Embed Size (px)

Citation preview

AUDIT TAX SYSTEMS ADVISORY

Always Accretive. . . …

Arvil Stanford

Audit Partner

Always Accretive…

Accounting Playbook

Expectation -

General Areas of Discussion -

Q&A

Highlight Real

Focus on awareness

Private Company Council (PCC)

Selected Accounting Standard Updates (ASU)

FASB Simplification Initiative

U.S. & International Convergence

Always Accretive…

Alumni & Friends Tailgate - A&A Playbook

Selected Accounting Standard Updates for

2014

ASU 2014-08

ASU 2014-09

ASU 2014-10

ASU 2014-15

Always Accretive…

Alumni & Friends Tailgate - A&A Playbook

ASU 2014-08

Reporting Discontinued Operations and

Disclosures of Disposals of Components of an

Entity

April 2014

Always Accretive…

ASU 2014-08 Reporting Discontinued Operations & Disclosures of Disposals of Components of an Entity

Why Is the FASB Issuing This Accounting Standards Update? Feedback to Board –

Too many disposals recurring in nature qualify for discontinued operations presentation.

That results in financial statements that are less decision useful for users.

Other stakeholders noted – Some of the guidance on reporting discontinued operations results in higher costs for

preparers

It can be complex and difficult to apply.

The amendments in this Update address those issues by changing the criteria for reporting discontinued operations

Enhancing convergence with IASB reporting requirements.

Always Accretive…

ASU 2014-08 Reporting Discontinued Operations & Disclosures of Disposals of Components of an Entity

What are the main provisions? The amendments in this Update change the requirements for reporting

discontinued operations in Subtopic 205-20.

A disposal is required to be reported in discontinued operations if the disposal represents a strategic shift that has (or will have) a major effect on an entity’s operations and financial results when any of the following occurs:

The component of an entity meets the criteria to be classified as held for sale.

The component of an entity is disposed of by sale.

The component of an entity is disposed of other than by sale (for example, by abandonment or in a distribution to owners in a spinoff)

Always Accretive…

ASU 2014-08 Reporting Discontinued Operations & Disclosures of Disposals of Components of an Entity

What are the main provisions? Requires an entity to present, for each comparative period, the assets

and liabilities of a disposal group that includes a discontinued operation separately in the asset and liability sections, respectively, of the statement of financial position.

The amendments require additional disclosures about discontinued operations, including: Major classes of line items constituting pretax profit or loss

Total operating and investing cash flows or depreciation, amortization, capital expenditures, and significant operating and investing noncash items

Reconciliation of major classes of assets and liabilities of the discontinued operation classified as held for sale

Reconciliation of major classes of line items constituting pretax profit or loss as disclosed in the notes to the financial statements.

Always Accretive…

ASU 2014-08 Reporting Discontinued Operations & Disclosures of Disposals of Components of an Entity

What are the main provisions?

Requires all other entities to provide disclosures about a disposal of an individually significant component of an entity that does not qualify for discontinued operations presentation in the financial statements, including: The pretax profit or loss attributable to the component of an entity for the

period in which it is disposed of or is classified as held for sale

If the component of an entity includes a noncontrolling interest, the pretax profit or loss attributable to the parent for the period in which it is disposed of or is classified as held for sale.

Always Accretive…

ASU 2014-08 Reporting Discontinued Operations & Disclosures of Disposals of Components of an Entity

What are the main provisions?

Expands the disclosures about an entity’s significant continuing involvement with a discontinued operation, including:

The amount of any cash inflows (outflows) from (to) the discontinued operation

following its disposal

Information about a discontinued operation in which an entity retains an equity method investment after disposal transaction.

Always Accretive…

ASU 2014-08 Reporting Discontinued Operations & Disclosures of Disposals of Components of an Entity

Effective Dates:

Public entities – apply amendments prospectively for events occurring

within annual periods beginning on or after December 15, 2014, and interim periods within those years

All other entities – apply amendments prospectively for events occurring within annual periods beginning on or after December 15, 2014, and interim periods within annual periods beginning on or after December 15, 2015

Always Accretive…

Alumni & Friends Tailgate - A&A Playbook

ASU 2014-09

Revenue from Contracts with Customers

May 2014

Always Accretive…

ASU 2014-09 Revenue From Contracts with Customers

Why is the FASB Issuing This Accounting Standards Update? Revenue is an important number to users of financial statements.

Previous revenue recognition requirements in U.S. GAAP differ from those in IFRS,

and both sets of requirements were in need of improvement.

Previous revenue recognition guidance (U.S.) comprised broad revenue recognition concepts together with numerous revenue requirements

for particular industries or transactions,

which sometimes resulted in different accounting for economically similar transactions.

In contrast, IFRS provided limited guidance IAS 18, Revenue, and IAS 11, Construction Contracts, could be difficult to apply to complex

transactions.

Additionally, IAS 18 provides limited guidance on important revenue topics such as accounting for multiple-element arrangements.

Always Accretive…

ASU 2014-09 Revenue From Contracts with Customers

Why is the FASB Issuing This Accounting Standards Update? The FASB and the IASB initiated a joint project to clarify the principles for

recognizing revenue and to develop a common revenue standard for U.S. GAAP and IFRS that would: Remove inconsistencies and weaknesses in revenue requirements.

Provide a more robust framework for addressing revenue issues.

Improve comparability of revenue recognition practices across entities, industries, jurisdictions, and capital markets.

Provide more useful information to users of financial statements through improved disclosure requirements.

Simplify the preparation of financial statements by reducing the number of requirements to which an entity must refer.

Always Accretive…

ASU 2014-09 Revenue From Contracts with Customers

Why is the FASB Issuing This Accounting Standards Update?

To meet those objectives, the FASB is amending the FASB Accounting Standards Codification® and

creating a new Topic 606, Revenue from Contracts with Customers,

and the IASB is issuing IFRS 15, Revenue from Contracts with Customers.

The issuance of these documents completes the joint effort by the FASB and the IASB to meet those objectives and improve financial reporting by creating common revenue recognition guidance for U.S. GAAP and IFRS.

Always Accretive…

ASU 2014-09 Revenue From Contracts with Customers

What are the main provisions:

The core principle of the guidance is an entity should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services.

Always Accretive…

ASU 2014-09 Revenue From Contracts with Customers

What are the main provisions?

To achieve that core principle, an entity should apply the following steps:

Identify the contract with a customer

Identify the performance obligations (promises) in the contract

Determine the transaction price

Allocate the transaction price to the performance obligations in the contract

Recognize revenue when (or as) the reporting organization satisfies performance obligations

Always Accretive…

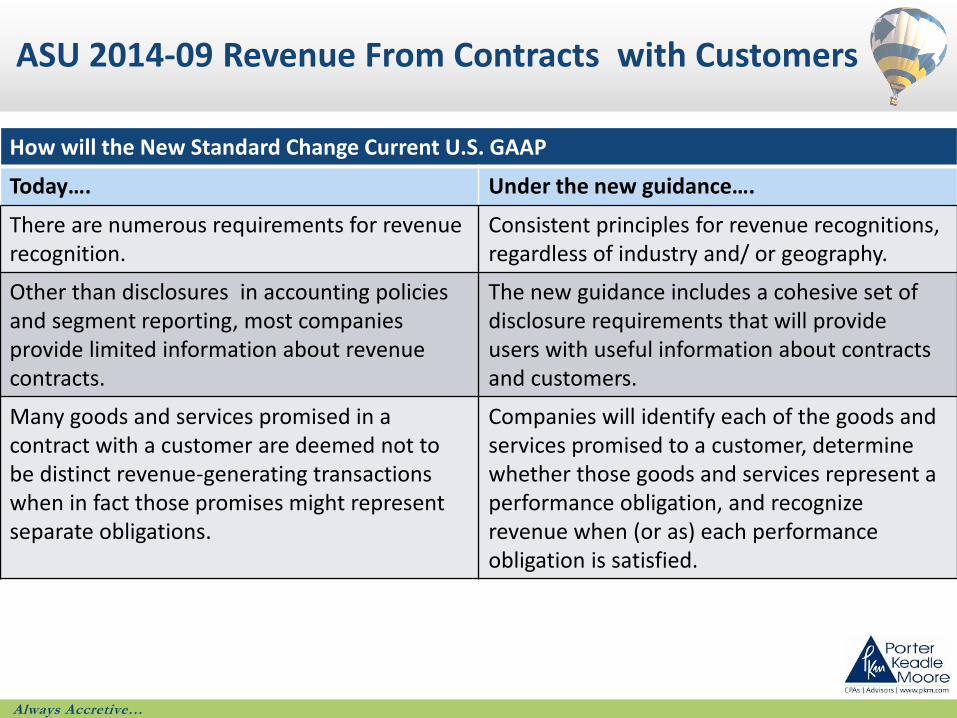

ASU 2014-09 Revenue From Contracts with Customers

How will the New Standard Change Current U.S. GAAP

Today…. Under the new guidance….

There are numerous requirements for revenue recognition.

Consistent principles for revenue recognitions, regardless of industry and/ or geography.

Other than disclosures in accounting policies and segment reporting, most companies provide limited information about revenue contracts.

The new guidance includes a cohesive set of disclosure requirements that will provide users with useful information about contracts and customers.

Many goods and services promised in a contract with a customer are deemed not to be distinct revenue-generating transactions when in fact those promises might represent separate obligations.

Companies will identify each of the goods and services promised to a customer, determine whether those goods and services represent a performance obligation, and recognize revenue when (or as) each performance obligation is satisfied.

Always Accretive…

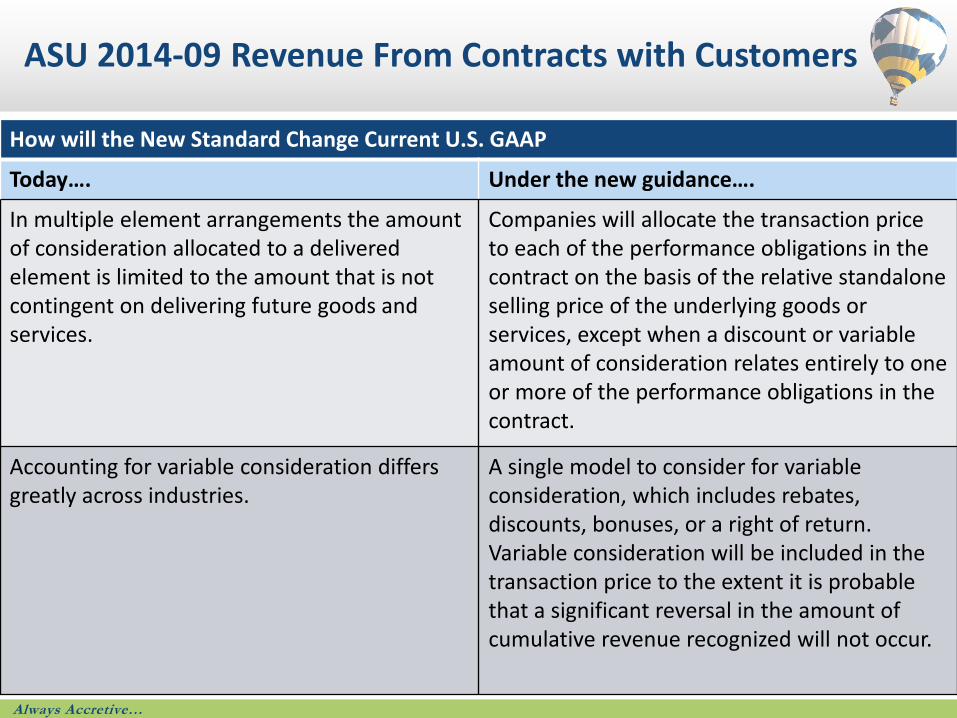

ASU 2014-09 Revenue From Contracts with Customers

How will the New Standard Change Current U.S. GAAP

Today…. Under the new guidance….

In multiple element arrangements the amount of consideration allocated to a delivered element is limited to the amount that is not contingent on delivering future goods and services.

Companies will allocate the transaction price to each of the performance obligations in the contract on the basis of the relative standalone selling price of the underlying goods or services, except when a discount or variable amount of consideration relates entirely to one or more of the performance obligations in the contract.

Accounting for variable consideration differs greatly across industries.

A single model to consider for variable consideration, which includes rebates, discounts, bonuses, or a right of return. Variable consideration will be included in the transaction price to the extent it is probable that a significant reversal in the amount of cumulative revenue recognized will not occur.

Always Accretive…

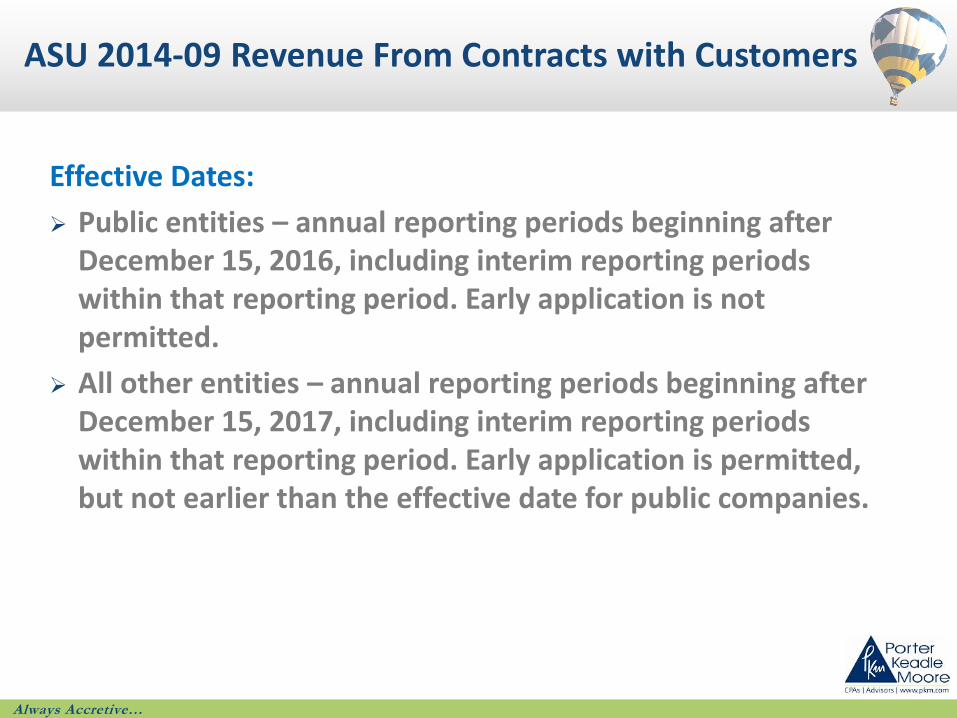

ASU 2014-09 Revenue From Contracts with Customers

Effective Dates:

Public entities – annual reporting periods beginning after December 15, 2016, including interim reporting periods within that reporting period. Early application is not permitted.

All other entities – annual reporting periods beginning after December 15, 2017, including interim reporting periods within that reporting period. Early application is permitted, but not earlier than the effective date for public companies.

Always Accretive…

Alumni & Friends Tailgate - A&A Playbook

ASU 2014-10

Development Stage Entities: Elimination of

Certain Financial Reporting Requirements

June 2014

Always Accretive…

AUP 2014-10 Development Stage Entities – Elimination of Certain Financial Reporting Requirements

Why is the FASB Issuing This Accounting Standards Update? Feedback from users told the Board;

The development stage entity distinction

The inception-to-date information

And certain other disclosures currently required under GAAP in the financial statements of development stage entities

Provide information that has limited relevance and is generally not decision useful.

As a result, the amendments in this Update remove All incremental financial reporting requirements from U.S. GAAP for development stage

entities,

Thereby improving financial reporting by eliminating the cost and complexity associated with providing that information.

Always Accretive…

ASU 2014-10 Development Stage Entities – Elimination of Certain Financial Reporting Requirements

What are the main provisions?

Remove the definition of a development stage entity from the Codification.

In addition, the amendments eliminate the requirements for development stage entities to: Present inception-to-date information in the statements of income,

cash flows, and shareholder equity,

Label the financial statements as those of a development stage entity,

Disclose a description of the development stage activities in which the entity is engaged, and

Disclose in the first year in which the entity is no longer a development stage entity that in prior years it had been in the development stage.

Always Accretive…

ASU 2014-10 Development Stage Entities – Elimination of Certain Financial Reporting Requirements

Effective Dates:

Retrospective application

Public entities – effective for annual reporting periods beginning after December 15, 2014, and interim periods therein.

For other entities – effective for annual reporting periods beginning after December 15, 2014, and interim reporting periods beginning after December 15, 2015.

Always Accretive…

Alumni & Friends Tailgate - A&A Playbook

ASU 2014-15

Presentation of Financial Statements – Going

Concern

August 2014

Always Accretive…

Disclosure of Uncertainties about an Entity’s Ability to Continue as a Going Concern

Why is the FASB Issuing This Accounting Standards Update? Under GAAP

Continuation of a reporting entity as a going concern is presumed as the basis for preparing financial statements

Unless and until the entity’s liquidation becomes imminent.

Even if an entity’s liquidation is not imminent There may be conditions or events that raise substantial doubt about the entity’s ability

to continue as a going concern.

In those situations FS’s should continue to be prepared under the going concern basis of accounting,

But the amendments in this Update should be followed to determine whether to disclose information about the relevant conditions and events.

Always Accretive…

Disclosure of Uncertainties about an Entity’s Ability to Continue as a Going Concern

Why is the FASB Issuing This Accounting Standards Update? There is no guidance in GAAP about management’s responsibility

To evaluate whether there is substantial doubt about an entity’s ability to continue as a going concern

Or to provide related footnote disclosures.

Feedback to the Board Indicating that because of the lack of guidance in GAAP

And the differing views about when there is substantial doubt about an entity’s ability to continue as a going concern,

There is diversity in whether, when, and how an entity discloses the relevant conditions and events in its footnotes.

The amendments provide guidance about management’s responsibility to Evaluate whether there is substantial doubt about an entity’s ability to continue as a

going concern

And to provide related footnote disclosures.

Always Accretive…

Disclosure of Uncertainties about an Entity’s Ability to Continue as a Going Concern

What are the main provisions? An entity’s management should evaluate whether there are

Conditions or events,

Considered in the aggregate,

That raise substantial doubt about the entity’s ability to continue as a going concern

Within one year after the date of issuance.

Substantial doubt about an entity’s ability to continue as a going concern exists when Relevant conditions and events,

Considered in the aggregate,

Indicate that it is probable that the entity will be unable to meet its obligations as they become due

Within one year after the date that the financial statements are issued.

Always Accretive…

Disclosure of Uncertainties about an Entity’s Ability to Continue as a Going Concern

What are the main provisions? When management identifies conditions or events that raise substantial

doubt about an entity’s ability to continue as a going concern, Management should consider whether its plans that are intended to mitigate those

relevant conditions or events

Will alleviate the substantial doubt.

The mitigating effect of management’s plans should be considered only to the extent that

It is probable that the plans will be effectively implemented and, if so,

It is probable that the plans will mitigate the conditions or events that raise substantial doubt about the entity’s ability to continue as a going concern.

Always Accretive…

Disclosure of Uncertainties about an Entity’s Ability to Continue as a Going Concern

What are the main provisions?

If substantial doubt exist,

But the substantial doubt is alleviated as a result of consideration of management’s plans,

The entity should disclose information that enables users of the financial statements to understand all of the following:

Principal conditions or events that raised substantial doubt about the entity’s ability to continue as a going concern (before consideration of management’s plans)

Management’s evaluation of the significance of those conditions or events in relation to the entity’s ability to meet its obligations

Management’s plans that alleviated substantial doubt about the entity’s ability to continue as a going concern.

Always Accretive…

Disclosure of Uncertainties about an Entity’s Ability to Continue as a Going Concern

What are the main provisions?

If substantial doubt exist,

and not alleviated after consideration of management’s plans,

an entity should include a statement in the footnotes indicating that there is substantial doubt about the entity’s ability to continue as a going concern within one year after the date that the financial statements are issued.

Additionally, the entity should disclose the following:

Principal conditions or events that raise substantial doubt about the entity’s ability to continue as a going concern

Management’s evaluation of the significance of those conditions or events in relation to the entity’s ability to meet its obligations

Management’s plans that are intended to mitigate the conditions or events that raise substantial doubt about the entity’s ability to continue as a going concern.

Always Accretive…

Disclosure of Uncertainties about an Entity’s Ability to Continue as a Going Concern

Effective Date:

Effective for the annual period ending after December 15, 2016, and for annual periods and interim periods thereafter.

Early application is permitted.

Always Accretive…

Alumni & Friends Tailgate - A&A Playbook

Private Company Council (PCC)

ASU 2013-12

ASU 2014-02

ASU 2014-03

ASU 2014-07

Always Accretive…

Private Company Council

The Private Company Council (PCC) has two principal responsibilities:

The PCC and the FASB, Have mutually agreed on a set of criteria to decide whether and when alternatives within

U.S. GAAP

Are warranted for private companies.

Based on those criteria, PCC will review and propose alternatives within U.S. GAAP

To address the needs of users of private company FS’s.

The PCC also serves as The primary advisory body to the FASB on the appropriate treatment for private

companies,

For items under active consideration on the FASB’s technical agenda.

Always Accretive…

Alumni & Friends Tailgate - A&A Playbook

ASU 2013-12

Definition of a Public Business Entity

December 2013

Always Accretive…

ASU 2013–12 Public Business Entity

The primary purposes of this update are to:

Amend the Master Glossary of the FASB Accounting Standards Codification To include one definition of public business entity for future use in U.S. GAAP

That definition will be used By the Board,

The Private Company Council (PCC),

And the Emerging Issues Task Force (EITF)

In specifying the scope of future financial accounting and reporting guidance.

Minimize diversity in practice as to what constitutes a non-public entity and a public entity.

Always Accretive…

ASU 2013–12 Public Business Entity

Definition of a Public Business Entity The amendment specifies that:

An entity that is required by the SEC to file or furnish financial statements with the SEC, or does file or furnish financial statements with the SEC, is considered a public business entity.

A consolidated subsidiary of a public company Is not considered a public business entity for purposes of its standalone financial

statements

Other than those included in an SEC filing by its parent

Or by other registrants or those that are issuers and are required to file or furnish financial statements with the SEC.

Always Accretive…

ASU 2013–12 Public Business Entity

Definition of a Public Business Entity The amendment specifies that:

A business entity that has securities that are not subject to contractual restrictions on transfer and that is by law, contract or regulation required to prepare U.S. GAAP financial statements (including footnotes) and make them publicly available on a periodic basis is considered a public business entity.

All Non-profits (NFPs) are excluded from definition of public business entity.

Employee benefit plans are excluded from the definition of public business entities.

Always Accretive…

ASU 2013 – 12 Public Business Entity

Effective Date: There was no actual effective date for the amendment in this Update.

However, the term public business entity was used in Accounting Standards Updates No. 2014-01, Intangibles—Goodwill and Other (Topic 350): Accounting for Goodwill, and No. 2014-02, Derivatives and Hedging (Topic 815): Accounting for Certain Receive-Variable, Pay-Fixed Interest Rate Swaps—Simplified Hedge Accounting Approach, which are the first Updates that will use the term public business entity.

Always Accretive…

Alumni & Friends Tailgate - Accounting Playbook

ASU 2014-02

Accounting for Goodwill

January 2014

Always Accretive…

ASU 2014-02 Accounting for Goodwill for Private Companies

Why Is the FASB Issuing This Accounting Standards Update? The Private Company Council (PCC) added this issue to its agenda

In connection with a separate but related issue addressing identifiable intangible assets acquired in a business combination.

Goodwill is a residual asset calculated after recognizing other (tangible and intangible) assets and liabilities acquired in a business combination, Any modifications to the initial recognition and measurement guidance for identifiable

intangible assets would correspondingly

Change the goodwill amount recognized in the business combination.

Accordingly, The PCC decided that it should take such modifications into consideration in determining

how private companies should account for goodwill after a business combination.

Always Accretive…

ASU 2014-02 Accounting for Goodwill for Private Companies

What are the main provisions? The amendments allow

An accounting alternative for the subsequent measurement of goodwill

An entity within the scope of the amendments that elects the accounting alternative

Should amortize goodwill on a straight-line basis over 10 years, or less than 10 years if the entity demonstrates that another useful life is more appropriate.

The accounting alternative applies to all existing goodwill and subsequently acquired goodwill.

An entity that elects the accounting alternative is further required To make an accounting policy election to test goodwill for impairment

At either the entity level or the reporting unit level.

Always Accretive…

ASU 2014-02 Accounting for Goodwill for Private Companies

What are the main provisions? Goodwill should be tested for impairment when a triggering event occurs

Indicates that the fair value of an entity may be below its carrying amount.

When a triggering event occurs, An entity has the option to first assess qualitative factors to determine whether the

quantitative impairment test is necessary.

If that qualitative assessment indicates that it is more likely than not that goodwill is impaired,

The entity must perform the quantitative test to compare the entity’s fair value with its carrying amount, including goodwill.

If the qualitative assessment indicates that it is not more likely than not that goodwill is impaired, further testing is unnecessary.

Always Accretive…

ASU 2014-02 Accounting for Goodwill for Private Companies

Effective Dates:

The accounting alternative should be applied prospectively.

Effective for, Goodwill existing as of the beginning of the period of adoption

And new goodwill recognized in annual periods beginning after December 15, 2014,

and interim periods within annual periods beginning after December 15, 2015.

Early application is permitted, including application to any period for which the entity’s annual or interim financial

statements have not yet been made available for issuance.

Always Accretive…

Alumni & Friends Tailgate - Accounting Playbook

ASU 2014-03

Accounting for Certain Receive-Variable, Pay-

Fixed Interest Rate Swaps – Simplified Hedge

Accounting Approach

January 2014

Always Accretive…

ASU 2014-03 Simplified Hedge Accounting for Private Companies

Why Is the FASB Issuing This Accounting Standards Update? Feedback received,

Private companies often find it difficult to obtain fixed-rate borrowing.

Therefore, some private companies enter into a receive-variable, pay-fixed interest rate swap to economically convert their variable-rate borrowing into a fixed-rate borrowing.

Under U.S. GAAP, a swap is a derivative instrument.

GAAP requires that an entity recognize all interest rate swaps on its balance sheet as either assets or liabilities and measure them at fair value.

To mitigate income statement volatility of recording a swap’s change in fair value, GAAP permits an entity to elect hedge accounting if certain requirements under that

Topic are met.

Always Accretive…

ASU 2014-03 Simplified Hedge Accounting for Private Companies

Why Is the FASB Issuing This Accounting Standards Update?

The objective of the amendments is to

Address the concerns of private company stakeholders

By providing an additional hedge accounting alternative

For certain types of swaps that are entered into by a private company

For the purpose of economically converting a variable-rate borrowing into a fixed-rate borrowing.

This hedge accounting alternative acts as A practical expedient to qualify for cash flow hedge accounting

If certain conditions are met.

Always Accretive…

ASU 2014-03 Simplified Hedge Accounting for Private Companies

What are the main provisions? The amendments in this Update allow

The use of the simplified hedge accounting approach

To account for swaps that are entered into for the purpose of

Economically converting a variable-rate borrowing into a fixed-rate borrowing.

Under this approach, The income statement charge for interest expense

Will be similar to the amount that would result if the entity had directly entered into a fixed-rate borrowing

Instead of a variable-rate borrowing and a receive-variable, pay-fixed interest rate swap.

Documentation required to qualify as a hedge must be completed by the date the financials are available to be issued.

Always Accretive…

ASU 2014-03 Simplified Hedge Accounting for Private Companies

Effective Dates:

For annual periods beginning after December 15, 2014, and interim periods within annual periods beginning after December 15, 2015, with early adoption permitted.

Always Accretive…

Alumni & Friends Tailgate - A&A Playbook

ASU 2014-07

Applying Variable Interest Entities Guidance to

Common Control Leasing Arrangements

March 2014

Always Accretive…

Alternative VIE Guidance for Common Control Leasing Arrangements

Why Is the FASB Issuing This Accounting Standards Update?

Feedback received from private company stakeholders

Indicated that the benefits of applying variable interest entities (VIE) guidance to a lessor entity under common control do not justify the related costs.

Because the Private Company Decision-Making Framework focuses on User-relevance and cost-benefit considerations for private companies,

The PCC decided that the concerns expressed about the cost and complexity of applying VIE guidance

And the lack of relevance to users when consolidating lessor entities under common control

Indicated that a change to VIE guidance should be explored.

Always Accretive…

Alternative VIE Guidance for Common Control Leasing Arrangements

What are the main provisions?

The amendments permit a private company lessee to elect an alternative

not to apply VIE guidance to a lessor entity if: The lessee and lessor entities are under common control

The lessee has a lease arrangement with the lessor entity

Substantially all of the activities between the lessee and the lessor are related to leasing activities

If the lessee explicitly guarantees or provides collateral for any obligation of the lessor entity related to the asset leased by the private company, then the principal amount of the obligation at inception of such guarantee or collateral arrangement does not exceed the value of the asset leased by the private company from the lessor entity

Always Accretive…

Alternative VIE Guidance for Common Control Leasing Arrangements

What are the main provisions? Election of alternative is an accounting policy decision that must be

applied to all current and future lessor entities under common control

Under the alternative, lessee would not be required to provide the VIE disclosures about the lessor entity

Lessee company is required to disclose: The amount and key terms of liabilities recognized by the lessor that expose the lessee to

providing financial support

Qualitative description of circumstances not recognized in the financial statements of the lessor that expose the lessee to providing financial support

Always Accretive…

Alternative VIE Guidance for Common Control Leasing Arrangements

Consolidation, effective date & transition:

If any of the conditions to use the alternative cease to be met,

An entity needs to consider if it must consolidate under VIE requirements.

Effective Date; Periods beginning after 12/15/14; Early adoption permitted for any unissued statements

Transition Adoption of a new accounting principle

Retrospective application to all periods presented

Deconsolidation may result in a cumulative effect adjustment to retained earnings

Always Accretive…

Alumni & Friends Tailgate - A&A Playbook

FASB Launches Initiative to Simplify Accounting

Standards

Always Accretive…

FASB Simplification Initiative

What is the Simplification Initiative?

The FASB has launched a initiative to Make narrow-scope simplifications and improvements to accounting

standards

Through a series of short-term projects.

The projects included in the initiative are Intended to improve or maintain the usefulness of the information

reported to investors

While reducing costs and complexity in financial reporting.

Always Accretive…

FASB Simplification Initiative

The FASB added the following projects to the agenda:

Simplifying the Measure of Inventory: The proposed update issued for comment in July 2014

Seeks to address concerns about the complexity of measuring inventory

By requiring organizations to estimate only net realizable value.

Extraordinary Items: The proposed update issued for comment in July of 2014

Seeks to simplify income statement presentation

By eliminating the notion of separately presenting extraordinary items.

Always Accretive…

FASB Simplification Initiative

The FASB added the following projects to the agenda:

Presentation of debt issuance costs: The project is expected to simplify the accounting by aligning the

presentation of debt discount or premium and issuance costs.

Measurement date of defined benefit pension plan assets: The project is expected to reduce cost

By aligning the measurement date of defined benefit pension plan assets

With the date that valuation information is provided by third-party service providers.

Always Accretive…

FASB Simplification Initiative

The FASB added the following projects to the agenda:

Balance sheet classification of debt: The project is expected to reduce cost and complexity

By replacing the existing fact-pattern specific guidance

With a principle to classify debt as current or noncurrent

Based on the contractual terms of a debt arrangement and an organization’s current compliance with debt covenants.

Always Accretive…

FASB Simplification Initiative

Accounting for income taxes: The project is expected to simplify accounting for income taxes by:

Eliminating the requirement for organizations that present a classified statement of financial position to classify deferred tax assets and liabilities as current and noncurrent, and instead require that they classify all deferred tax assets and liabilities as noncurrent.

Eliminating the prohibition on the recognition of income taxes for transfers of assets from one jurisdiction to another.

Stock-based Compensation: The project is intended to make some relatively narrow simplifications and improvements

to accounting for stock compensation to employees.

Always Accretive…

FASB Simplification Initiative

Other projects in which the FASB is looking to simplify accounting standards and reduce cost and complexity in financial reporting include:

Clarifying Certain Existing Principles on Statement of Cash Flows

Accounting for Financial Instruments – Hedging

Liabilities & Equity – Short-term Improvements

Always Accretive…

FASB Simplification Initiative

Taking credit – Recently completed FASB projects that, while not part of the Simplification Initiative, did simplify some elements of GAAP:

Discontinued Operations

Development Stage Entities

Always Accretive…

Alumni & Friends Tailgate - A&A Playbook

U.S. & International

Convergence

Always Accretive…

International Convergence

During the past ten years, the FASB and IASB collaborated through joint projects to develop common standards. The FASB has issued those standards as U.S. GAAP and

The IASB has issued them as IFRS.

Over time, the two sets of standards are expected to both Improve in quality

And become increasingly similar, if not identical.

The four remaining joint projects are: revenue recognition;

financial instruments;

leases;

and insurance.

Always Accretive…

International Convergence

Revenue Recognition

Revenue is an important indicator for users of financial reports

In assessing a company’s performance and prospects

However, revenue recognition guidance differs in GAAP and IFRS

And many believe both are in need of improvement

To that end, the Boards embarked on a joint project aimed at establishing the principles to report useful information to users of financial statements about the nature, timing, and uncertainty of revenue from contracts with customers

On May 28, 2014, the FASB and the IASB issued converged guidance on recognizing revenue in contracts with customers

The new guidance is a major achievement in the Boards’ joint efforts to improve this important area of financial reporting

Always Accretive…

International Convergence

Leases

Leases are an important source of financing for many companies that

lease assets.

However, many lease transactions currently are recognized off-balance sheet.

The objective of the leases project is to increase transparency and comparability among organizations that lease assets by recognizing assets and liabilities that arise from lease transactions on a lessee’s balance sheet.

The Boards issued for public comment a revised Exposure Draft on Leases in May 2013.

Always Accretive…

International Convergence

Financial Instruments

The objective of the joint project on accounting for financial instruments

provide financial statement users with a more timely and representative depiction of a company, institution, or not-for-profit organization’s involvement in financial instruments,

while reducing the complexity in accounting for those instruments.

The Boards are conducting this project in three phases, and both have issued proposed

standards on the first two phases: accounting for credit losses

and recognition and measurement of financial instruments.

Both Boards have proposed expected credit loss models to replace the current incurred loss model, but their proposed models differ on when those losses should be recognized. Following the conclusion of the comment period on credit losses, the Boards will determine if there is common ground in developing a converged standard. The third phase of the accounting for financial instruments project looks at hedging.

Always Accretive…

International Convergence

Insurance Existing U.S. GAAP comprehensively addresses insurance accounting.

However, IFRS currently lacks specific accounting requirements for insurance contracts.

The Boards undertook the Insurance Contracts project to develop common, high-quality guidance that will address

recognition, measurement, presentation, and disclosure requirements

for insurance contracts (including reinsurance),

even if the contracts are not issued by an insurance company.

In general, the Boards are developing a model that would reflect current estimates of the amount necessary to fulfill an insurance obligation. However, they have not reached consistent conclusions about some elements of the model.

Always Accretive…

Alumni & Friends Tailgate - A&A Playbook

Q&A

University of Georgia Research: Why It Matters

David Lee UGA Vice President for Research

December 3, 2014

Porter, Keadle, Moore LLC – December 3, 2014 2

University Research – Why Do It? Promotes understanding of complex issues

for decision makers and citizens

Addresses grand challenges as only

universities can

Keeps the land-grant mission fresh

Provides unique educational opportunities

for students

Fuels America’s discovery pipeline

Promotes technology-based economic

development

Porter, Keadle, Moore LLC – December 3, 2014 3

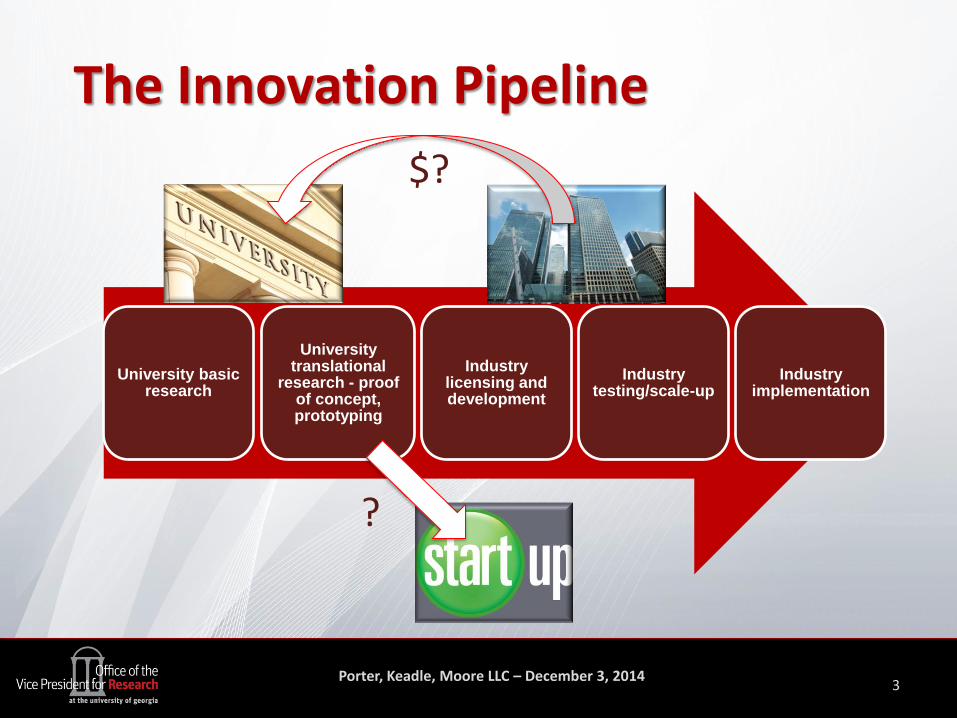

The Innovation Pipeline

University basic research

University translational

research - proof of concept, prototyping

Industry licensing and development

Industry testing/scale-up

Industry implementation

$?

?

Porter, Keadle, Moore LLC – December 3, 2014 4

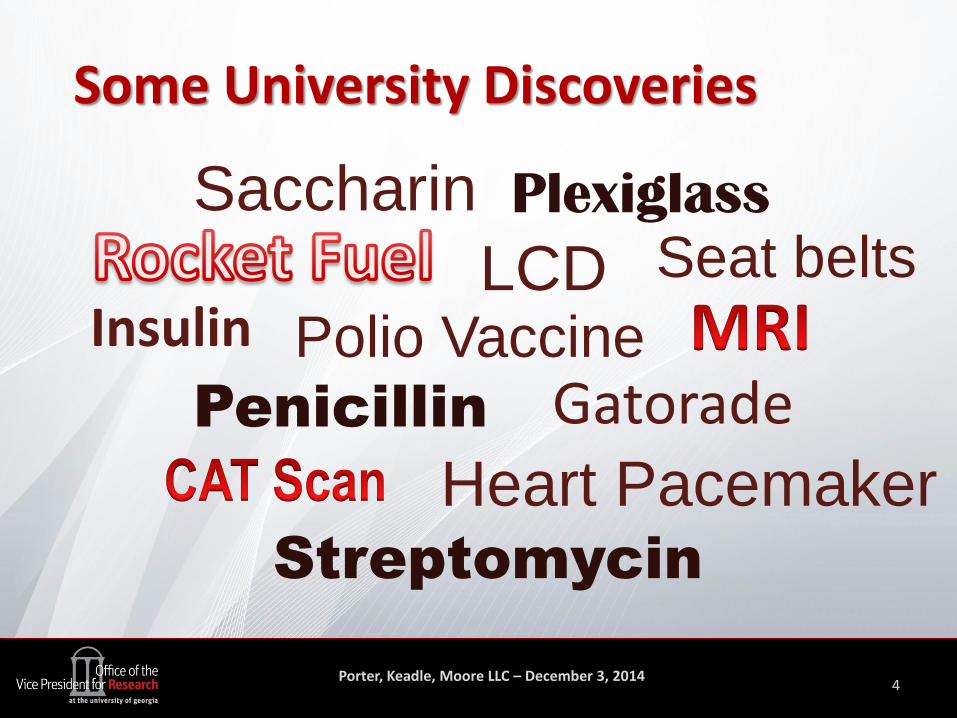

Some University Discoveries

Insulin

Saccharin

LCD

Heart Pacemaker

Polio Vaccine

Seat belts

Penicillin Gatorade

Streptomycin

Plexiglass

Porter, Keadle, Moore LLC – December 3, 2014 5

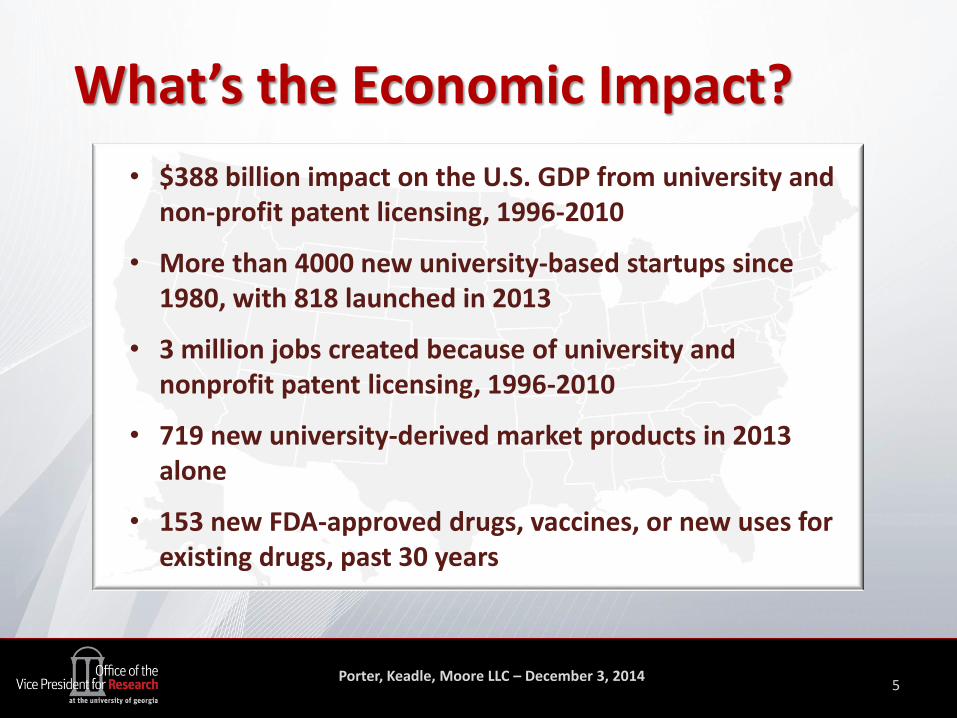

What’s the Economic Impact?

• $388 billion impact on the U.S. GDP from university and non-profit patent licensing, 1996-2010

• More than 4000 new university-based startups since 1980, with 818 launched in 2013

• 3 million jobs created because of university and nonprofit patent licensing, 1996-2010

• 719 new university-derived market products in 2013 alone

• 153 new FDA-approved drugs, vaccines, or new uses for existing drugs, past 30 years

Porter, Keadle, Moore LLC – December 3, 2014 6

Technology-based Development

Porter, Keadle, Moore LLC – December 3, 2014 7

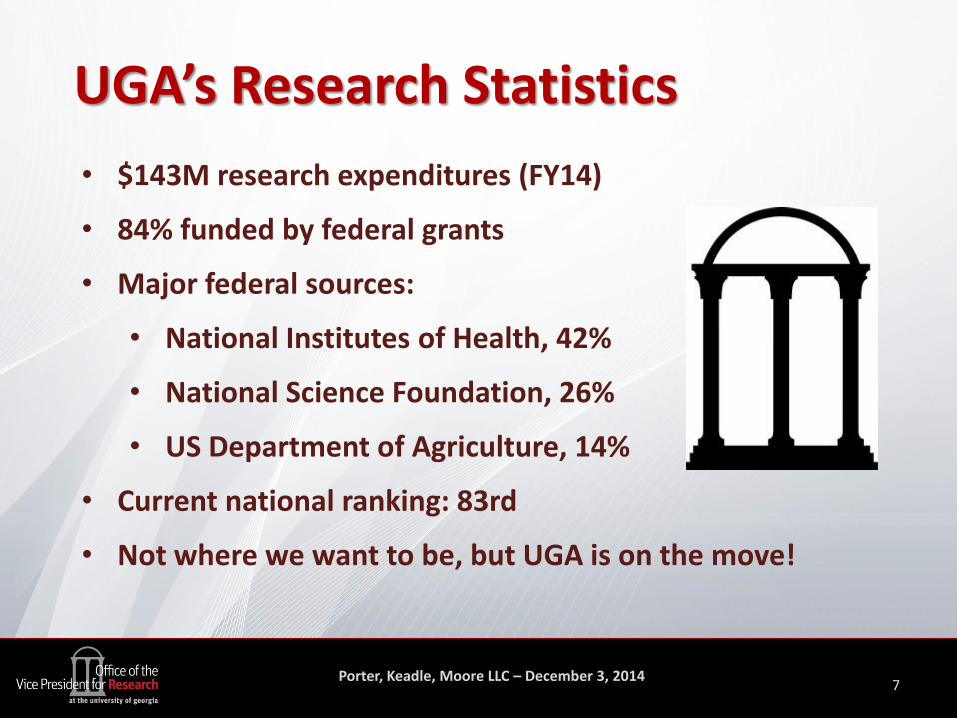

UGA’s Research Statistics

• $143M research expenditures (FY14)

• 84% funded by federal grants

• Major federal sources:

• National Institutes of Health, 42%

• National Science Foundation, 26%

• US Department of Agriculture, 14%

• Current national ranking: 83rd

• Not where we want to be, but UGA is on the move!

Porter, Keadle, Moore LLC – December 3, 2014 8

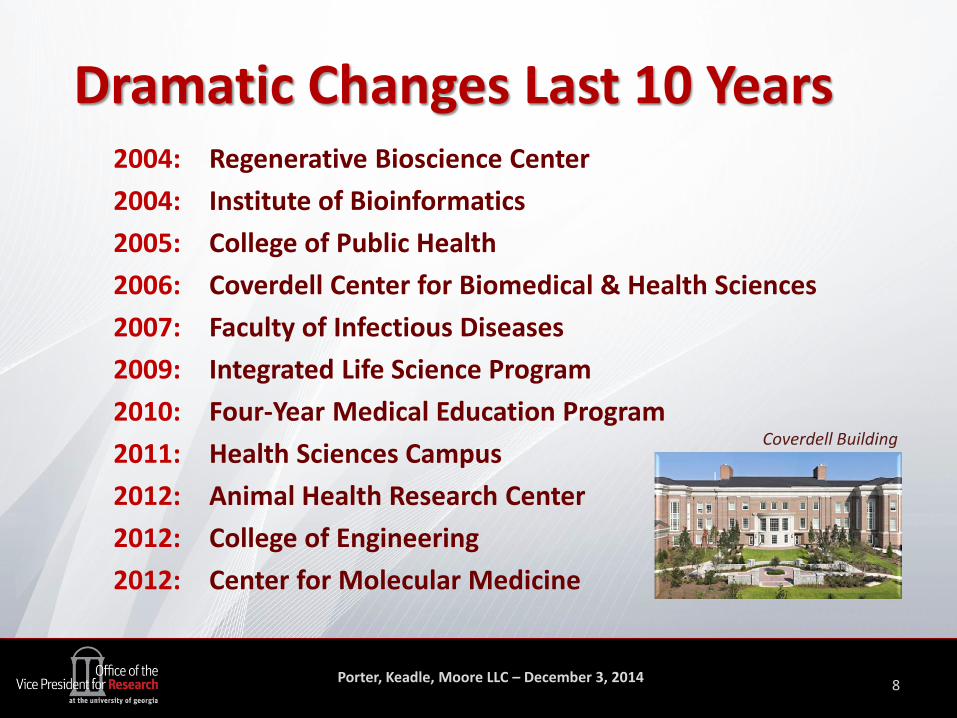

2004: Regenerative Bioscience Center

2004: Institute of Bioinformatics

2005: College of Public Health

2006: Coverdell Center for Biomedical & Health Sciences

2007: Faculty of Infectious Diseases

2009: Integrated Life Science Program

2010: Four-Year Medical Education Program

2011: Health Sciences Campus

2012: Animal Health Research Center

2012: College of Engineering

2012: Center for Molecular Medicine

Dramatic Changes Last 10 Years

Coverdell Building

Porter, Keadle, Moore LLC – December 3, 2014 9

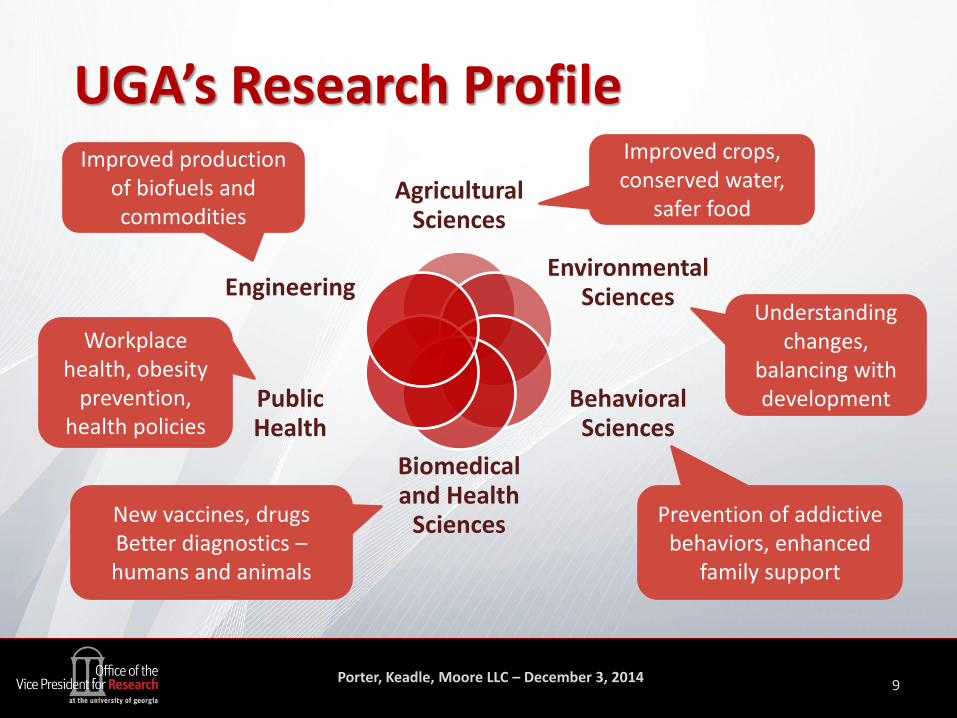

UGA’s Research Profile

Agricultural Sciences

Environmental Sciences

Behavioral Sciences

Biomedical and Health

Sciences

Public Health

Engineering

Improved crops, conserved water,

safer food

New vaccines, drugs Better diagnostics – humans and animals

Understanding changes,

balancing with development

Improved production of biofuels and commodities

Prevention of addictive behaviors, enhanced

family support

Workplace health, obesity

prevention, health policies

Porter, Keadle, Moore LLC – December 3, 2014 10

• UGA scientists receive $30+ million over 10 years to help lead a federal bioenergy initiative to make biofuels cost-effective

• Professor Jessie Kissinger receives $13 million over 15 years to develop a comprehensive gene database for human infectious pathogens, as a step towards new vaccines and drugs

• An all-Georgia consortium (UGA, Emory, GA Tech, CDC, Yerkes Primate Center) receives $20 million NIH contract to better understand malaria infections – how to crack this disease!

• Professor Ralph Tripp and other UGA scientists participate in NIH’s $33 million Regional Center of Excellence for Influenza Research & Surveillance based at Emory

Some Recent Major Developments

Porter, Keadle, Moore LLC – December 3, 2014 11

• Professor Dan Colley leads $34 million effort by the Gates Foundation to reduce the impact of schistosomiasis worldwide

• Professor Geert-Jan Boons receives $7.4 million NIH grant to better understand the critical role of sugar chains in life, from plants to humans

• Professor Gene Brody receives two NIH awards totaling $13 million to understand how genetic predisposition combines with environment to forecast poor behavioral outcomes among youth and to improve intervention programs

• UGA scientists receive $6 million from the NSF to improve corn varieties for drought and disease resistance

Other Major Developments

Porter, Keadle, Moore LLC – December 3, 2014 12

• We need more successes like these to “move the needle”, and we need to support the faculty responsible for these successes

• Note how prominent UGA’s biomedical research has become, though we see successes in other areas as well

• Don’t let anyone tell you that Georgia’s research universities aren’t collaborating!

Thoughts on Major Developments

Porter, Keadle, Moore LLC – December 3, 2014 13

Multifaceted –

Aggressively moving UGA discoveries into the marketplace via licensing to industry

Supporting new business startups

Collaborating with industry

Doing our part for advanced workforce development

Ensuring access to UGA assets for industry and economic development

Research to Economic Development

Porter, Keadle, Moore LLC – December 3, 2014 14

Moving inventions from the lab/field to the marketplace is a high priority –

• 525+ products on the market, with 28 added in 2014

• Over 1200 active IP licenses, 25% with GA companies

• 500+ U.S. and foreign patents, with licenses worldwide

• “Top 5” university for licenses and options (7th consecutive year)

• 132 companies started based on UGA research, with 904 jobs created, a $100 million economic impact, 300+ student interns

Licensing of UGA Discoveries

Porter, Keadle, Moore LLC – December 3, 2014

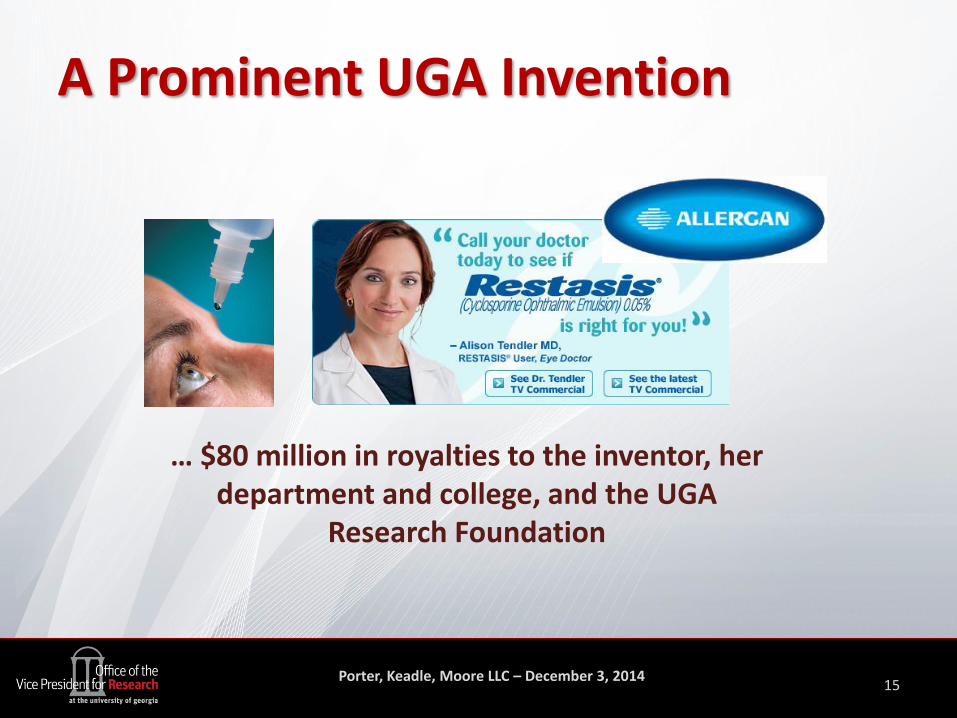

A Prominent UGA Invention

15

… $80 million in royalties to the inventor, her department and college, and the UGA

Research Foundation

Porter, Keadle, Moore LLC – December 3, 2014

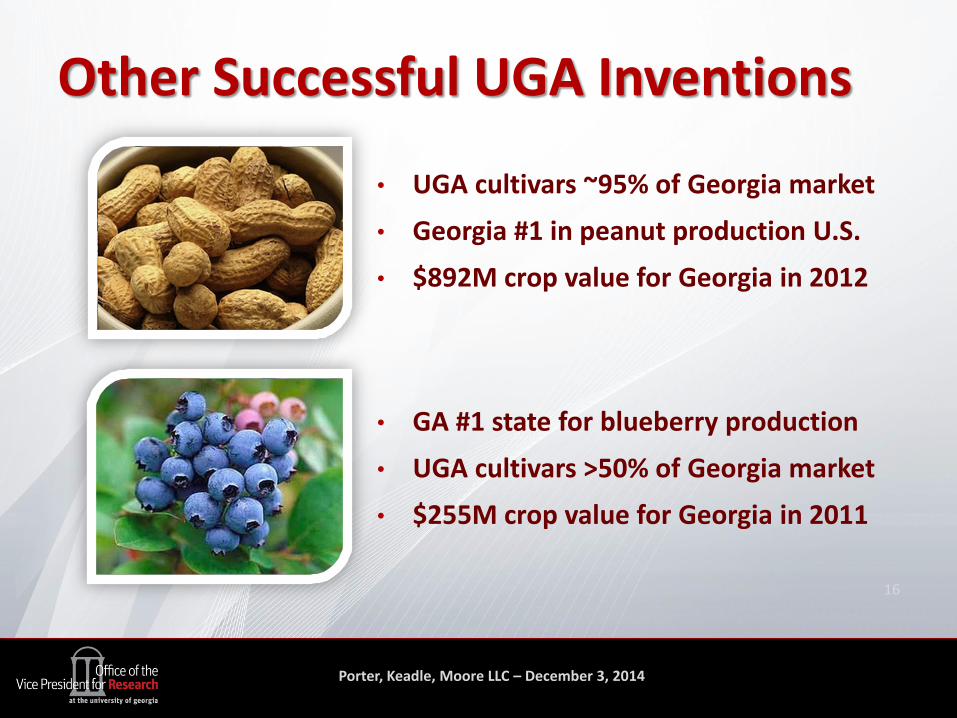

Other Successful UGA Inventions

16

• GA #1 state for blueberry production

• UGA cultivars >50% of Georgia market

• $255M crop value for Georgia in 2011

• UGA cultivars ~95% of Georgia market

• Georgia #1 in peanut production U.S.

• $892M crop value for Georgia in 2012

Porter, Keadle, Moore LLC – December 3, 2014

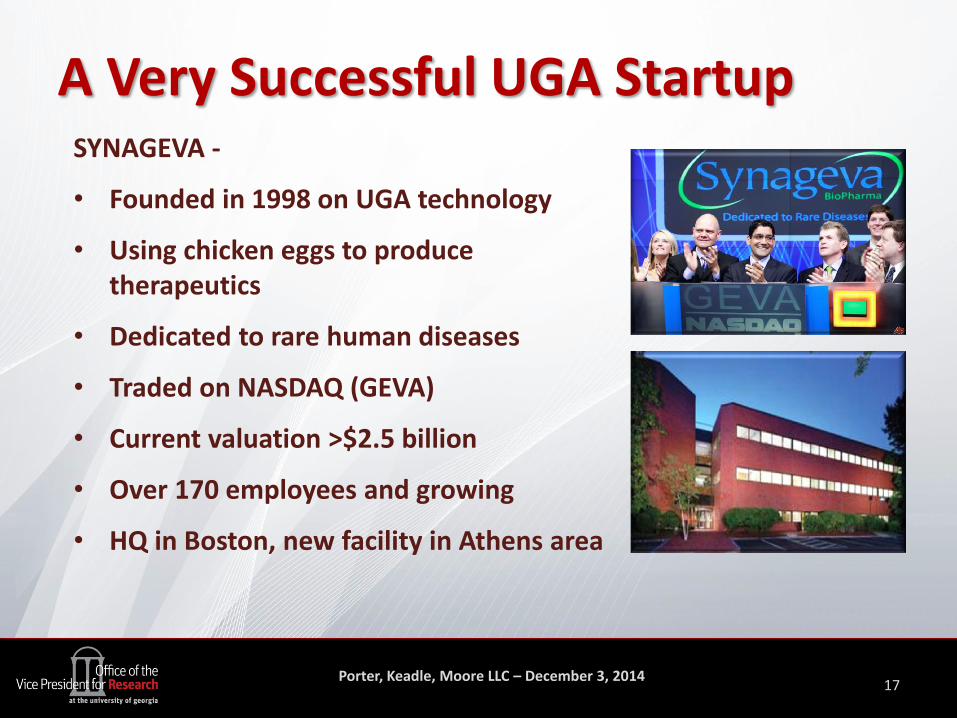

A Very Successful UGA Startup

17

SYNAGEVA -

• Founded in 1998 on UGA technology

• Using chicken eggs to produce therapeutics

• Dedicated to rare human diseases

• Traded on NASDAQ (GEVA)

• Current valuation >$2.5 billion

• Over 170 employees and growing

• HQ in Boston, new facility in Athens area

Porter, Keadle, Moore LLC – December 3, 2014

Last Thoughts

18

• Discoveries at America’s universities fuel the innovation pipeline and ignite the imaginations of our future advanced workforce

• Top-flight research universities are key to Georgia’s long-term success in the global innovation economy

• Partnerships – among our universities, and with industry and government are key to success

• So is continuing to strengthen and broaden our research base, including at UGA

• Research universities like UGA must ensure robust transfer of new technology to the marketplace and actively engage in economic development

Porter, Keadle, Moore LLC – December 3, 2014

Economic Development Office

19

Sean McMillan

Porter, Keadle, Moore LLC – December 3, 2014 20

These Are Exciting Times At UGA!

Go Research Dogs!

AUDIT TAX SYSTEMS ADVISORY

Always Accretive. . . …

Terry Ammons Tim Davis

Systems Partner Systems Senior

Always Accretive…

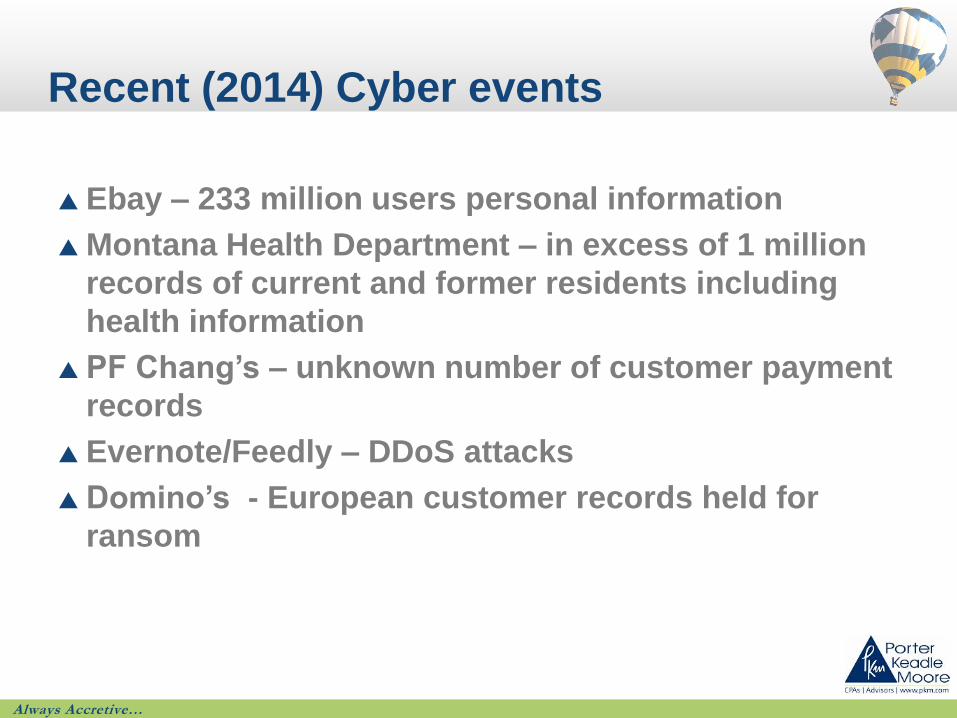

Recent (2014) Cyber events

Ebay – 233 million users personal information

Montana Health Department – in excess of 1 million

records of current and former residents including

health information

PF Chang’s – unknown number of customer payment

records

Evernote/Feedly – DDoS attacks

Domino’s - European customer records held for

ransom

Always Accretive…

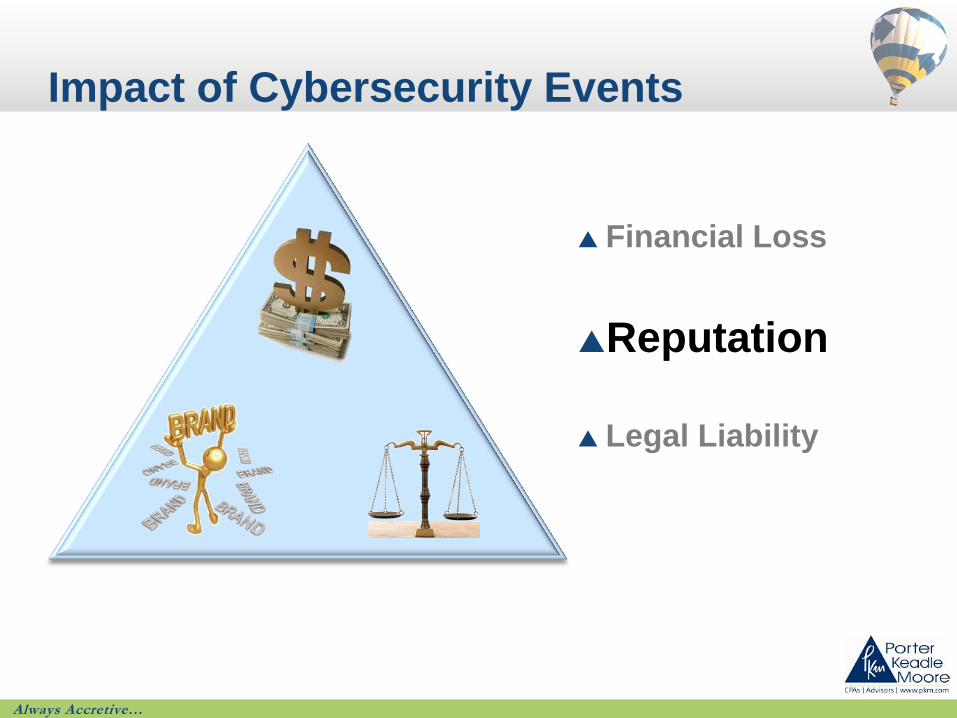

Impact of Cybersecurity Events

Financial Loss

Reputation

Legal Liability

Always Accretive…

Bank Regulators Pushing Back

OCC Thomas J. Curry – at 10th Annual Community

Bankers Symposium

- “Financial institutions are often on the hook to compensate customers for

fraudulent charges, and replace credit and debit cards and monitor

account activity for fraud at significant cost.”

- Recent incidents highlight the need for improved cyber security “but they

also demonstrate why we to level the playing field between FIs and

merchants. The same expectations for security of customer information

and customer notification when breaches occur should apply to all

institutions. And when breaches occur in merchant systems, it only

seems fair to me that they should be responsible for some of the

expenses that result.”

Always Accretive…

Impact – Federal Government

Executive Order – Improving Critical Infrastructure

Cybersecurity

- One of the most problematic elements of cybersecurity is the

quickly and constantly evolving nature of security risks.

- Current controls in place are inadequate to protect against

cybersecurity attacks on financial infrastructure.

- FI regulators and security officials have expanded their focus from

fraud detection to cybersecurity prevention.

Always Accretive…

Impact – Federal Government

Increased Government Involvement – Executive

order – Safeguarding Consumer’ Financial Security*

- Requiring chip and PIN payment technology for all government

related CC payments

- Pushing retailers to adopt more secure technology

- Resources for assisting victims of identity theft

- Easier access to impacts of credit scores

- Push for national Data Breach and Cybersecurity legislation

* - Fact sheet: Safeguarding Consumers Financial Security 10/17/14

Always Accretive…

Impact – Industry Groups/New Technology

FFIEC - Cybersecurity and Critical Infrastructure

Working Group

PCI – Increased focus on more vulnerable

transactions – Card Not Present and ecommerce

NIST – recommendations for Federal Information in

Non federal Information Systems

Retailers – adoption of POS systems that encrypt

transactions from throughout the its lifecycle

Apple Pay

Peer to Peer payment systems – Pay Pal, Google

Wallet

Always Accretive…

Elements of a Cybersecurity Risk

Management Program

Threat intelligence and collaboration – Internal &

External Resources

Incident response and resilience

Third -party service provider and vendor risk

management

Always Accretive…

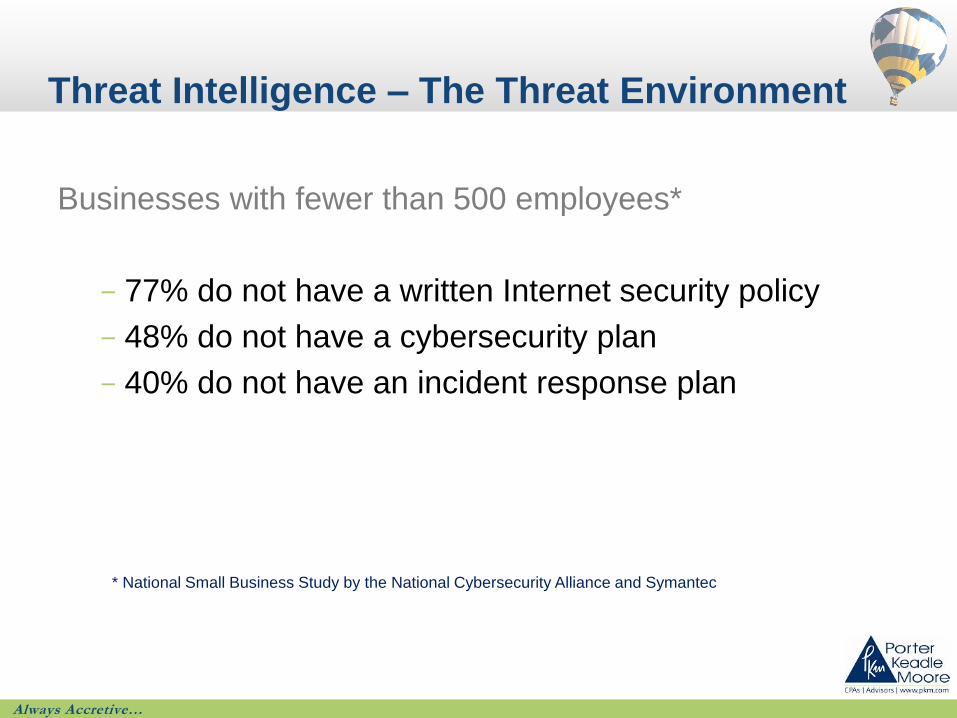

Threat Intelligence – The Threat Environment

Businesses with fewer than 500 employees*

- 77% do not have a written Internet security policy

- 48% do not have a cybersecurity plan

- 40% do not have an incident response plan

* National Small Business Study by the National Cybersecurity Alliance and Symantec

Always Accretive…

Defining Cyber Threat Intelligence

Acquisition and analysis of information to identify,

track and predict cyber capabilities, intentions and

activities that offer courses of actions to enhance

decision making.

Gathering, monitoring, analyzing and sharing

information from multiple sources on cyber threats

and vulnerabilities.

Always Accretive…

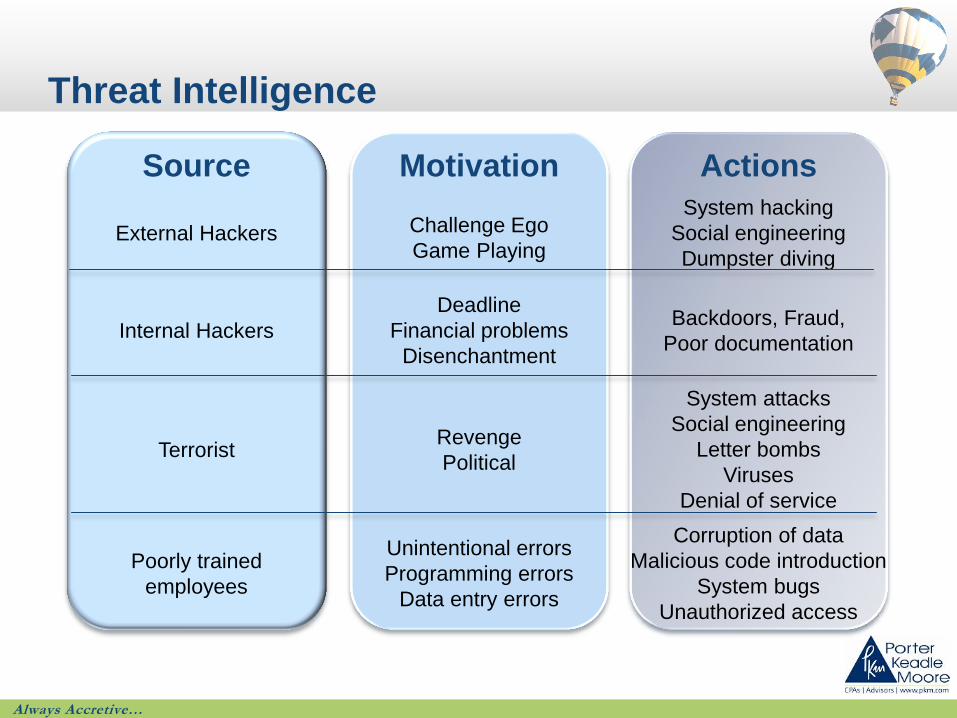

Threat Intelligence

Source Motivation

External Hackers Challenge Ego

Game Playing

System hacking

Social engineering

Dumpster diving

Internal Hackers

Deadline

Financial problems

Disenchantment

Backdoors, Fraud,

Poor documentation

Terrorist Revenge

Political

System attacks

Social engineering

Letter bombs

Viruses

Denial of service

Poorly trained

employees

Unintentional errors

Programming errors

Data entry errors

Corruption of data

Malicious code introduction

System bugs

Unauthorized access

Actions

Always Accretive…

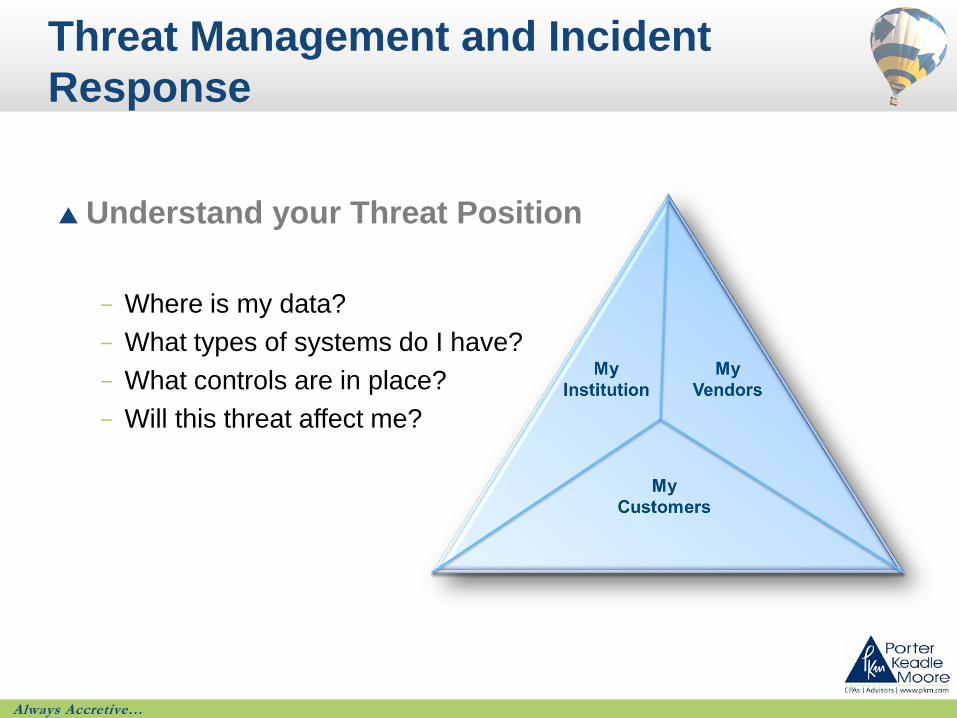

Threat Management and Incident

Response

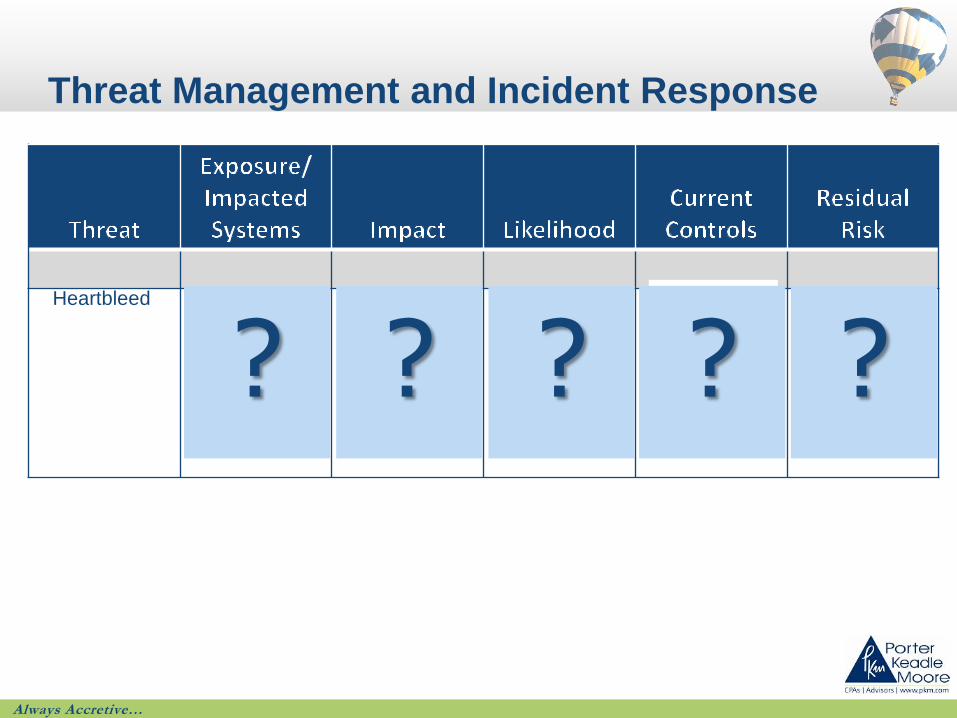

Understand your Threat Position

- Where is my data?

- What types of systems do I have?

- What controls are in place?

- Will this threat affect me?

Always Accretive…

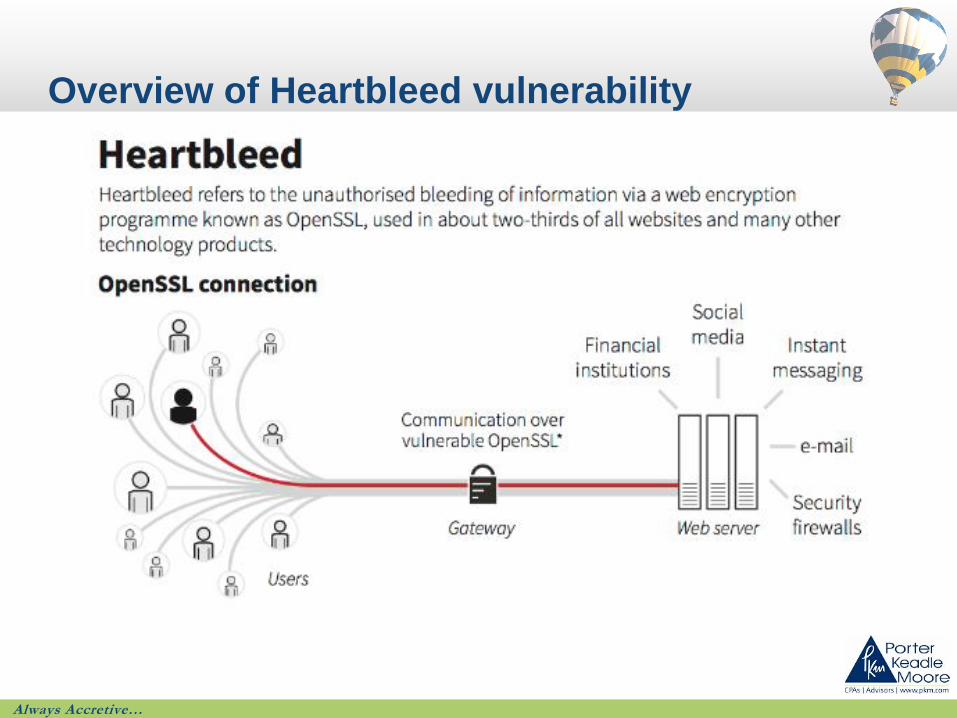

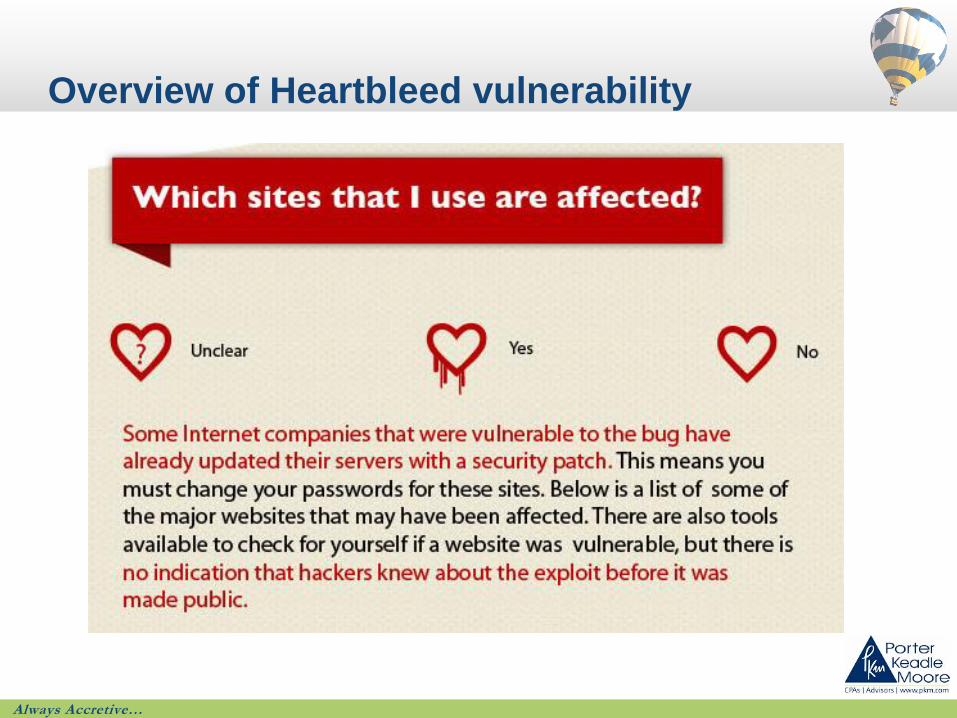

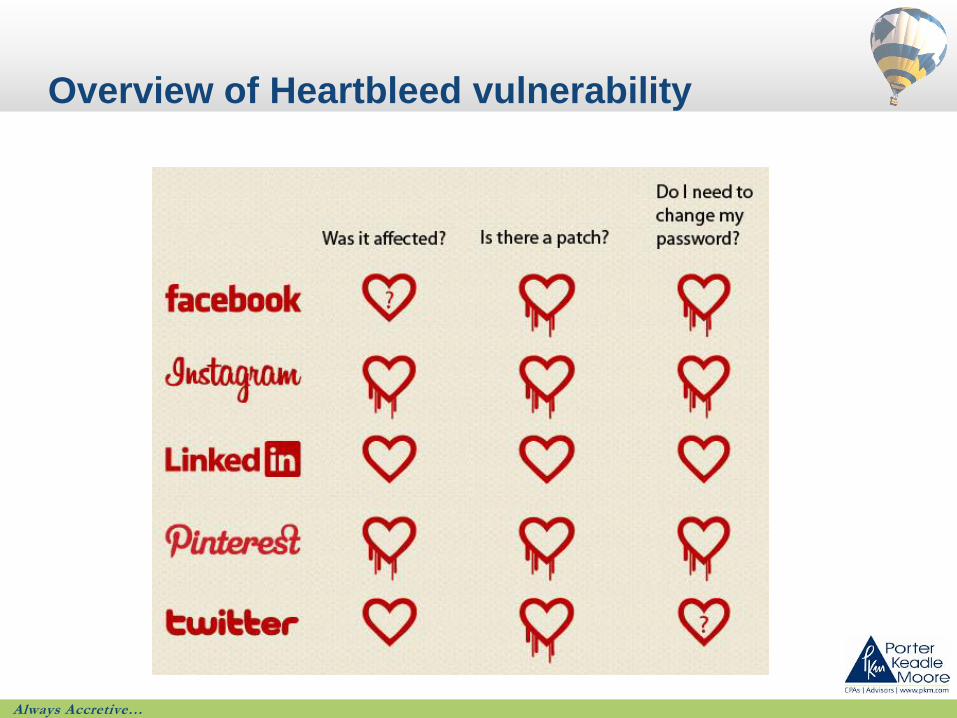

Overview of Heartbleed vulnerability

Always Accretive…

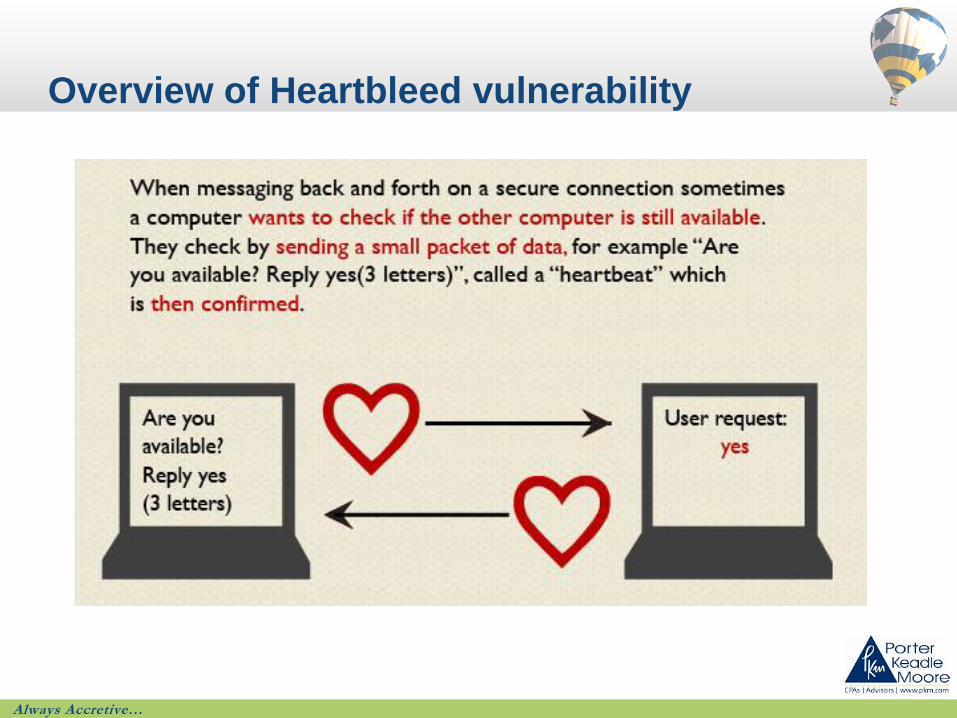

Overview of Heartbleed vulnerability

Always Accretive…

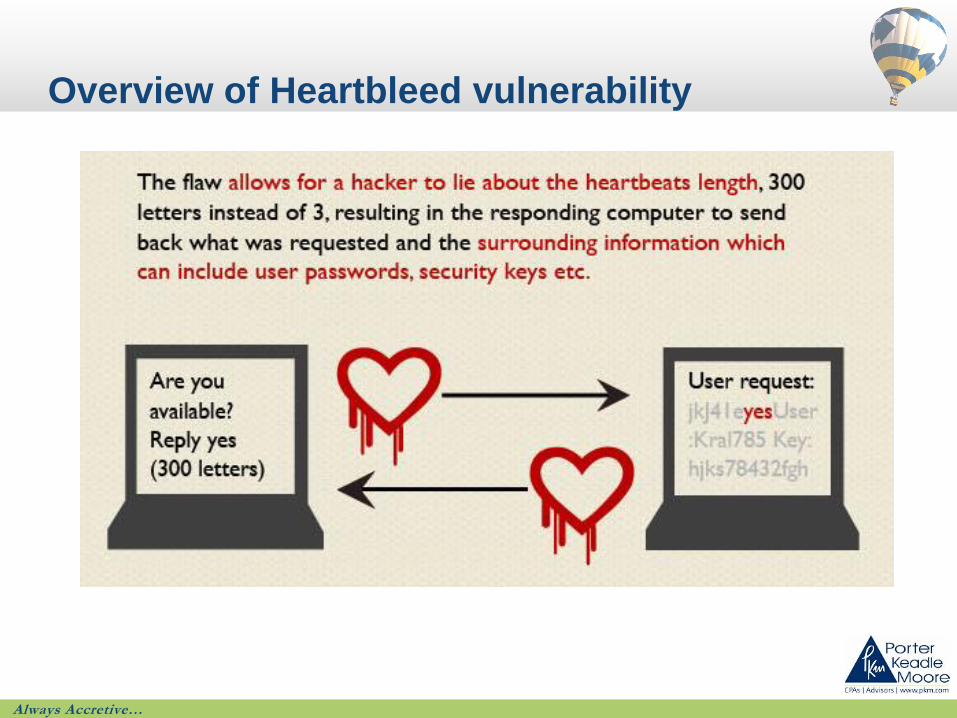

Overview of Heartbleed vulnerability

Always Accretive…

Overview of Heartbleed vulnerability

Always Accretive…

Overview of Heartbleed vulnerability

Always Accretive…

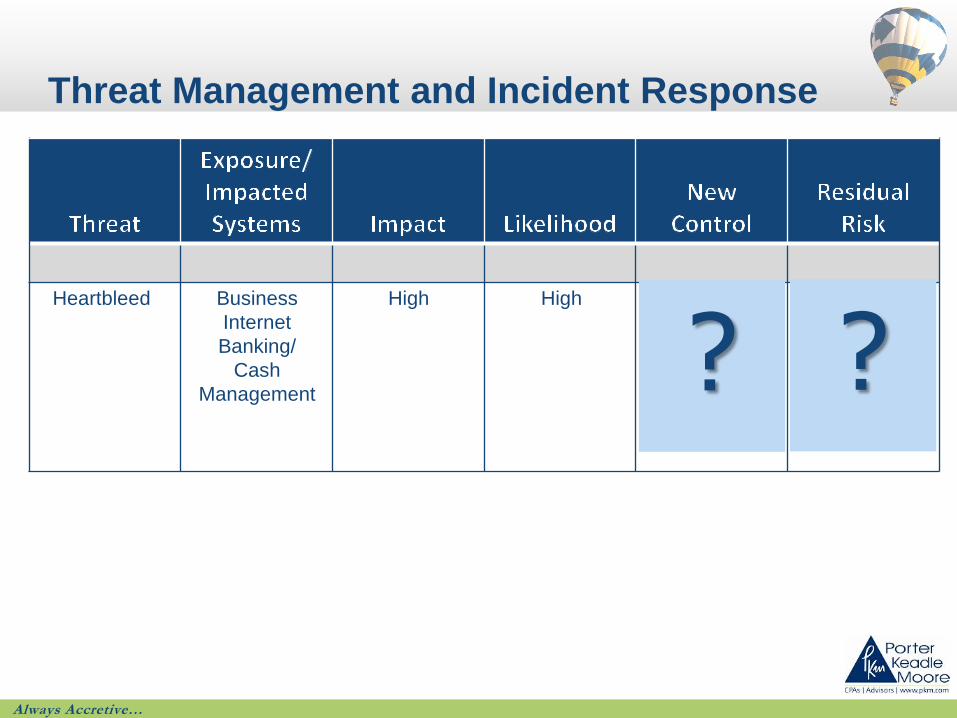

Threat Management and Incident Response

Whether it originates internally or externally, a

cybersecurity incident is a virtual certainty.

Be Prepared:

- Update your incident response program (IRP) to include

cybersecurity events.

- Ensure your IRP contains the following elements:

The incident response team members

A method for classifying the severity of the incident

A response based on severity, to include internal escalation, and

external notification.

Periodic testing and Board reporting

Always Accretive…

Threat Management and Incident Response

Business

Internet

Banking/

Cash

Management

High High High Heartbleed

? ? ? ? User ID’s

and

passwords

Network

hardening

IPS/IDS

User ID’s

and

passwords

Network

hardening

IPS/IDS

?

Always Accretive…

Threat Management and Incident Response

Business

Internet

Banking/

Cash

Management

High High Acceptable Heartbleed Multi factor authentication

? ?

Always Accretive…

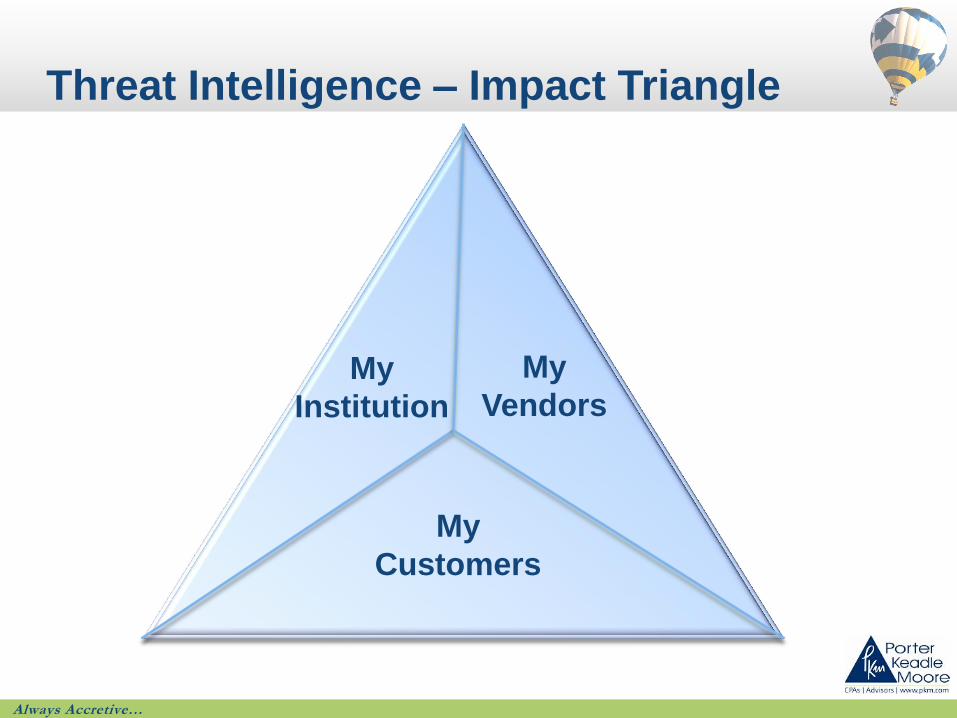

Threat Intelligence – Impact Triangle

My

Institution

My

Vendors

My

Customers

Always Accretive…

Third-party Service Provider and

Vendor Risk Management

Managing cybersecurity relies on managing the risk

originating at third-parties

- Focus on vendors with access to your network, customer data

and/or other sensitive information

Pay particular attention to the following:

- Pre-contract planning and negotiation

- Review of current contracts with critical vendors

- Ongoing monitoring of vendor practices

- Prompt notification of material incidents

- Termination/disengagement with noncompliant vendors

Always Accretive…

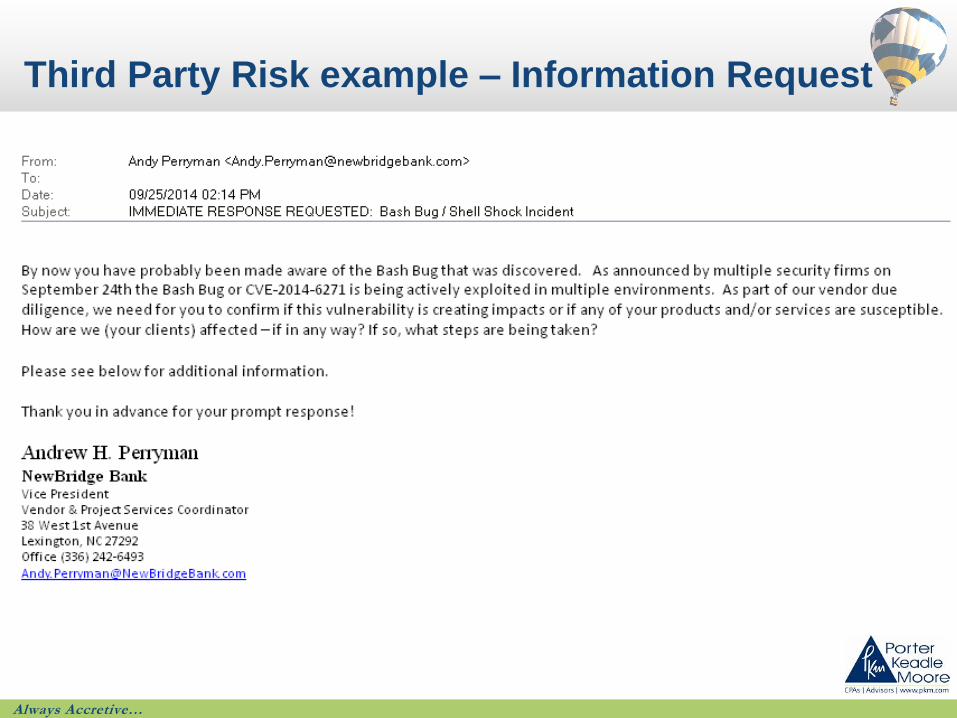

Third Party Risk example – Information Request

Always Accretive…

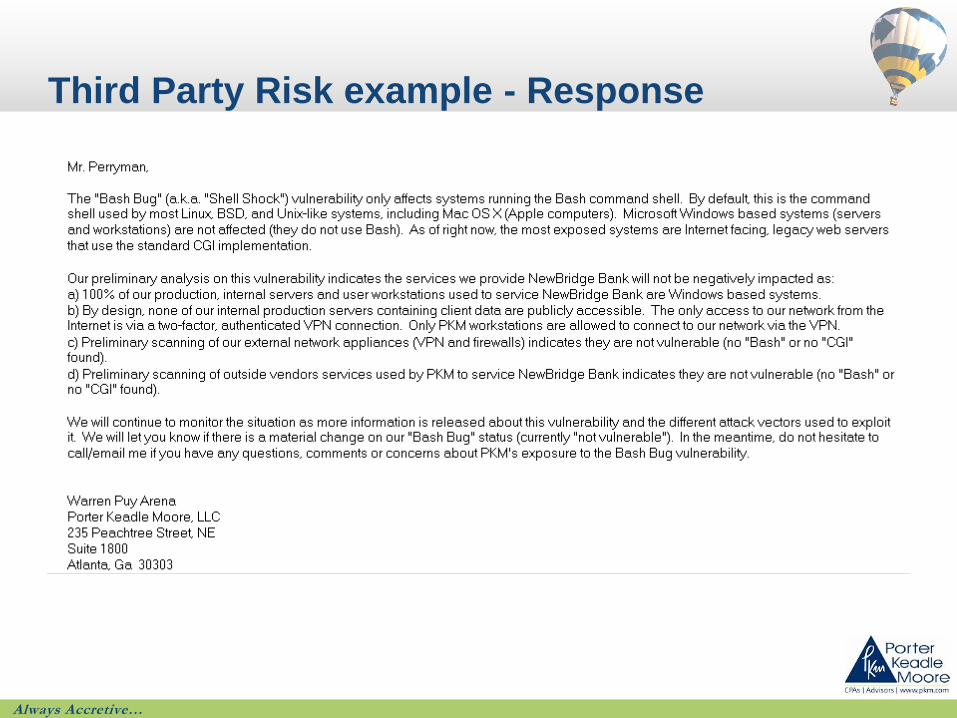

Third Party Risk example - Response

Always Accretive…

Threat Management “Take Aways”

Implement threat intelligence monitoring--Identify and monitor

cybersecurity threats to your organization, your vendors and

your customers.

Threat Intelligence Internal & External Monitoring Tools:

- Financial Services Information Sharing and Analysis Centers (ISACs) -

https://www.fsisac.com/

- U.S. Secret Service Electronic Crimes Task Force (ECTF) -

www.secretservice.gov/ectf.shtml

- FBI InfraGard - www.infragard.org

- NCUA Cybersecurity Resources - www.ncua.gov/Resources/Pages/cyber-

security-resources.aspx

- FDIC Cyber Challenge: A Community Bank Cyber Exercise –

www.fdic.gov/regulations/resources/director/technical/cyber/cyber.html

Always Accretive…

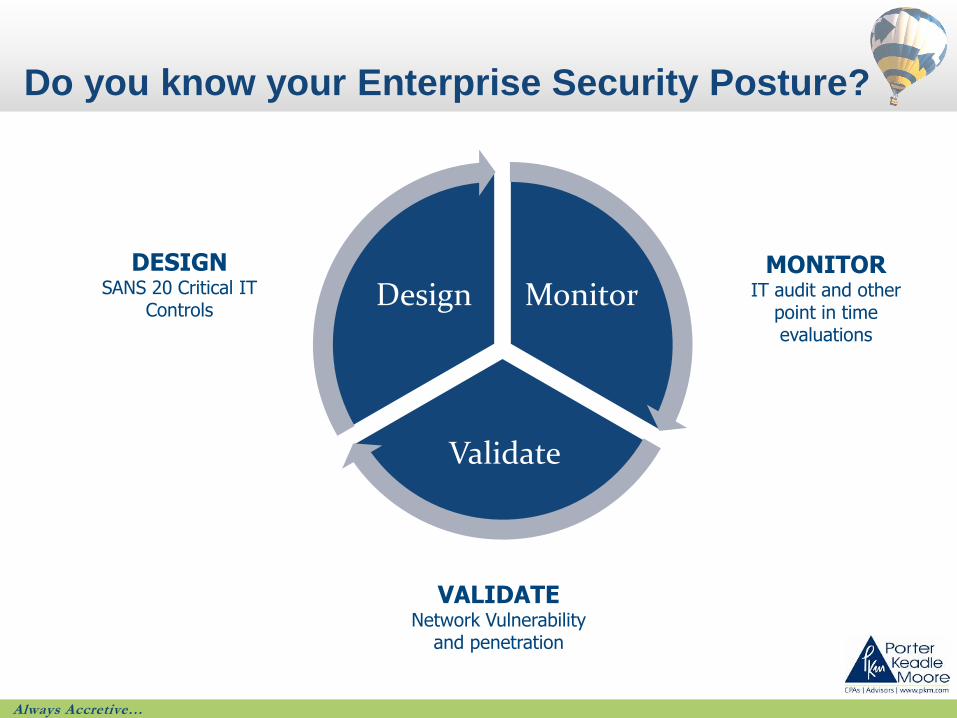

Do you know your Enterprise Security Posture?

Monitor

Validate

Design MONITOR

IT audit and other point in time evaluations

VALIDATE Network Vulnerability

and penetration

DESIGN SANS 20 Critical IT

Controls

Always Accretive…

Questions?

Terry Ammons Systems Partner (404) 420-5679 [email protected]

Timothy Davis Systems Senior (404) 420-5793 [email protected]