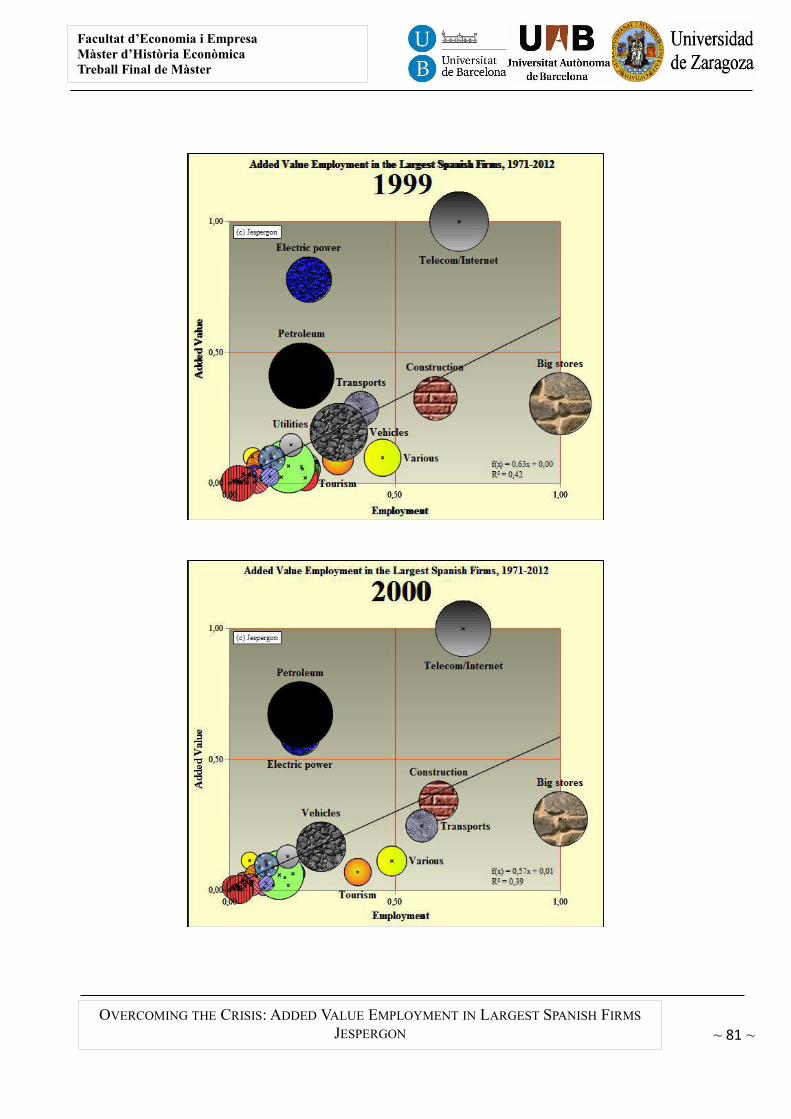

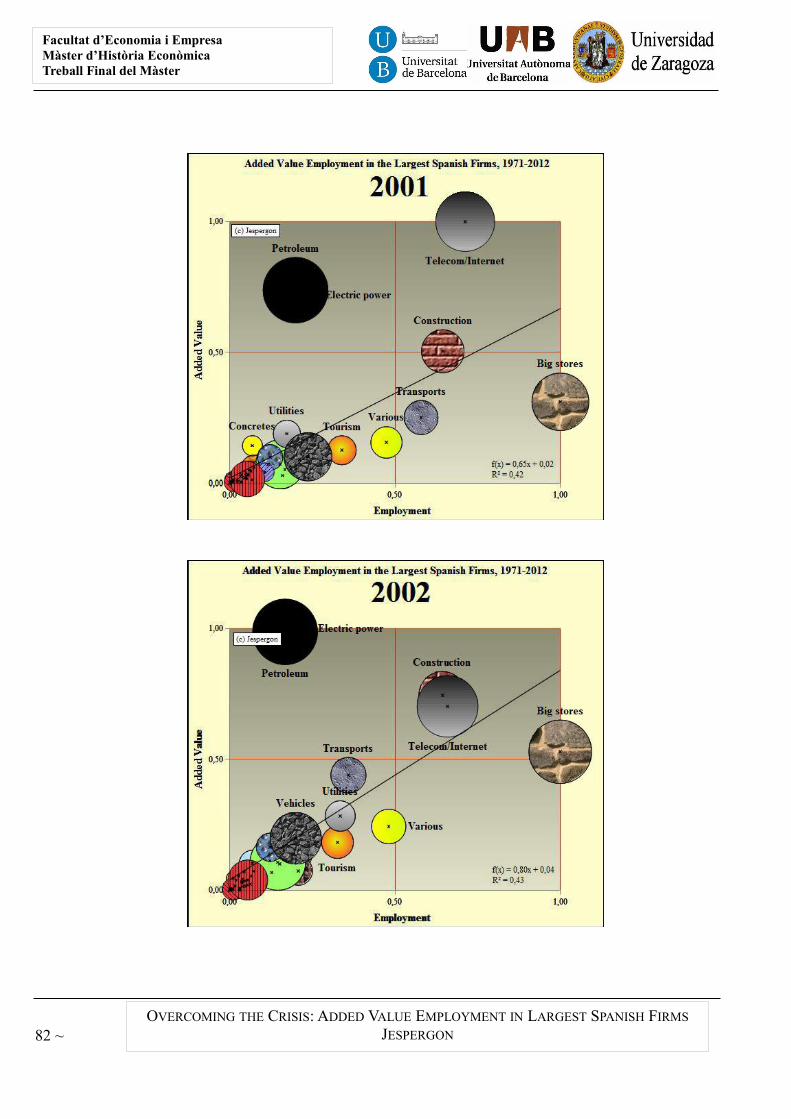

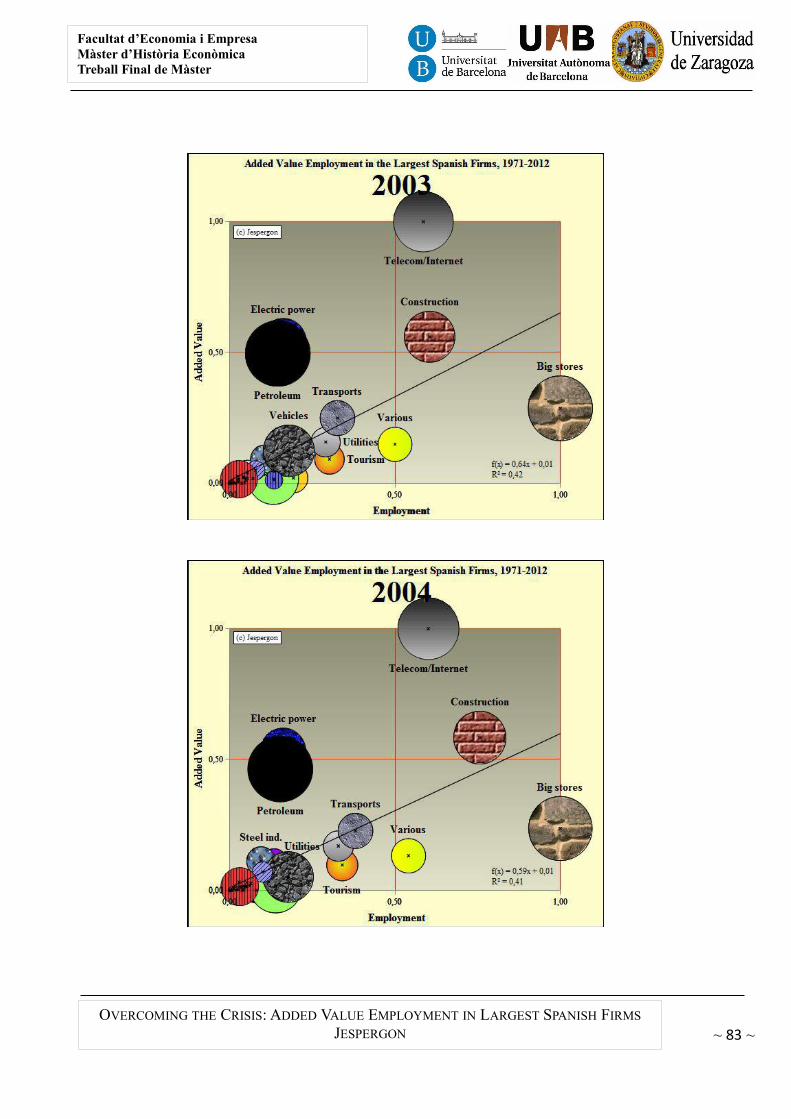

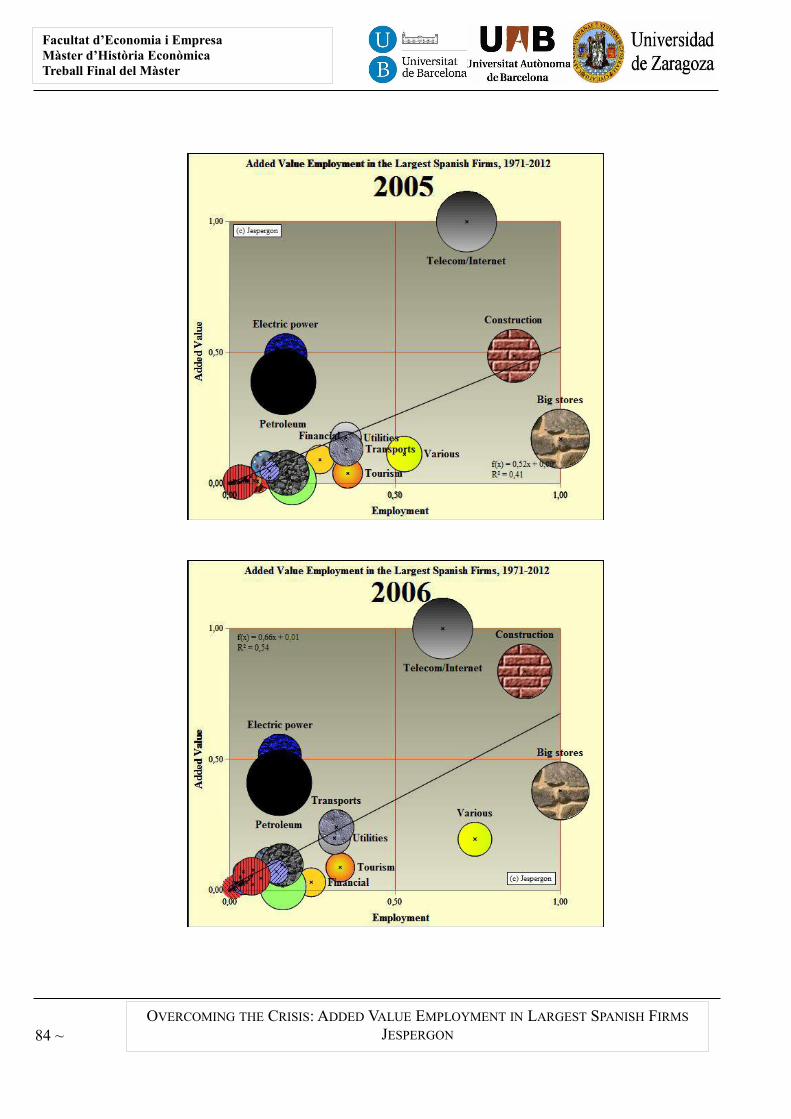

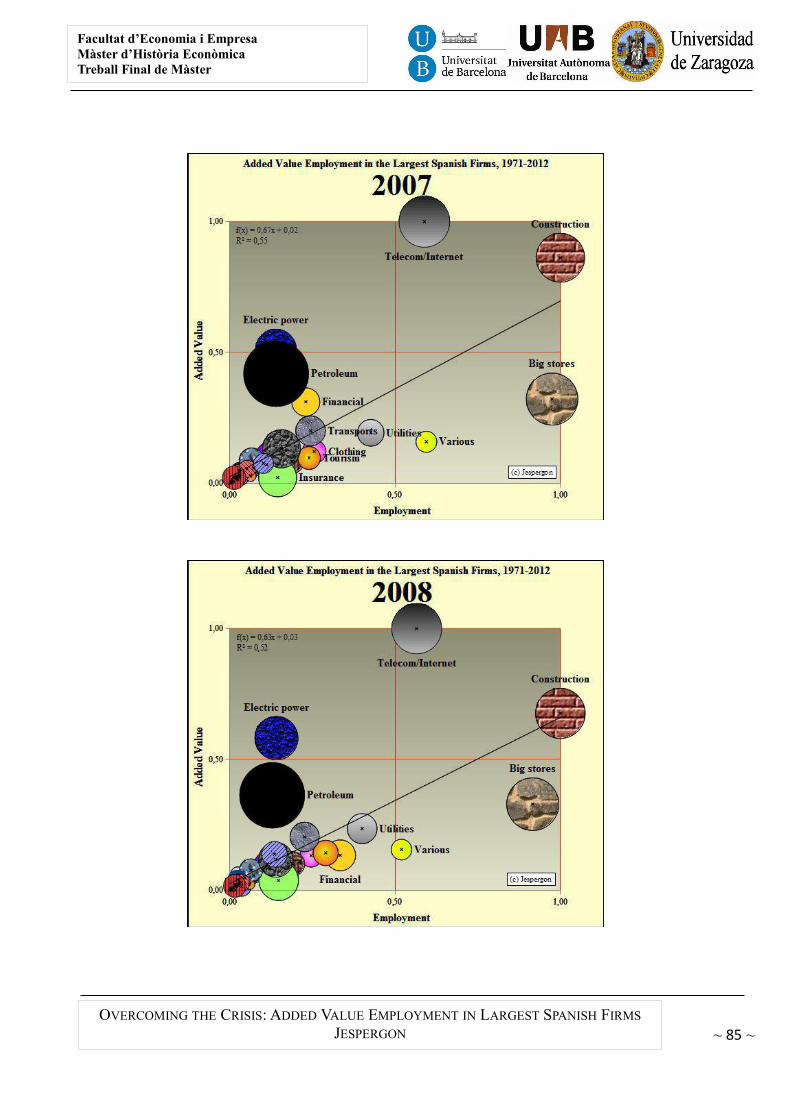

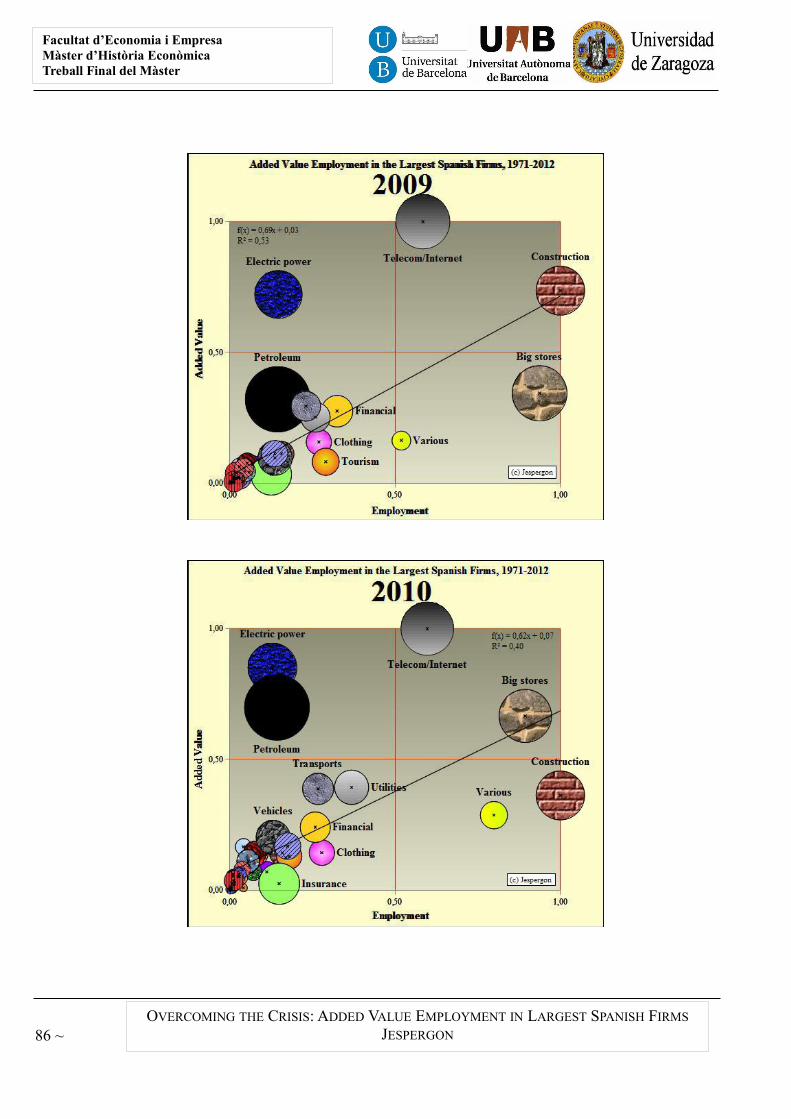

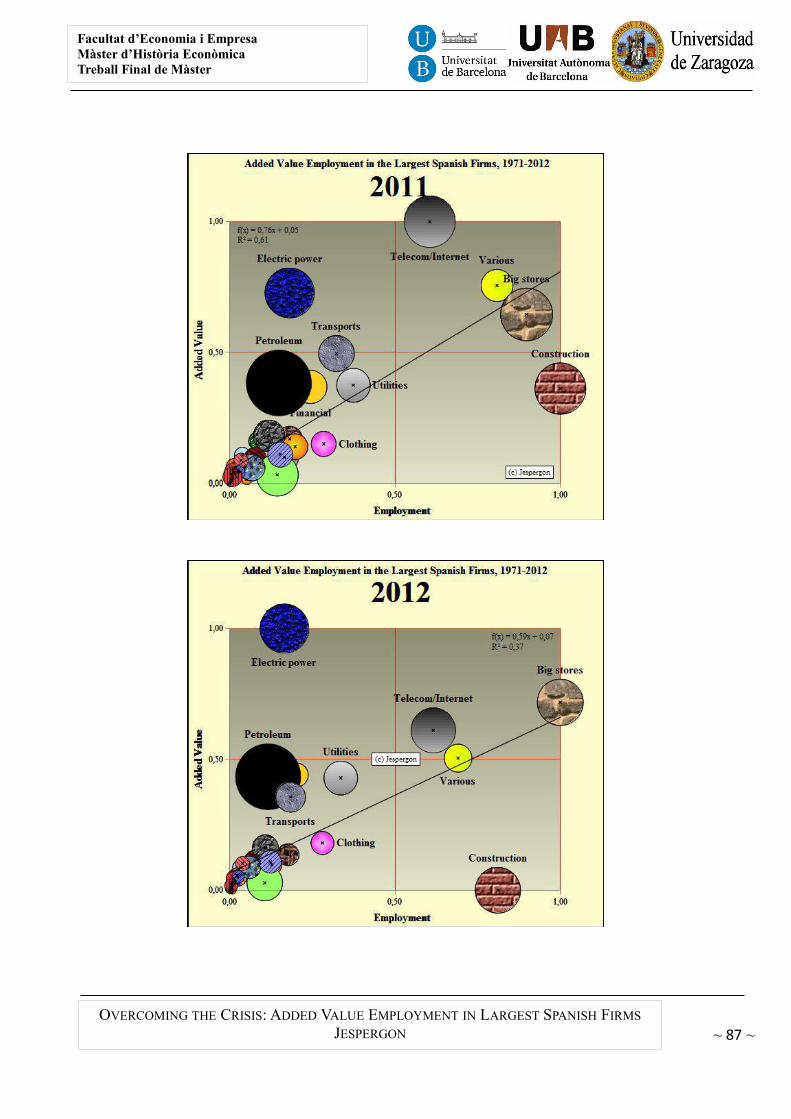

Figure 1. Quadrants Structure Modeling.

Source: Own made.

How to calculate which quadrant belongs to an «element»? Given quantity of employment of

an element in a year (EMPi), measured by number of people employed, and tangible added value of

the same element and year (ADDi), measured by real monetary values, of a sample of n elements;

then position of an element (xi,yi) in this 2D-plotted model is calculated as follows:

20 ~

High added valueLow employment

High added valueHigh employment

Low added valueLow employment

Low added valueHigh employment

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final de Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON

If an element is maximum employment and added value of the sample ( EMP i=max(EMPi)

and ADDi=max(ADDi) ), then position element is the upper right corner ( (xi,yi)=(1,1) ). If an

element is half of maximum employment and added value of the sample ( EMP i=max(EMPi)/2 and

ADDi=max(ADDi)/2 ), then position element is just located in the center ( (xi,yi)=(0.5,0.5) ). If an

element is maximum employment of the sample ( EMP i=max(EMPi) ) and half of maximum added

value of the sample ( ADDi=max(ADDi)/2 ), then position element is located in the right center

( (xi,yi)=(1,0.5) ). All possible combinations may be as following:

When an element equals zero added value ( yi=0 ) may means that, or there are no available

values for this element, or monetary added value is negative ( ADDi<0 ). An element can not be

zero employment quantity. I use the term «element» because the sample may be, or by economic

activities, or by economic sectors, or by individual firms, or by any other classification.

Figure 2. Quadrants Positioning Elements.

Source: Own made.

~ 21 ~

xi=1yi=1

xi=0.5)yi=0.5)

xiϵ(0,0.5]yiϵ[0,0.5]

xiϵ(0,0.5]yiϵ(0.5,1]

xiϵ(0.5,1]yiϵ(0.5,1]

xiϵ(0.5,1]yiϵ[0,0.5]

xi=1yi=0.5

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final del Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON

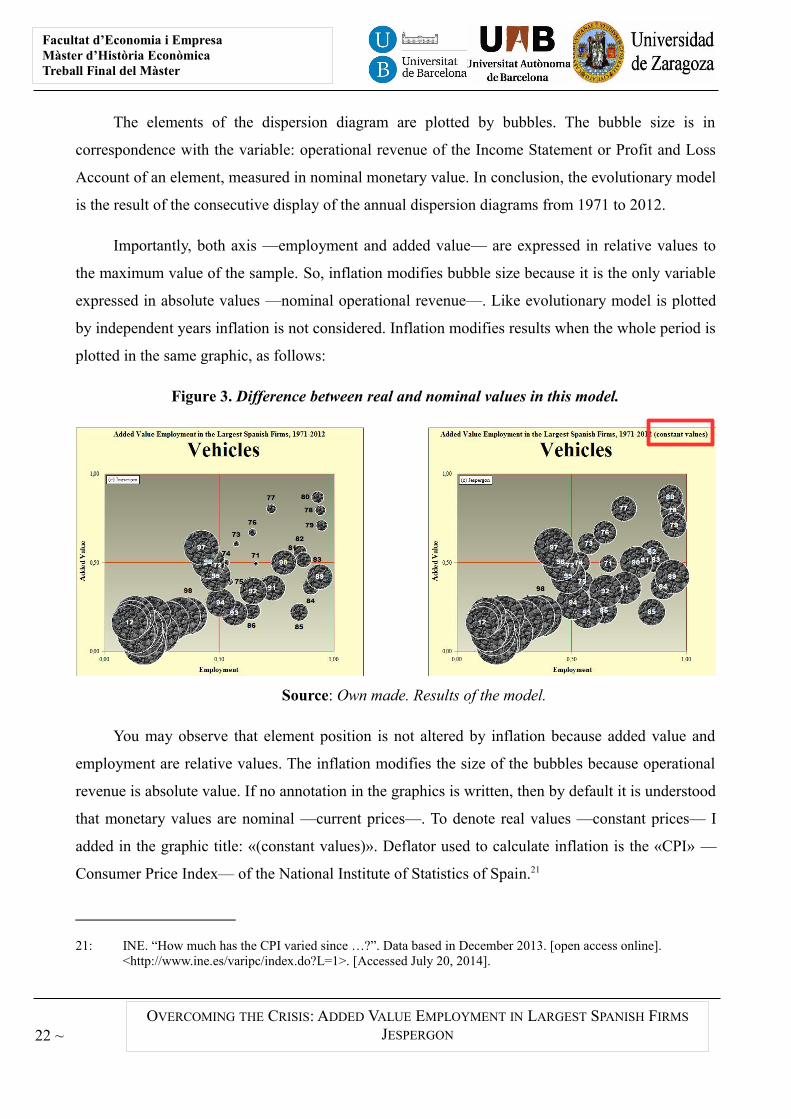

The elements of the dispersion diagram are plotted by bubbles. The bubble size is in

correspondence with the variable: operational revenue of the Income Statement or Profit and Loss

Account of an element, measured in nominal monetary value. In conclusion, the evolutionary model

is the result of the consecutive display of the annual dispersion diagrams from 1971 to 2012.

Importantly, both axis —employment and added value— are expressed in relative values to

the maximum value of the sample. So, inflation modifies bubble size because it is the only variable

expressed in absolute values —nominal operational revenue—. Like evolutionary model is plotted

by independent years inflation is not considered. Inflation modifies results when the whole period is

plotted in the same graphic, as follows:

Figure 3. Difference between real and nominal values in this model.

Source: Own made. Results of the model.

You may observe that element position is not altered by inflation because added value and

employment are relative values. The inflation modifies the size of the bubbles because operational

revenue is absolute value. If no annotation in the graphics is written, then by default it is understood

that monetary values are nominal —current prices—. To denote real values —constant prices— I

added in the graphic title: «(constant values)». Deflator used to calculate inflation is the «CPI» —

Consumer Price Index— of the National Institute of Statistics of Spain.21

21: INE. “How much has the CPI varied since …?”. Data based in December 2013. [open access online]. <http://www.ine.es/varipc/index.do?L=1>. [Accessed July 20, 2014].

22 ~

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final de Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON

2.3. Discussion

I have found eight points that they may be in discussion in this study.

a) According to Jorgenson, Ho & Stiroh,22 modeling of production processes must be respected

as much as possible the reality. Added value concept is an artificial construct considering only

primary inputs and, therefore, does not correspond to the output produced by a particular

industry. So, gross output is the correct way to reproduce the reality, and the added value so

does not.

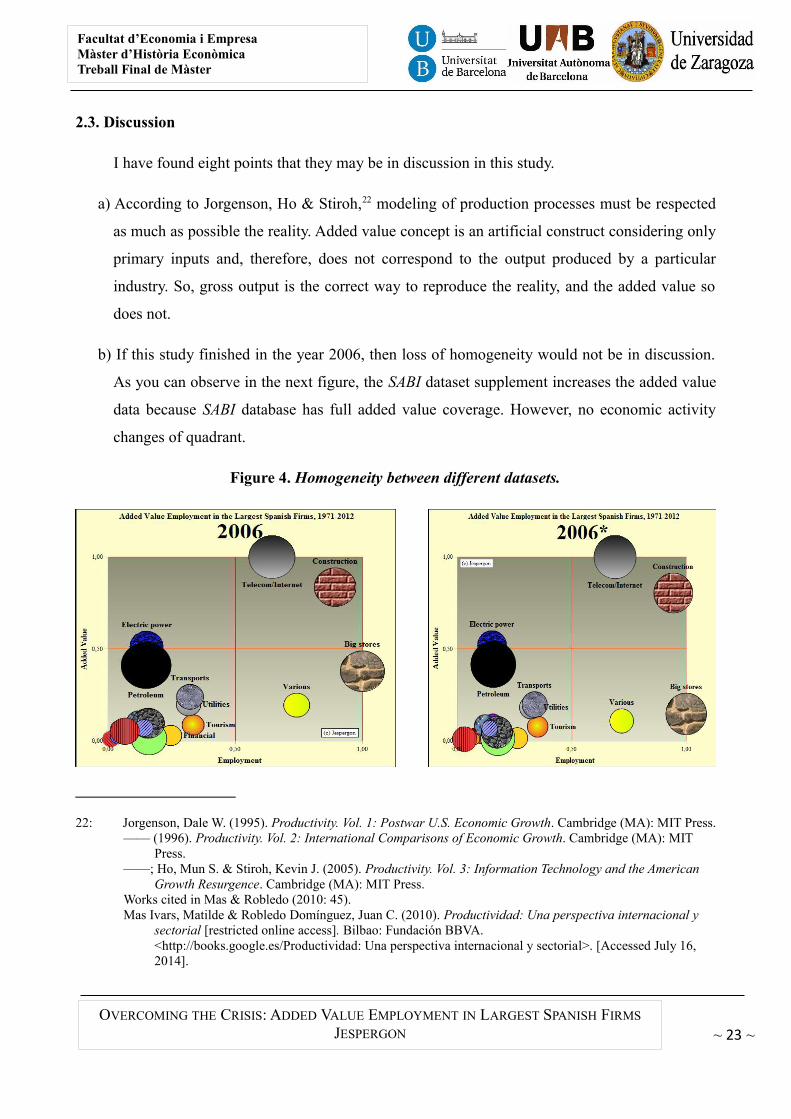

b) If this study finished in the year 2006, then loss of homogeneity would not be in discussion.

As you can observe in the next figure, the SABI dataset supplement increases the added value

data because SABI database has full added value coverage. However, no economic activity

changes of quadrant.

Figure 4. Homogeneity between different datasets.

22: Jorgenson, Dale W. (1995). Productivity. Vol. 1: Postwar U.S. Economic Growth. Cambridge (MA): MIT Press.—— (1996). Productivity. Vol. 2: International Comparisons of Economic Growth. Cambridge (MA): MIT

Press.——; Ho, Mun S. & Stiroh, Kevin J. (2005). Productivity. Vol. 3: Information Technology and the American

Growth Resurgence. Cambridge (MA): MIT Press.Works cited in Mas & Robledo (2010: 45).Mas Ivars, Matilde & Robledo Domínguez, Juan C. (2010). Productividad: Una perspectiva internacional y

sectorial [restricted online access]. Bilbao: Fundación BBVA.<http://books.google.es/Productividad: Una perspectiva internacional y sectorial>. [Accessed July 16, 2014].

~ 23 ~

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final del Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON

Source: Own made. Results of the model.

The left graphic —2006— shows the results of the top 816 firms by operational revenue of

the mix between Fomento de la producción (2006) and SABI dataset, and 78.1 percentage

points of added value data coverage. The right one —2006*— is the same but without the

supplement of SABI dataset, ergo a sample size of 675 firms with added value data coverage

of 35.3 percentage points. Especially «big stores» is the recipient of SABI supplement as it

increases its value added.

However, in order to maintain a major homogeneity in this study, I did not want to prolong

the time period until 2013, despite the availability of SABI dataset for this year, because I did

not have any available data of the journal Fomento de la producción.

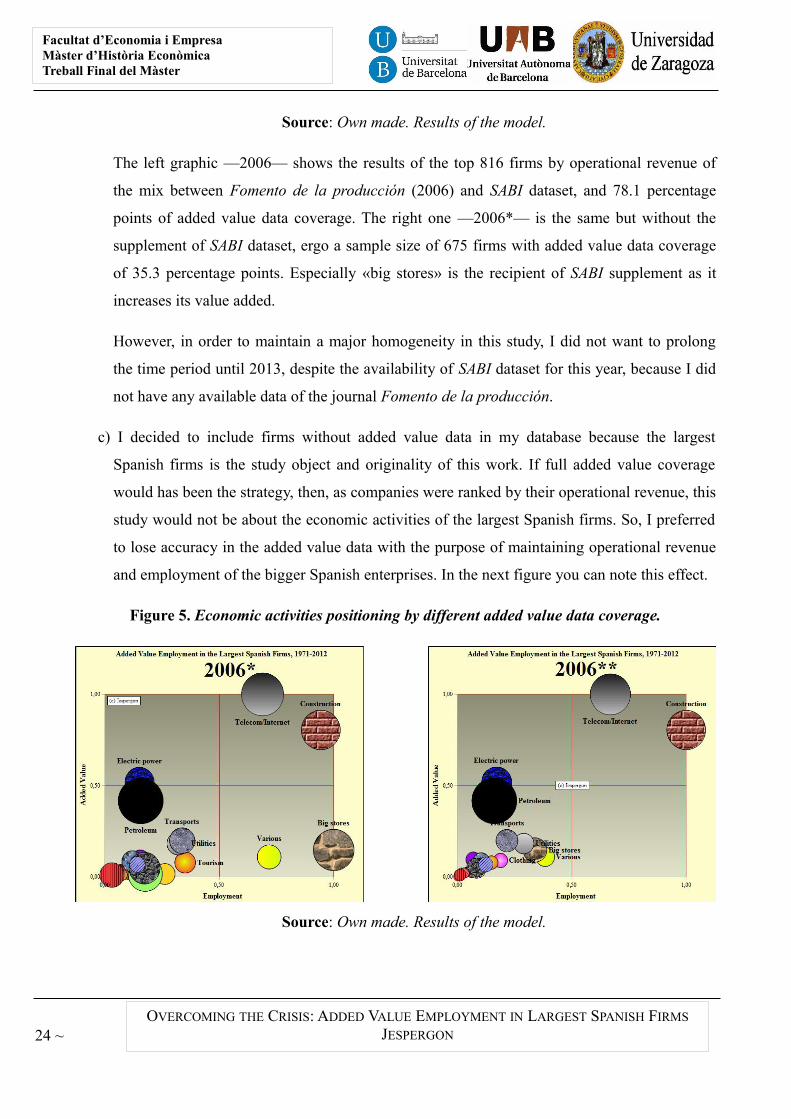

c) I decided to include firms without added value data in my database because the largest

Spanish firms is the study object and originality of this work. If full added value coverage

would has been the strategy, then, as companies were ranked by their operational revenue, this

study would not be about the economic activities of the largest Spanish firms. So, I preferred

to lose accuracy in the added value data with the purpose of maintaining operational revenue

and employment of the bigger Spanish enterprises. In the next figure you can note this effect.

Figure 5. Economic activities positioning by different added value data coverage.

Source: Own made. Results of the model.

24 ~

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final de Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON

The left graphic —2006*— shows the results of the top 675 firms by operational revenue of

Fomento de la producción (2006) without the supplement of SABI dataset. The right one —

2006**— is the same but with the firms without available added value data removed, ergo a

sample size of 238 firms with full data coverage. Differences are plausible. While

«telecom/Internet», «construction/real-estate», and «electric power» economic activities

maintain their same position in the quadrants; «big stores» and «various» economic activities

have changed of quadrant —from bottom right to bottom left—.

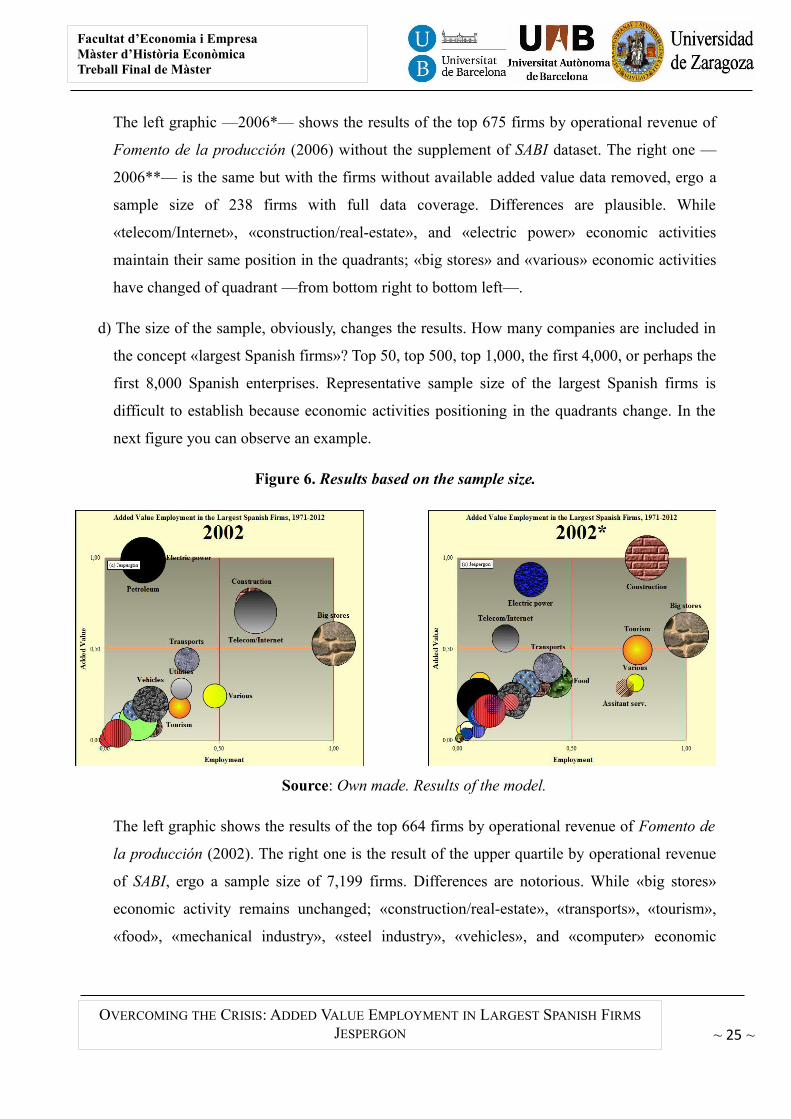

d) The size of the sample, obviously, changes the results. How many companies are included in

the concept «largest Spanish firms»? Top 50, top 500, top 1,000, the first 4,000, or perhaps the

first 8,000 Spanish enterprises. Representative sample size of the largest Spanish firms is

difficult to establish because economic activities positioning in the quadrants change. In the

next figure you can observe an example.

Figure 6. Results based on the sample size.

Source: Own made. Results of the model.

The left graphic shows the results of the top 664 firms by operational revenue of Fomento de

la producción (2002). The right one is the result of the upper quartile by operational revenue

of SABI, ergo a sample size of 7,199 firms. Differences are notorious. While «big stores»

economic activity remains unchanged; «construction/real-estate», «transports», «tourism»,

«food», «mechanical industry», «steel industry», «vehicles», and «computer» economic

~ 25 ~

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final del Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON

activities increase in both employment and added value; «electric power» increases in

employment and decreases in added value; and, «telecom/Internet» and «petroleum» decrease

in both employment and added value.

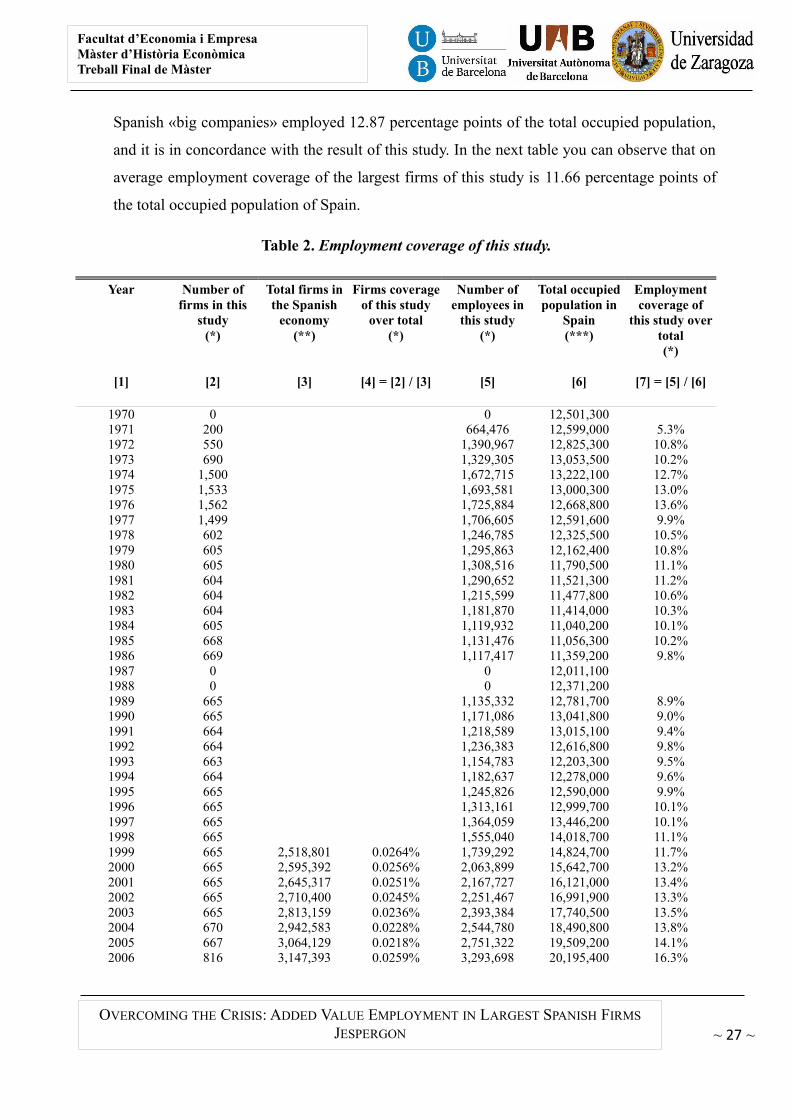

e) Are largest Spanish firms of this study representative of the employment structure in Spain?

For answering this question is necessary to realize a little exercise.

According to the data of the Central Business Register of the National Institute of Statistics of

Spain,23 during the period 1999-2009, on average registered companies may be distributed in

four stretch. Spanish companies without employees were a 52.35 percentage points of the

registered companies in Spain during this period, firms between 1 and 49 employees were a

46.78 percentage points of the total, between 50 and 499 employees were a 0.82 percentage

points, and more of 500 employees were 0.05 percentage points.

According to the data of the Labor Force Survey of the National Institute of Statistics of

Spain,24 during the period 2008-2013, on average occupied population may be distributed in

three stretch. Self-employed were 17.15 percentage points of the occupied population in Spain

during this period, public employees were 16.93 percentage points, and private employees

were 65.91 percentage points.

For the common years —2008 and 2009— I proxy total private employees of the Labor Force

Survey between absolute number of firms with employees of the Central Business Register

assuming a uniform distribution and a constant number of employees for each stretch.

The average distribution of the private employees over total occupied population —65.91%—

between the three registered stretch of companies with employees in Spain in the years 2008

and 2009 were: 36.84 percentage points of the private employees work in a company between

1 and 49 employees, 17.08 percentage points in a firm between 50 and 499 employees, and

12.87 percentage points more of 500 employees.

23: INE. Directorio Central de Empresas (DIRCE). Firms without employees included. <http://www.ine.es/jaxi/menu.do?type=pcaxis&path=%2Ft37%2Fp201&file=inebase&L=1>. [Accessed July 23, 2014].

24: INE. Encuesta de Población Activa (EPA). Data for the fourth quarter of each year. <http://www.ine.es/en/inebaseDYN/epa30308/epa_inicio_en.htm>. [Accessed July 23, 2014].

26 ~

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final de Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON

Spanish «big companies» employed 12.87 percentage points of the total occupied population,

and it is in concordance with the result of this study. In the next table you can observe that on

average employment coverage of the largest firms of this study is 11.66 percentage points of

the total occupied population of Spain.

Table 2. Employment coverage of this study.

Year

[1]

Number offirms in this

study(*)

[2]

Total firms inthe Spanish

economy(**)

[3]

Firms coverageof this study

over total(*)

[4] = [2] / [3]

Number ofemployees in

this study(*)

[5]

Total occupiedpopulation in

Spain(***)

[6]

Employmentcoverage of

this study overtotal(*)

[7] = [5] / [6]

1970 0 0 12,501,3001971 200 664,476 12,599,000 5.3%1972 550 1,390,967 12,825,300 10.8%1973 690 1,329,305 13,053,500 10.2%1974 1,500 1,672,715 13,222,100 12.7%1975 1,533 1,693,581 13,000,300 13.0%1976 1,562 1,725,884 12,668,800 13.6%1977 1,499 1,706,605 12,591,600 9.9%1978 602 1,246,785 12,325,500 10.5%1979 605 1,295,863 12,162,400 10.8%1980 605 1,308,516 11,790,500 11.1%1981 604 1,290,652 11,521,300 11.2%1982 604 1,215,599 11,477,800 10.6%1983 604 1,181,870 11,414,000 10.3%1984 605 1,119,932 11,040,200 10.1%1985 668 1,131,476 11,056,300 10.2%1986 669 1,117,417 11,359,200 9.8%1987 0 0 12,011,1001988 0 0 12,371,2001989 665 1,135,332 12,781,700 8.9%1990 665 1,171,086 13,041,800 9.0%1991 664 1,218,589 13,015,100 9.4%1992 664 1,236,383 12,616,800 9.8%1993 663 1,154,783 12,203,300 9.5%1994 664 1,182,637 12,278,000 9.6%1995 665 1,245,826 12,590,000 9.9%1996 665 1,313,161 12,999,700 10.1%1997 665 1,364,059 13,446,200 10.1%1998 665 1,555,040 14,018,700 11.1%1999 665 2,518,801 0.0264% 1,739,292 14,824,700 11.7%2000 665 2,595,392 0.0256% 2,063,899 15,642,700 13.2%2001 665 2,645,317 0.0251% 2,167,727 16,121,000 13.4%2002 665 2,710,400 0.0245% 2,251,467 16,991,900 13.3%2003 665 2,813,159 0.0236% 2,393,384 17,740,500 13.5%2004 670 2,942,583 0.0228% 2,544,780 18,490,800 13.8%2005 667 3,064,129 0.0218% 2,751,322 19,509,200 14.1%2006 816 3,147,393 0.0259% 3,293,698 20,195,400 16.3%

~ 27 ~

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final del Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON

2007 542 3,336,657 0.0162% 2,934,400 20,717,900 14.2%2008 539 3,422,239 0.0157% 3,108,558 20,055,300 15.5%2009 513 3,355,830 0.0153% 2,843,782 18,890,400 15.1%2010 528 3,143,732 18,674,900 16.8%2011 557 3,367,719 18,153,000 18.6%2012 559 3,219,946 17,339,400 18.6%

TOTAL 28,461 71,492,245 613,329,800 11.66%

Source: (*) Own made. Results of the model.(**) Central Business Register of the National Institute of Statistics of Spain.(***) Nicolau (2005: table 2.29 in pages 150-151) for the period 1970-2001,

and Labor Force Survey of the National Institute of Statistics of Spain for the period 2002-2012.

f) CPI deflator is not the most appropriate indicator to measure the inflation effects in an

economy, the best one is the GDP deflator. The GDP deflator is a measure of the level of

prices of all new, domestically produced, final goods and services in an economy, while CPI

deflator only includes a representative basket of goods and services consumed by households.

However, for greater accuracy, deflator of each economic activity should be used since, for

example, the energy price index is not the same as the food price index because deflator is

used in this study for measuring the price effect in an economic activity during the whole

period.

g) The NACE 2009 primary code conversion of the SABI dataset —four digits— to the Fomento

de la producción economic activities may be in discussion. There are no automatic conversion

because a NACE may belong to different economic activities of Fomento de la producción.

So, a manual conversion would had been necessary.

h) The classification of the economic activities made by the authors of Fomento de la

producción may be in discussion. Obviously, any other economic activities classification

change the results. Firm economic activity classification was not fixed, and it might evolve

during the period 1971-2012. As next table shows, initially, there were twenty seven

economic activities in the year 1971: oils, various —tobacco and oil distribution25—,26 food,

beverages, rubber/tires, concrete, construction/real-estate, shipbuilding, mechanical industry,

25: The private leasing companies of national oil monopoly were classified by the authors of Fomento de la producción in «various» economic activity till the year 1981 when it changed to «refining petroleum» economic activity. 26: Later, «various» economic activity may include firms of games of chance, jewelry, soccer teams. security, or cleaning.

28 ~

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final de Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON

electronic, electric power, pharma industries, electrical equipment, construction material, non-

metallic metallurgical, mining, paper, leather, plastics, milk products, chemical, refining

petroleum,27 utilities, steel industry, textile, vehicles, and glass.

In the year 1972 ten new economic activities were incorporated: commercial, wearing

apparel, publishers,28 big stores, tourism/hospitality, wood and furniture,29 insurance,

transports, holding,30 and advertising agencies.31

In the year 1982 five new economic activities appeared: commercial pharma, appliances,

computer, engineering, and perfumes/detergents; and one more the next year: commercial

vehicles.

The year 1999 authors of Fomento de la producción unified «electric power», «petroleum»,

and some firms of the «utilities» economic activities in the «energy» economic activity. I did

not follow this change because I wished to follow separately the path of this economic

activities. This year appeared a new economic activity: «telecommunications». It was the

aggregation of some firms of «utilities» and «electronic» economic activities. I followed it but

with changes. I aggregated only two electronic firms to «telecom» economic activity, the rest

of electronic firms did not be aggregated and remained in their economic activity.

Telecommunications firms removed from «utilities» economic activity caused that «utilities»

lost its previous role, for this reason I have jointly represented both economic activities in the

results.

27: The «refining petroleum» economic activity was renamed to «petroleum» in the year 1983.

28: The «publishers» economic activity was renamed to «publishing and arts graphics» in the year 1973, and «mass media» in the year 1999.

29: The «wood and furniture» economic activity was renamed to «wood and cork» in the year 1999.30: The «holding» economic activity appeared only two consecutive years in the journal Fomento de la

producción. The first year —1972— this economic activity included the National Institute of Industry —INI—, a Spanish state-owned financing and industrial holding company. However, it did not include the broad range of public national enterprises. The second year —1973— «holding» economic activity included the INI, Rumasa and Ensidesa.

31: The «advertising agencies» economic activity appeared in the year 1972, and it did not come back to appear tillthe year 1982.

~ 29 ~

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final del Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON

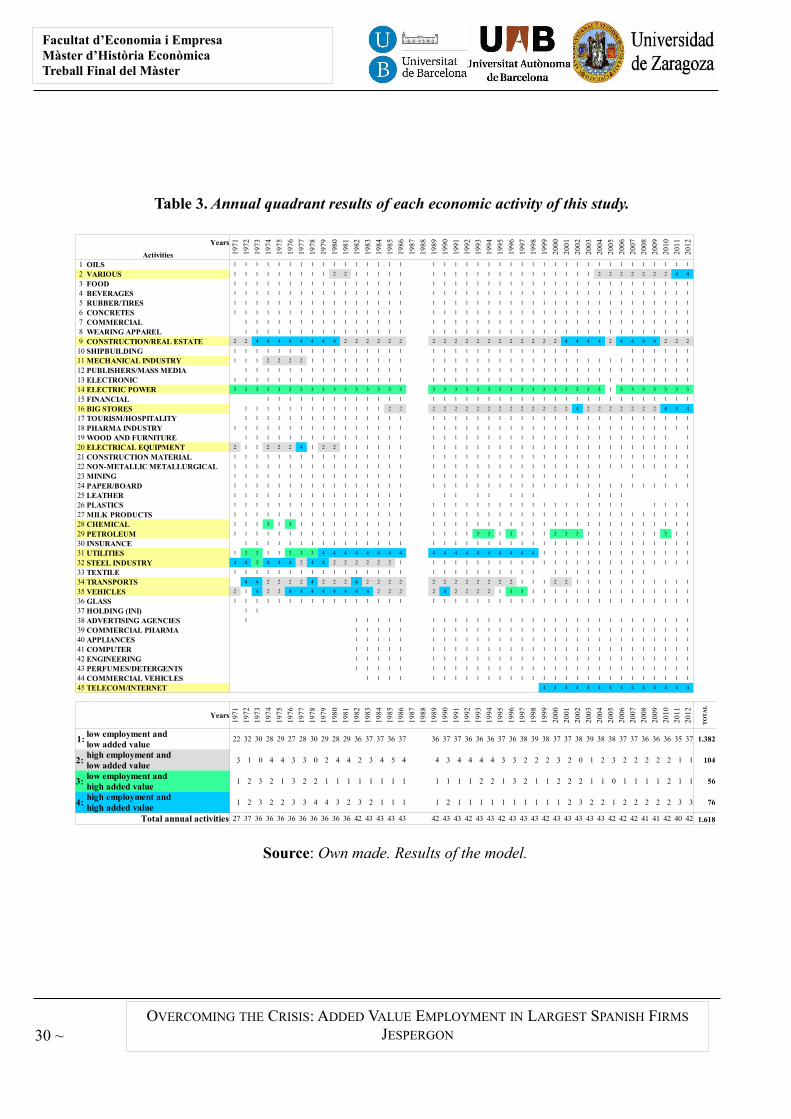

Table 3. Annual quadrant results of each economic activity of this study.

Source: Own made. Results of the model.

30 ~

Years19

71

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Activities1 OILS 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

2 VARIOUS 1 1 1 1 1 1 1 1 1 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 4 4

3 FOOD 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

4 BEVERAGES 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

5 RUBBER/TIRES 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

6 CONCRETES 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

7 COMMERCIAL 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

8 WEARING APPAREL 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

9 CONSTRUCTION/REAL ESTATE 2 2 4 4 4 4 4 4 4 4 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 4 4 4 4 2 4 4 4 4 2 2 2

10 SHIPBUILDING 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

11 MECHANICAL INDUSTRY 1 1 1 2 2 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

12 PUBLISHERS/MASS MEDIA 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

13 ELECTRONIC 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

14 ELECTRIC POWER 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 1 3 3 3 3 3 3 3

15 FINANCIAL 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

16 BIG STORES 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 4 2 2 2 2 2 2 2 4 4 4

17 TOURISM/HOSPITALITY 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

18 PHARMA INDUSTRY 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

19 WOOD AND FURNITURE 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

20 ELECTRICAL EQUIPMENT 2 1 1 2 2 2 4 1 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

21 CONSTRUCTION MATERIAL 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

22 NON-METALLIC METALLURGICAL 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

23 MINING 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

24 PAPER/BOARD 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

25 LEATHER 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

26 PLASTICS 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

27 MILK PRODUCTS 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

28 CHEMICAL 1 1 1 3 1 3 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

29 PETROLEUM 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 3 3 1 3 1 1 1 3 3 3 1 1 1 1 1 1 1 3 1 1

30 INSURANCE 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

31 UTILITIES 1 3 3 1 1 3 3 3 4 4 4 4 4 4 4 4 4 4 4 4 4 4 4 4 4 4 1 1 1 1 1 1 1 1 1 1 1 1 1 1

32 STEEL INDUSTRY 4 4 3 4 4 4 2 4 4 2 2 2 2 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

33 TEXTILE 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

34 TRANSPORTS 4 4 2 2 2 2 4 2 2 2 4 2 2 2 2 2 2 2 2 2 2 2 2 1 1 1 2 2 1 1 1 1 1 1 1 1 1 1 1

35 VEHICLES 2 1 4 2 2 4 4 4 4 4 4 4 4 2 2 2 2 4 2 2 2 2 1 3 3 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

36 GLASS 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

37 HOLDING (INI) 1 1

38 ADVERTISING AGENCIES 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

39 COMMERCIAL PHARMA 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

40 APPLIANCES 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

41 COMPUTER 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

42 ENGINEERING 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

43 PERFUMES/DETERGENTS 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

44 COMMERCIAL VEHICLES 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

45 TELECOM/INTERNET 4 4 4 4 4 4 4 4 4 4 4 4 4 4

Years

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

TO

TA

L

1: 22 32 30 28 29 27 28 30 29 28 29 36 37 37 36 37 36 37 37 36 36 36 37 36 38 39 38 37 37 38 39 38 38 37 37 36 36 36 35 37 1.382

2: 3 1 0 4 4 3 3 0 2 4 4 2 3 4 5 4 4 3 4 4 4 4 3 3 2 2 2 3 2 0 1 2 3 2 2 2 2 2 1 1 104

3: 1 2 3 2 1 3 2 2 1 1 1 1 1 1 1 1 1 1 1 1 2 2 1 3 2 1 1 2 2 2 1 1 0 1 1 1 1 2 1 1 56

4: 1 2 3 2 2 3 3 4 4 3 2 3 2 1 1 1 1 2 1 1 1 1 1 1 1 1 1 1 2 3 2 2 1 2 2 2 2 2 3 3 76

Total annual activities 27 37 36 36 36 36 36 36 36 36 36 42 43 43 43 43 42 43 43 42 43 43 42 43 43 43 42 43 43 43 43 43 42 42 42 41 41 42 40 42 1.618

low employment and low added valuehigh employment and low added valuelow employment and high added valuehigh employment and high added value

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final de Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON

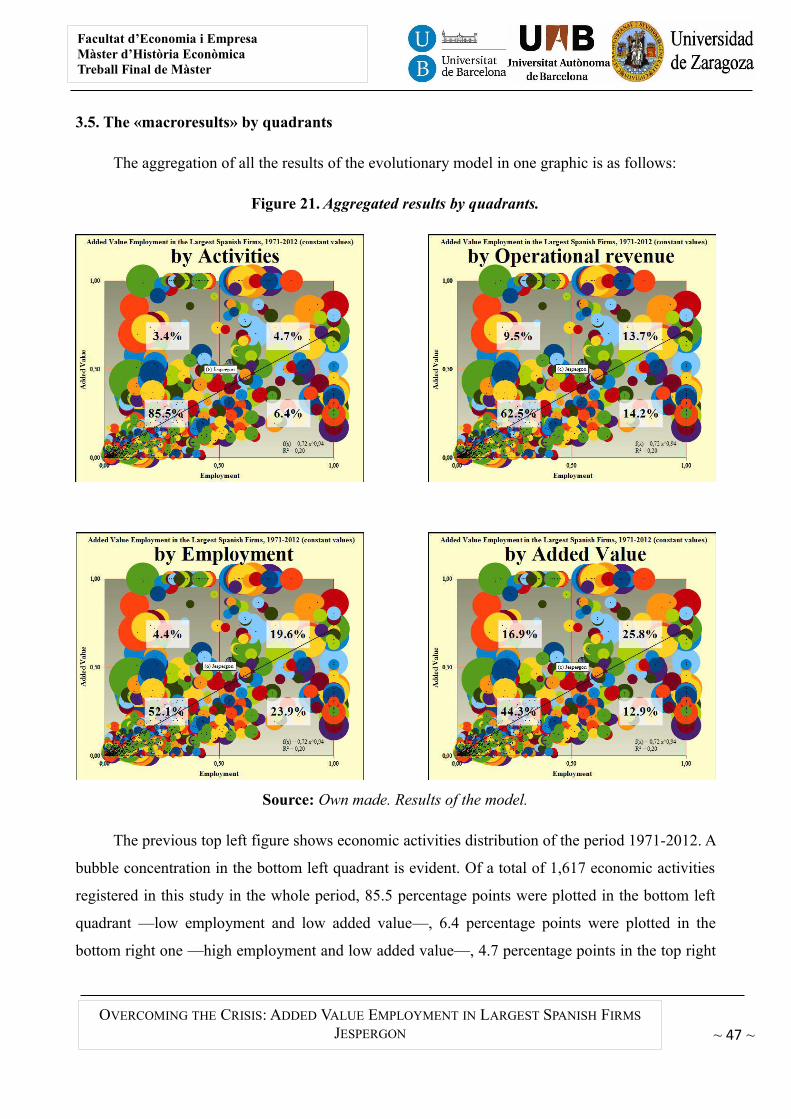

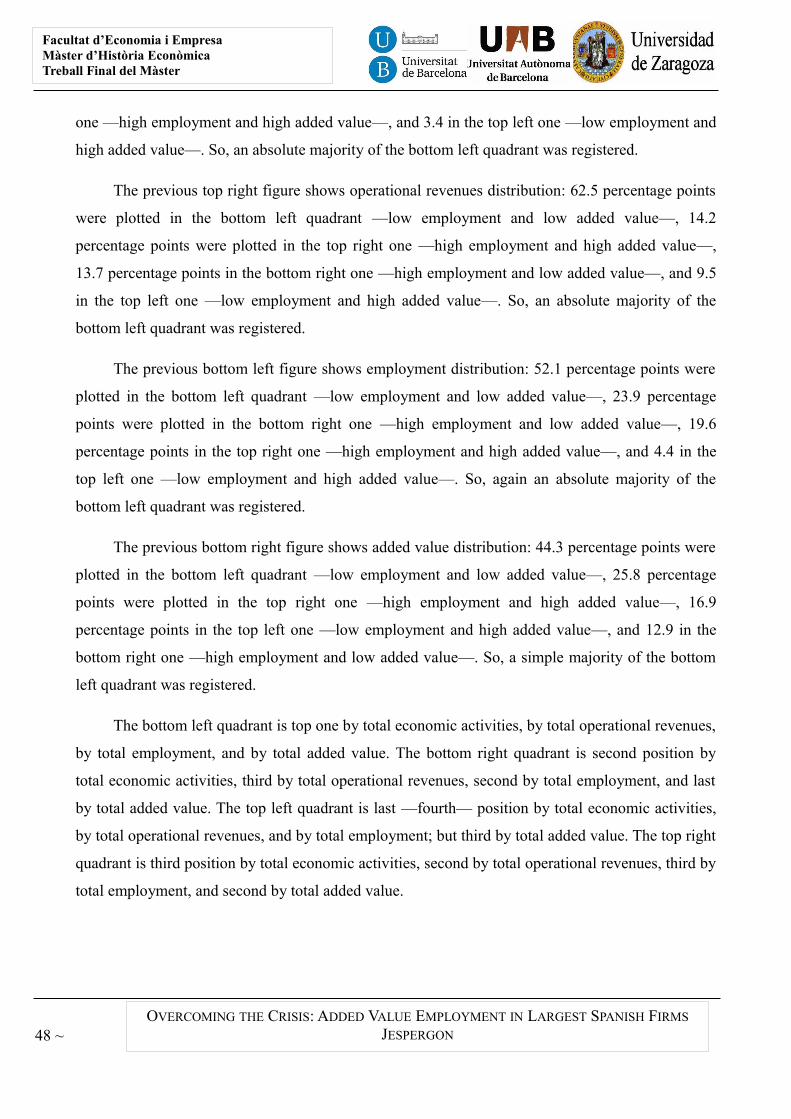

3. Results

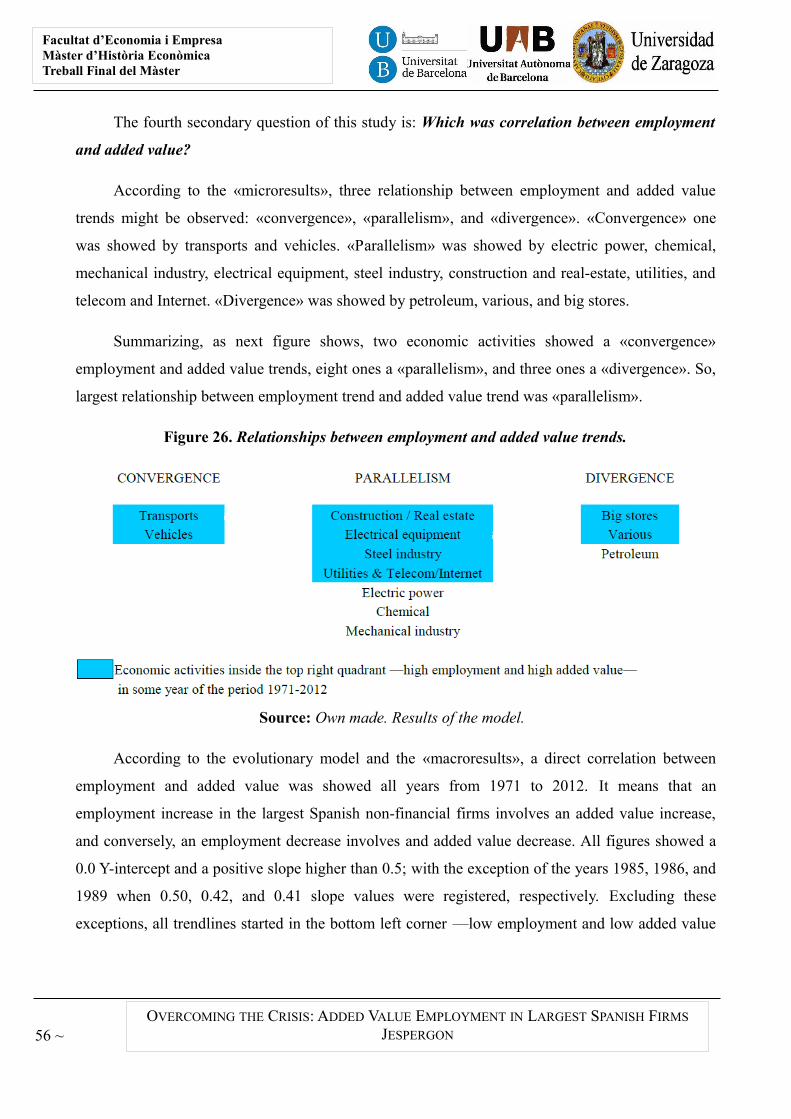

The expected results should must show a continuous path in correspondence with an

evolutionary model in constant adaption to its environment in the absence of radical changes —

technological revolutions—, incremental changes —products, services, processes, market or

organizational innovations—, or internal or external perturbations —political, economic,

sociological, cultural, artificial or natural—.

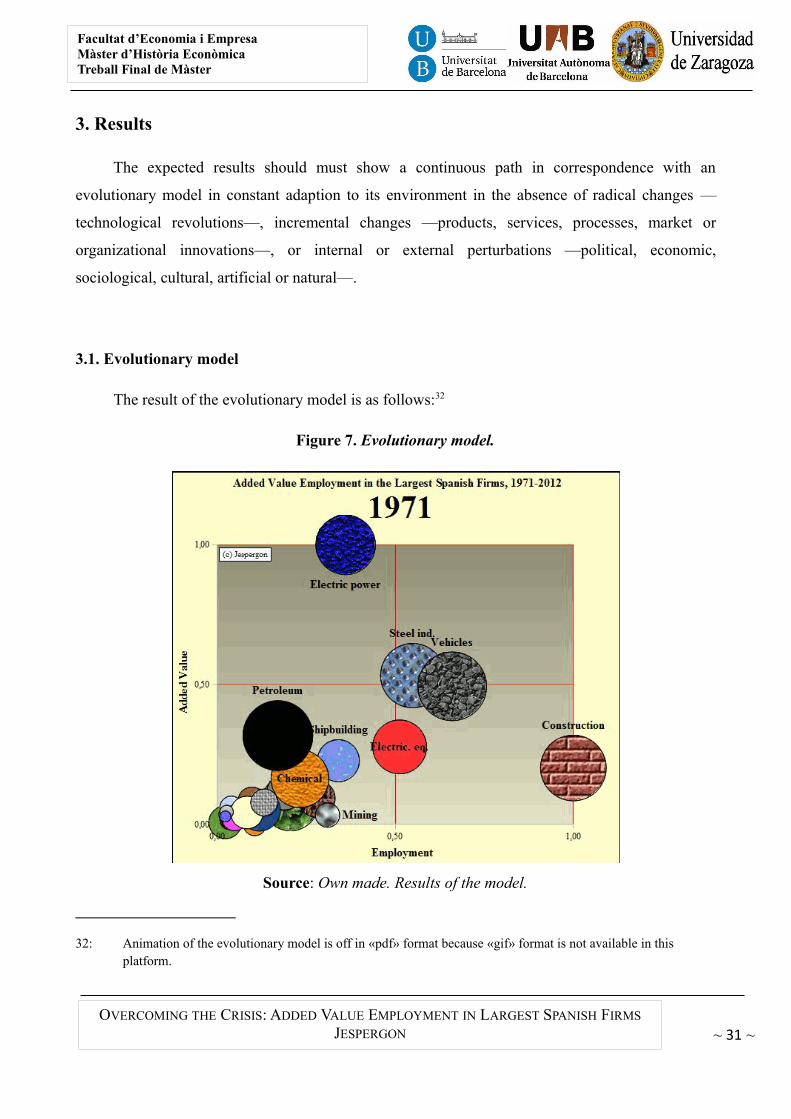

3.1. Evolutionary model

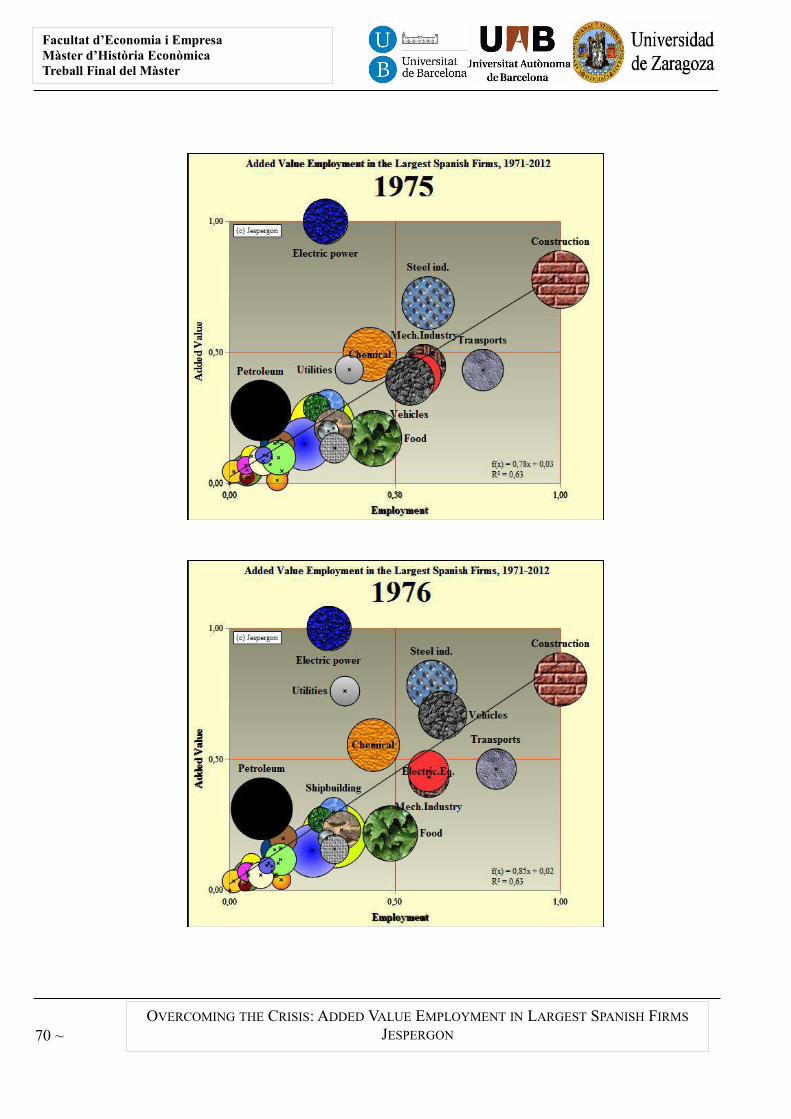

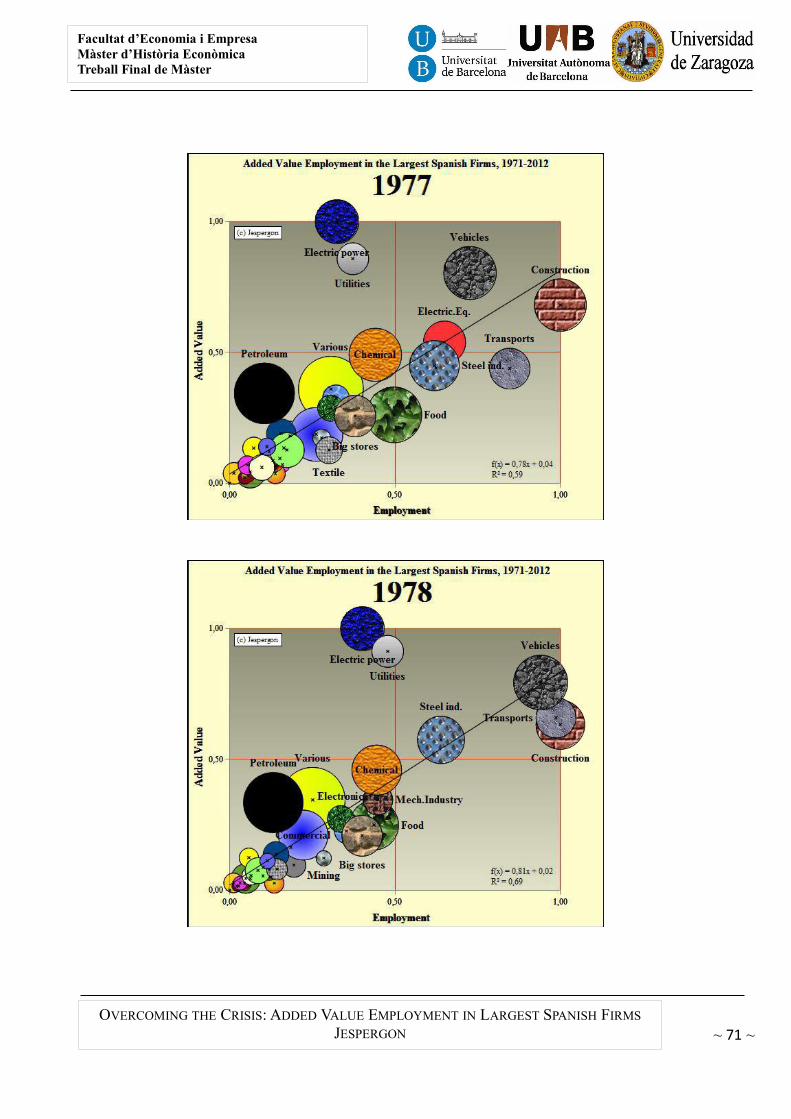

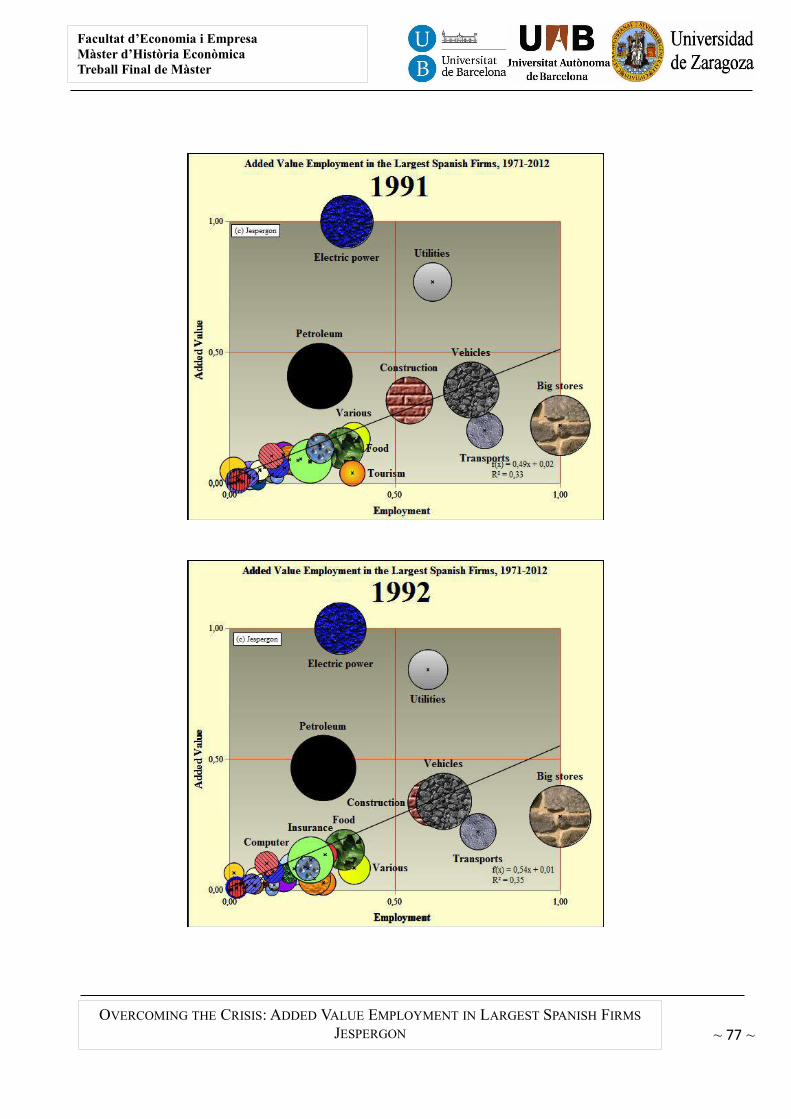

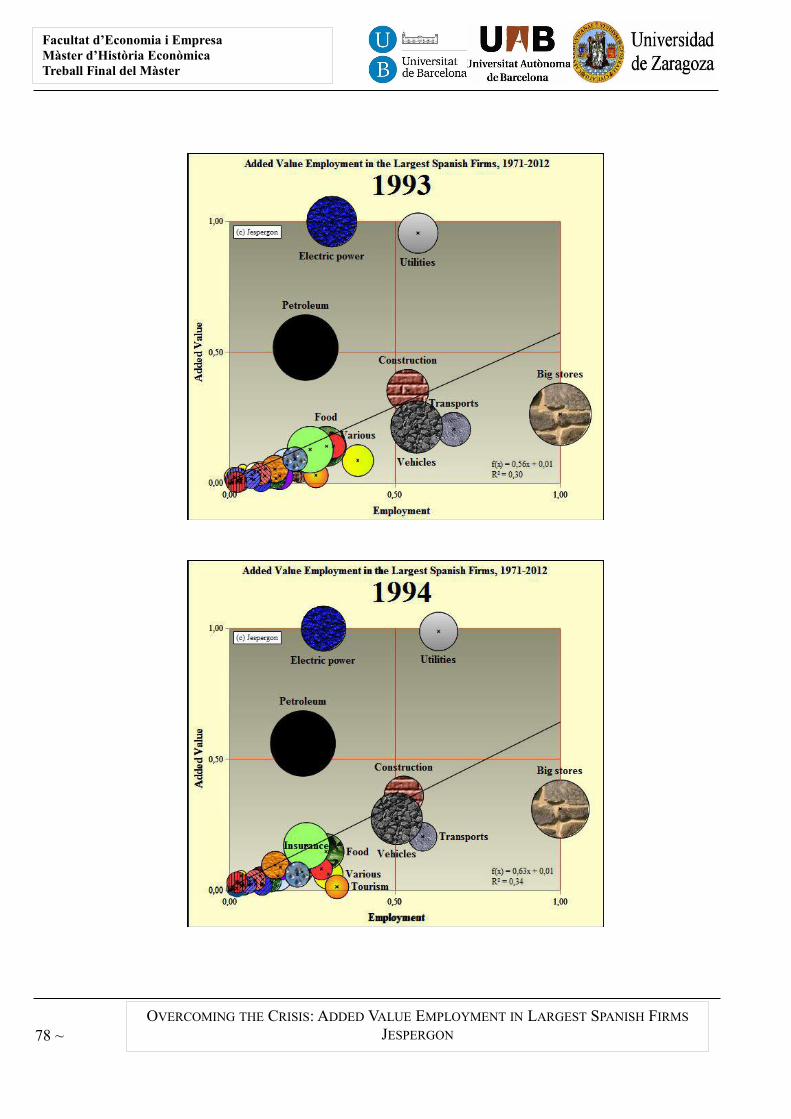

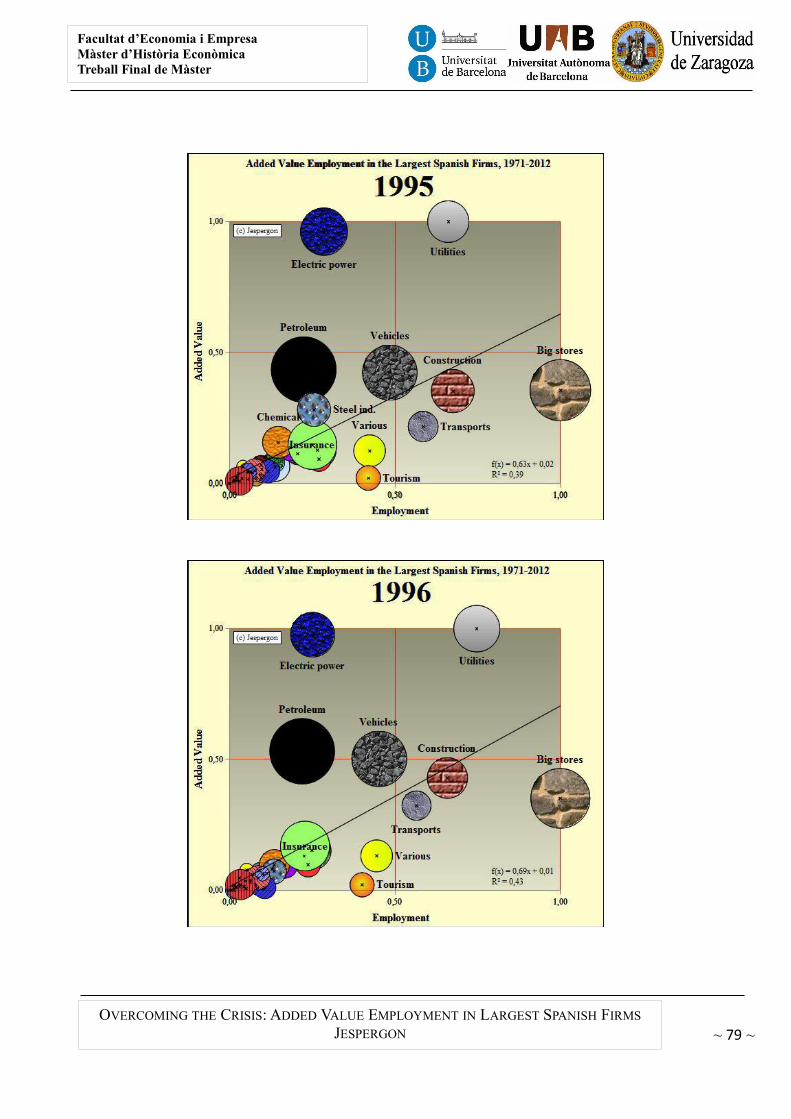

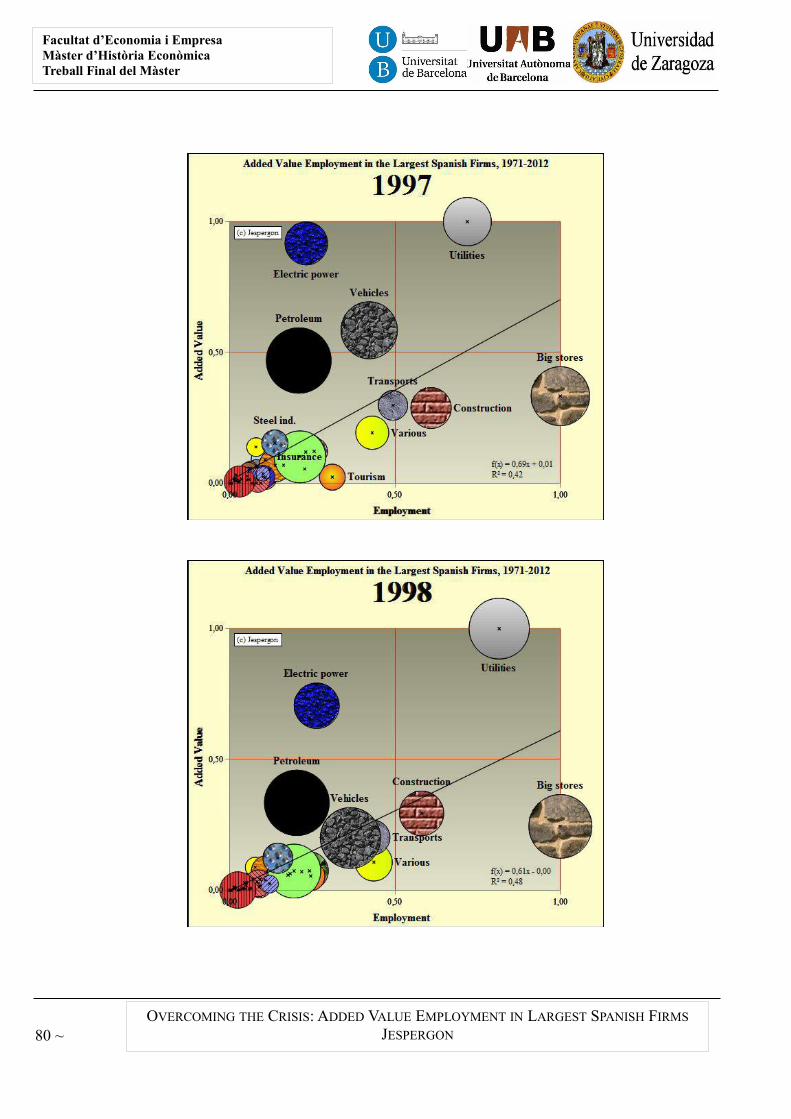

The result of the evolutionary model is as follows:32

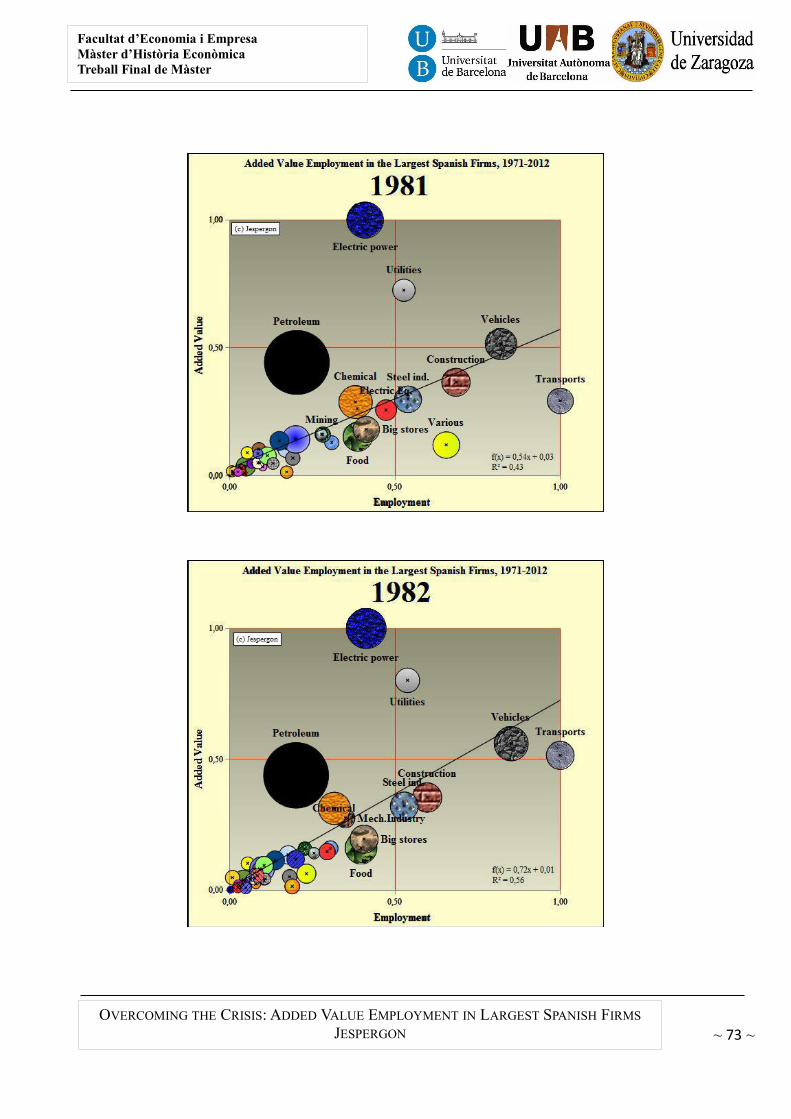

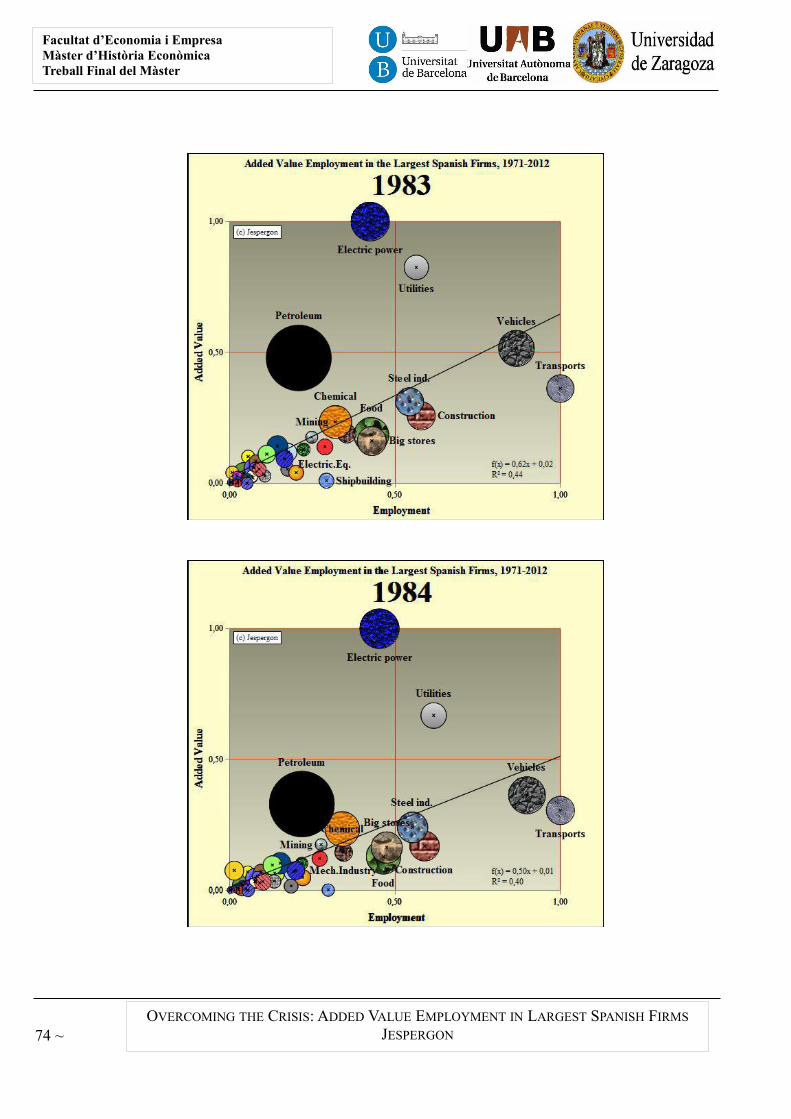

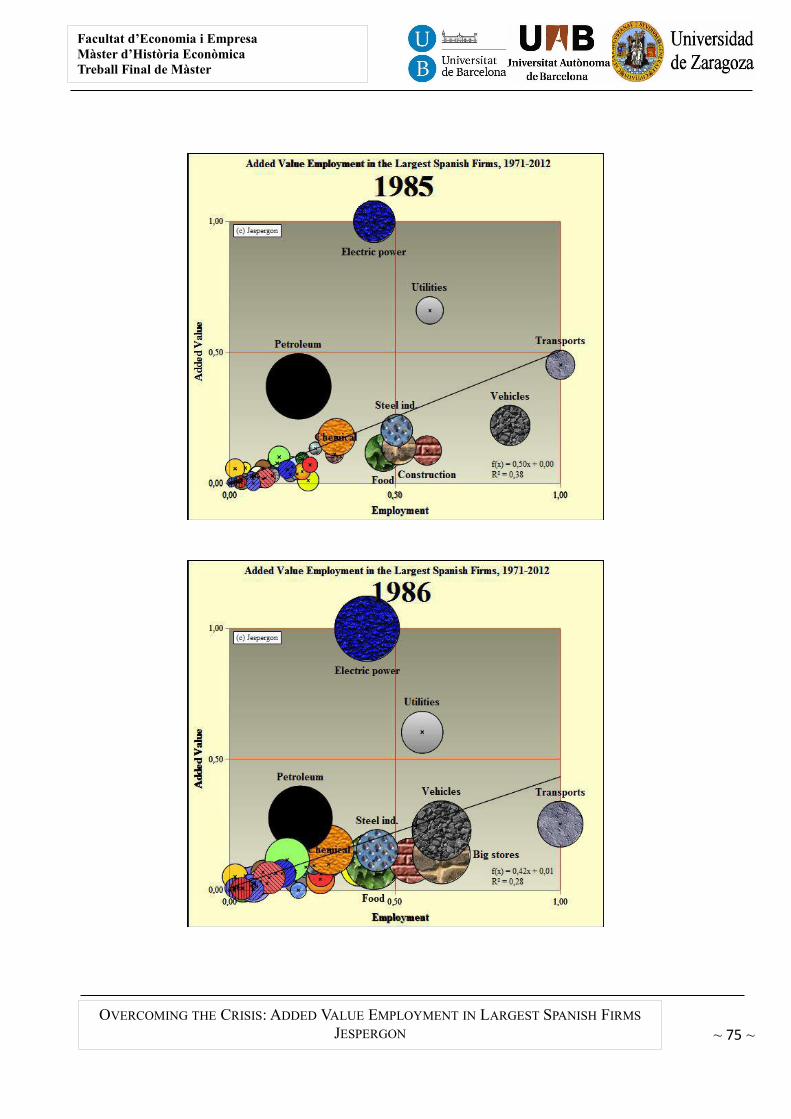

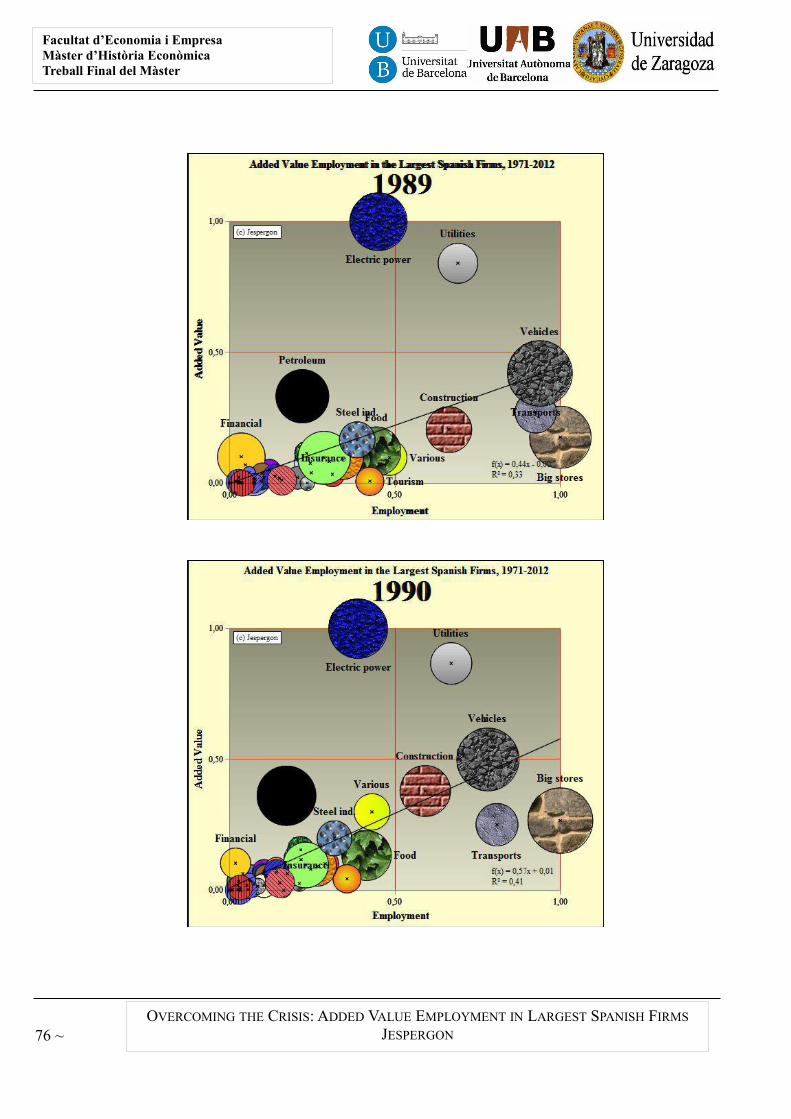

Figure 7. Evolutionary model.

Source: Own made. Results of the model.

32: Animation of the evolutionary model is off in «pdf» format because «gif» format is not available in this platform.

~ 31 ~

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final del Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON

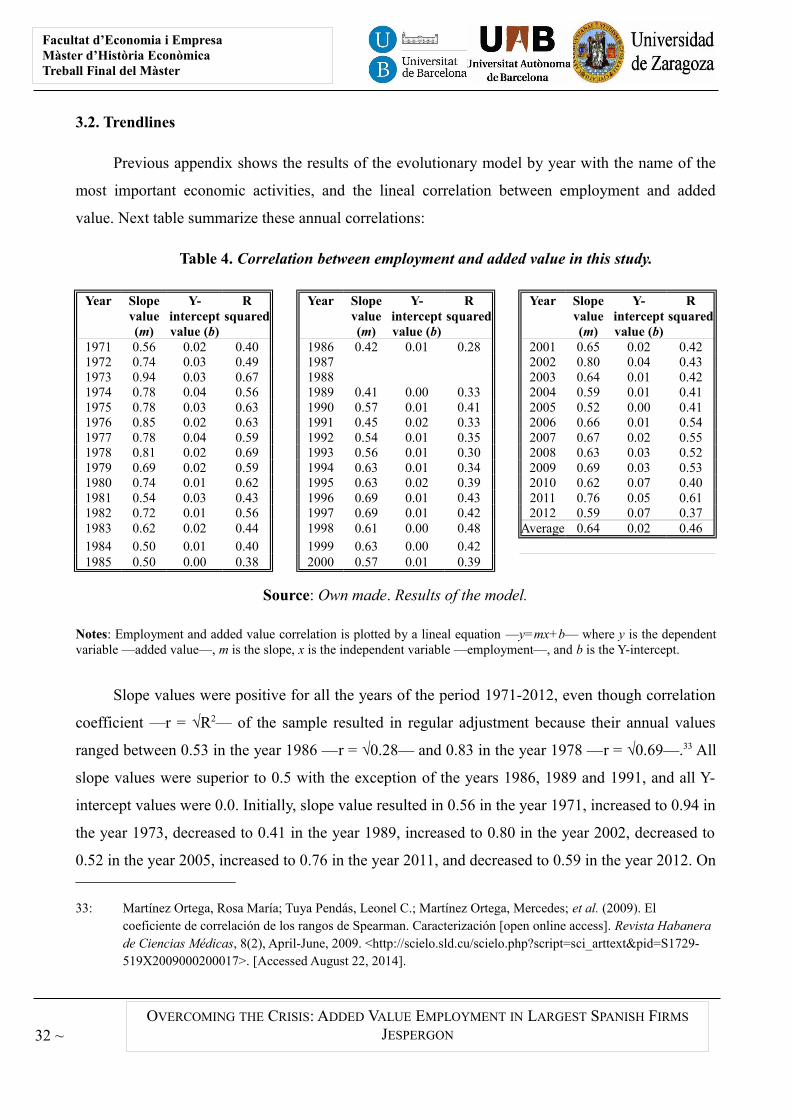

3.2. Trendlines

Previous appendix shows the results of the evolutionary model by year with the name of the

most important economic activities, and the lineal correlation between employment and added

value. Next table summarize these annual correlations:

Table 4. Correlation between employment and added value in this study.

Year Slopevalue(m)

Y-interceptvalue (b)

Rsquared

Year Slopevalue(m)

Y-interceptvalue (b)

Rsquared

Year Slopevalue(m)

Y-interceptvalue (b)

Rsquared

1971 0.56 0.02 0.40 1986 0.42 0.01 0.28 2001 0.65 0.02 0.421972 0.74 0.03 0.49 1987 2002 0.80 0.04 0.431973 0.94 0.03 0.67 1988 2003 0.64 0.01 0.421974 0.78 0.04 0.56 1989 0.41 0.00 0.33 2004 0.59 0.01 0.411975 0.78 0.03 0.63 1990 0.57 0.01 0.41 2005 0.52 0.00 0.411976 0.85 0.02 0.63 1991 0.45 0.02 0.33 2006 0.66 0.01 0.541977 0.78 0.04 0.59 1992 0.54 0.01 0.35 2007 0.67 0.02 0.551978 0.81 0.02 0.69 1993 0.56 0.01 0.30 2008 0.63 0.03 0.521979 0.69 0.02 0.59 1994 0.63 0.01 0.34 2009 0.69 0.03 0.531980 0.74 0.01 0.62 1995 0.63 0.02 0.39 2010 0.62 0.07 0.401981 0.54 0.03 0.43 1996 0.69 0.01 0.43 2011 0.76 0.05 0.611982 0.72 0.01 0.56 1997 0.69 0.01 0.42 2012 0.59 0.07 0.371983 0.62 0.02 0.44 1998 0.61 0.00 0.48 Average 0.64 0.02 0.461984 0.50 0.01 0.40 1999 0.63 0.00 0.421985 0.50 0.00 0.38 2000 0.57 0.01 0.39

Source: Own made. Results of the model.

Notes: Employment and added value correlation is plotted by a lineal equation —y=mx+b— where y is the dependentvariable —added value—, m is the slope, x is the independent variable —employment—, and b is the Y-intercept.

Slope values were positive for all the years of the period 1971-2012, even though correlation

coefficient —r = √R2— of the sample resulted in regular adjustment because their annual values

ranged between 0.53 in the year 1986 —r = √0.28— and 0.83 in the year 1978 —r = √0.69—.33 All

slope values were superior to 0.5 with the exception of the years 1986, 1989 and 1991, and all Y-

intercept values were 0.0. Initially, slope value resulted in 0.56 in the year 1971, increased to 0.94 in

the year 1973, decreased to 0.41 in the year 1989, increased to 0.80 in the year 2002, decreased to

0.52 in the year 2005, increased to 0.76 in the year 2011, and decreased to 0.59 in the year 2012. On

33: Martínez Ortega, Rosa María; Tuya Pendás, Leonel C.; Martínez Ortega, Mercedes; et al. (2009). El coeficiente de correlación de los rangos de Spearman. Caracterización [open online access]. Revista Habanera de Ciencias Médicas, 8(2), April-June, 2009. <http://scielo.sld.cu/scielo.php?script=sci_arttext&pid=S1729-519X2009000200017>. [Accessed August 22, 2014].

32 ~

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final de Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON

average, correlation between employment and added value resulted in 0.02 Y-intercept and 0.64

slope values, and 0.68 correlation coefficient —R squared value of 0.46—.

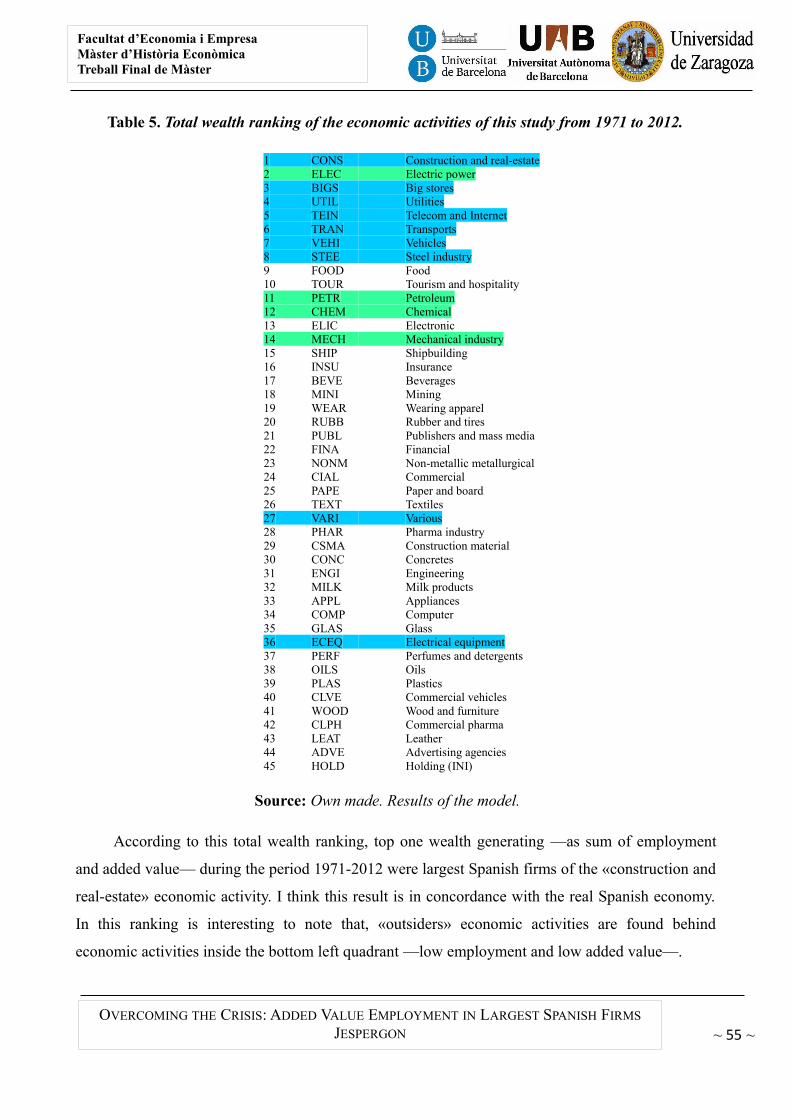

Appendix shows that, of a total of forty five activities, thirty two are in the bottom left

quadrant —low employment and low added value—: oils, food, beverages, rubber/tires, concretes,

commercial, wearing apparel, shipbuilding, publishers/mass media, electronic, financial,

tourism/hospitality, pharma industry, wood and furniture, construction material, non-metallic

metallurgical, mining, paper/board, leather, plastics, milk products, insurance, textile, glass,

holding, advertising agencies, commercial pharma, appliances, computer, engineering,

perfumes/detergents, and commercial vehicles; and, thirteen sectors are outside this quadrant.

Now is time to analyze these outsiders.

3.3. The ««microresults»» of the outsiders

For all graphs in this section, the left graphics show the results of a single economic activity

throughout the whole period in the evolutionary model in constant values, and the right graphics

show the annual quadrant positioning of employment and value added of this economic activity

with their respective lineal trends. If employment and added value positioning data are lower than

0.5, then economic activity is inside the bottom left quadrant —low employment and low added

value—. If employment positioning data is higher than 0.5 and added value positioning data is

lower than 0.5, then economic activity is inside the bottom right quadrant —high employment and

low added value—. If employment positioning data is lower than 0.5 and added value positioning

data is higher than 0.5, then economic activity is inside the top left quadrant —low employment and

low added value—. If employment and added value positioning data are higher than 0.5, then

economic activity is inside the top right quadrant —high employment and high added value—.

Remember that all graphs do not show values for 1987 and 1988 due to the absence of added

value data in the original data source.

The disaggregation of the economic activities outside the bottom left quadrant are as follow:

~ 33 ~

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final del Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON

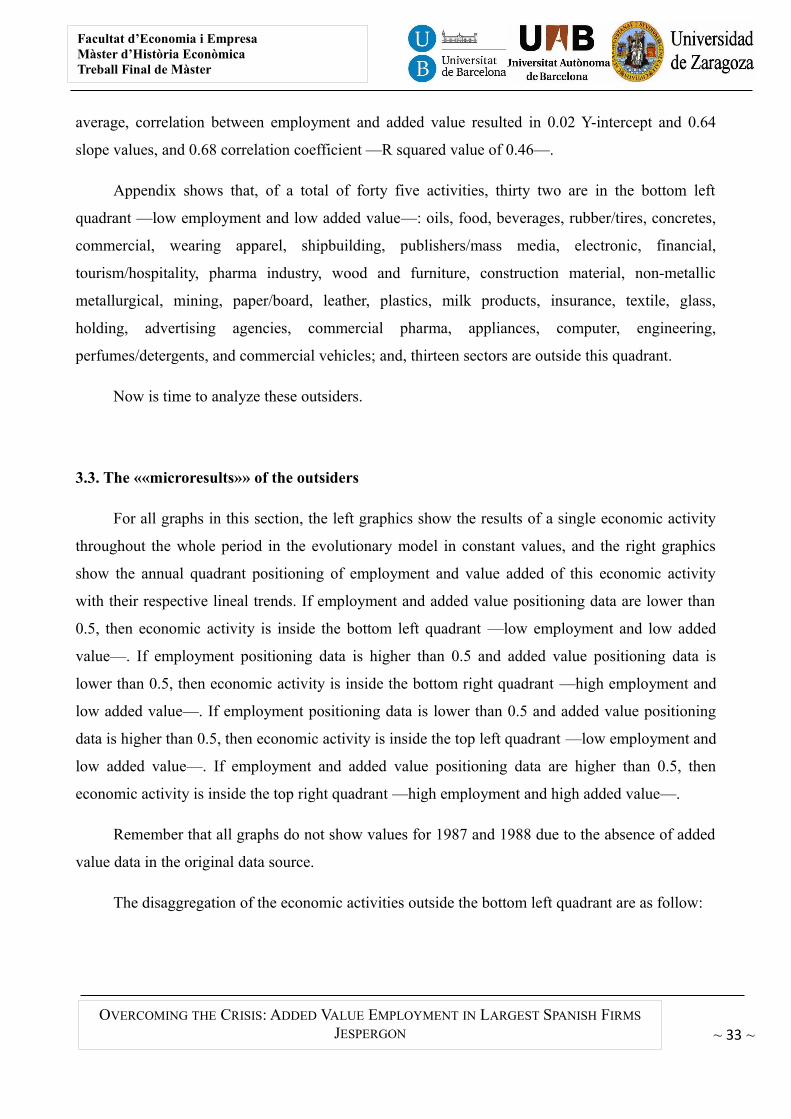

Figure 8. Electric power economic activity results.

Source: Own made. Results of the model.

The electric power economic activity plotted a bubble «continuous path». It evolved inside

the top left quadrant —low employment and high added value— during the whole period 1971-

2012, with the exception of the year 2005 that it appeared in the bottom left quadrant —low

employment and low added value—. It was maximum added value of the sample from 1971 to

1994, when it showed a U-shaped during the period 1994-2012, with the exception of the years

2002 and 2012 when it came back to be maximum added value. It was never maximum

employment of the sample. It showed a «regression» employment lineal trend during the whole

period, and a «regression» added value one from 1990 to 2012. Employment trend evolved from 0.4

points respect to maximum value of the sample in 1971 to under 0.2 points in 2012, and added

value trend evolved from 1 points to under 0.7 points. A «parallelism» relationship between

employment and added value might be inferred.

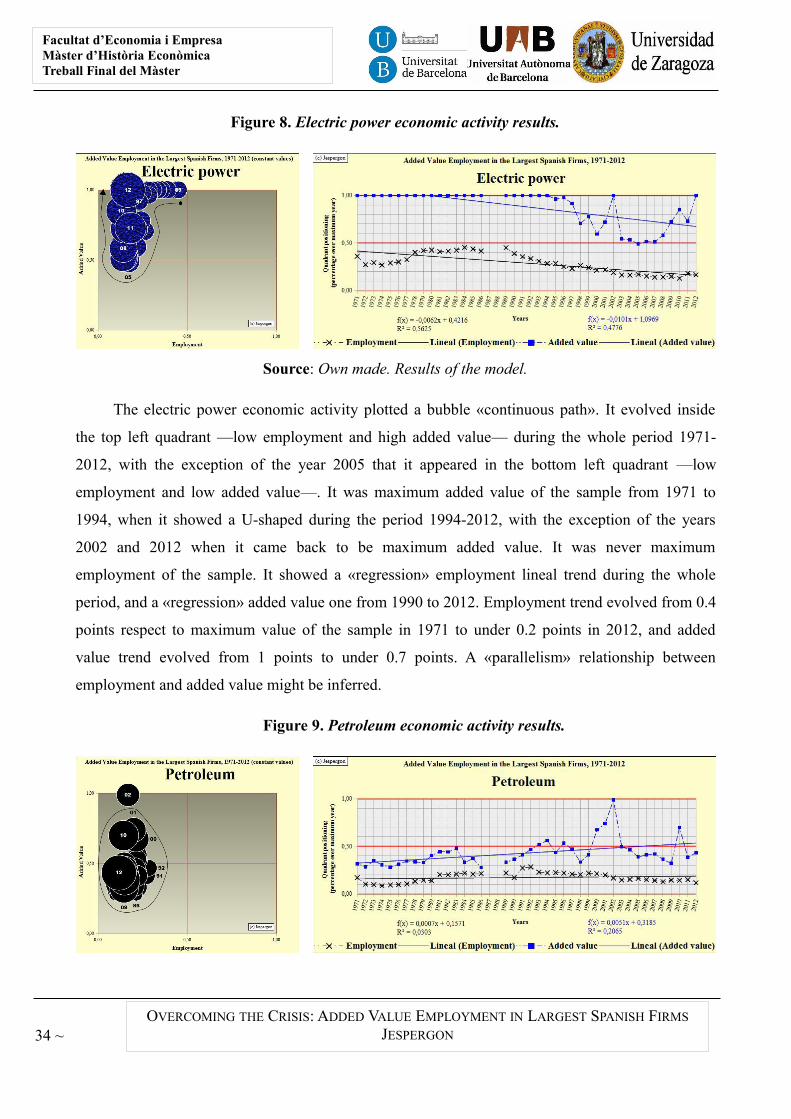

Figure 9. Petroleum economic activity results.

34 ~

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final de Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON

Source: Own made. Results of the model.

The petroleum economic activity plotted a bubble «cumulus» with a positive bubble

«mutation» in the year 2002. It evolved inside the bottom left quadrant —low employment and low

added value— during the whole period 1971-2012, with the exception of the years 1993, 1994,

1996, 2000-2002, and 2010 that they appeared in the top left quadrant —low employment and high

added value—. It was never maximum added value and employment of the sample. It showed a

«constant» employment lineal trend during the whole period with a value near to 0.2 points, and a

«progress» added value one. Added value trend evolved from above 0.3 points in 1971 to above 0.5

points in 2012. Two fast up and down «mutations» need to be mentioned. The first one from 1998

to 2003 when it got its maximum added value scored in the year 2002, and the second one from

2008 to 2011. A «divergence» relationship between employment and added value might be inferred.

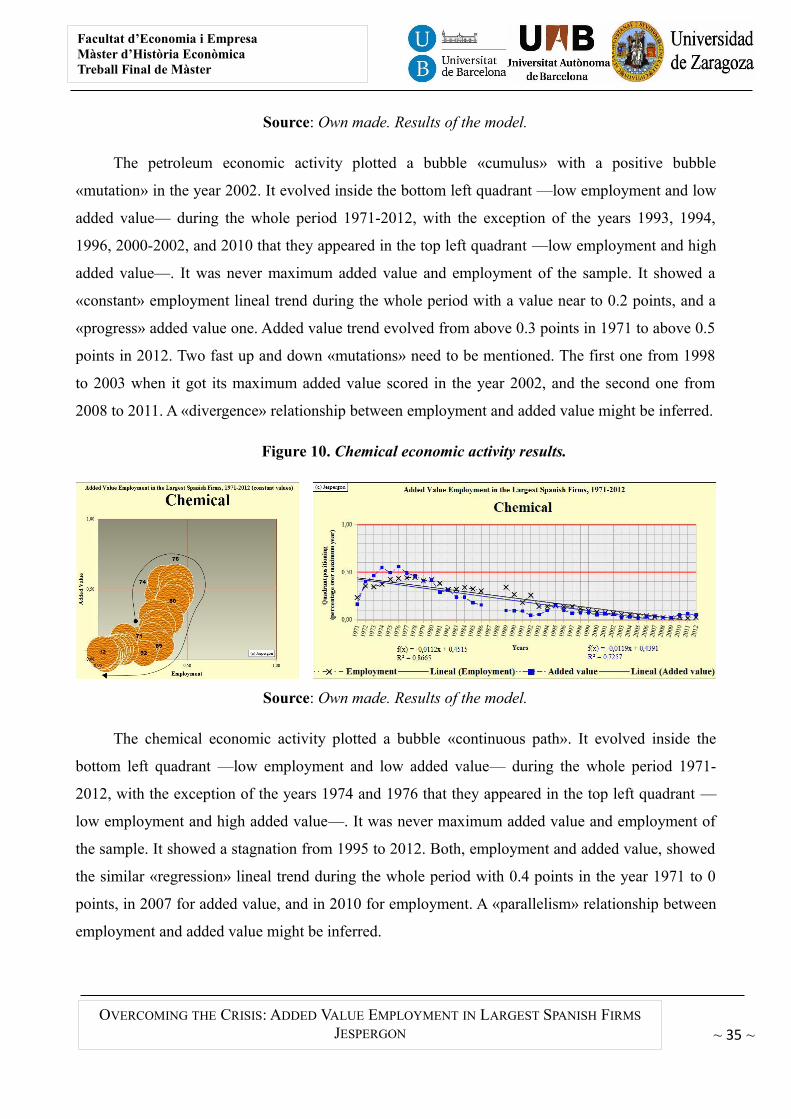

Figure 10. Chemical economic activity results.

Source: Own made. Results of the model.

The chemical economic activity plotted a bubble «continuous path». It evolved inside the

bottom left quadrant —low employment and low added value— during the whole period 1971-

2012, with the exception of the years 1974 and 1976 that they appeared in the top left quadrant —

low employment and high added value—. It was never maximum added value and employment of

the sample. It showed a stagnation from 1995 to 2012. Both, employment and added value, showed

the similar «regression» lineal trend during the whole period with 0.4 points in the year 1971 to 0

points, in 2007 for added value, and in 2010 for employment. A «parallelism» relationship between

employment and added value might be inferred.

~ 35 ~

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final del Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON

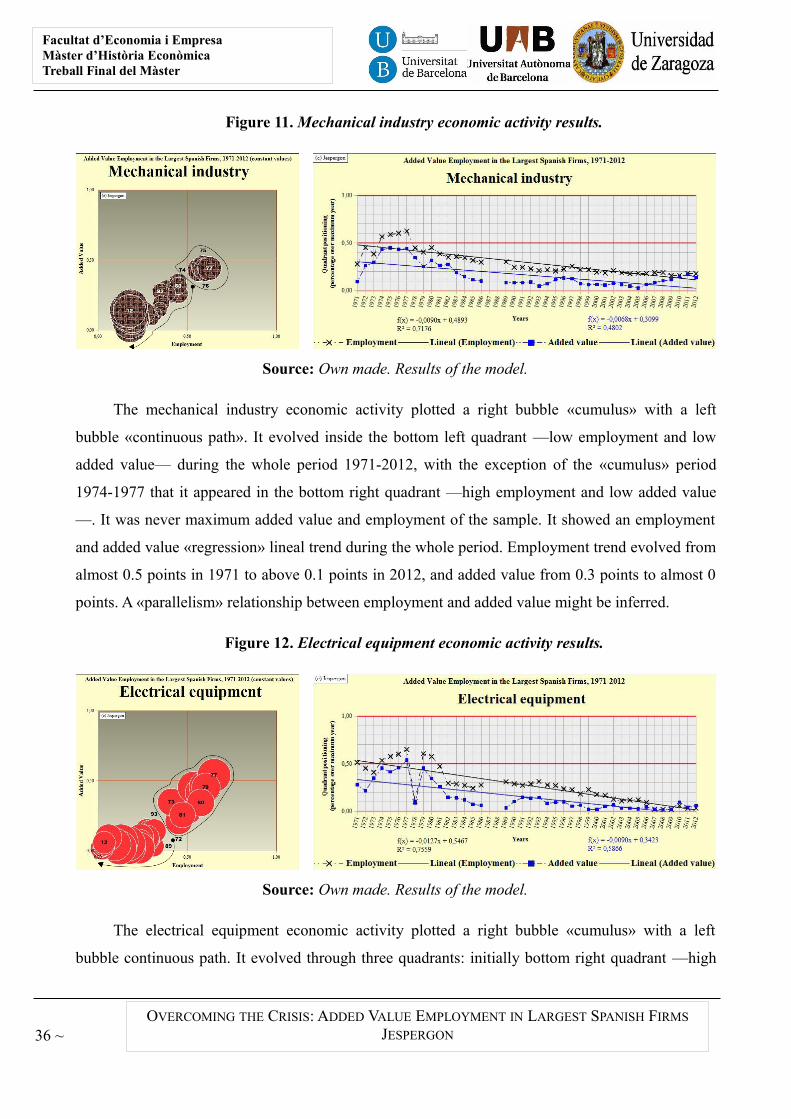

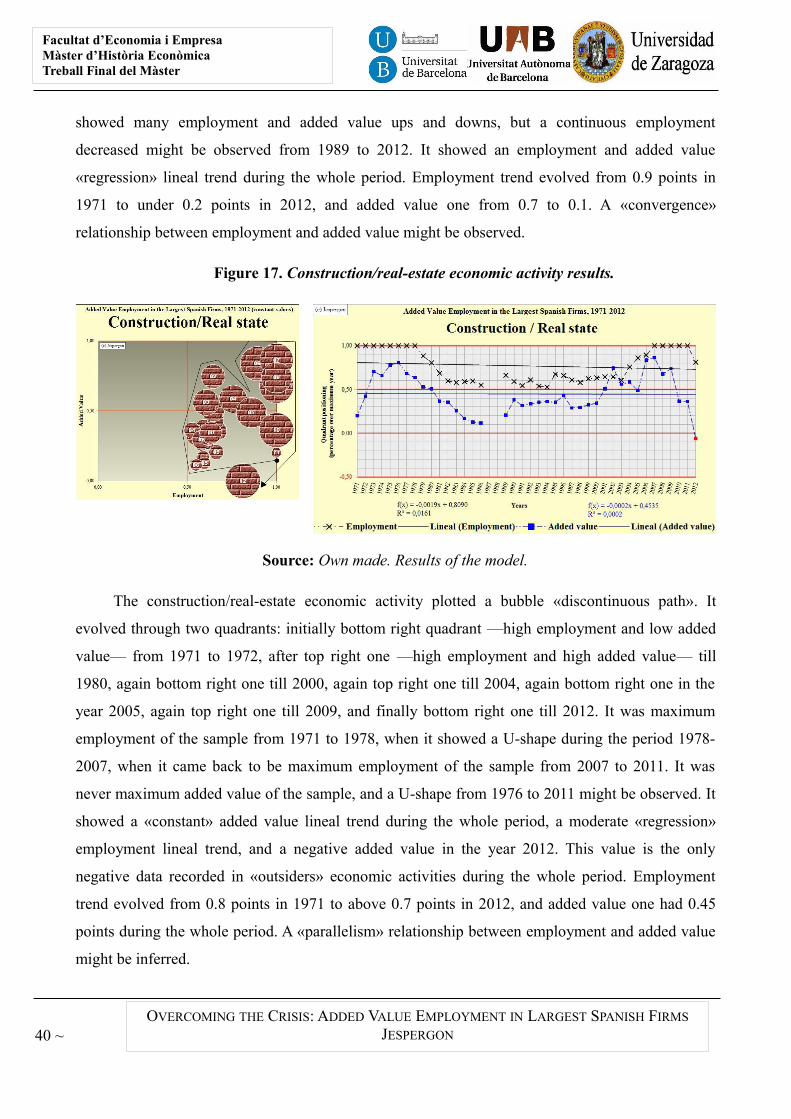

Figure 11. Mechanical industry economic activity results.

Source: Own made. Results of the model.

The mechanical industry economic activity plotted a right bubble «cumulus» with a left

bubble «continuous path». It evolved inside the bottom left quadrant —low employment and low

added value— during the whole period 1971-2012, with the exception of the «cumulus» period

1974-1977 that it appeared in the bottom right quadrant —high employment and low added value

—. It was never maximum added value and employment of the sample. It showed an employment

and added value «regression» lineal trend during the whole period. Employment trend evolved from

almost 0.5 points in 1971 to above 0.1 points in 2012, and added value from 0.3 points to almost 0

points. A «parallelism» relationship between employment and added value might be inferred.

Figure 12. Electrical equipment economic activity results.

Source: Own made. Results of the model.

The electrical equipment economic activity plotted a right bubble «cumulus» with a left

bubble continuous path. It evolved through three quadrants: initially bottom right quadrant —high

36 ~

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final de Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON

employment and low added value— in the year 1971, after bottom left one —low employment and

low added value— till 1974, again bottom right one till 1976, after top right one —high

employment and high added value— in 1977, again bottom left one in 1978, again bottom right one

till 1980, and finally again bottom left one till 2012. It was never maximum added value and

employment of the sample. It showed an employment and added value «regression» lineal trend

during the whole period with a negative «mutation» in the year 1978. Employment trend evolved

from above 0.50 points in 1971 to almost 0 points in 2012, and added value trend from above 0.3

points to 0 points. A «parallelism» relationship between employment and added value might be

inferred.

Figure 13. Steel industry economic activity results.

Source: Own made. Results of the model.

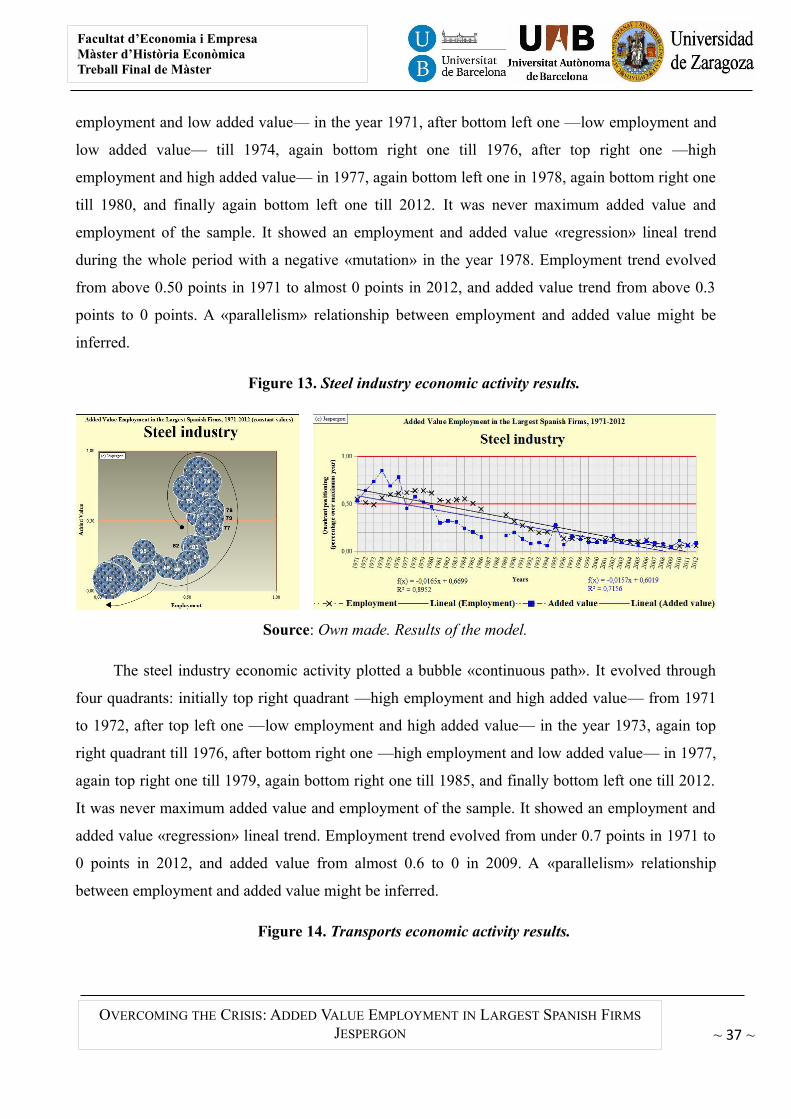

The steel industry economic activity plotted a bubble «continuous path». It evolved through

four quadrants: initially top right quadrant —high employment and high added value— from 1971

to 1972, after top left one —low employment and high added value— in the year 1973, again top

right quadrant till 1976, after bottom right one —high employment and low added value— in 1977,

again top right one till 1979, again bottom right one till 1985, and finally bottom left one till 2012.

It was never maximum added value and employment of the sample. It showed an employment and

added value «regression» lineal trend. Employment trend evolved from under 0.7 points in 1971 to

0 points in 2012, and added value from almost 0.6 to 0 in 2009. A «parallelism» relationship

between employment and added value might be inferred.

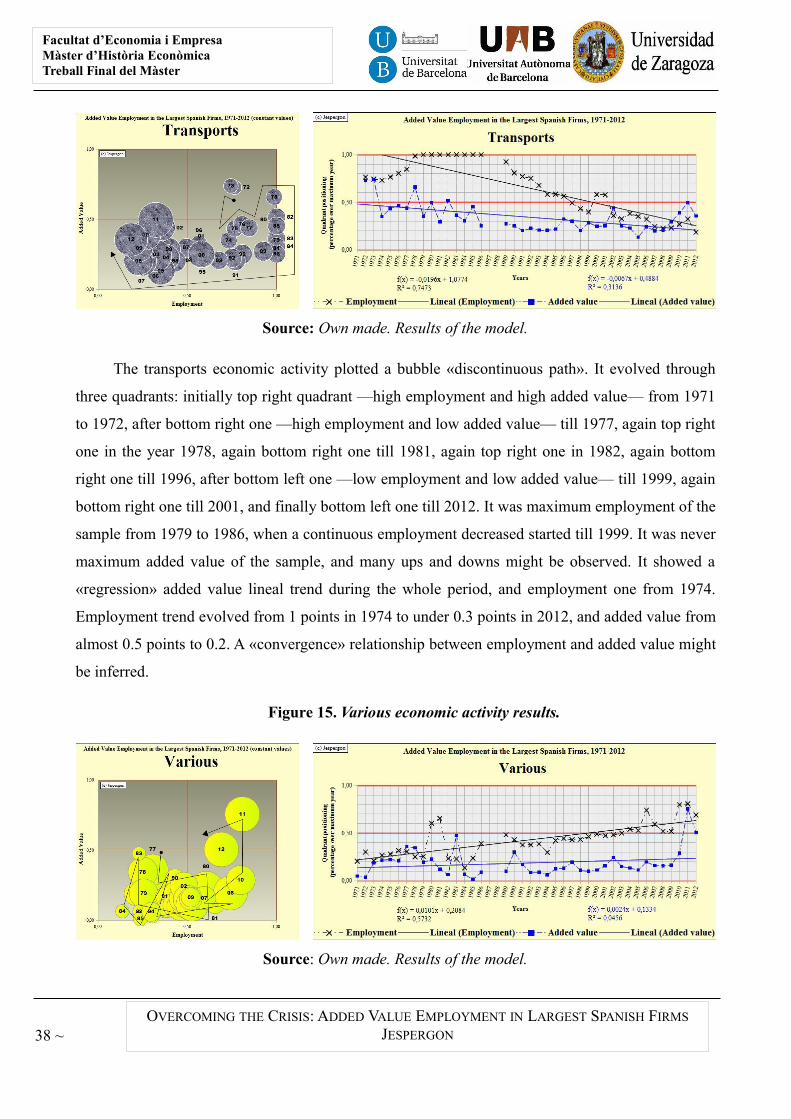

Figure 14. Transports economic activity results.

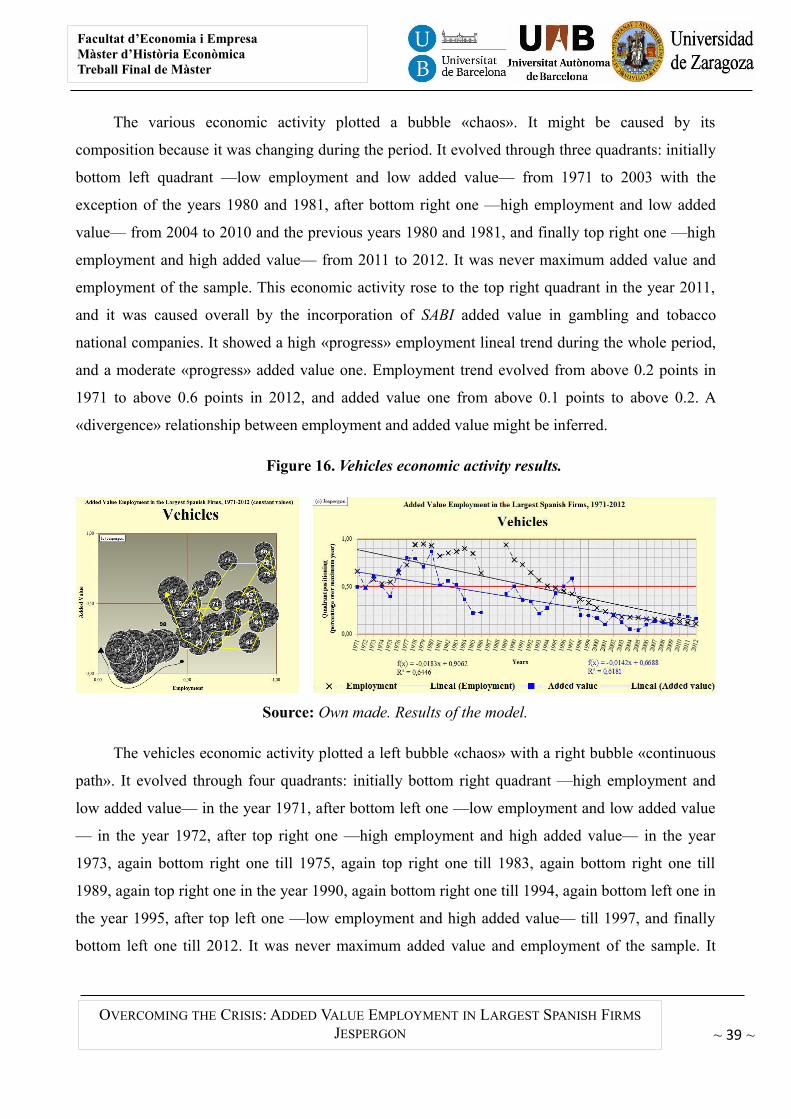

~ 37 ~

Facultat d’Economia i EmpresaMàster d’Història EconòmicaTreball Final del Màster

OVERCOMING THE CRISIS: ADDED VALUE EMPLOYMENT IN LARGEST SPANISH FIRMS

JESPERGON

Source: Own made. Results of the model.

The transports economic activity plotted a bubble «discontinuous path». It evolved through

three quadrants: initially top right quadrant —high employment and high added value— from 1971

to 1972, after bottom right one —high employment and low added value— till 1977, again top right

one in the year 1978, again bottom right one till 1981, again top right one in 1982, again bottom

right one till 1996, after bottom left one —low employment and low added value— till 1999, again

bottom right one till 2001, and finally bottom left one till 2012. It was maximum employment of the

sample from 1979 to 1986, when a continuous employment decreased started till 1999. It was never

maximum added value of the sample, and many ups and downs might be observed. It showed a