Embed Size (px)

Citation preview

Minimizing Your Tax Obligations

401(k)tax benefits

Contribution Limits

Under 50 years of age$18,000

Over 50 years of age$18,000Plus Catch up contribution up to $6,000

Salary deferral plus employer contribution is limited to $53,000

Traditional Pre-Tax ContributionsContributions withheld from pay before tax

Gains are tax deferred while in the plan

Distributions taxed as ordinary income

Up to $4,500 annual tax savings prior to age 50 and $6,000 for 50 or older*

*Based upon a 25% tax rate

$20 Pre-tax Contribution

Costs $15 in take home pay

Roth Contributions

Contributions withheld from pay after tax

Gains are tax deferred while in the plan

Distributions are tax free after 59 ½ and 5 years after initial Roth Contribution

Roth in 401k avoids IRA income limitations

Pre-tax vs Roth

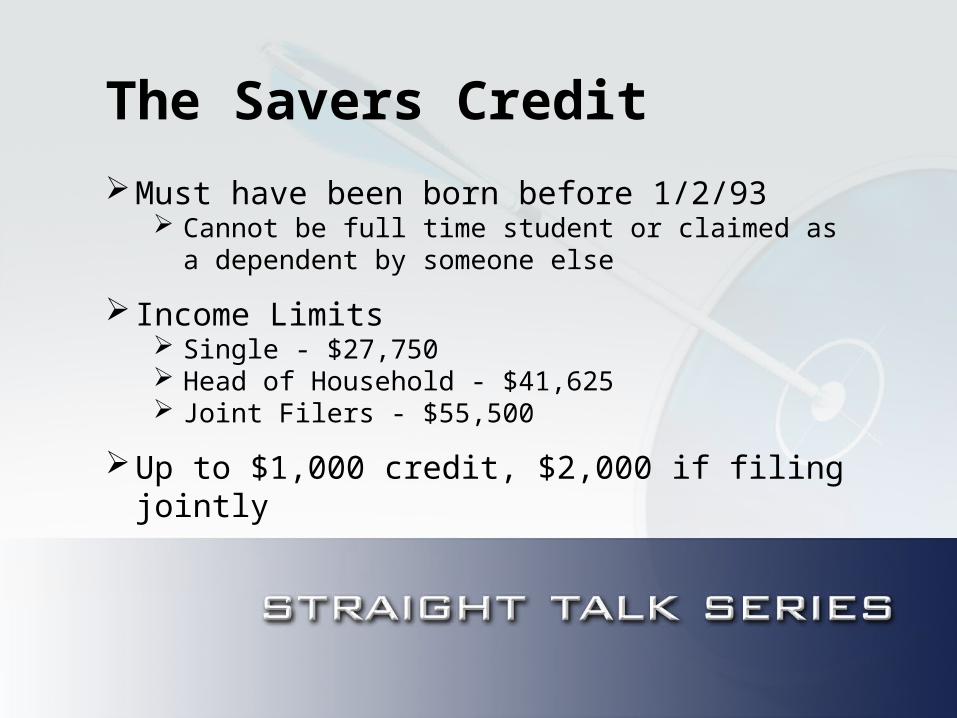

The Savers Credit

Must have been born before 1/2/93 Cannot be full time student or claimed as a

dependent by someone else

Income Limits Single - $27,750 Head of Household - $41,625 Joint Filers - $55,500

Up to $1,000 credit, $2,000 if filing jointly

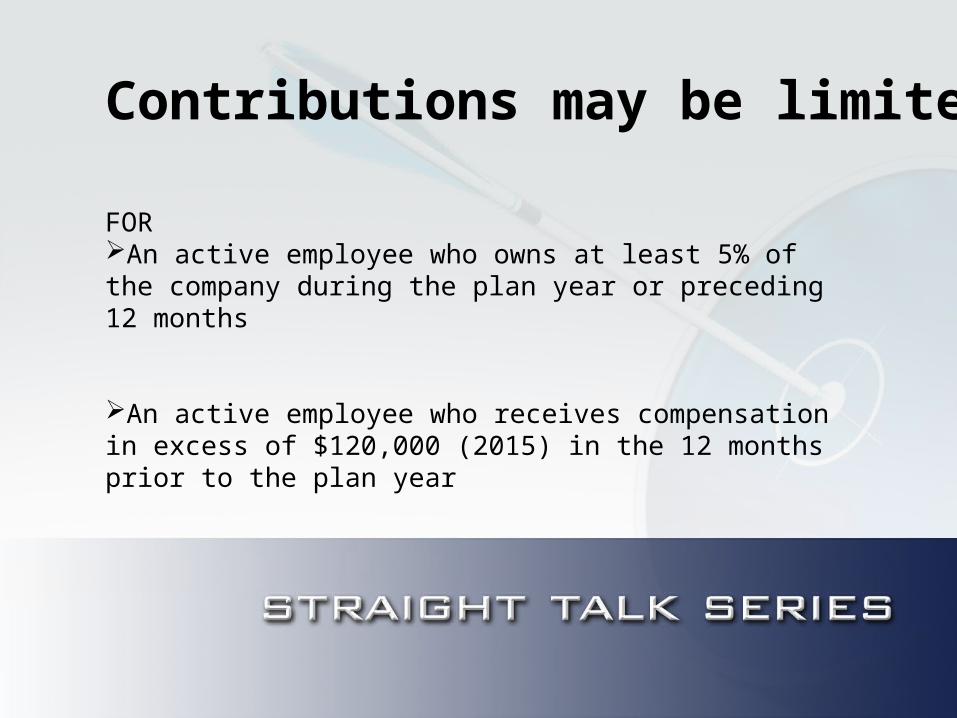

Contributions may be limited

FORAn active employee who owns at least 5% of the company during the plan year or preceding 12 months

An active employee who receives compensation in excess of $120,000 (2015) in the 12 months prior to the plan year

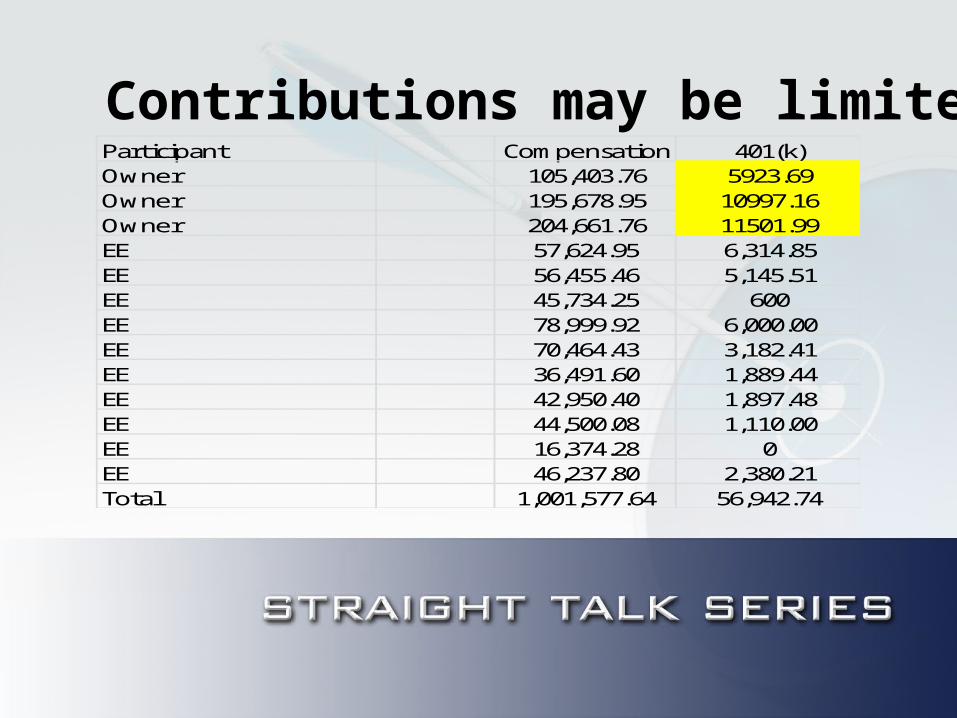

Contributions may be limitedParticipant Compensation 401(k)Owner 105,403.76 5923.69Owner 195,678.95 10997.16Owner 204,661.76 11501.99EE 57,624.95 6,314.85EE 56,455.46 5,145.51EE 45,734.25 600EE 78,999.92 6,000.00EE 70,464.43 3,182.41EE 36,491.60 1,889.44EE 42,950.40 1,897.48EE 44,500.08 1,110.00EE 16,374.28 0EE 46,237.80 2,380.21Total 1,001,577.64 56,942.74

Increasing Contributions

Education works – long term commitment required

Matching contributions have a direct impact

Automatic Enrollment

Safe Harbor Plans

Safe Harbor Plans

Avoid ADP/ACP testing requirement

HCEs may contribute full 401k dollar amount ($18,000 in 2015)

May satisfy top heavy minimum requirements

Safe Harbor Plans

Required employer contributions

Matching contribution - $1 for $1 on the first 3% of pay and $0.50 for $1 on the next 2% of pay

OR

3% contribution to all employees who have met the plan’s eligibility requirement

Safe Harbor Plans

Additional requirement

Safe Harbor contributions must be 100% vested

Employees must receive a Safe Harbor notice 30 days before the beginning of the plan year

Plan document must reflect Safe Harbor election

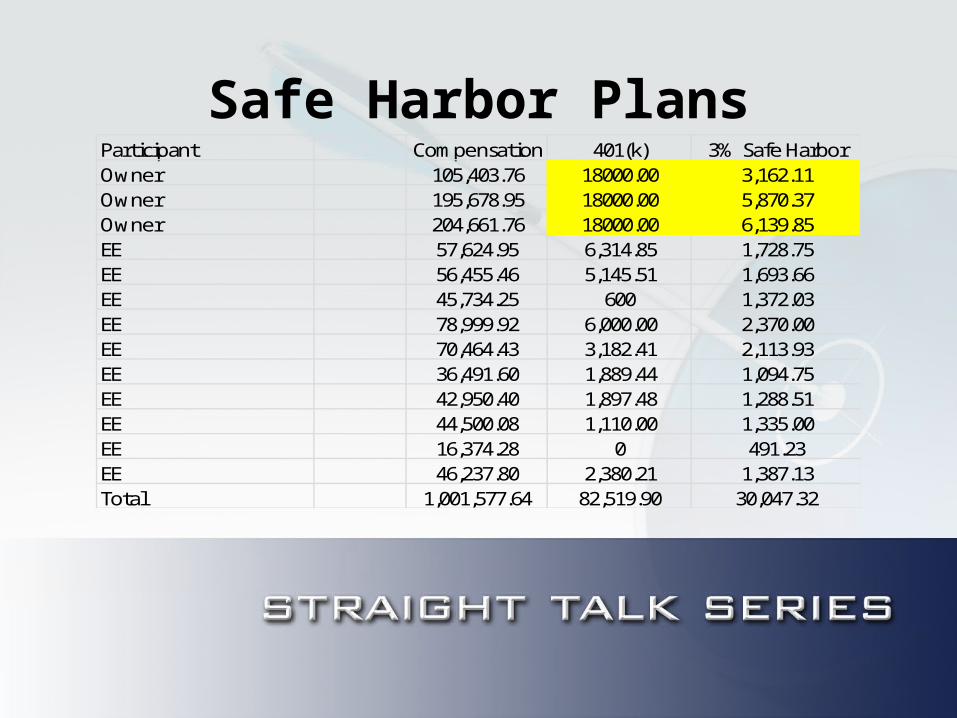

Safe Harbor PlansParticipant Compensation 401(k) 3% Safe HarborOwner 105,403.76 18000.00 3,162.11Owner 195,678.95 18000.00 5,870.37Owner 204,661.76 18000.00 6,139.85EE 57,624.95 6,314.85 1,728.75EE 56,455.46 5,145.51 1,693.66EE 45,734.25 600 1,372.03EE 78,999.92 6,000.00 2,370.00EE 70,464.43 3,182.41 2,113.93EE 36,491.60 1,889.44 1,094.75EE 42,950.40 1,897.48 1,288.51EE 44,500.08 1,110.00 1,335.00EE 16,374.28 0 491.23EE 46,237.80 2,380.21 1,387.13Total 1,001,577.64 82,519.90 30,047.32

Safe Harbor Plans

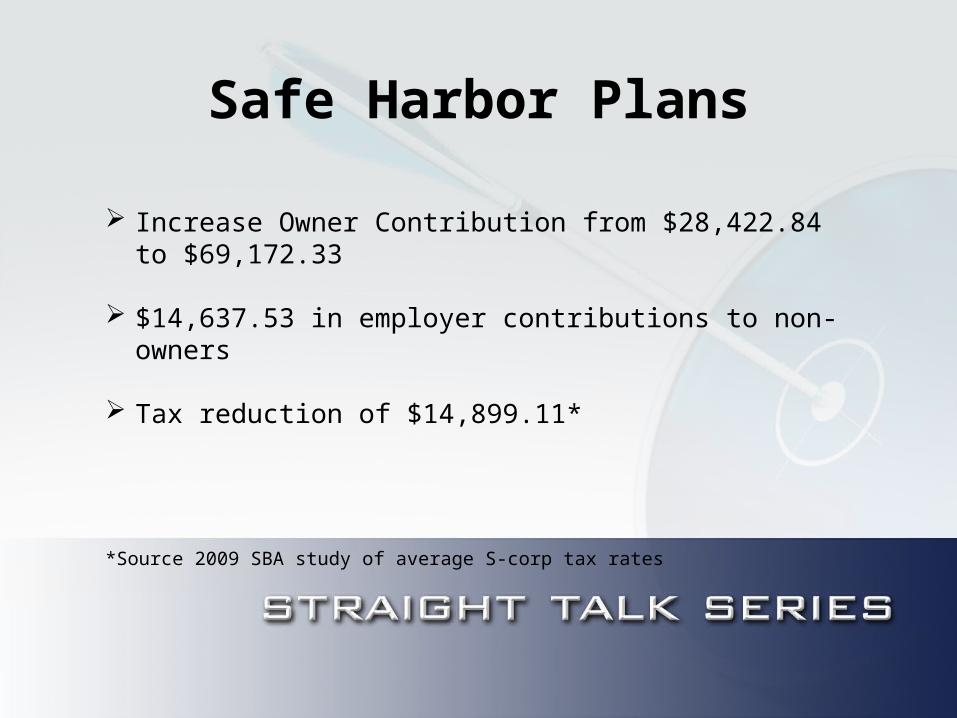

Increase Owner Contribution from $28,422.84 to $69,172.33

$14,637.53 in employer contributions to non-owners

Tax reduction of $14,899.11*

*Source 2009 SBA study of average S-corp tax rates

Profit Sharing

Profit Sharing Plans

Pro-rata

Integrated

Age Weighted

New Comparability/Cross Tested

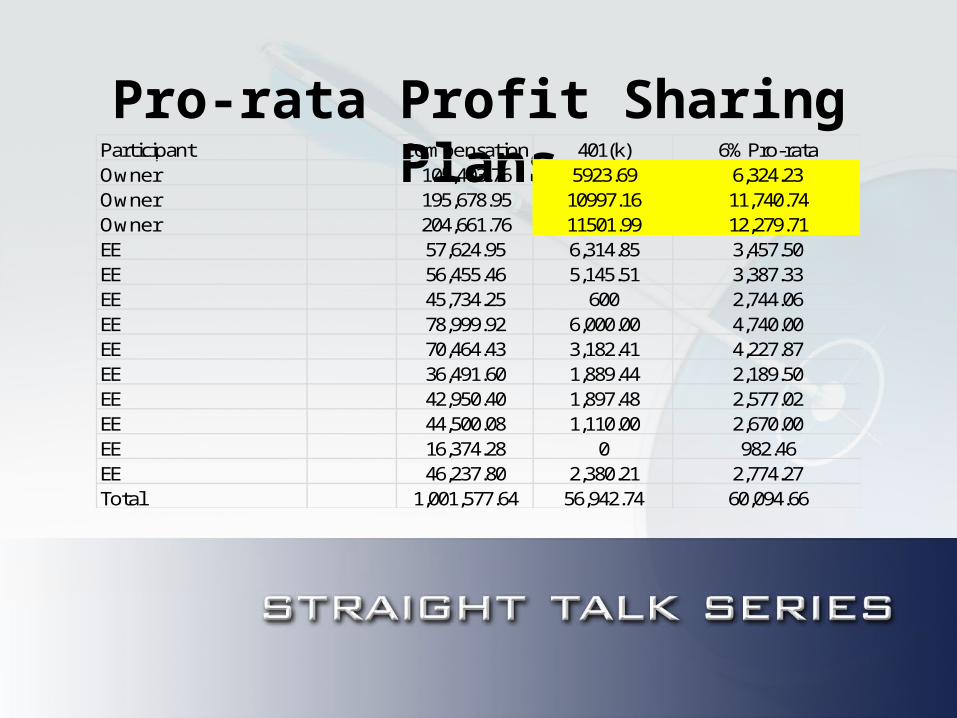

Pro-rata Profit Sharing Plans

Participant Compensation 401(k) 6% Pro-rataOwner 105,403.76 5923.69 6,324.23Owner 195,678.95 10997.16 11,740.74Owner 204,661.76 11501.99 12,279.71EE 57,624.95 6,314.85 3,457.50EE 56,455.46 5,145.51 3,387.33EE 45,734.25 600 2,744.06EE 78,999.92 6,000.00 4,740.00EE 70,464.43 3,182.41 4,227.87EE 36,491.60 1,889.44 2,189.50EE 42,950.40 1,897.48 2,577.02EE 44,500.08 1,110.00 2,670.00EE 16,374.28 0 982.46EE 46,237.80 2,380.21 2,774.27Total 1,001,577.64 56,942.74 60,094.66

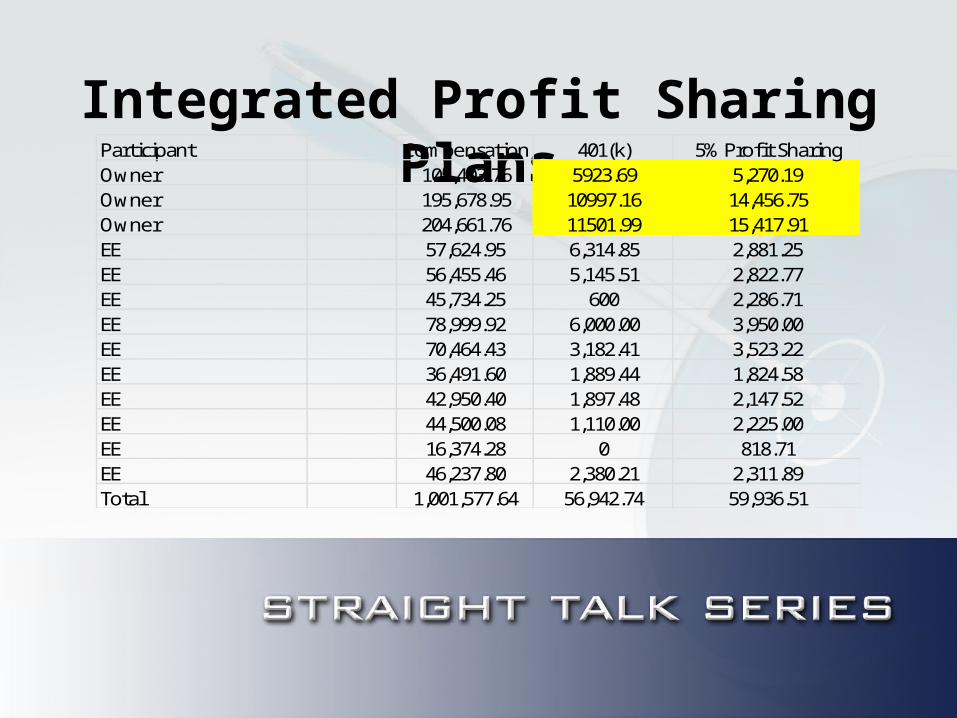

Integrated Profit Sharing PlansParticipant Compensation 401(k) 5% Profit SharingOwner 105,403.76 5923.69 5,270.19Owner 195,678.95 10997.16 14,456.75Owner 204,661.76 11501.99 15,417.91EE 57,624.95 6,314.85 2,881.25EE 56,455.46 5,145.51 2,822.77EE 45,734.25 600 2,286.71EE 78,999.92 6,000.00 3,950.00EE 70,464.43 3,182.41 3,523.22EE 36,491.60 1,889.44 1,824.58EE 42,950.40 1,897.48 2,147.52EE 44,500.08 1,110.00 2,225.00EE 16,374.28 0 818.71EE 46,237.80 2,380.21 2,311.89Total 1,001,577.64 56,942.74 59,936.51

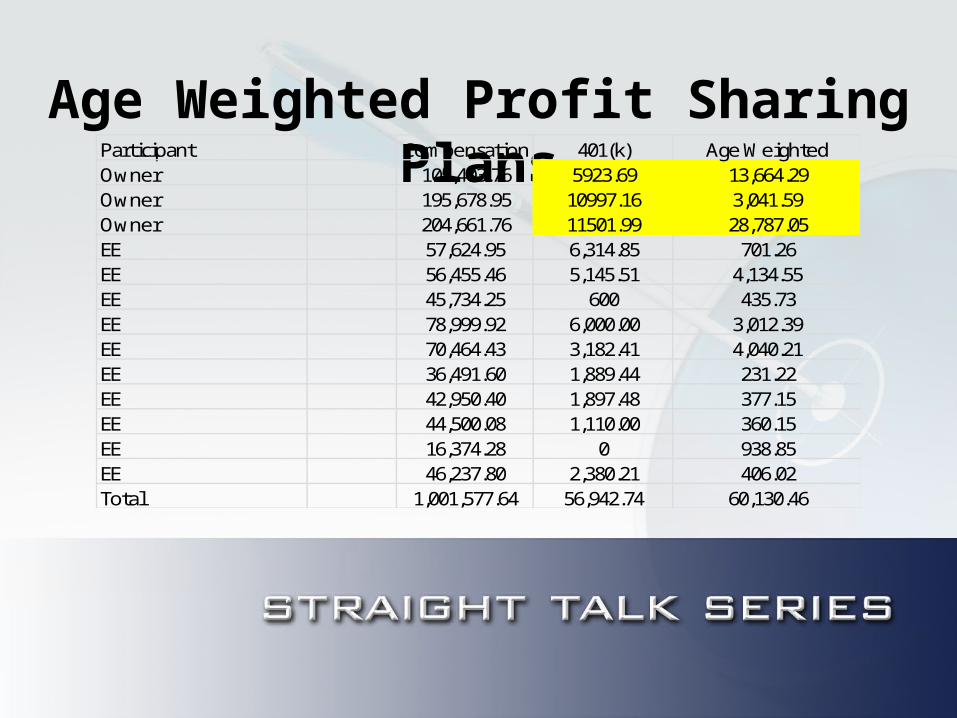

Age Weighted Profit Sharing Plans

Participant Compensation 401(k) Age WeightedOwner 105,403.76 5923.69 13,664.29Owner 195,678.95 10997.16 3,041.59Owner 204,661.76 11501.99 28,787.05EE 57,624.95 6,314.85 701.26EE 56,455.46 5,145.51 4,134.55EE 45,734.25 600 435.73EE 78,999.92 6,000.00 3,012.39EE 70,464.43 3,182.41 4,040.21EE 36,491.60 1,889.44 231.22EE 42,950.40 1,897.48 377.15EE 44,500.08 1,110.00 360.15EE 16,374.28 0 938.85EE 46,237.80 2,380.21 406.02Total 1,001,577.64 56,942.74 60,130.46

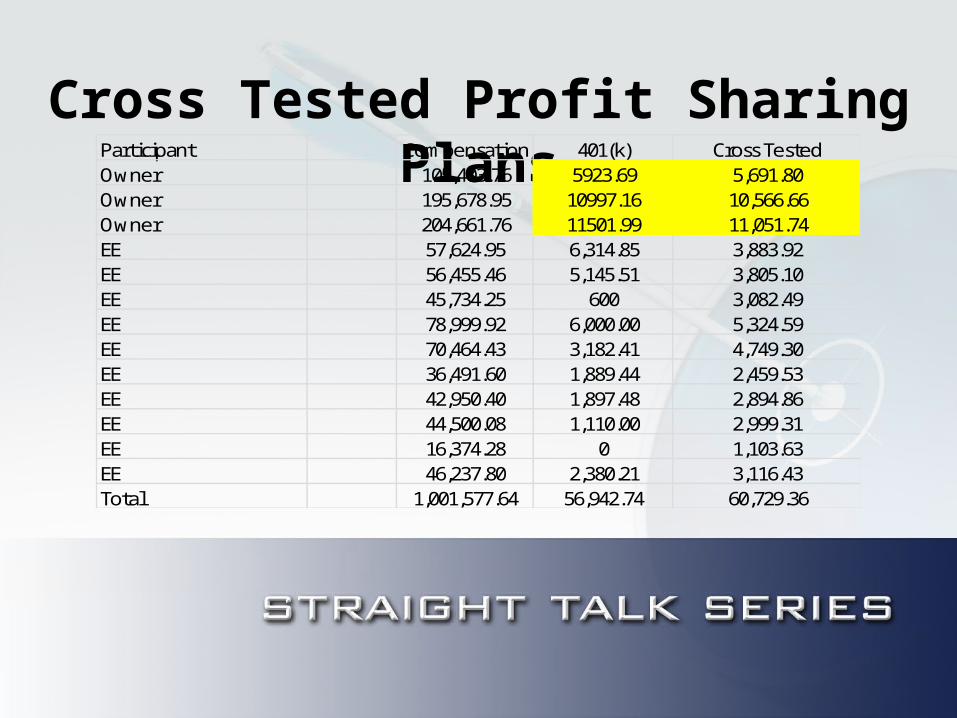

Cross Tested Profit Sharing Plans

Participant Compensation 401(k) Cross TestedOwner 105,403.76 5923.69 5,691.80Owner 195,678.95 10997.16 10,566.66Owner 204,661.76 11501.99 11,051.74EE 57,624.95 6,314.85 3,883.92EE 56,455.46 5,145.51 3,805.10EE 45,734.25 600 3,082.49EE 78,999.92 6,000.00 5,324.59EE 70,464.43 3,182.41 4,749.30EE 36,491.60 1,889.44 2,459.53EE 42,950.40 1,897.48 2,894.86EE 44,500.08 1,110.00 2,999.31EE 16,374.28 0 1,103.63EE 46,237.80 2,380.21 3,116.43Total 1,001,577.64 56,942.74 60,729.36

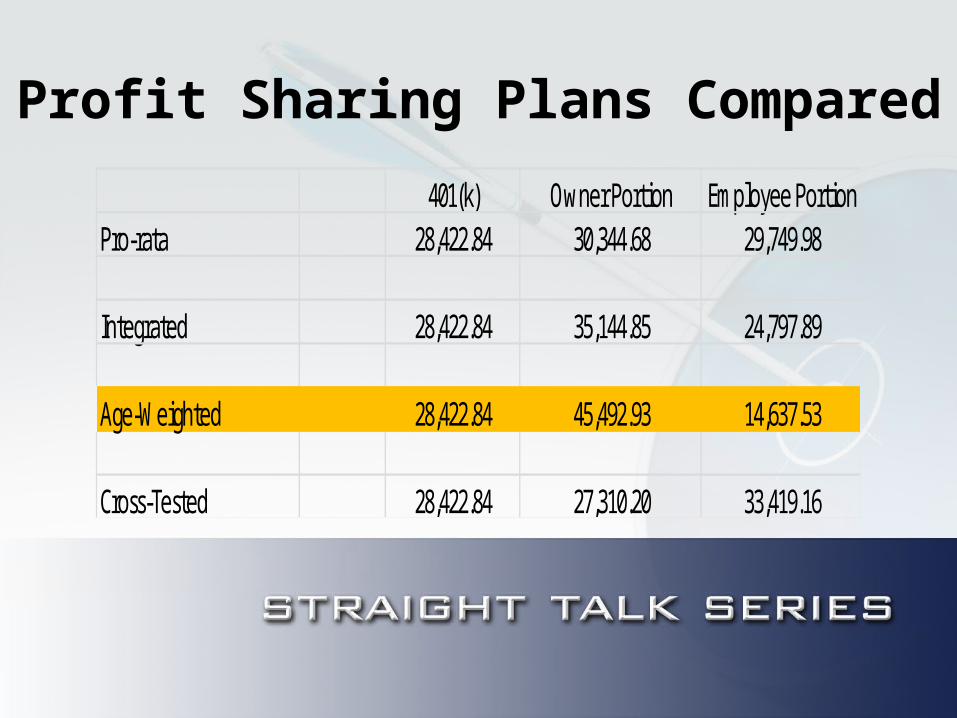

Profit Sharing Plans Compared

401(k) Owner Portion Employee PortionPro-rata 28,422.84 30,344.68 29,749.98

Integrated 28,422.84 35,144.85 24,797.89

Age-Weighted 28,422.84 45,492.93 14,637.53

Cross-Tested 28,422.84 27,310.20 33,419.16

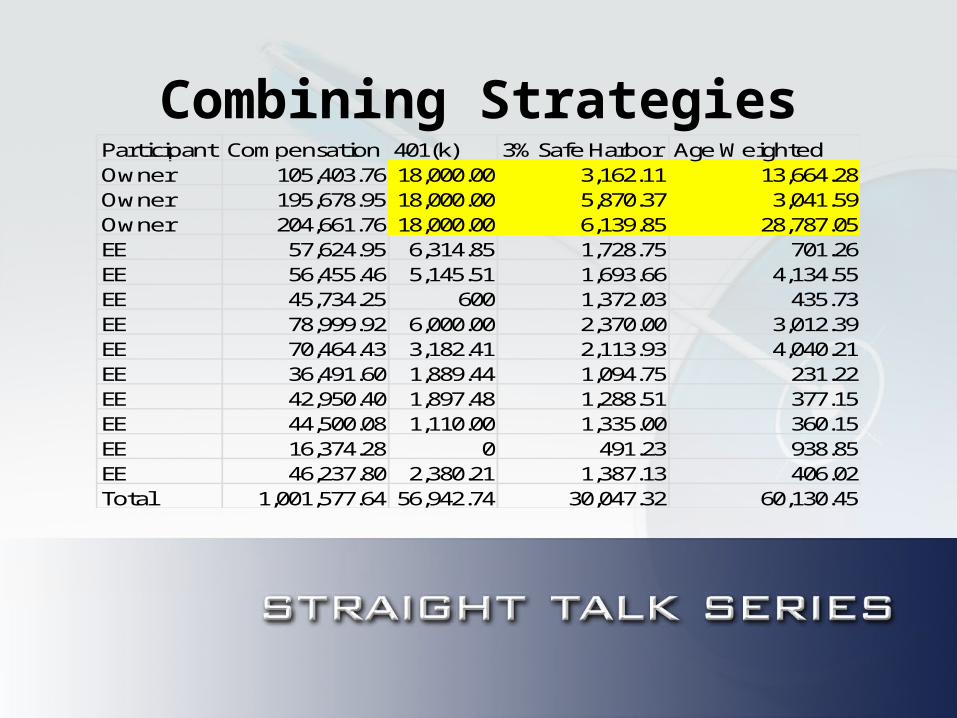

Combining StrategiesParticipant Compensation 401(k) 3% Safe Harbor Age WeightedOwner 105,403.76 18,000.00 3,162.11 13,664.28Owner 195,678.95 18,000.00 5,870.37 3,041.59Owner 204,661.76 18,000.00 6,139.85 28,787.05EE 57,624.95 6,314.85 1,728.75 701.26EE 56,455.46 5,145.51 1,693.66 4,134.55EE 45,734.25 600 1,372.03 435.73EE 78,999.92 6,000.00 2,370.00 3,012.39EE 70,464.43 3,182.41 2,113.93 4,040.21EE 36,491.60 1,889.44 1,094.75 231.22EE 42,950.40 1,897.48 1,288.51 377.15EE 44,500.08 1,110.00 1,335.00 360.15EE 16,374.28 0 491.23 938.85EE 46,237.80 2,380.21 1,387.13 406.02Total 1,001,577.64 56,942.74 30,047.32 60,130.45

Combining Strategies

Increase Owner Contribution from $28,422.84 to $114,665.26

$29,512.52 in employer contributions to non-owners

Tax reduction of $31,138.08*

*Source 2009 SBA study of average S-corp tax rates

The Bottom Line

A 401(k) Plan is a valuable tax planning tool

Tax benefits exist for all participants

Business owners can make significant enhancement to their own accounts while benefiting employees and reducing their tax liability

Careful analysis and a customized solution are needed since the dynamics of each business are different

Minimizing Your Tax Obligations