Embed Size (px)

Citation preview

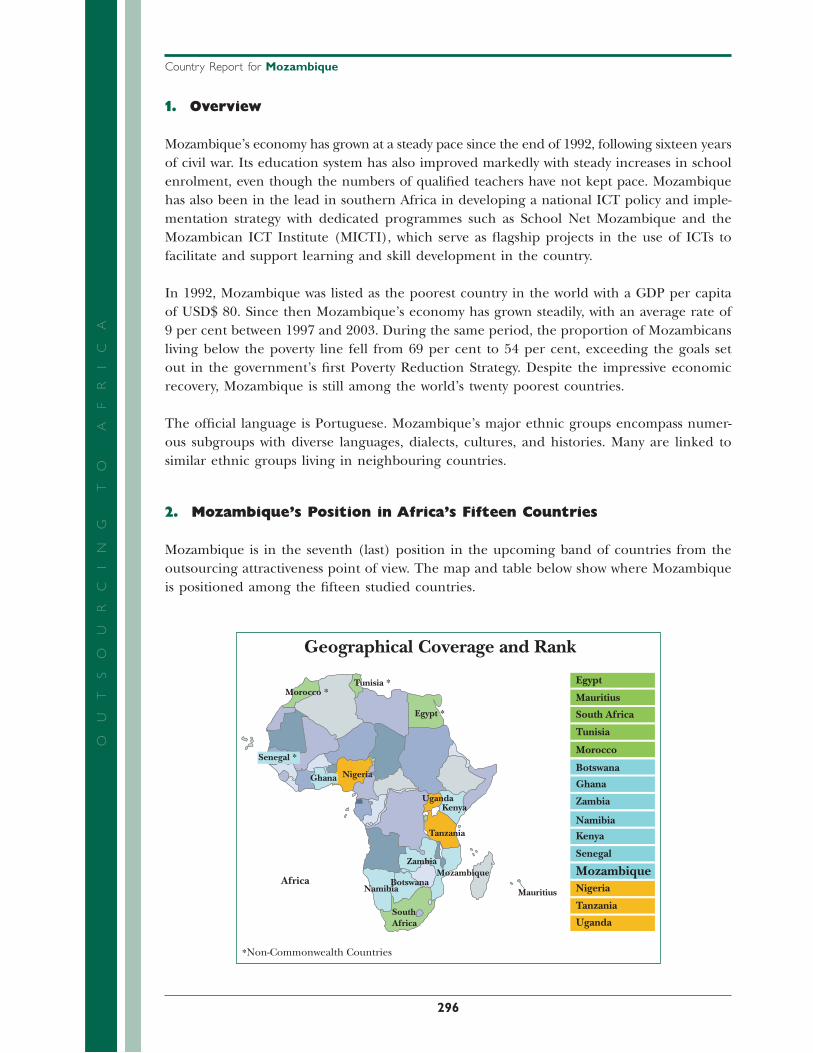

A R e l a t i v e R a n k i n g o f 1 5 C o u n t r y L o c a t i o n sOUTSOURCING TO AFRICA

OU

TS

OU

RC

ING

TO

AF

RIC

A A

Re

lative R

ankin

g of 1

5 C

ou

ntry L

ocatio

ns

OUTSOURCING TO AFRICA

A Relative Ranking of 15 Country Locations

02_Africa_Report09_FR.indd Sec3:i02_Africa_Report09_FR.indd Sec3:i 2/26/09 12:14:04 PM2/26/09 12:14:04 PM

OU

TS

OU

RC

IN

G

TO

A

FR

IC

A

Disclaimer

This comparative ranking report and the following fi fteen country reports provide a general overview of current activities and issues related to ICT Outsourcing in the country. The data presented here should be regarded as illustrative rather than exhaustive. ICT Outsourcing is at a particularly dynamic stage in Africa; new developments and announcements are happening almost on a daily basis somewhere on the continent. Therefore, these reports should be seen as ‘snapshots’ that were current at the time they were taken; it is expected that certain facts and fi gures presented may become outdated very quickly.

The fi ndings, interpretations and conclusions expressed herein are a faithful representation of the respond-ents of the interviews and secondary data collected. Strict analytical analysis has been carried out with the minimal infl uence of the authors/team members. References to data sources have been made as far as possible. In the case of the detailed data parameters used for scores and ranking, the same data source and timeline has been used for all the fi fteen countries compared. In the descriptive section of the country reports, all data received from the individual country has been used in order to give a complete assess-ment. Thus, countries that have provided more information have a better coverage than those that have not been able to provide data to the research team.

Board of Executive Directors of the CBC or CyberMedia cannot guarantee the accuracy of the data included in this work. The boundaries, colours, denominations, and other information shown on any map in this work do not imply on the part of the CBC and CyberMedia any judgment of the legal status of any territory or the endorsement or acceptance of such boundaries.

Neither the fi rm nor its directors, employees, agents or representatives shall be liable for any damages, whether direct or indirect, special or consequential including lost revenue or profi ts that may arise from or in connection with the use of this information. The information is in review and will be subject to change and amendments as appropriate.

“The content of this report is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavour to provide accurate information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate examination of the particular situation.”

Any clarifi cations/queries on the information should be addressed to CyberMedia.

02_Africa_Report09_FR.indd Sec3:ii02_Africa_Report09_FR.indd Sec3:ii 2/26/09 12:14:05 PM2/26/09 12:14:05 PM

02_Africa_Report09_FR.indd Sec3:iv02_Africa_Report09_FR.indd Sec3:iv 2/26/09 12:14:05 PM2/26/09 12:14:05 PM

OU

TS

OU

RC

IN

G

TO

A

FR

IC

A

DEDICATION

Development and education have come to many African nations but have the aspirations of all the African people been met? How many have employment opportunities matching their capabilities? How many people of African origin have reached the top positions in the rest of the world?

This study is dedicated to the youth in developing African nations, where unemployment is high and employment opportunities are low.

Although the central theme of outsourcing of services is cost-cutting, outsourced ICT tasks to youth at IT-enabled service centers in developing nations, is an opportunity to give dignifi ed employment to the educated youth. Such experience in work done remotely in Africa to serve the developed world enable the youth to obtain skills, experience and fi erce competi-tive capabilities to face the challenging global world.

This study focuses on what all the African nations covered in this study could do to improve and leverage the benefi ts that outsourcing can offer.

Arindam BoseResearch Advisor Global ServicesCyberMedia India

02_Africa_Report09_FR.indd Sec3:iii02_Africa_Report09_FR.indd Sec3:iii 2/26/09 12:14:05 PM2/26/09 12:14:05 PM

02_Africa_Report09_FR.indd Sec3:vi02_Africa_Report09_FR.indd Sec3:vi 2/26/09 12:14:05 PM2/26/09 12:14:05 PM

v

OU

TS

OU

RC

IN

G

TO

A

FR

IC

A

Foreword by Director General CBC vii

Preface by Chairman CyberMedia ix

In This Study 1

Methodology 1

Scope and Defi nitions 2

Project Team 2

1. Africa Situation Overview 3

1.1. Introduction 3

1.2. Overview of the Fifteen African Countries as Outsourcing Destinations 6

1.3. Outsourcing Attractiveness' Overall Scores and Ranking 7

1.4. Infrastructure, People & Skills and Business Environment Scores and Ranks 9

2. Methodology 23

2.1. Geographical Coverage 23

2.2. Research Framework and Design 24

2.3. Normalization and Calculation 25

2.4. Defi nitions of Lower Level Abstraction, Constructs, and Major Data Points 28

2.5. Defi nitions of Data Parameters, Units of Measurements, and Source 34

Glossary 37

Appendix I: Infrastructure Data Table 40

Appendix II: People and Skills Data Table 42

Appendix III: Business Environment Data Table 44

Appendix IV: Fifteen Africa Country Profi les 47

TABLE OF CONTENTS

02_Africa_Report09_FR.indd Sec3:v02_Africa_Report09_FR.indd Sec3:v 2/26/09 12:14:05 PM2/26/09 12:14:05 PM

02_Africa_Report09_FR.indd Sec3:viii02_Africa_Report09_FR.indd Sec3:viii 2/26/09 12:14:05 PM2/26/09 12:14:05 PM

vii

OU

TS

OU

RC

IN

G

TO

A

FR

IC

A

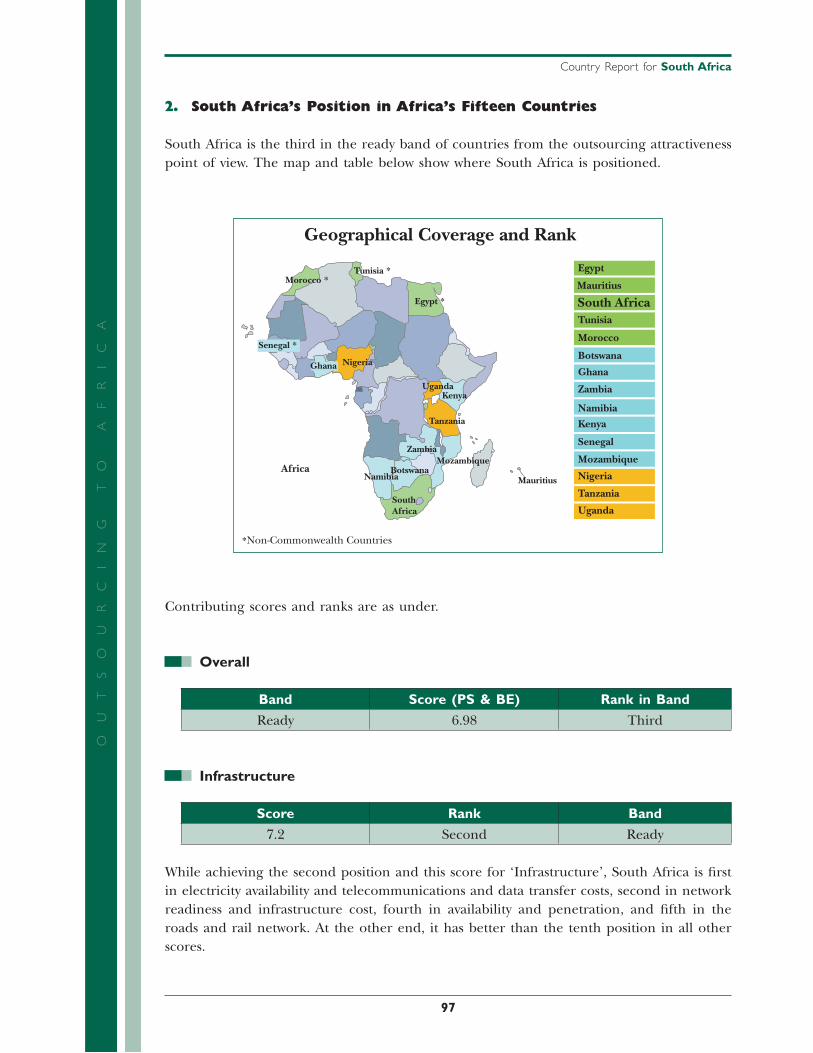

I am delighted to present this report on the outsourcing potential of Africa, which is the fi rst of its kind to outline the key issues that face the continent. Whilst there are dominant nations in the outsourcing arena such as India, Philippines, Mexico, and China, there is a strong case emerging for African nations. With vastly improved connectivity; proximity to key markets; multi-lingual skills; lower wage costs and suitable time-zones, many African nations are now vying for a share of the global outsourcing business.

Having been given the mandate from the Commonwealth Heads of Government in 1997 to involve the private sector in the promotion of trade and investment within the Common-wealth, the Commonwealth Business Council set out its vision for “sharing global prosperity by making globalisation work for all”. Since then, CBC has pursued its mission through the promotion of global trade and investment with an enhanced role for the private sector.

The Commonwealth Business Council is committed to pursuing the agenda on outsourcing in Africa. This report, as well as providing a clear picture of the current state of play with regard to infrastructure, society and economics, should act as a springboard for identifying new areas for projects to fl ourish. I sincerely hope that governments and the private sector fi nd this report useful.

We look forward to working together to achieve our common goals for economic growth and sustainable development in Africa.

FOREWORD

by Dr Mohan Kaul, Director General, CBC

02_Africa_Report09_FR.indd Sec3:vii02_Africa_Report09_FR.indd Sec3:vii 2/26/09 12:14:05 PM2/26/09 12:14:05 PM

02_Africa_Report09_FR.indd Sec3:x02_Africa_Report09_FR.indd Sec3:x 2/26/09 12:14:06 PM2/26/09 12:14:06 PM

ix

OU

TS

OU

RC

IN

G

TO

A

FR

IC

A

PREFACE

by Mr. Pradeep Gupta, Chairman, CyberMedia

The world of outsourcing is going through major changes with a number of countries emerg-ing as challengers to grab a share of the rapidly expanding pie. CyberMedia has witnessed, chronicled and catalyzed the growth of the Indian outsourcing industry. CyberMedia was part of the World Bank funded study in 1992, which looked into India’s competitiveness in IT services. At that time, India’s total exports were under $150mn. In seventeen years, this fi gure has risen to a stupendous $17bn. As part of the Steering Committee of that study, I saw how seeds of an idea can be converted into strategy and executed to make a complete transformation of an industry and indeed a nation.

Africa is ready to chart this journey. Of course, the path followed by India, will not work today. A new strategy has to evolve relevant for a mature market with formidable players. It is with this background that CyberMedia became the knowledge partner with Common-wealth Business Council in putting together this report that compares 15 African nations and provides pointers and data for their growth into the outsourcing area.

This is merely the fi rst step. I am sure the Africans nations covered in the study will evolve their future strategies on the strength of this report.

02_Africa_Report09_FR.indd Sec3:ix02_Africa_Report09_FR.indd Sec3:ix 2/26/09 12:14:06 PM2/26/09 12:14:06 PM

1

OU

TS

OU

RC

IN

G

TO

A

FR

IC

A

Methodology

The attractiveness of a nation as an outsourcing destination depends on the ICT and other supporting infrastructure available, the skill levels of the people and their availability, and the business environment.

In this study, a framework comprising of qualitative and quantitative assessment was followed. Parameters pertaining to outsourcing were carefully selected from reputed international stud-ies. The data collected was converted to merit scores for Infrastructure, People and Skills and Business Environment and sub elements of these aspects. This unique ‘CyberMedia Research Methodology’ used to calculate the scores are described in chapter two of this report.

Multi-faceted observations, which cannot be directly measured, were observed. The following qualitative aspects important in attracting a potential investor coming to the country to set up an outsourcing operation have been analysed by survey of literature—Internet search and limited country visits and telephonic interviews:

Country, Political and Economic Profi le.

Principal Government Offi cials.

Foreign Relations.

Living, Security, and Safety Perceptions.

ICT Policy, ICT Infrastructure and Service.

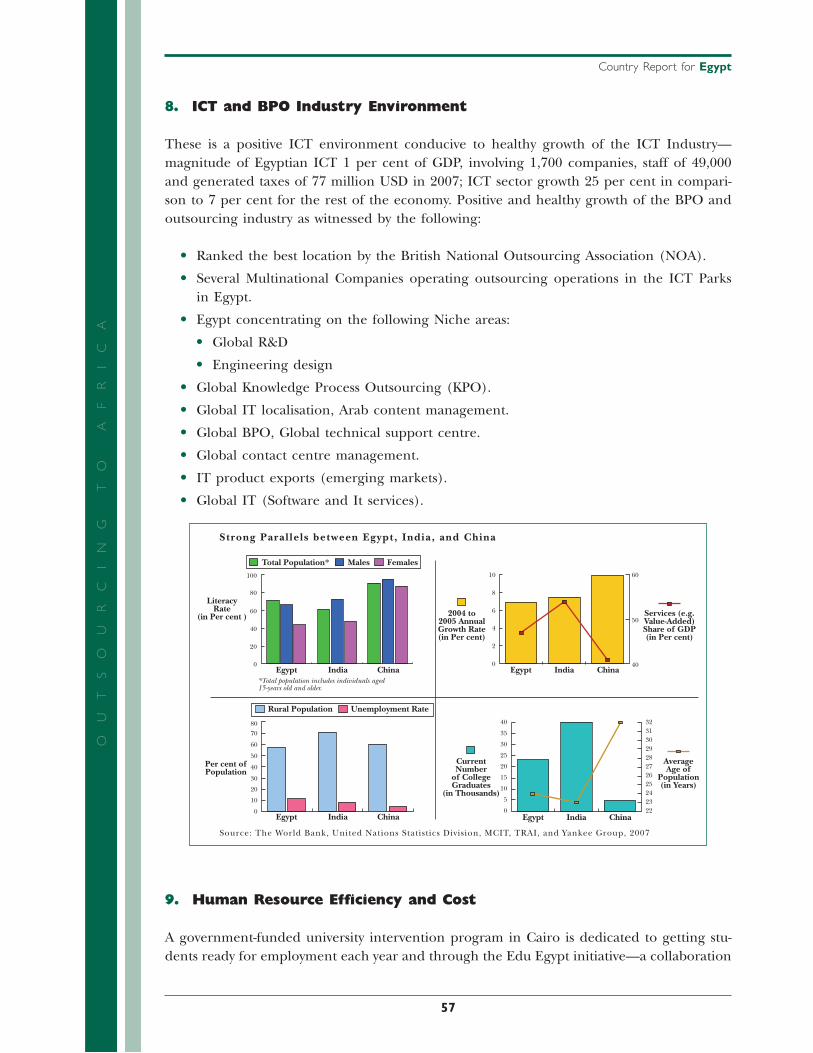

ICT and BPO Industry Environment.

Human Resource Effi ciency and Cost.

Legal and Enforcement Issues.

Labour and Expatriate Worker’s Permits.

Revenue, Tax, and Repatriation Issues.

Investment Policy and Incentives.

Government Agencies Giving Support to Outsourcing.

In case of the detailed data parameters used for scores and ranking, the same data source and timeline has been used in order to give as complete an assessment as possible, for ranks and scores. The ‘Infrastructure’ scores are calculated on the various infrastructure-related parameters, and thereafter scores are divided into three bands i.e. ‘Ready’, ‘ Upcoming’, and ‘Yet to be ready’, for becoming an attractive outsourcing destination. In ‘Outsourcing

•

•

•

•

•

•

•

•

•

•

•

•

IN THIS STUDY

02_Africa_Report09_FR.indd Sec1:102_Africa_Report09_FR.indd Sec1:1 2/26/09 12:14:06 PM2/26/09 12:14:06 PM

2

OU

TS

OU

RC

IN

G

TO

A

FR

IC

AAttractiveness Index’, there are two abstraction levels—‘People and Skills’ and ‘Business Environment’, having equal weightage in overall rankings of index.

The fi nal outsourcing attractiveness index is produced keeping infrastructure rankings as the base; only the countries which are able to qualify in infrastructure bands are placed higher in the outsourcing attractiveness index.

Scope and Defi nitions

Whilst there are dominant nations in the outsourcing arena such as India, Philippines, Mexico, and China, etc., there is a strong case emerging for African nations.

With improving connectivity, proximity to key markets, multi-lingual skills, lower wage costs and physical infrastructure costs, and suitable time-zones many African nations are now vying for a share of the global outsourcing business.

To make the best of this emerging opportunity, the Commonwealth Business Council (CBC) with Global Services (GS), a CyberMedia (India) group company, is presenting the fi rst ever ‘African Outsourcing Summit’ in 2009. This summit will bring representatives from over fi fteen African nations together with key decision makers and other stakeholders from European and global outsourcing industry.

This research effort by CyberMedia-Global Services (India) benchmarks fi fteen African coun-tries on many different parameters that will help decision makers in matching the right outsourcing destinations with outsourcing needs. This report is the background paper for the summit.

Project Team

Mr. Kamal Vohra, Assistant Manager, CyberMedia India

Mr. Kapil Dev Singh, Senior Vice-President, CyberMedia India

Mr. Arindam Bose, Research Advisor, CyberMedia India

Mr. Hoshie Ghaswalla, President, CyberMedia India

Ms. Keerthi Nair, Sr. Manager (Editorial), CyberMedia India (Editorial Support)

Mr. Bhupendra Bhanu, GM, CyberMedia India (Production Co-ordinator)

Mr. Satish Khankriyal, Manager (R&D), CyberMedia India (Design & Layout)

Mr. Ashimendu Dey, Associate Art and Ms. Poonam Ujjainwal, Sr. Illustrator, CyberMedia India (Illustrations)

Mr. Raj Kishore, Graphic Designer, CyberMedia India (Cover Design)

1.

2.

3.

4.

5.

6.

7.

8.

9.

In This Study

02_Africa_Report09_FR.indd Sec1:202_Africa_Report09_FR.indd Sec1:2 2/26/09 12:14:06 PM2/26/09 12:14:06 PM

3

OU

TS

OU

RC

IN

G

TO

A

FR

IC

A

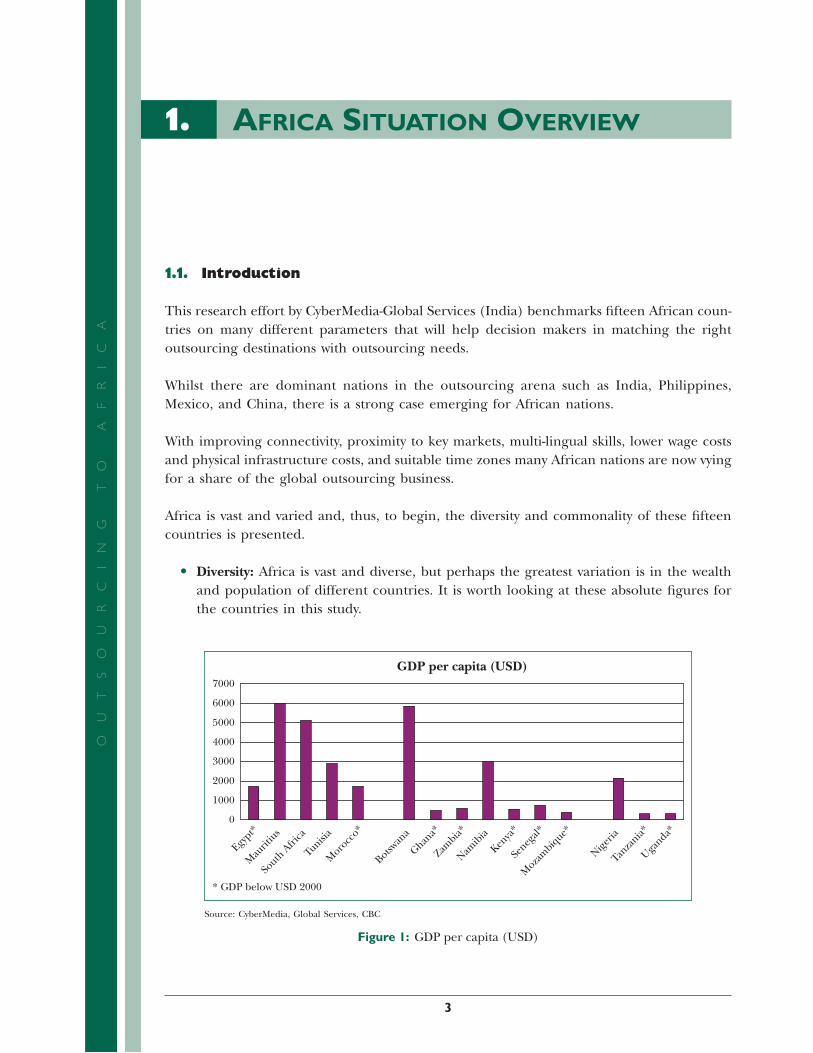

1.1. Introduction

This research effort by CyberMedia-Global Services (India) benchmarks fi fteen African coun-tries on many different parameters that will help decision makers in matching the right outsourcing destinations with outsourcing needs.

Whilst there are dominant nations in the outsourcing arena such as India, Philippines, Mexico, and China, there is a strong case emerging for African nations.

With improving connectivity, proximity to key markets, multi-lingual skills, lower wage costs and physical infrastructure costs, and suitable time zones many African nations are now vying for a share of the global outsourcing business.

Africa is vast and varied and, thus, to begin, the diversity and commonality of these fi fteen countries is presented.

Diversity: Africa is vast and diverse, but perhaps the greatest variation is in the wealth and population of different countries. It is worth looking at these absolute fi gures for the countries in this study.

GDP per capita (USD)7000

6000

5000

4000

3000

2000

1000

0

* GDP below USD 2000

Egypt*

Mau

ritiu

s

South

Afri

ca

Tunisia

Moro

cco*

Botswan

a

Ghana*

Zambia*

Namib

ia

Kenya

*

Seneg

al*

Moza

mbiq

ue*

Nigeria

Tanza

nia*

Uganda*

Source: CyberMedia, Global Services, CBC

Figure 1: GDP per capita (USD)

•

1. AFRICA SITUATION OVERVIEW

02_Africa_Report09_FR.indd Sec1:302_Africa_Report09_FR.indd Sec1:3 2/26/09 12:14:06 PM2/26/09 12:14:06 PM

4

1. Africa Situation Overview

OU

TS

OU

RC

IN

G

TO

A

FR

IC

A

Egypt**

Mau

ritiu

s**

South

Afri

ca

Tunisia*

*

Moro

cco**

Botswan

a

Ghana*

*

Zambia*

*

Namib

ia

Kenya

Seneg

al

Moza

mbiq

ue

Nigeria

**

Tanza

nia**

Uganda*

*

60.00Population unemployed (% of labour...)

50.00

40.00

30.00

20.00

10.00

0

** Unemployment below 20%

Source: CyberMedia, Global Services, CBC

Figure 2: Population unemployed

The gross national per capita income, population, population density, un-employment, poverty, and other major characteristics are very diverse and at times seemingly contra-dictory. All possible combinations are there across these fi fteen nations, namely:

Low GDP* and Low Unemployment**: Egypt, Morocco, Tanzania, Uganda, Ghana, and Zambia.

High GDP and Low Unemployment: Mauritius, Nigeria, and Tunisia.

Low GDP and High Unemployment: Kenya, Mozambique, and Senegal.

High GDP and High Unemployment: Botswana, South Africa, and Namibia.

Commonality: There is one aspect common to Africa and specially sub-Saharan Africa—severe limitations in broadband connectivity. This diagram shows the severe limitations of this continent with reference to all other continents.

Fiber in use as of year-end 2004

>500 500 50 10

Gbps

Source: TeleGeography Research @ 2006 PriMetrica.lnc.

Figure 3: Existing broadband connectivity to Africa

•

02_Africa_Report09_FR.indd Sec1:402_Africa_Report09_FR.indd Sec1:4 2/26/09 12:14:06 PM2/26/09 12:14:06 PM

1. Africa Situation Overview

5

OU

TS

OU

RC

IN

G

TO

A

FR

IC

AAttempts to improve this situation are in progress and will take till 2011 to materialize with the following systems coming up to connect African countries:

Seacom

East Coast.

13 700 km undersea cable.

To connect Southern and East Africa.

To India and Europe via Madagascar, Mozambique, Tanzania, Kenya.

Complete by June 2009.

To provide low-cost broadband.

EASSy

East Coast.

10 000 km.

To connect South Africa, Mozambique, Madagascar, Somalia, Djibouti, Sudan.

To be complete by end of 2010.

Financed by World Bank and DBSA.

Infraco

West Coast to UK.

To be complete by fi rst half of 2010.

Originally built by State Companies Eskom and Transnet—both shareholders at Neotel.

This is the expected scenario by 2011.

Source: CyberMedia, Global Services, CBC

Figure 4: Anticipated broadband scenario by 2011

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

02_Africa_Report09_FR.indd Sec1:502_Africa_Report09_FR.indd Sec1:5 2/26/09 12:14:06 PM2/26/09 12:14:06 PM

6

1. Africa Situation Overview

OU

TS

OU

RC

IN

G

TO

A

FR

IC

AConsequently the cost of connectivity is extremely high—negative to outsourcing efforts; the fi gure below shows the comparison of connectivity costs of African coun-tries with others.

South Asia

US$

per

100

kbp

s (2

006)

Middle East &North Africa

Europe &Central Asia

Latin America& Caribbean

East Asia &Pacific

Sub-SaharanAfrica

0

20

40

60

80

100

120

Comparison of Regional Average Broadband Retail Prices

Source: ITU 2007a. World Bank staff analysis

Figure 5: Broadband connectivity costs by region

With the developments expected this situation should improve. This graph clearly shows an advantage that North Africa has over sub-Saharan, central, and southern Africa on outsourc-ing infrastructure. Still, Africa is far disadvantaged as compared to East Asia, Pacifi c, and even Latin America and the Caribbean.

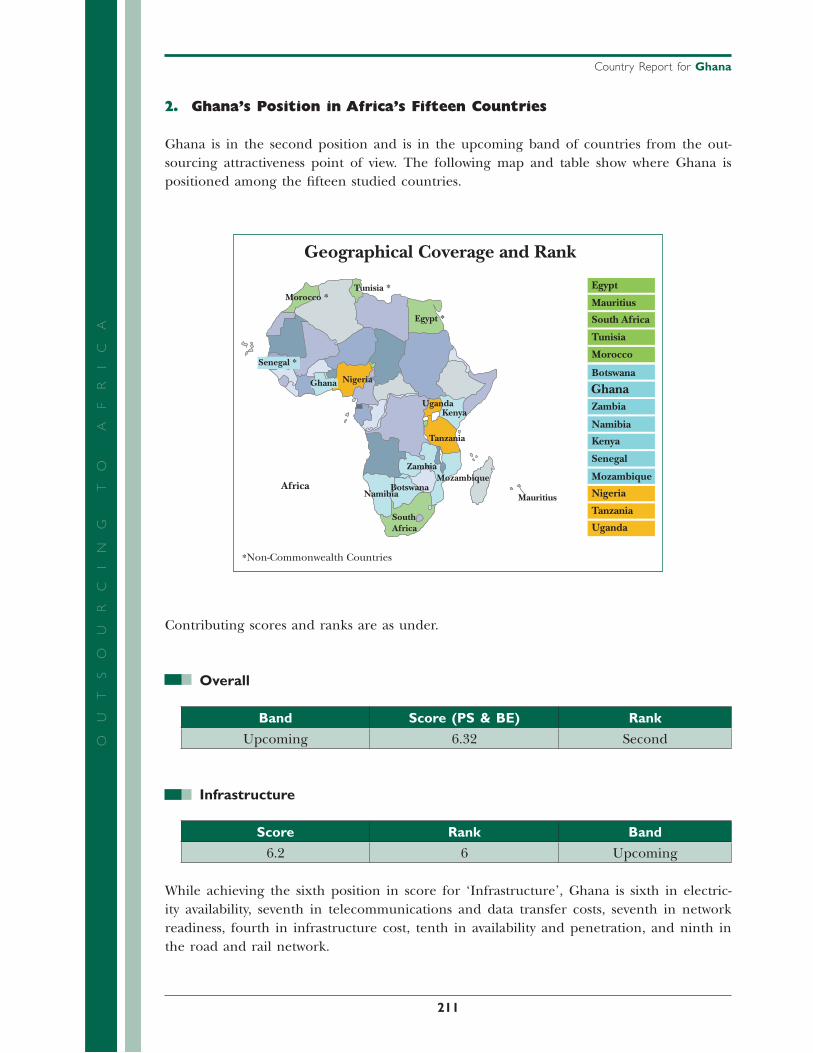

1.2. Overview of the Fifteen African Countries as Outsourcing Destinations

Outsourcing has arrived in Africa. This report quantitatively shows what is possible. In spite of the negative perceptions that Africa has only places like Somalia with pirates, Congo full of rebels, Nigeria the citadel of cyber crime, and South Africa the hotbed of carjacking and Wild West type of shootouts, Africa has the most peaceful, clean, and serene locations. Today most ‘Bollywood’1 and even some ‘Hollywood’ movies are shot in Africa. Thus outsourcing has come for good, and it is for the African nations to come together and spread the right message to propagate the right image of Africa as an outsourcing destination.

The fi ndings reveal that Africa has arrived in outsourcing with North Africa leading and South Africa close behind. The broadband connectivity projects in hand due to be com-pleted in the next few years will make parts of Africa, more tranquil, sparsely populated, and environmentally clear and clean—the next preferred outsourcing destination.

1Citadel of the Indian Cinema Industry—Hollywood of India

02_Africa_Report09_FR.indd Sec1:602_Africa_Report09_FR.indd Sec1:6 2/26/09 12:14:07 PM2/26/09 12:14:07 PM

1. Africa Situation Overview

7

OU

TS

OU

RC

IN

G

TO

A

FR

IC

A

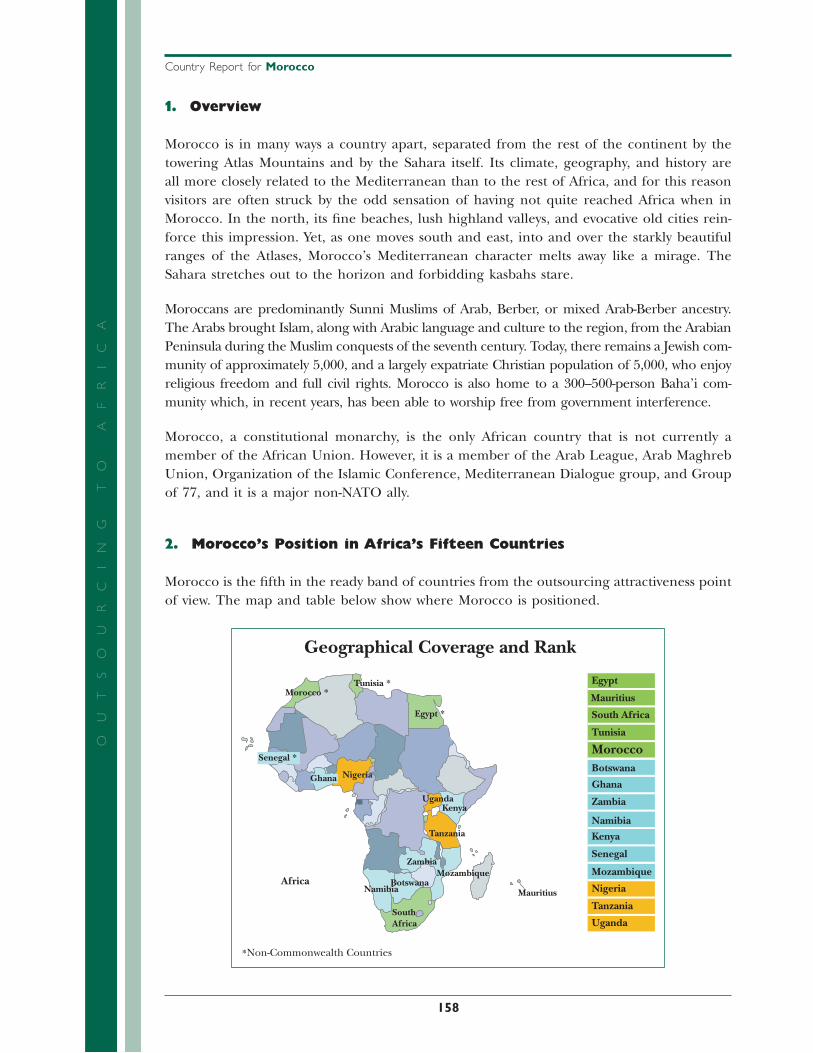

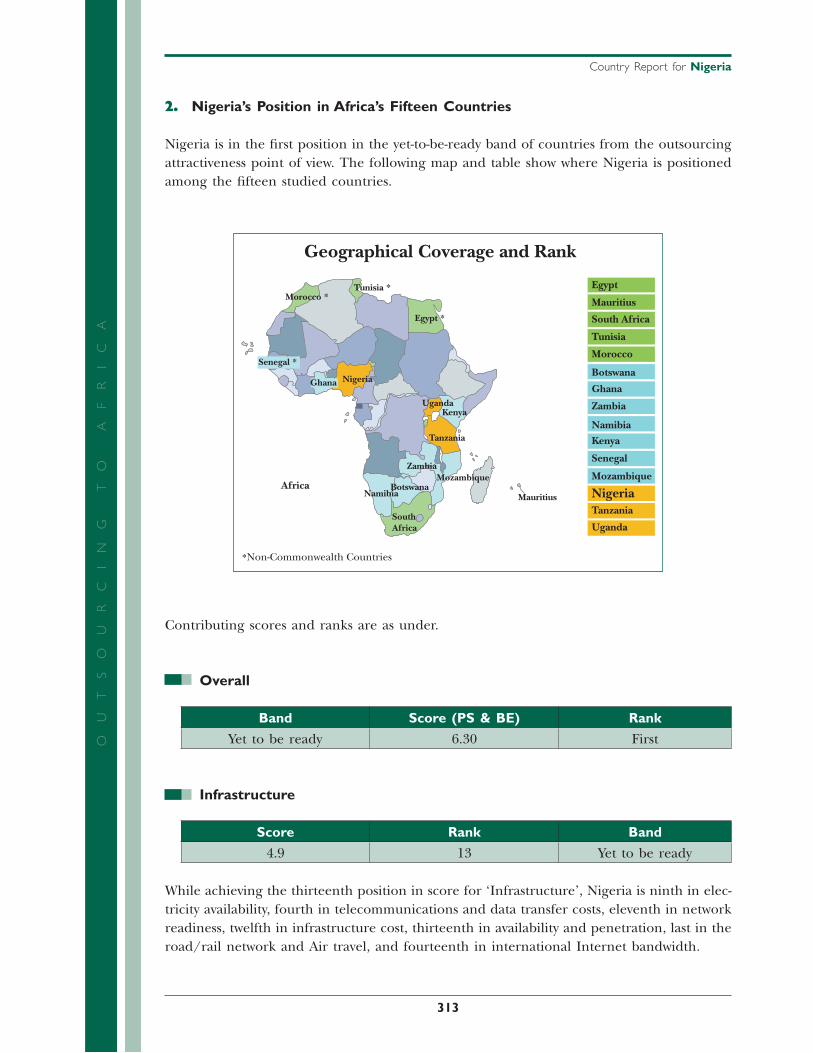

Morocco *

Morocco

Tunisia *

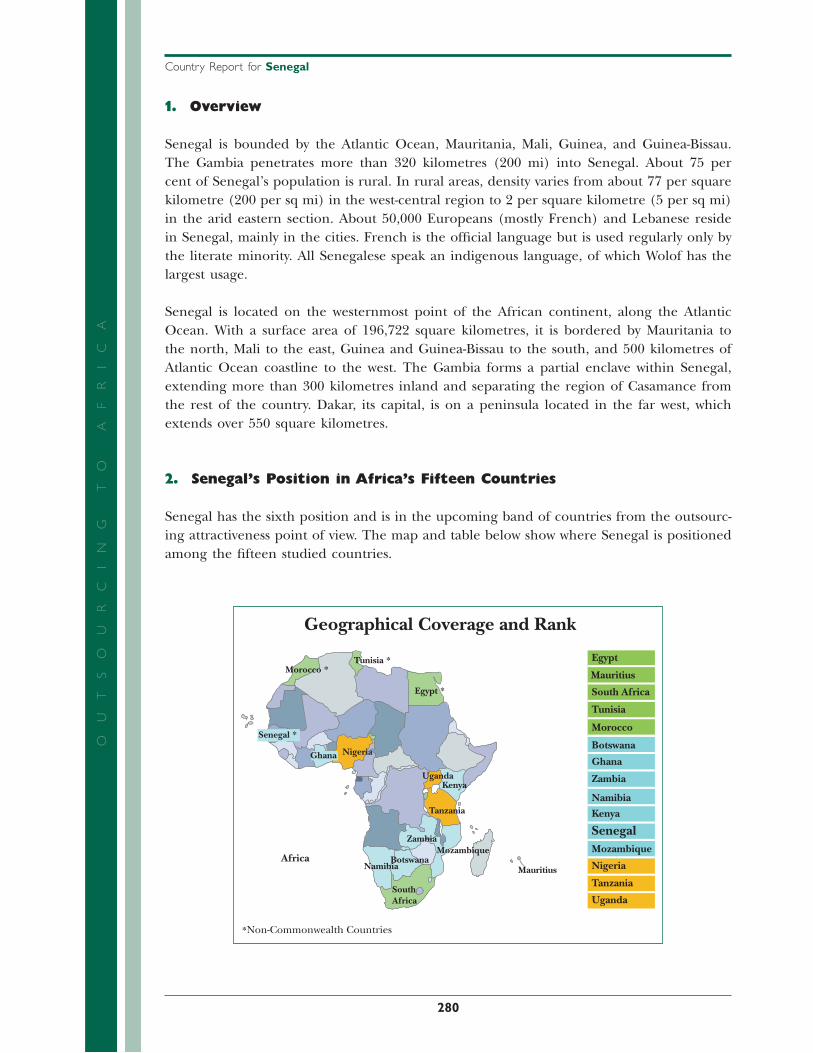

Geographical Coverage and Rank

Tunisia

Egypt *

Egypt

Senegal *

Senegal

GhanaGhana

Nigeria

Nigeria

Uganda

Uganda

Kenya

KenyaTanzania

Tanzania

Zambia

Zambia

Mozambique MozambiqueBotswana

Botswana

Namibia

Namibia

SouthAfrica

South Africa

MauritiusAfrica

*Non-Commonwealth Countries

Mauritius

Source: CyberMedia, Global Services, CBC

Figure 6: Map of Africa showing the countries in the three bands—Ready, Upcoming, and Yet to be ready Infrastructure Status

1.3. Outsourcing Attractiveness’ Overall Scores and Ranking

The overall outsourcing attractiveness depends primarily on the infrastructure readiness fol-lowed by a combination of people and skills and business environment. The countries are fi rst categorized in bands depending on infrastructure readiness followed by ranking within the bands based on the sum of the people and skills and business environment scores. People and skills and business environment have equal importance, hence equal weightage.

Outsourcing Attractiveness Index

Countries are ranked within their bands based on theirBE + People & Skill Scores

Countries are ranked within their bands based on their:

People & Skills Scores

plus

Business Environment Scores

Source: CyberMedia, Global Services, CBC

Figure 7: Deriving outsourcing attractiveness ranking

02_Africa_Report09_FR.indd Sec1:702_Africa_Report09_FR.indd Sec1:7 2/26/09 12:14:07 PM2/26/09 12:14:07 PM

8

1. Africa Situation Overview

OU

TS

OU

RC

IN

G

TO

A

FR

IC

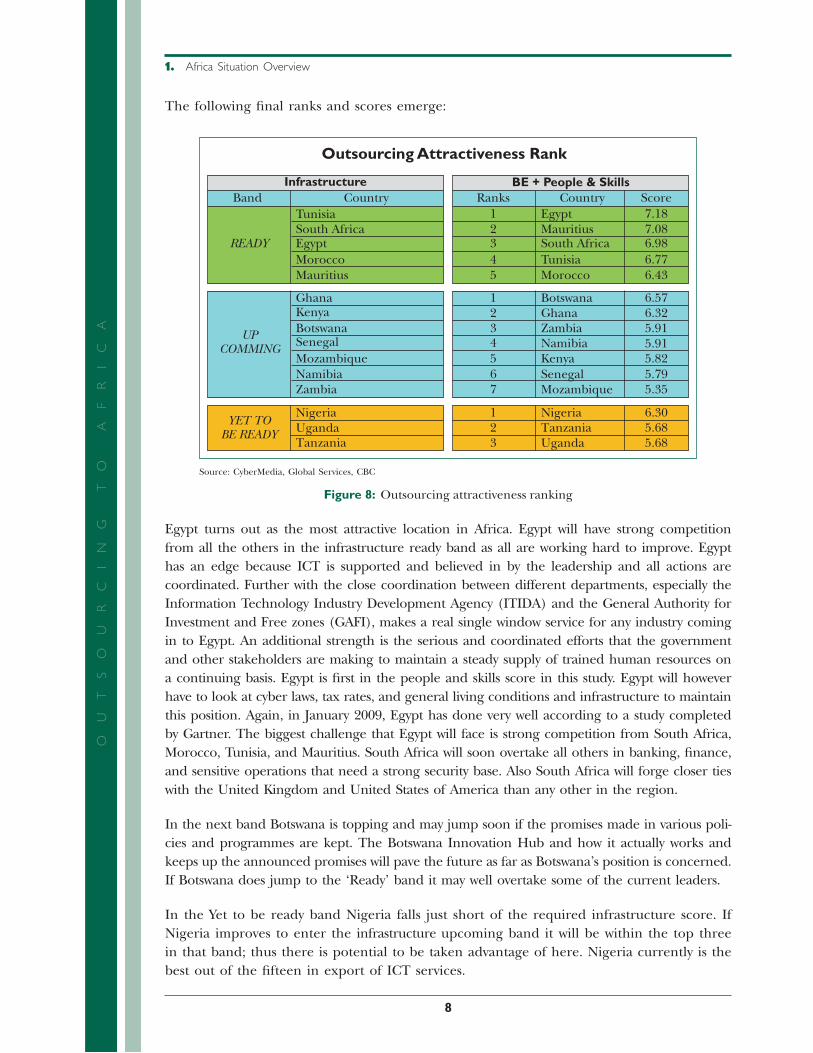

AThe following fi nal ranks and scores emerge:

Outsourcing Attractiveness Rank

GhanaKenyaBotswanaSenegalMozambiqueNamibiaZambia

UPCOMMING

BotswanaGhanaZambiaNamibiaKenyaSenegalMozambique

6.576.325.915.915.825.795.35

1234567

NigeriaTanzaniaUganda

123

6.305.685.68

InfrastructureBand Country

TunisiaSouth AfricaEgyptMoroccoMauritius

READY

BE + People & SkillsRanks Country Score

EgyptMauritiusSouth AfricaTunisiaMorocco

12345

7.187.086.986.776.43

Nigeria

TanzaniaUganda

YET TOBE READY

Source: CyberMedia, Global Services, CBC

Figure 8: Outsourcing attractiveness ranking

Egypt turns out as the most attractive location in Africa. Egypt will have strong competition from all the others in the infrastructure ready band as all are working hard to improve. Egypt has an edge because ICT is supported and believed in by the leadership and all actions are coordinated. Further with the close coordination between different departments, especially the Information Technology Industry Development Agency (ITIDA) and the General Authority for Investment and Free zones (GAFI), makes a real single window service for any industry coming in to Egypt. An additional strength is the serious and coordinated efforts that the government and other stakeholders are making to maintain a steady supply of trained human resources on a continuing basis. Egypt is fi rst in the people and skills score in this study. Egypt will however have to look at cyber laws, tax rates, and general living conditions and infrastructure to maintain this position. Again, in January 2009, Egypt has done very well according to a study completed by Gartner. The biggest challenge that Egypt will face is strong competition from South Africa, Morocco, Tunisia, and Mauritius. South Africa will soon overtake all others in banking, fi nance, and sensitive operations that need a strong security base. Also South Africa will forge closer ties with the United Kingdom and United States of America than any other in the region.

In the next band Botswana is topping and may jump soon if the promises made in various poli-cies and programmes are kept. The Botswana Innovation Hub and how it actually works and keeps up the announced promises will pave the future as far as Botswana’s position is concerned. If Botswana does jump to the ‘Ready’ band it may well overtake some of the current leaders.

In the Yet to be ready band Nigeria falls just short of the required infrastructure score. If Nigeria improves to enter the infrastructure upcoming band it will be within the top three in that band; thus there is potential to be taken advantage of here. Nigeria currently is the best out of the fi fteen in export of ICT services.

02_Africa_Report09_FR.indd Sec1:802_Africa_Report09_FR.indd Sec1:8 2/26/09 12:14:08 PM2/26/09 12:14:08 PM

1. Africa Situation Overview

9

OU

TS

OU

RC

IN

G

TO

A

FR

IC

A1.4. Infrastructure, People & Skills and Business

Environment Scores and Ranks

A. Infrastructure Readiness

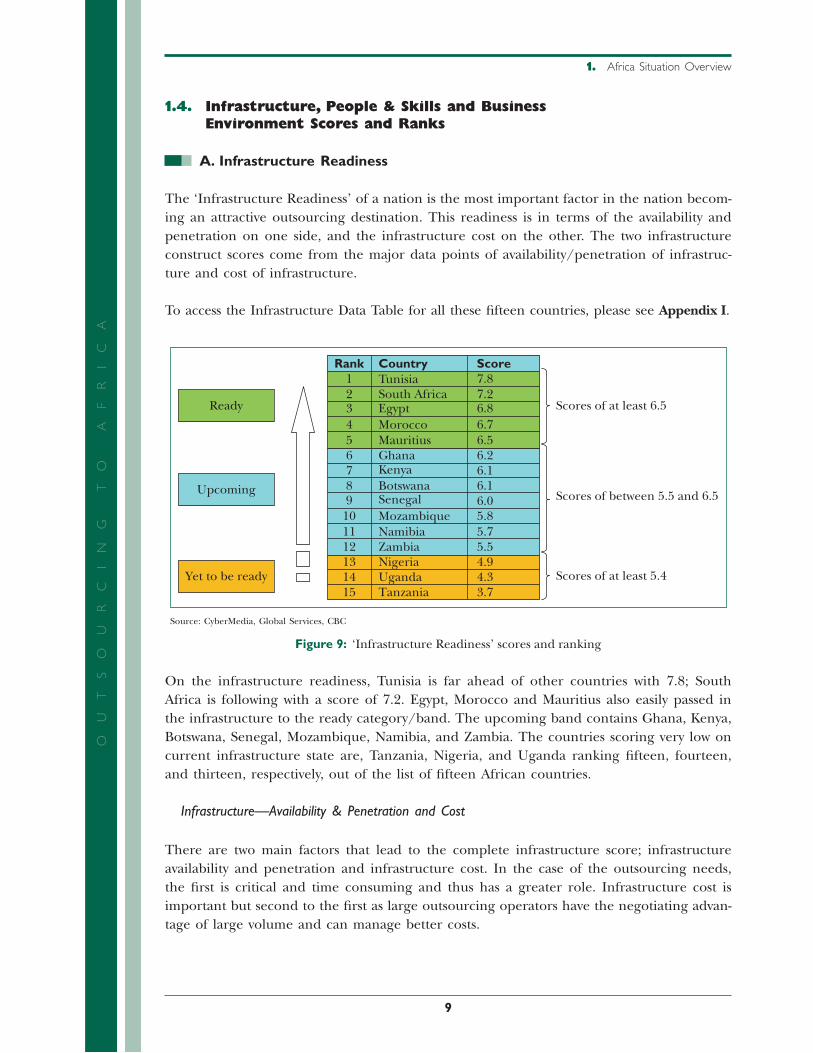

The ‘Infrastructure Readiness’ of a nation is the most important factor in the nation becom-ing an attractive outsourcing destination. This readiness is in terms of the availability and penetration on one side, and the infrastructure cost on the other. The two infrastructure construct scores come from the major data points of availability/penetration of infrastruc-ture and cost of infrastructure.

To access the Infrastructure Data Table for all these fi fteen countries, please see Appendix I.

6.26.16.16.05.85.75.5

6789

101112131415

4.94.33.7

Rank Country Score12345

7.87.26.86.76.5

GhanaKenyaBotswanaSenegalMozambiqueNamibiaZambia

TunisiaSouth AfricaEgyptMoroccoMauritius

NigeriaUgandaTanzania

Ready Scores of at least 6.5

Scores of between 5.5 and 6.5

Scores of at least 5.4

Upcoming

Yet to be ready

Source: CyberMedia, Global Services, CBC

Figure 9: ‘Infrastructure Readiness’ scores and ranking

On the infrastructure readiness, Tunisia is far ahead of other countries with 7.8; South Africa is following with a score of 7.2. Egypt, Morocco and Mauritius also easily passed in the infrastructure to the ready category/band. The upcoming band contains Ghana, Kenya, Botswana, Senegal, Mozambique, Namibia, and Zambia. The countries scoring very low on current infrastructure state are, Tanzania, Nigeria, and Uganda ranking fi fteen, fourteen, and thirteen, respectively, out of the list of fi fteen African countries.

Infrastructure—Availability & Penetration and Cost

There are two main factors that lead to the complete infrastructure score; infrastructure availability and penetration and infrastructure cost. In the case of the outsourcing needs, the fi rst is critical and time consuming and thus has a greater role. Infrastructure cost is important but second to the fi rst as large outsourcing operators have the negotiating advan-tage of large volume and can manage better costs.

02_Africa_Report09_FR.indd Sec1:902_Africa_Report09_FR.indd Sec1:9 2/26/09 12:14:08 PM2/26/09 12:14:08 PM

10

1. Africa Situation Overview

OU

TS

OU

RC

IN

G

TO

A

FR

IC

AInfrastructure availability and penetration

This construct score is made up of the major data point (MDP) scores Network Readi-ness, Internet Bandwidth, Electricity Availability, and the Road and Rail Network.

Infrastructure Availability & Penetration5.5

54.5

43.5

32.5

21.5

10.5

0

Egypt

Mau

ritiu

s

South

Afri

ca

Tunisia

Moro

cco

Botswan

a

Ghana

Zambia

Namib

ia

Kenya

Seneg

al

Moza

mbiq

ue

Nigeria

Tanza

nia

Uganda

Ready

Upcoming

Yet to be ready

Source: CyberMedia, Global Services, CBC

Figure 10: Infrastructure Availability and Penetration Scores and Ranking

Infrastructure—cost

This construct score is made up of the major data point (MDP) scores coming from cost of space and facilities (Africa Research Report, Knight Frank); Cost of Stay and Trans-port (UNDP rates and prevailing air fares) and data transfer costs (World Bank).

3.5

Infrastructure Cost

Ready

Upcoming

Yet to be ready3

2.5

2

1.5

1

0.5

0

Tunisia

South

Afri

ca

Moza

mbiq

ue

Ghana

Kenya

Mau

ritiu

s

Egypt

Botswan

a

Seneg

al

Moro

cco

Zambia

Nigeria

Namib

ia

Tanza

nia

Uganda

Source: CyberMedia, Global Services, CBC

Figure 11: Infrastructure costs scores and ranking

It is now pertinent to look at each one of the individual ‘Major Data Points’ (MDPs) that go towards these two constructs, namely availability and cost.

•

•

02_Africa_Report09_FR.indd Sec1:1002_Africa_Report09_FR.indd Sec1:10 2/26/09 12:14:08 PM2/26/09 12:14:08 PM

1. Africa Situation Overview

11

OU

TS

OU

RC

IN

G

TO

A

FR

IC

AInfrastructure—availability/penetration-network readiness

Egypt

Mau

ritiu

s

South

Afri

ca

Tunisia

Moro

cco

Botswan

a

Ghana

Zambia

Namib

ia

Kenya

Seneg

al

Moza

mbiq

ue

Nigeria

Tanza

nia

Uganda

Ready

Upcoming

Yet to be ready

Network Readiness9.008.007.006.005.004.003.002.001.000.00

Source: CyberMedia, Global Services, CBC

Figure 12: Network readiness ‘MDP’ scores

In this MDP score all the fi fteen countries are scoring between 5.79 (for Mozambique) and 7.78 (for Tunisia, which is the best).

Infrastructure—availability/penetration-international Internet bandwidth

Ready

Upcoming

Yet to be ready

Moro

cco

Zambia

Tunisia

Kenya

South

Afri

ca

Moza

mbiq

ue

Mau

ritiu

s

Ghana

Nigeria

Egypt

Seneg

al

Botswan

a

Namib

ia

Uganda

Tanza

nia

International Internet Bandwidth12.0010.00

8.006.004.002.000.00

Source: CyberMedia, Global Services, CBC

Figure 13: International Internet bandwidth

It is important to recognise that all these will improve as soon as broadband connection from all the new projects are complete in 2009 to 2011.

•

•

02_Africa_Report09_FR.indd Sec1:1102_Africa_Report09_FR.indd Sec1:11 2/26/09 12:14:08 PM2/26/09 12:14:08 PM

12

1. Africa Situation Overview

OU

TS

OU

RC

IN

G

TO

A

FR

IC

AInfrastructure—availability/penetration-electricity availability

Ready

Upcoming

Yet to be ready

South

Afri

ca

Tunisia

Moza

mbiq

ue

Ghana

Kenya

Mau

ritiu

s

Egypt

Botswan

a

Seneg

al

Moro

cco

Zambia

Nigeria

Namib

ia

Tanza

nia

Uganda

12.00

Electricity Availability

10.008.006.004.002.000.00

Source: CyberMedia, Global Services, CBC

Figure 14: Electricity availability

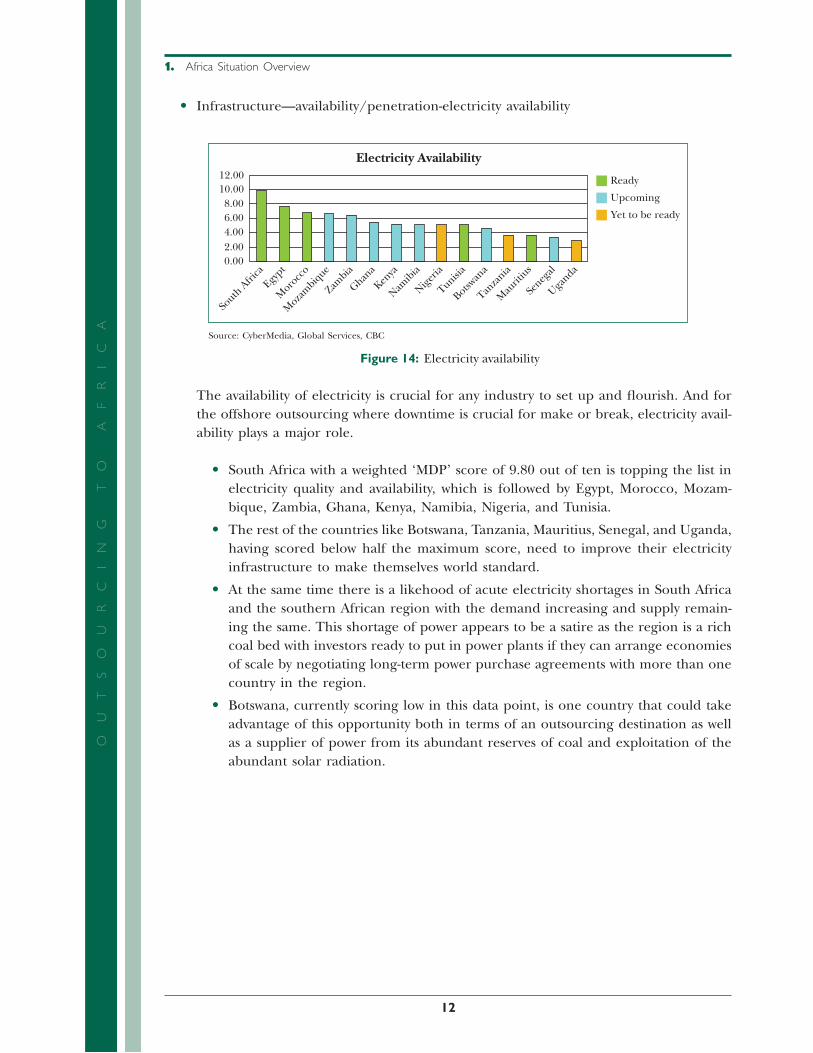

The availability of electricity is crucial for any industry to set up and fl ourish. And for the offshore outsourcing where downtime is crucial for make or break, electricity avail-ability plays a major role.

South Africa with a weighted ‘MDP’ score of 9.80 out of ten is topping the list in electricity quality and availability, which is followed by Egypt, Morocco, Mozam-bique, Zambia, Ghana, Kenya, Namibia, Nigeria, and Tunisia.

The rest of the countries like Botswana, Tanzania, Mauritius, Senegal, and Uganda, having scored below half the maximum score, need to improve their electricity infrastructure to make themselves world standard.

At the same time there is a likehood of acute electricity shortages in South Africa and the southern African region with the demand increasing and supply remain-ing the same. This shortage of power appears to be a satire as the region is a rich coal bed with investors ready to put in power plants if they can arrange economies of scale by negotiating long-term power purchase agreements with more than one country in the region.

Botswana, currently scoring low in this data point, is one country that could take advantage of this opportunity both in terms of an outsourcing destination as well as a supplier of power from its abundant reserves of coal and exploitation of the abundant solar radiation.

•

•

•

•

•

02_Africa_Report09_FR.indd Sec1:1202_Africa_Report09_FR.indd Sec1:12 2/26/09 12:14:09 PM2/26/09 12:14:09 PM

1. Africa Situation Overview

13

OU

TS

OU

RC

IN

G

TO

A

FR

IC

AInfrastructure—availability/penetration

Egypt

Mau

ritiu

s

South

Afri

ca

Tunisia

Moro

cco

Botswan

a

Ghana

Zambia

Namib

iaKen

ya

Seneg

al

Moza

mbiq

ue

Nigeria

Tanza

nia

Uganda

Ready

Upcoming

Yet to be ready

Road/Rail Network and Air Travel9.008.007.006.005.004.003.002.001.000.00

Source: CyberMedia, Global Services, CBC

Figure 15: Road and rail network

More than half the countries score high in this major data point (MDP) with Tunisia, Namibia, and Botswana leading, though Botswana and Namibia are in the Upcoming band.

Infrastructure cost—rental and cost of commercial premises

The rental and cost of commercial premises is a Major Data Parameter (MDP) that helps in calculating overall cost of rental (per sq ft) and cost of ownership of premises for commercial activity. It is worth remembering that a higher score means a more cost-effective space and facilities. Thus space and facilities in Botswana are more cost effective than those in South Africa or Egypt.

Egypt

Mau

ritiu

s

South

Afri

ca

Tunisia

Moro

cco

Botswan

a

Ghana

Zambia

Namib

ia

Kenya

Seneg

al

Moza

mbiq

ue

Nigeria

Tanza

nia

Uganda

ReadyUpcoming

Yet to be ready

Rental and Cost of Commercial Premises12.0010.008.006.004.002.000.00

Source: CyberMedia, Global Services, CBC

Figure 16: Costs of inputs in terms of space and facilities

•

•

02_Africa_Report09_FR.indd Sec1:1302_Africa_Report09_FR.indd Sec1:13 2/26/09 12:14:09 PM2/26/09 12:14:09 PM

14

1. Africa Situation Overview

OU

TS

OU

RC

IN

G

TO

A

FR

IC

AInfrastructure cost—stay and travel ‘MDP’ scores

Travel and stay costs of the people travelling to support the outsourcing industries from countries that buy these services need to be considered. This ‘MDP’ is based on the UNDP travelling allowance rates and prevailing cost of tickets from London to the destination country as the detailed data points.

Ready

Upcoming

Yet to be ready

Tunisia

Seneg

al

Moro

cco

Botswan

aEgy

pt

Zambia

Ghana

Mau

ritiu

s

Nigeria

Namib

ia

Moza

mbiq

ue

South

Afri

ca

Tanza

nia

Kenya

Uganda

8.00

Cost of Stay & Travel

6.007.00

5.004.003.002.00

0.001.00

Source: CyberMedia, Global Services, CBC

Figure 17: Costs of inputs in travel and stay

Infrastructure cost—telecom/data transfer ‘MDP’ cost

The Telecom/Data Transfer Cost major data parameters is based on the detailed data parameter for call charges (mobile/landline) to major world cities and the Internet/data transfer tariff per month. South Africa has the lowest telecom and data transfer cost and is topping the list of fi fteen African countries; it is followed closely by Egypt and Tunisia. Namibia, Tanzania, Uganda, Botswana, and Kenya have to improve the effi ciency of their telecom infrastructure in this sector to lower the cost.

Ready

Upcoming

Yet to be ready

South

Afri

ca

Moro

cco

Nigeria

Mau

ritiu

s

Ghana

Tanza

niaEgy

pt

Kenya

Uganda

Tunisia

Seneg

al

Zambia

Moza

mbiq

ue

Botswan

a

Namib

ia

8.009.00

Telecom/Data Transfer Cost

6.007.00

5.004.003.002.00

0.001.00

Source: CyberMedia, Global Services, CBC

Figure 18: Costs of inputs in terms of telecom/data transfer

•

•

02_Africa_Report09_FR.indd Sec1:1402_Africa_Report09_FR.indd Sec1:14 2/26/09 12:14:09 PM2/26/09 12:14:09 PM

1. Africa Situation Overview

15

OU

TS

OU

RC

IN

G

TO

A

FR

IC

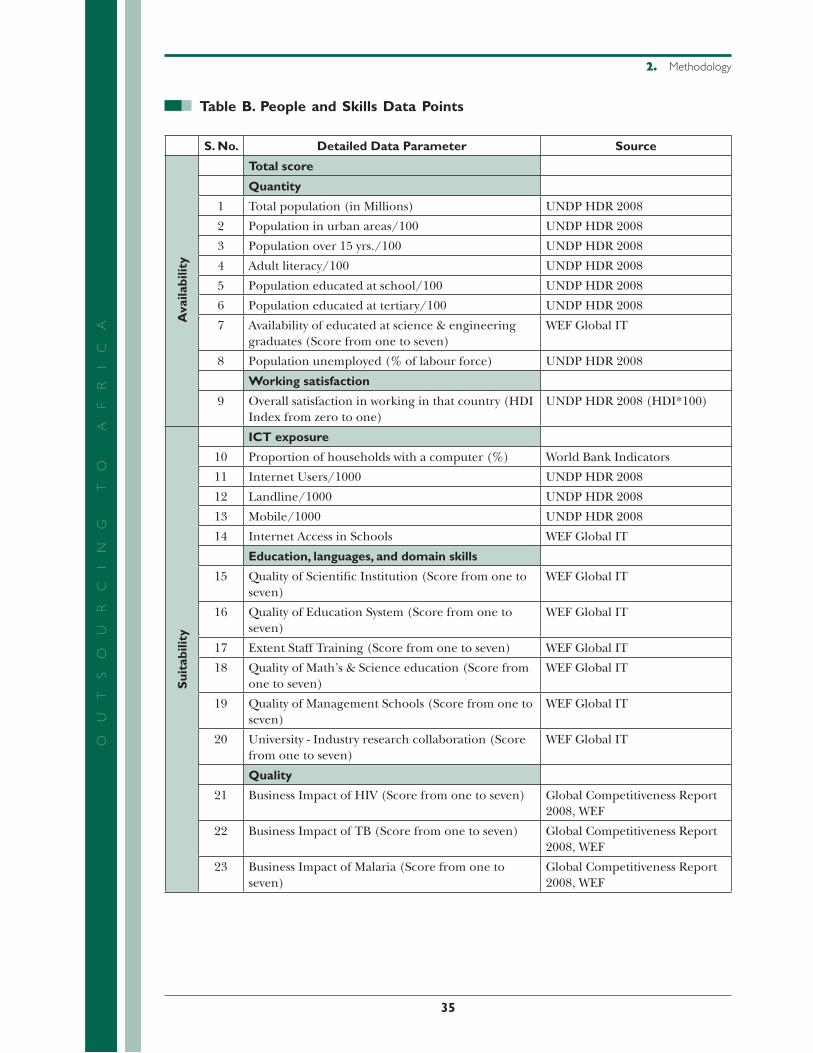

AB. People and Skills

This lower level abstraction covers the resources in terms of people and skills-set require-ments that go into an outsourcing engagement from the point of view of people and avail-able skill sets to successfully operate outsourcing operations. People and skills lower level abstraction score emerges from the construct scores related to availability, suitability and HR Costs and is based on the following MDP’s:

Quantity and Working Satisfaction.

Quality.

ICT Exposure and Education.

Language and Domain Skills.

Personnel Compensation and Cost of Living.

3.2153.1733.0092.9642.9482.9332.884

6789

101112131415

2.8792.8672.640

Ranks Country Score12345

3.6203.5433.4913.4473.385

BotswanaMoroccoKenyaUgandaTanzaniaNamibiaZambia

EgyptGhanaSouth AfricaTunisiaMauritius

NigeriaSenegalMozambique

Ready

Upcoming

Yet to be ready

Source: CyberMedia, Global Services, CBC

Figure 19: People and skills—ranking and scores

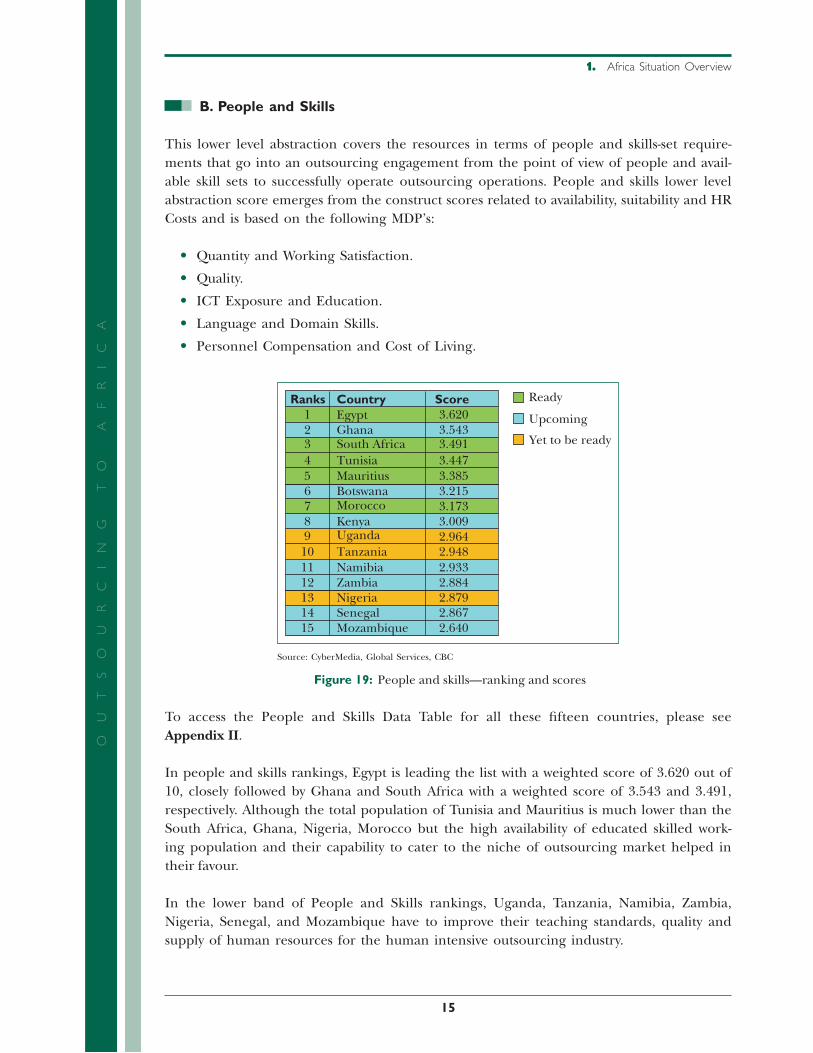

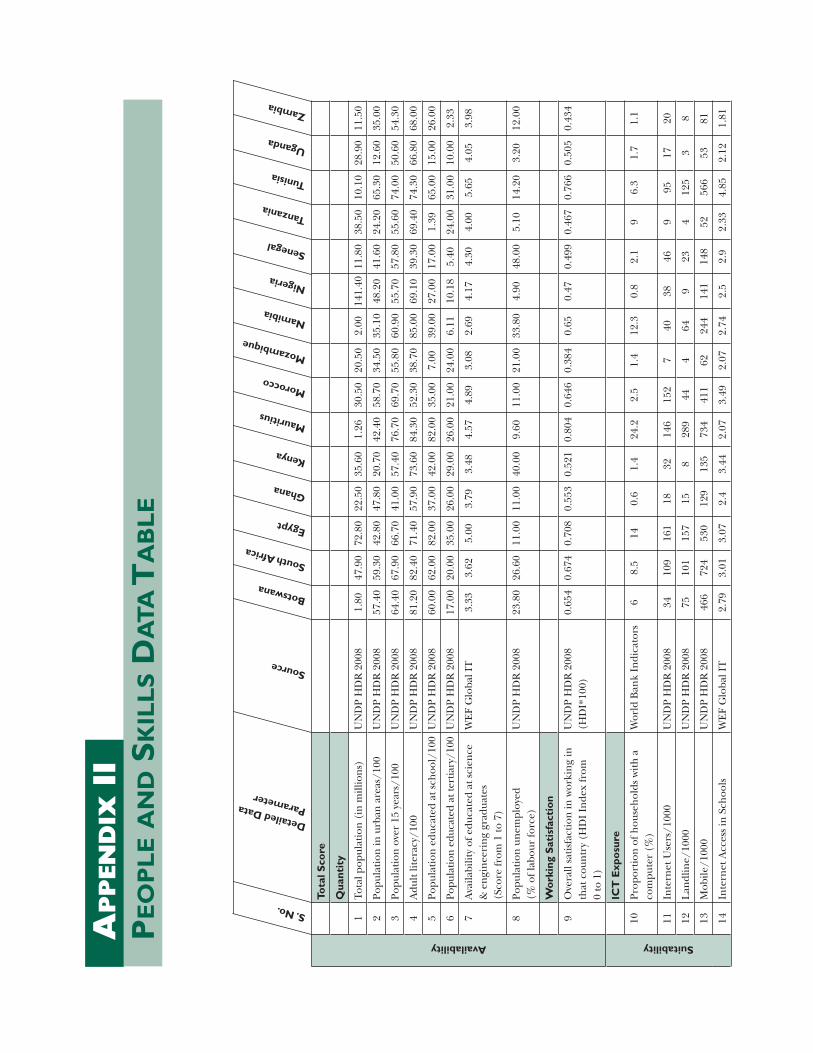

To access the People and Skills Data Table for all these fi fteen countries, please see Appendix II.

In people and skills rankings, Egypt is leading the list with a weighted score of 3.620 out of 10, closely followed by Ghana and South Africa with a weighted score of 3.543 and 3.491, respectively. Although the total population of Tunisia and Mauritius is much lower than the South Africa, Ghana, Nigeria, Morocco but the high availability of educated skilled work-ing population and their capability to cater to the niche of outsourcing market helped in their favour.

In the lower band of People and Skills rankings, Uganda, Tanzania, Namibia, Zambia, Nigeria, Senegal, and Mozambique have to improve their teaching standards, quality and supply of human resources for the human intensive outsourcing industry.

•

•

•

•

•

02_Africa_Report09_FR.indd Sec1:1502_Africa_Report09_FR.indd Sec1:15 2/26/09 12:14:10 PM2/26/09 12:14:10 PM

16

1. Africa Situation Overview

OU

TS

OU

RC

IN

G

TO

A

FR

IC

ABotswana, Morocco, Kenya, Uganda and Tanzania are in the mid ranks and can improve by improving the ICT exposure and by adopting better teaching standards suitable for out-sourcing industry.

To conclude, the variation in this lower level abstraction covering people and skills is not so great among all the fi fteen countries.

The contributing factors to these fi ndings are illustrated in the next section in graphs that show the scores achieved by each country in a given contributing parameter.

People and skills—availability

This construct gives a score that indicates the availability of human resources required for an outsourcing destination. The major data points are the quantity and working satisfaction in the country. Quantity is based on a number of detailed data parameters related to population, literacy, education levels, and unemployment rates.

The fi ndings for the fi fteen countries are shown as under.

People & Skills — Availability

Tuni

sia

Sout

h Af

rica

Moz

ambi

que

Gha

na

Keny

a

Mau

ritiu

s

Egyp

t

Botsw

ana

Sene

gal

Mor

occo

Zam

bia

Nig

eria

Nam

ibia

Tanz

ania

Uga

nda

Ready

1.4

1.2

1

0.8

0.6

0.4

0.2

0

Working Satisfaction Quantity

Upcoming Yet to be ready

Source: CyberMedia, Global Services, CBC

Figure 20: People and skills availability

It is interesting to observe that with diverse population fi gures from as low as 1.1 mil-lion to fi gures as high as 141 million all countries do contribute. The study has come up with tangible scores for all countries. The variation of the scores among the diverse countries is not so great. This shows that all fi fteen countries have potential, and our methodology caters for such a fair assessment in such diversity.

•

02_Africa_Report09_FR.indd Sec1:1602_Africa_Report09_FR.indd Sec1:16 2/26/09 12:14:10 PM2/26/09 12:14:10 PM

1. Africa Situation Overview

17

OU

TS

OU

RC

IN

G

TO

A

FR

IC

APeople and skills—suitability

The detailed data points relevant data from international sources as indicated in the methodology. The fi ndings for the fi fteen countries are shown as under.

Egypt

Mau

ritiu

s

South

Afri

ca

Tunisia

Moro

cco

Botswan

a

Ghana

Zambia

Namib

ia

Kenya

Seneg

al

Moza

mbiq

ue

Nigeria

Tanza

nia

Uganda

People & Skills—Suitability

ICT Exposure QualityEducation, Languages, and Domain skills

0.8

0.7

0.6

0.5

0.4

0.3

0.2

0.1

0

Ready Upcoming Yet to be ready

Source: CyberMedia, Global Services, CBC

Figure 21: People and skills suitability

This construct assesses the suitability of the human resources available in the country for outsourcing operations. The major data parameters include ICT exposure, educa-tion, language and domain skills, and quality.

The graph shows that there is a relatively large variation in ICT exposure among the different countries with the countries in the infrastructure ready and upcoming bands leading. In the case of education and quality all countries are comparable.

People and skills—human resource costs

This construct assesses the human resource cost factor in outsource operations and is based on scores for personnel compensation and the cost of living. The detailed data parameters used are from the UNDO local salary rates and cost of living index from World Bank World Development indicators. The fi ndings from the fi fteen countries are presented in the graph below. It is important to remember that a low score for the cost of living indicates an expensive country and similarly a high personal compensation score represents a lower salary rate. Thus Botswana, Ghana, and Tanzania are more competitive than South Africa or Tunisia.

•

•

02_Africa_Report09_FR.indd Sec1:1702_Africa_Report09_FR.indd Sec1:17 2/26/09 12:14:10 PM2/26/09 12:14:10 PM

18

1. Africa Situation Overview

OU

TS

OU

RC

IN

G

TO

A

FR

IC

APeople & Skills— HR Cost

HR Cost — Personal compensation1

0.8

0.6

0.4

0.2

0

Cost of living

Tuni

sia

Sout

h Af

rica

Mau

ritiu

s

Egyp

t

Mor

occo

Moz

ambi

que

Gha

na

Keny

a

Botsw

ana

Sene

gal

Zam

bia

Nam

ibia

Nig

eria

Tanz

ania

Uga

nda

Ready Upcoming Yet to be ready

Source: CyberMedia, Global Services, CBC

Figure 22: People and skills—HR costs

C. Business Environment

This lower-level abstraction covers a large number of factors that go into making a business operation successful in the country especially with reference to outsourcing. Factors like the economic outlook, corruption perception, rule of law, government policies related to outsourcing, tax policies, risk factors, and fi nancial aspects are considered in this data set.

3.3263.2613.0262.9762.9272.8132.781

6789

101112131415

2.7352.7132.711

Ranks Country Score12345

3.6953.5583.4863.4193.357

TunisiaMoroccoZambiaNamibiaSenegalKenyaGhana

MauritiusEgyptSouth AfricaNigeriaBotswana

TanzaniaUgandaMozambique

Ready

Upcoming

Yet to be ready

Source: CyberMedia, Global Services, CBC

Figure 23: Business environment—scores and ranking

The Business Environment lower-level abstraction score emerges from fi ve construct scores indicated:

02_Africa_Report09_FR.indd Sec1:1802_Africa_Report09_FR.indd Sec1:18 2/26/09 12:14:11 PM2/26/09 12:14:11 PM

1. Africa Situation Overview

19

OU

TS

OU

RC

IN

G

TO

A

FR

IC

ABusiness Environment Index.

ICT Industry Activeness.

Economic Outlook.

Risk Parameter.

Tax and Financial Incentives.

The detailed framework links the lower level abstraction with the constructs and major data points covered in Chapter 2 (Methodology).

To access the Business Environment Data Table for all the fi fteen countries, please see Appendix III.

In the business environment rankings, Mauritius is leading the list with weighted score of 3.695 for its business-positive environment. Egypt is at second position with a weighted score of 3.558; closely following is South Africa with weighted score of 3.486. Startlingly, the rank-ings of Tunisia and Morocco are trailing the list at sixth and seventh positions with weighted scores of 3.326 and 3.261, respectively.

The contributing factors to these fi ndings are illustrated in the next section in graphs that show the scores achieved by each country in a given contributing parameter.

Contributing Constructs and Major Data Points

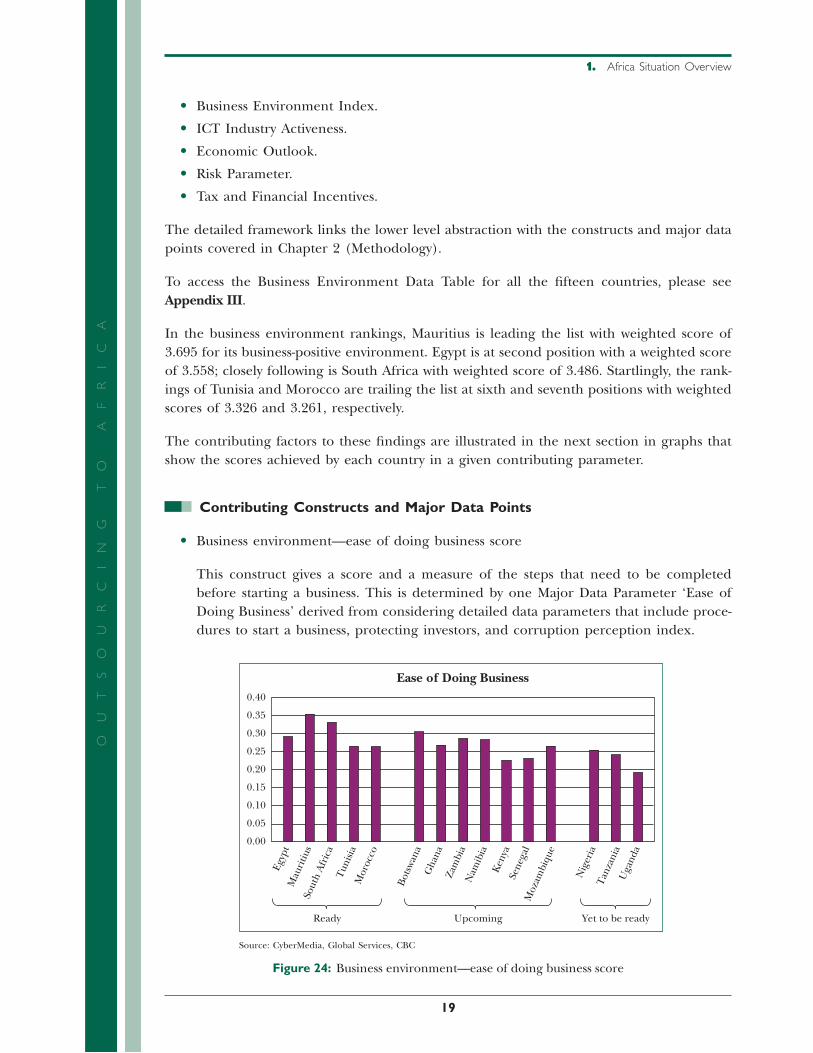

Business environment—ease of doing business score

This construct gives a score and a measure of the steps that need to be completed before starting a business. This is determined by one Major Data Parameter ‘Ease of Doing Business’ derived from considering detailed data parameters that include proce-dures to start a business, protecting investors, and corruption perception index.

Tun

isia

Sout

h A

fric

a

Moz

ambi

que

Gha

na

Ken

ya

Mau

ritiu

s

Egyp

t

Bots

wana

Sene

gal

Mor

occo

Zam

bia

Nig

eria

Nam

ibia

Tan

zani

aU

gand

a

Ready Upcoming Yet to be ready

0.40

0.35

0.30

0.25

0.20

0.15

0.10

0.05

0.00

Ease of Doing Business

Source: CyberMedia, Global Services, CBC

Figure 24: Business environment—ease of doing business score

•

•

•

•

•

•

02_Africa_Report09_FR.indd Sec1:1902_Africa_Report09_FR.indd Sec1:19 2/26/09 12:14:11 PM2/26/09 12:14:11 PM

20

1. Africa Situation Overview

OU

TS

OU

RC

IN

G

TO

A

FR

IC

AMauritius, South Africa, and Botswana are leading and are closely, followed by Egypt, though in practice Egypt is perhaps doing much better after the establishment of the General Authority for Investment and Free Zones (GAFI) as a true single window; in the case of outsourcing industry in Egypt, the Information Technology Industry Development Agency (ITIDA) supports the GAFI. The time and effort were found to have really improved as a result of this initiative. South Africa and Mauritius have simi-lar agencies in place working for the last few years, and once the Botswana Innovation Hub (BIH) is operational Botswana would improve further.

Business environment—ICT industry attractiveness score

The ICT industry attractiveness has been determined by the ICT Legislation and enforcement procedures in place and the magnitude of ICT in exports.

ICT Industry Attractiveness

0.450.4

0.350.3

0.250.2

0.150.1

0.050

Tuni

sia

Sout

h Af

rica

Mau

ritiu

s

Egyp

t

Moz

ambi

que

Gha

na

Keny

a

Botsw

ana

Sene

gal

Zam

bia

Nam

ibia

Nig

eria

Tanz

ania

Uga

nda

ICT Security; Cyber Laws and IPR Scores Expot & Share of ICT

Ready Upcoming Yet to be ready

Mor

occo

Source: CyberMedia, Global Services, CBC

Figure 25: Business environment—ICT industry attractiveness score

In ICT laws and its enforcement South Africa and Kenya lead (most banks do their back-offi ce processing there). Even Egypt, Botswana, Morocco, and Tunisia need to improve. Nigeria has a moderate score here, but this is a bit of a surprise as cyber crime literature reports that most cyber crime and related negative actions originate in Nigeria. Further, Nigeria has the highest score of ICT exports; however, it is in the Yet to be ready band. Perhaps this is due to the population of 141 million and several Nige-rians working abroad. It is a case of ‘Buddy Shopping’ like in the old days in India.

•

02_Africa_Report09_FR.indd Sec1:2002_Africa_Report09_FR.indd Sec1:20 2/26/09 12:14:11 PM2/26/09 12:14:11 PM

1. Africa Situation Overview

21

OU

TS

OU

RC

IN

G

TO

A

FR

IC

ABusiness environment—economic outlook score

This is based on economic and trade parameters.

Tuni

sia

Sout

h Af

rica

Moz

ambi

que

Gha

na

Keny

a

Mau

ritiu

s

Egyp

t

Botsw

ana

Sene

gal

Mor

occo

Zam

bia

Nig

eria

Nam

ibia

Tanz

ania

Uga

nda

Ready Upcoming Yet to be ready

0.400.350.300.250.200.150.100.050.00

Economic OutlookShare of Services in GDP, Economy Size and Growth, InflationShare of Exports, Share of Services in ExportsCountry Forex Reserves

Source: CyberMedia, Global Services, CBC

Figure 26: Business Environment—economic outlook score

As per the report, South Africa, Mauritius, and Botswana lead with Egypt and Tunisia following close behind.

Business environment—risk parameter score

This factor is determined from the perceived risk in the country from geopolitical, currency fl uctuation, and legislative risk.

Business Environment—Risk Parameter

0.600.500.400.300.200.100.00

Tuni

sia

Sout

h Af

rica

Mau

ritiu

s

Egyp

t

Mor

occo

Moz

ambi

que

Gha

na

Keny

a

Botsw

ana

Sene

gal

Zam

bia

Nam

ibia

Nig

eria

Tanz

ania

Uga

nda

Geo-Political Risk Currecy Risk Legislative Risk

Ready Upcoming Yet to be ready

Source: CyberMedia, Global Services, CBC

Figure 27: Business environment—risk parameter score

•

•

02_Africa_Report09_FR.indd Sec1:2102_Africa_Report09_FR.indd Sec1:21 2/26/09 12:14:11 PM2/26/09 12:14:11 PM

22

1. Africa Situation Overview

OU

TS

OU

RC

IN

G

TO

A

FR

IC

AEgypt, Tunisia, and Morocco lead with the least risk in all three factors followed by South Africa and Botswana in all aspects except the currency risk where South Africa, Botswana, and Namibia (all ties to the rand basket) are the worst in Africa.

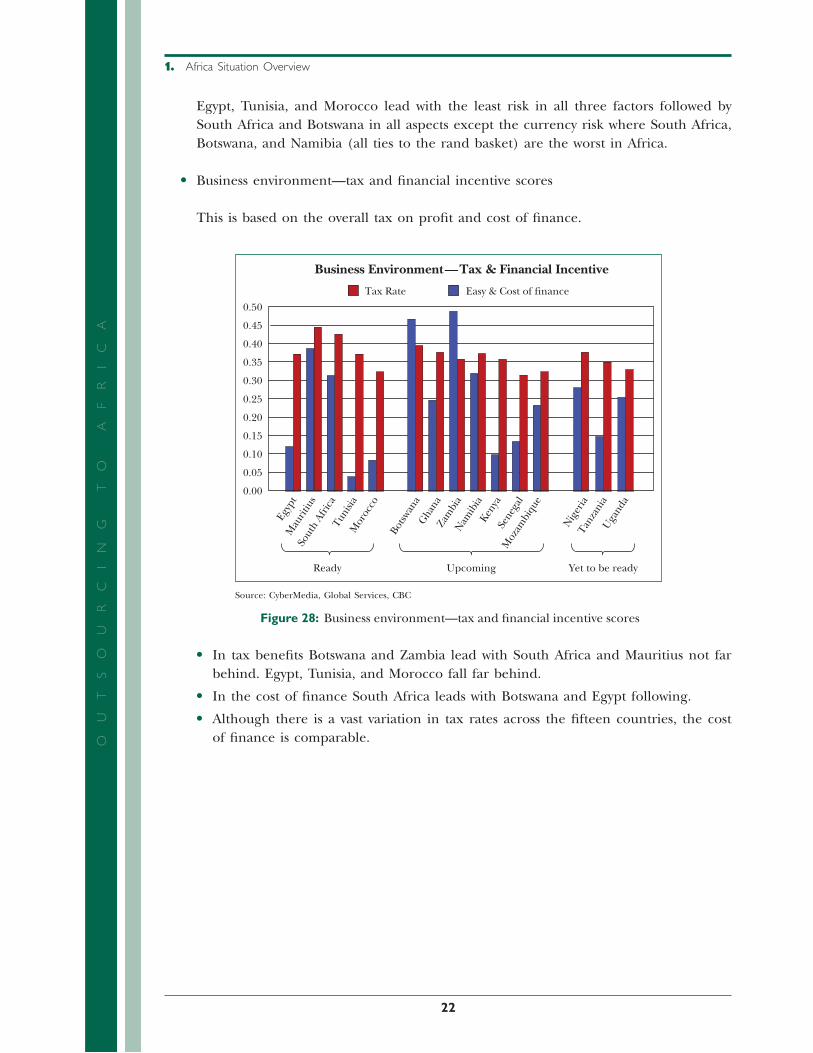

Business environment—tax and fi nancial incentive scores

This is based on the overall tax on profi t and cost of fi nance.

Business Environment—Tax & Financial Incentive

0.35

0.50

0.45

0.40

0.30

0.25

0.20

0.15

0.10

0.00

0.05

Tuni

sia

Sout

h Af

rica

Mau

ritiu

s

Egyp

t

Mor

occo

Moz

ambi

que

Gha

na

Keny

a

Botsw

ana

Sene

gal

Zam

bia

Nam

ibia

Nig

eria

Tanz

ania

Uga

nda

Tax Rate Easy & Cost of finance

Ready Upcoming Yet to be ready

Source: CyberMedia, Global Services, CBC

Figure 28: Business environment—tax and fi nancial incentive scores

In tax benefi ts Botswana and Zambia lead with South Africa and Mauritius not far behind. Egypt, Tunisia, and Morocco fall far behind.

In the cost of fi nance South Africa leads with Botswana and Egypt following.

Although there is a vast variation in tax rates across the fi fteen countries, the cost of fi nance is comparable.

•

•

•

•

02_Africa_Report09_FR.indd Sec1:2202_Africa_Report09_FR.indd Sec1:22 2/26/09 12:14:12 PM2/26/09 12:14:12 PM

23

OU

TS

OU

RC

IN

G

TO

A

FR

IC

A

2. METHODOLOGY

This part of the report describes the research methodology followed

2.1. Geographical Coverage

In this report, fi fteen African nations shown in the following map have been covered.

Morocco *Tunisia *

Egypt *

Senegal *

Ghana Nigeria

UgandaKenya

Tanzania

ZambiaMozambique

BotswanaNamibia

SouthAfrica

MauritiusAfrica

*Non-Commonwealth Countries

Source: CyberMedia, Global Services, CBC

Figure 29: Geographical coverage

02_Africa_Report09_FR.indd Sec1:2302_Africa_Report09_FR.indd Sec1:23 2/26/09 12:14:12 PM2/26/09 12:14:12 PM

24

OU

TS

OU

RC

IN

G

TO

A

FR

IC

A2.2. Research Framework and Design

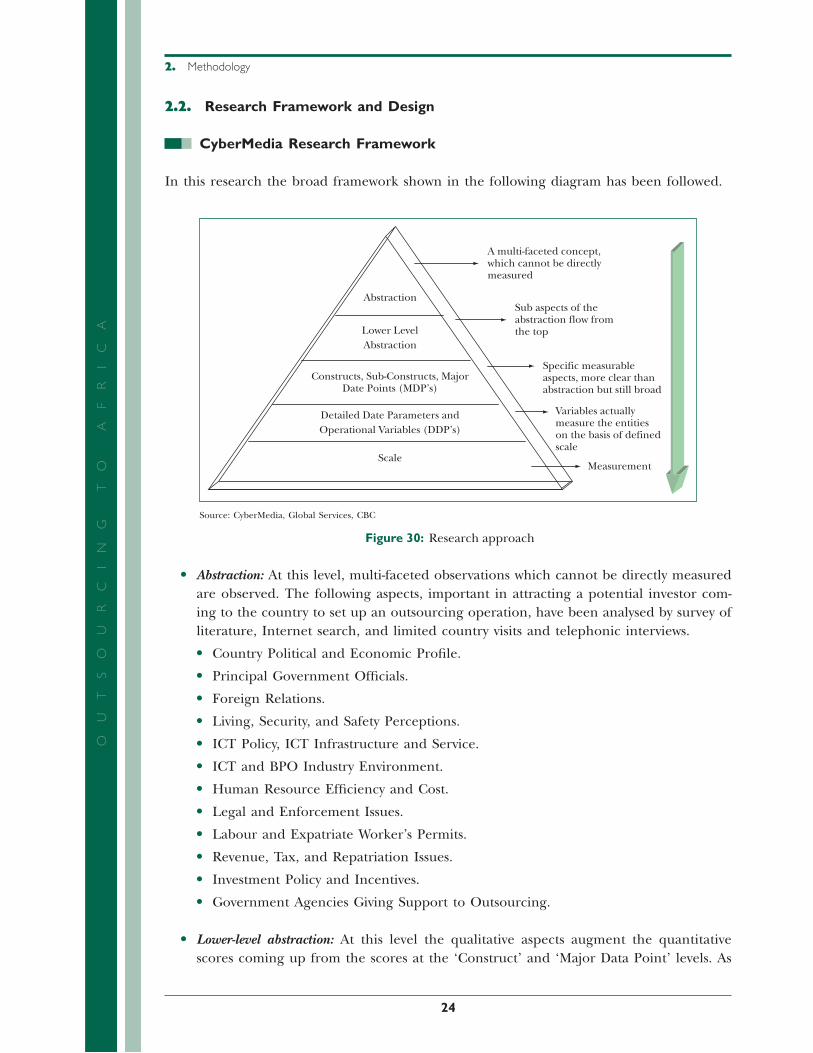

CyberMedia Research Framework

In this research the broad framework shown in the following diagram has been followed.

A multi-faceted concept,which cannot be directlymeasured

Sub aspects of theabstraction flow fromthe top

Specific measurableaspects, more clear thanabstraction but still broad

Variables actuallymeasure the entitieson the basis of definedscale

MeasurementScale

Lower LevelAbstraction

Detailed Date Parameters andOperational Variables (DDP’s)

Constructs, Sub-Constructs, MajorDate Points (MDP’s)

Abstraction

Source: CyberMedia, Global Services, CBC

Figure 30: Research approach

Abstraction: At this level, multi-faceted observations which cannot be directly measured are observed. The following aspects, important in attracting a potential investor com-ing to the country to set up an outsourcing operation, have been analysed by survey of literature, Internet search, and limited country visits and telephonic interviews.

Country Political and Economic Profi le.

Principal Government Offi cials.

Foreign Relations.

Living, Security, and Safety Perceptions.

ICT Policy, ICT Infrastructure and Service.

ICT and BPO Industry Environment.

Human Resource Effi ciency and Cost.

Legal and Enforcement Issues.

Labour and Expatriate Worker’s Permits.

Revenue, Tax, and Repatriation Issues.

Investment Policy and Incentives.

Government Agencies Giving Support to Outsourcing.

Lower-level abstraction: At this level the qualitative aspects augment the quantitative scores coming up from the scores at the ‘Construct’ and ‘Major Data Point’ levels. As

•

•

•

•

•

•

•

•

•

•

•

•

•

•

2. Methodology

02_Africa_Report09_FR.indd Sec1:2402_Africa_Report09_FR.indd Sec1:24 2/26/09 12:14:12 PM2/26/09 12:14:12 PM

25

OU

TS

OU

RC

IN

G

TO

A

FR

IC

Athe scores have to be added in a weighted sum depending on the relative importance of each data point, a careful normalisation and calculation method has been evolved. The weightage is defi ned in detailed research framework charts. These are explained in the next sections.

Constructs: These are specifi c and more measurable aspects, broad but clearer, than the lower level abstraction. The construct scores are derived by a weighted sum of ‘Major Data Points’. The principles are the same as indicated for lower level abstracts.

Major data points: These are more specifi c and more measurable aspects. The ‘Major Data Points’ scores are derived by the average of all the ‘Detailed Data Points’ allotted to that ‘Major Data Point’. The principles are the same as indicated for lower level abstracts.

Detailed data points: These are variables actually measured on the basis of unit and skill. In this research, such data has been collected from reliable internationally recognised and published reports. The data that has been used is in two forms:

Rating Scores representing the result of any extensive survey and study conducted by a recognised board like World Economic Forum’s Global Information Technology Report or Global Competitiveness Report, the United Nations Human Developments Reports. Such scores are in a skill of one to ten, one to seven, or zero to one.

Absolute values of data like number of procedures to start a business, total tax as a percentage of profi t (World Bank doing Business Report or International Internet Bandwidth [Bits per person]).

2.3. Normalization and Calculation

Normalization

All the scores need to be added, averaged, or proportionately averaged; thus normalisation is necessary. Thus scores for the ‘Detailed Data Points’ are determined as follows:

All rating scores in the range of zero to one, one to seven, or one to ten are normalised proportionately to a range of one to ten across all the data. All scores used further are thus in the range of one to ten before the weightage specifi ed in the detailed frame-work are applied.

All data in the form of absolute values are normalised to a score by using the follow-ing formulae

Score = Score = 1+ ((LOG10 (Actual Value)-LOG10 (Min Value))/(LOG10 (Max Value)-LOG10 (Min Value)))*9

Calculation

The calculations are done as follows:

‘Lower Level Abstract’ Score = Weighted Average of contributing ‘Constructs’ Scores.

‘Construct’ Scores = Weighted Average of contributing ‘Major Data Point’ Scores.

•

•

•

•

•

•

•

•

•

2. Methodology

02_Africa_Report09_FR.indd Sec1:2502_Africa_Report09_FR.indd Sec1:25 2/26/09 12:14:13 PM2/26/09 12:14:13 PM

26

OU

TS

OU

RC

IN

G

TO

A

FR

IC

A‘Major Data Point’ Scores = Average of contributing ‘Detailed Data Point’ Scores.

‘Detailed Data Point’ Score = the normalised value of the score as per the rule and formulae given above.

The overall ‘Outsourcing Attractiveness Index’ is determined by the following method:

People and Skills(50%)

BusinessEnvironment (50%)

OutsourcingAttractivenessRank

Lower Level Abstraction

Detailed Framework

Source: CyberMedia, Global Services, CBC

Figure 31: Detailed framework—outsourcing attractiveness

Outsourcing Attractiveness Index

Countries are ranked within their bands based on theirBE + People & Skill Scores

Countries are ranked within their bands based on their:

People & Skills Scores

plus

Business Environment Scores

Source: CyberMedia, Global Services, CBC

Figure 32: Components leading to outsourcing attractiveness

A. Infrastructure Bands

The ‘Infrastructure’ lower level abstraction score is calculated as per the detailed frame-work and the normalisation and calculation method indicated above.

The countries with an infrastructure score greater than 6.5 are placed in the ‘Ready’ band.

•

•

•

•

2. Methodology

02_Africa_Report09_FR.indd Sec1:2602_Africa_Report09_FR.indd Sec1:26 2/26/09 12:14:13 PM2/26/09 12:14:13 PM

27

OU

TS

OU

RC

IN

G

TO

A

FR

IC

AThe countries with an infrastructure score between 5.5 and 6.5 are placed in the ‘Upcoming’ band.

The countries with an infrastructure score less than 5.5 are placed in the ‘Yet to be ready’ band.

B. People & Skills and Business Environment Scores

The ‘People and Skills’ lower level abstraction score is calculated as per the detailed framework and the normalisation and calculation method indicated above.

The ‘Business Environment’ lower level abstraction score is calculated as per the detailed framework and the normalisation and calculation method indicated above.

C. Overall Outsourcing Attractiveness Scores and Ranks

The ‘Outsourcing Attractiveness’ score of the country is determined for countries in each band. This is the sum of the ‘People and Skills’ score and ‘Business Environment’ score.

The rankings are made in each band using this total score.

The following diagram shows this approach graphically.

The Approach

Political Economic Social Technology People

✓Attractiveness in terms of Outsourcing✓Characteristics of a country

Skill-sets

Business Environment People & Skills

Ready/UpcomingYet to be Ready

Infrastructure

Source: CyberMedia, Global Services, CBC

Figure 33: Detailed framework—outsourcing attractiveness

•

•

•

•

•

•

2. Methodology

02_Africa_Report09_FR.indd Sec1:2702_Africa_Report09_FR.indd Sec1:27 2/26/09 12:14:13 PM2/26/09 12:14:13 PM

28

OU

TS

OU

RC

IN

G

TO

A

FR

IC

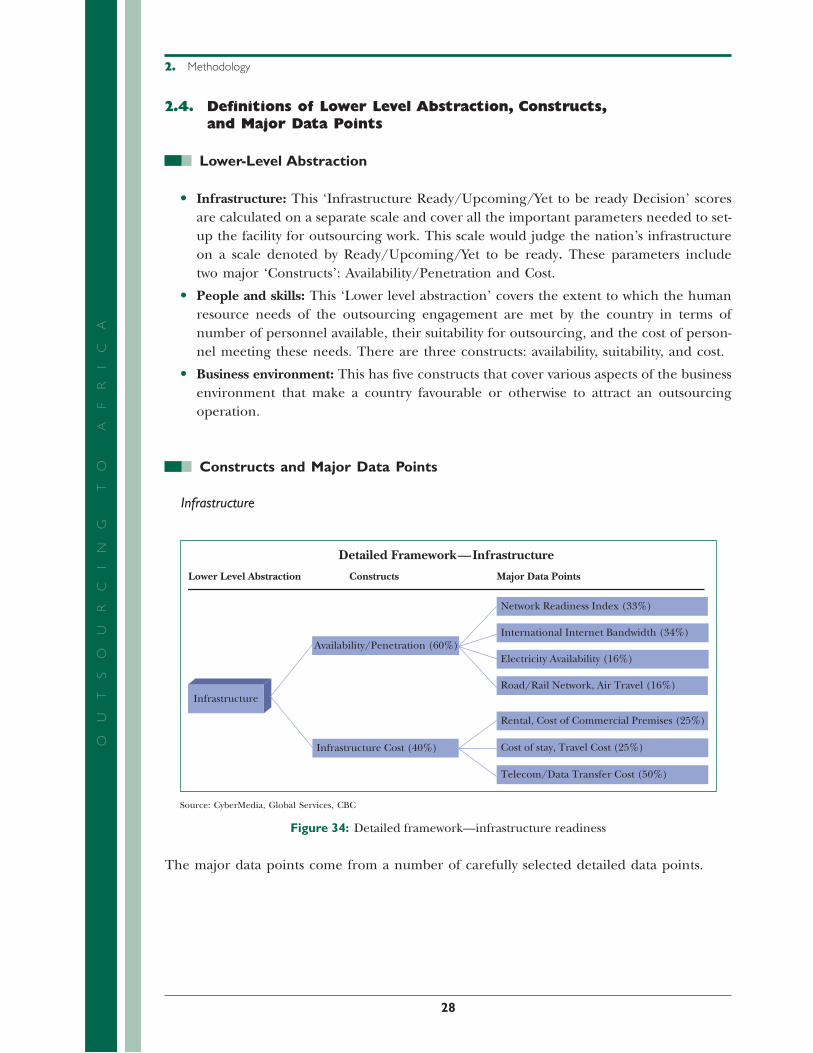

A2.4. Defi nitions of Lower Level Abstraction, Constructs,

and Major Data Points

Lower-Level Abstraction

Infrastructure: This ‘Infrastructure Ready/Upcoming/Yet to be ready Decision’ scores are calculated on a separate scale and cover all the important parameters needed to set-up the facility for outsourcing work. This scale would judge the nation’s infrastructure on a scale denoted by Ready/Upcoming/Yet to be ready. These parameters include two major ‘Constructs’: Availability/Penetration and Cost.

People and skills: This ‘Lower level abstraction’ covers the extent to which the human resource needs of the outsourcing engagement are met by the country in terms of number of personnel available, their suitability for outsourcing, and the cost of person-nel meeting these needs. There are three constructs: availability, suitability, and cost.

Business environment: This has fi ve constructs that cover various aspects of the business environment that make a country favourable or otherwise to attract an outsourcing operation.

Constructs and Major Data Points

Infrastructure

Infrastructure

Infrastructure Cost (40%)

Availability/Penetration (60%)

Lower Level Abstraction Constructs

Detailed Framework—Infrastructure

Major Data Points

Network Readiness Index (33%)

International Internet Bandwidth (34%)

Electricity Availability (16%)

Road/Rail Network, Air Travel (16%)

Rental, Cost of Commercial Premises (25%)

Cost of stay, Travel Cost (25%)

Telecom/Data Transfer Cost (50%)

Source: CyberMedia, Global Services, CBC

Figure 34: Detailed framework—infrastructure readiness

The major data points come from a number of carefully selected detailed data points.

•

•

•

2. Methodology

02_Africa_Report09_FR.indd Sec1:2802_Africa_Report09_FR.indd Sec1:28 2/26/09 12:14:13 PM2/26/09 12:14:13 PM

29

OU

TS

OU

RC

IN

G

TO

A

FR

IC

AInfrastructure—availability/penetration: This ‘Construct’ gives a score that covers the penetration of IT communication network by using the ‘Network Readiness Index’, and availability of other resources like Internet bandwidth, electricity, commercial space, railways, and air travel; the four ‘Major Data Points’ are as follows:

Network readiness index: This ‘Major Data Point’ is based on a report produced by the World Economic Forum in cooperation with INSEAD, published for the seventh consecutive year with record coverage of 127 economies worldwide, the report has become the world’s most comprehensive and authoritative international assessment of the impact of ICT on the development process and the competitiveness of nations. This index is a standard measure of the availability and penetration of ICT infra-structure in a country. This is updated annually. In this case no separate detailed data parameters will be considered as this ‘Network Readiness Index’ will be taken as it is (33 per cent weightage).

International Internet bandwidth: This ‘Major Data Point’ is based on World Develop-ment Indicators produced by the World Bank. This is indication of availability of Inter-national Internet Bandwidth in mbps in each country (34 per cent weightage).

Electricity availability: This ‘Major Data Point’ is based on ‘Detailed Data Parameters’ like electricity production, consumption and import. (5 per cent weightage).

Road/Rail/Air travel: This ‘Major Data Point’ is based on few ‘Detailed Data Param-eters’ like number of major railway stations, length of rail network (in km), length of road network (in km); number of major airports, connectivity with major cities of the world, frequency of fl ights, etc. (16 per cent weightage).

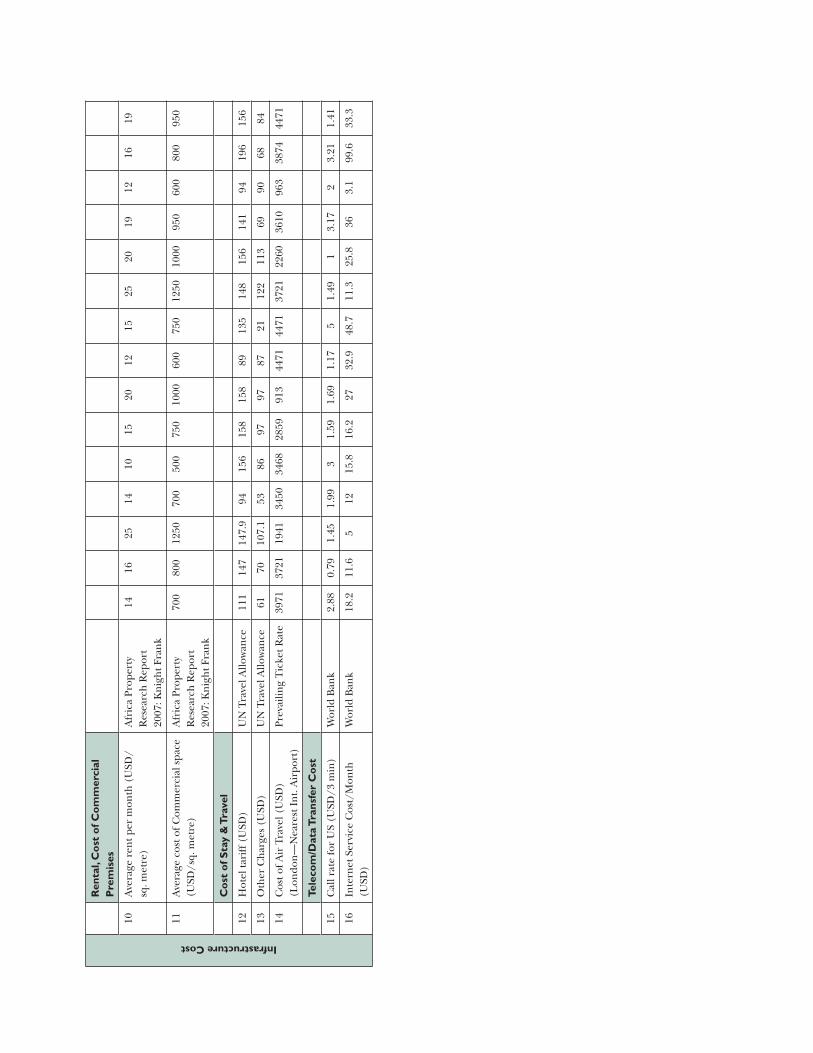

Infrastructure cost (40 per cent weightage): This ‘Construct’ will give us a score that includes the entire infrastructure cost incurred by business to acquire infrastructure resources, i.e., Communication, Electricity, Transportation, Railways, Air-Travel, etc. The three ‘major data points’ are as follows:

Rental and cost commercial premises: This ‘major data point’ is based on ‘Detailed Data Parameters’ that is used in calculating overall cost of rental (per sq. ft.) and cost of ownership of premises for commercial activity (25 per cent weightage).

Cost of stay and travel: This ‘Major Data Point’ is based on ‘Detailed Data Parameters’ that helps calculating the cost of stay for the expatriate executive; it includes board and lodging charges and travel costs to major countries where the outsourcing market exists (25 per cent weightage).

Telecom/Internet service cost: This ‘Major Data Point’ is based on ‘Detailed Data Parameters’ like call charges (mobile/landline) to major world cities, Internet/data transfer tariff per month, etc. (50 per cent weightage).

•

•

•

•

•

•

•

•

•

2. Methodology

02_Africa_Report09_FR.indd Sec1:2902_Africa_Report09_FR.indd Sec1:29 2/26/09 12:14:14 PM2/26/09 12:14:14 PM

30

OU

TS

OU

RC

IN

G

TO

A

FR

IC

APeople and Skills

H R Cost (30%)

People and Skills

Availability (40%)

Suitability (30%)

Quantity (75%)

Working Satisfaction (25%)

ICT Exposure (53%)

Education, Languages, and Domain Skills (33%)

Quality (14%)

Personnel Compensation at Various Levels (66%)

Cost of Living (34%)

Detailed Framework—People and Skills

Lower Level Abstraction Constructs Major Data Points

Source: CyberMedia, Global Services, CBC

Figure 35: Detailed framework—merit of people and skills

People and skills—availability: This ‘Construct’ gives a score that gives us an idea of the quantity of personnel available along with the attrition rates of available person-nel leaving; this will give a score to assess the availability of personnel in the country. (40 per cent weightage). The two ‘Major Data Points’ thus are as follows:

Quantity: This ‘Major Data Point’ is based on a number of ‘detailed data parameters’ like population, education, qualifi ed personnel available, ease of meeting shortfalls by expatriate employment, unemployment rate, and so on (75 per cent weightage).

Working satisfaction: This major data point is derived from the UNDP human develp-ment report 2008. This HDI Index, a number from 0 to 1, indicates the overall satisfaction in working in that country. (See Table B of section 2.5, S. No. 9 to understand it better.)

People and skills suitability: This ‘Construct’ gives a score that gives us an idea of the compatibility of personnel to the outsourcing work, based on quality of personnel, their language skills, and exposure to the cultures of other countries that are the outsourced service markets, (30 per cent weightage). The four ‘Major Data Points’ are as follows:

ICT exposure: This ‘Major Data Point’ will give an idea of the familiarity that the people or the available work force has to ICT. Detailed data parameters like density of PCs, mobile phones, Internet, etc., among the people will be used to assess this factor (53 per cent weightage).

Education, languages, and domain skills: This ‘Major Data Point’ is based on a few ‘detailed data parameters’ like knowledge of European languages, management, and ICT/domain skills relevant to outsourcing operations. The level of accreditation

•

•

•

•

•

•

2. Methodology

02_Africa_Report09_FR.indd Sec1:3002_Africa_Report09_FR.indd Sec1:30 2/26/09 12:14:14 PM2/26/09 12:14:14 PM

31

OU

TS

OU

RC

IN

G

TO

A

FR

IC

Aof these skills and qualifi cations to international standards will also be considered (33 per cent weightage).

Quality: This ‘Major Data Point’ is based on a few ‘detailed data parameters’ like the attitude of people towards work, health conditions affecting effi cient operations, and related issues (14 per cent weightage).

People and skills—HR cost: This ‘Construct’ gives a score that gives us an idea of the cost of personnel doing the outsourcing work (30 per cent weightage). The two ‘Major Data Points’ are as follows:

Compensation at various levels: This ‘Major Data Point’ is based on a few ‘detailed data parameters’ like the cost of a fresh graduate, cost of a professional with fi ve years’ experience, average cost of all other personnel, and related parameters (66 per cent weightage).

Consumer price index: This ‘Major Data Point’ is based on a few ‘detailed data parameters’ like the cost of living index, cost of medical insurance, cost of children’s education, and similar factors (34 per cent weightage).

Business Environment

BusinessEnvironment

Business Environment Index (10%)

ICT Industry Attractiveness (20%)

Economic Outlook (20%)

Risk Parameter (30%)

Tax & Financial Incentives (20%)

Lower Level Abstraction Constructs

Detailed Framework–Business Environment

Source: CyberMedia, Global Services, CBC

Figure 36: Detailed framework—merit of business environment

•

•

•

•

2. Methodology

02_Africa_Report09_FR.indd Sec1:3102_Africa_Report09_FR.indd Sec1:31 2/26/09 12:14:14 PM2/26/09 12:14:14 PM

32

OU

TS

OU

RC

IN

G

TO

A

FR

IC

A

ICT IndustryAttractiveness (20%)

Economic Outlook(20%)

Business EnvironmentIndex (10%)

Ease of Doing Business (100%)

ICT Security, Cyber Laws ans IPR (66%)

Exports and Share of ICT (34%)

Share of Services in GDP, Size and Growth, Inflation (40%)

Share of Exports, Share of Services in Exports (40%)

Foreign Exchange/Gold Reserves (20%)

Constructs Major Data Points

Detailed Framework—Business Environment

Source: CyberMedia, Global Services, CBC

Figure 37: Detailed framework—components of business environment

Risk Parameter (30%)

Tax & Financial Incentive (20%)

Geopolitical Risk (33%)

Currency Risk (33%)

Legislative Risk (34%)

Tax Rate (50%)

Ease & Cost of Finance (50%)

Constructs Major Data Points

Detailed Framework—Business Environment

Source: CyberMedia, Global Services, CBC

Figure 38: Detailed framework—components of business environment

Business Environment—business environment index: This ‘Construct’ will give us a score that covers all the important parameters needed for positive business environ-ment of a nation. This data will be taken from the World Bank ‘Ease of Doing Business’ research that examines a number of factors like starting a business, licences, employing workers, property, taxes, credit, protecting investors, enforcing contracts, trading across borders, and closing a business (10 per cent weightage).

Business Environment—ICT industry attractiveness: This ‘Construct’ will give us a score that covers all the important parameters needed for ICT Industry Attractiveness of a nation (20per cent weightage). It includes the following ‘Major Data Points’:

•

•

2. Methodology

02_Africa_Report09_FR.indd Sec1:3202_Africa_Report09_FR.indd Sec1:32 2/26/09 12:14:14 PM2/26/09 12:14:14 PM

33

OU

TS

OU

RC

IN

G

TO

A

FR

IC

ASecurity/IPR law: This ‘major data point’ will be based on ‘Detailed Data Param-eters’ like IPR laws, Cyber laws, etc. (66 per cent weightage).

Export and share of ICT industry: This ‘major data point’ will be based on ‘Detailed Data Parameters’ that helps us estimate the ICT industry size of a nation. It will also cover factors like total export/import of services, telecommunication revenue, etc. (34 per cent weightage).

Business Environment—economic outlook: This ‘Construct’ will give us a score that covers all the important parameters needed to defi ne Economic Outlook of a nation (20 per cent weightage). It includes the following ‘Major Data Points’:

Percentage of services of GDP, size and growth and infl ation: This ‘Major Data Point’ will be based on ‘Detailed Data Parameters’ like Total GDP, percentage of share of Services, increase of GDP, and Economic Growth, Infl ation of a nation (40 per cent weightage).

Percentage share of exports and share of services: This ‘major data point’ is based on ‘Detailed Data Parameters’ like percentage of Exports in overall economy of a nation (40 per cent weightage).

Foreign exchange/gold reserves: This ‘major data point’ is based on ‘Detailed Data Parameters’ like foreign exchange/gold reserves of a nation, etc. (20 per cent weightage).

Business Environment—risk parameters: This ‘Construct’ gives us a score that cov-ers all the important risk parameters needed to defi ne the risk to operate a business (30 per cent weightage). It includes the following ‘Major Data Points’:

Geo-political risk: Political risk, also known as ‘geopolitical risk’—the risk that an investment’s returns could suffer as a result of political changes or instability in a country. This ‘major data point’ is based on instability affecting investment returns could stem from a ‘Detailed Data Parameters’ like change in government, other foreign policy makers, or military control, factors in enforcement of contracts, etc. (33 per cent weightage).