Embed Size (px)

Citation preview

Dr Sheeba Kapil 1

Mergers & Acquisition

Dr Sheeba Kapil 2

Most of M&A fail ?

Pursue them when they make sense Deals should be above average Easier said than done‼ Why pursued by cos?

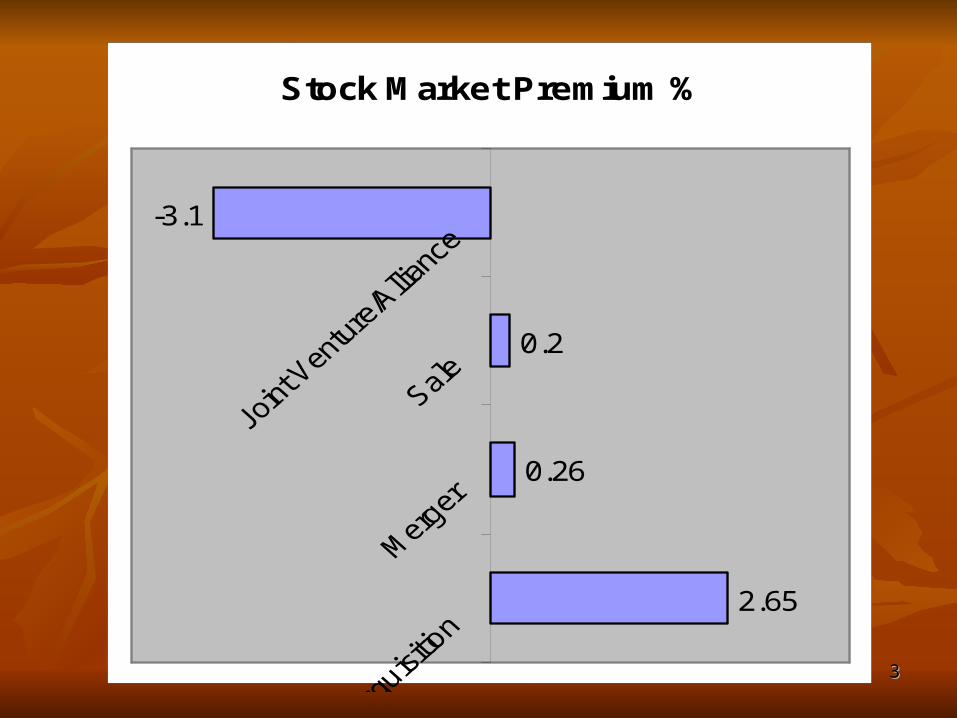

Maximum value is given by Market to acquisition deals as compared to alliances/sale

Dr Sheeba KapilDr Sheeba Kapil 33

Stock Market Premium %

2.65

0.26

0.2

-3.1

Dr Sheeba Kapil 4

Market prefers deals that are part of an “expansionist program”,

consolidation, new geographic regions, adding new distribution channels, for

existing products & services

Market less tolerant of “transformative deals” that move cos into new lines of business,

remove a chunk of an otherwise healthy business portfolio’

Dr Sheeba Kapil 5

MARKET PREFERSDEALS

CONSOLIDATING

NEW GEOGRAPHIC REGION

ADD NEW DISTRIBUTION

CHANNEL

EXPANSIONPROGRAM

TRANSFORMATIVE NATURE

Dr Sheeba Kapil 6

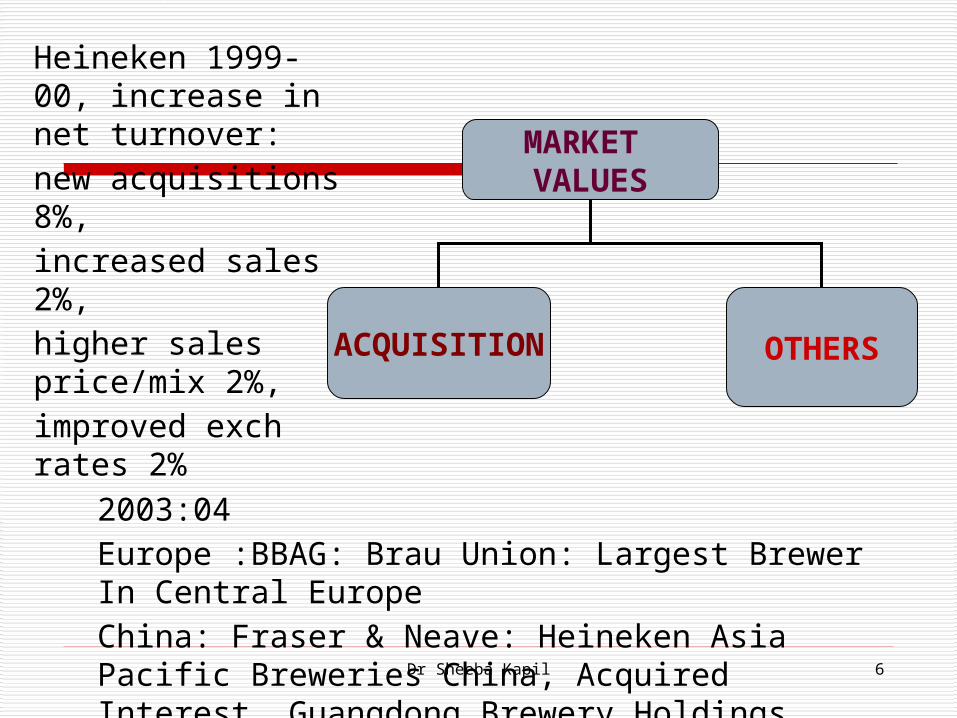

MARKET VALUES

ACQUISITION OTHERS

Heineken 1999-00, increase in net turnover: new acquisitions 8%, increased sales 2%, higher sales price/mix 2%, improved exch rates 2%

2003:04Europe :BBAG: Brau Union: Largest Brewer In Central EuropeChina: Fraser & Neave: Heineken Asia Pacific Breweries China, Acquired Interest Guangdong Brewery HoldingsAustralia: JV Lion Nathan Australia: Heineken Lion Nathan

Dr Sheeba Kapil 7

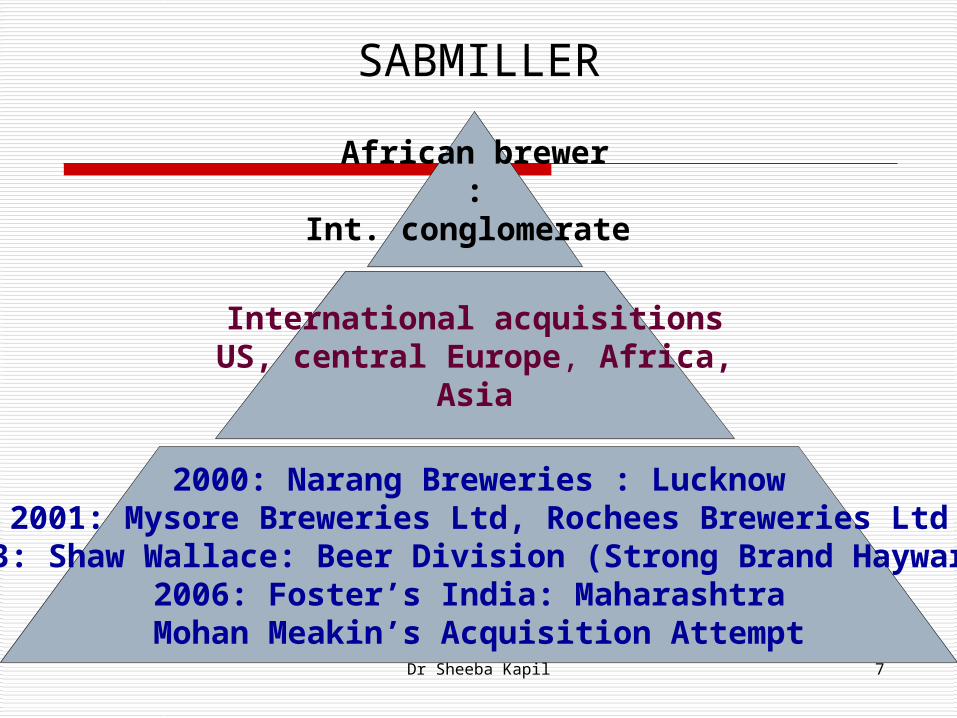

SABMILLER

African brewer:

Int. conglomerate

International acquisitionsUS, central Europe, Africa,

Asia

2000: Narang Breweries : Lucknow2001: Mysore Breweries Ltd, Rochees Breweries Ltd

2003: Shaw Wallace: Beer Division (Strong Brand Haywards)2006: Foster’s India: Maharashtra

Mohan Meakin’s Acquisition Attempt

Dr Sheeba Kapil 8

Dr Sheeba Kapil 9

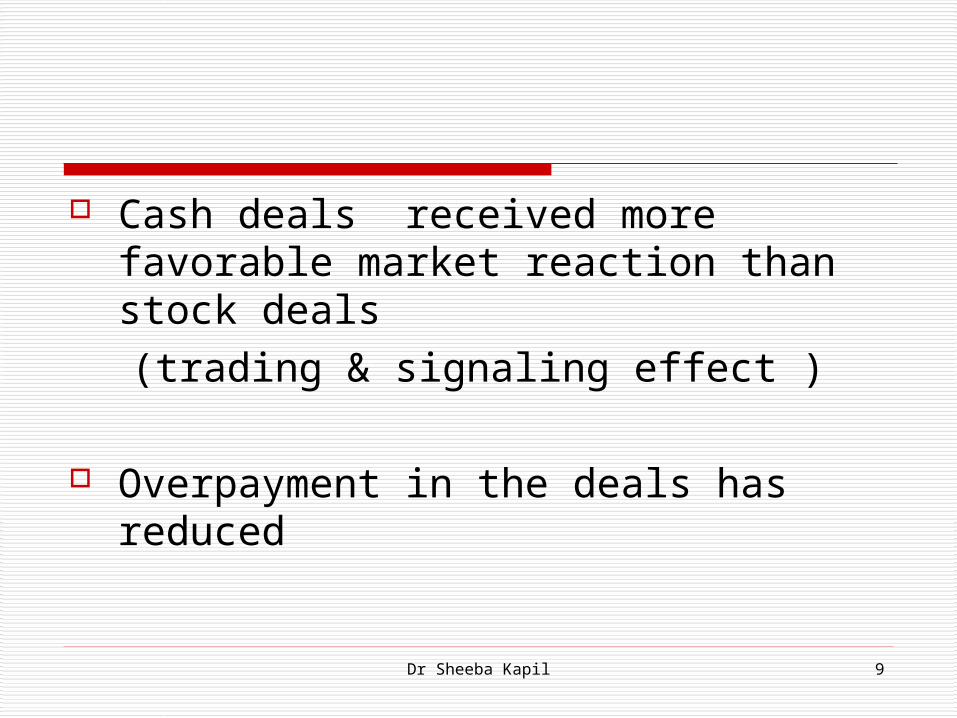

Cash deals received more favorable market reaction than stock deals

(trading & signaling effect )

Overpayment in the deals has reduced

Dr Sheeba Kapil 10

Positive correlation announcement effects & long run value creation

Record level in announced M&A

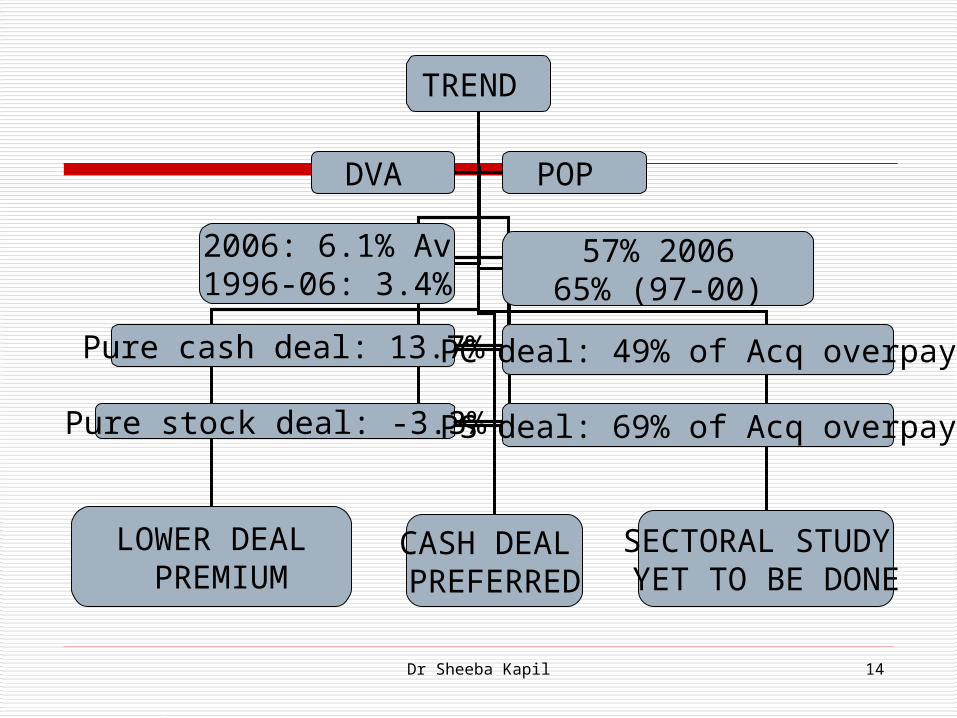

DVA- total value deals create

POP- proportion of cos overpaying

Dr Sheeba Kapil 11

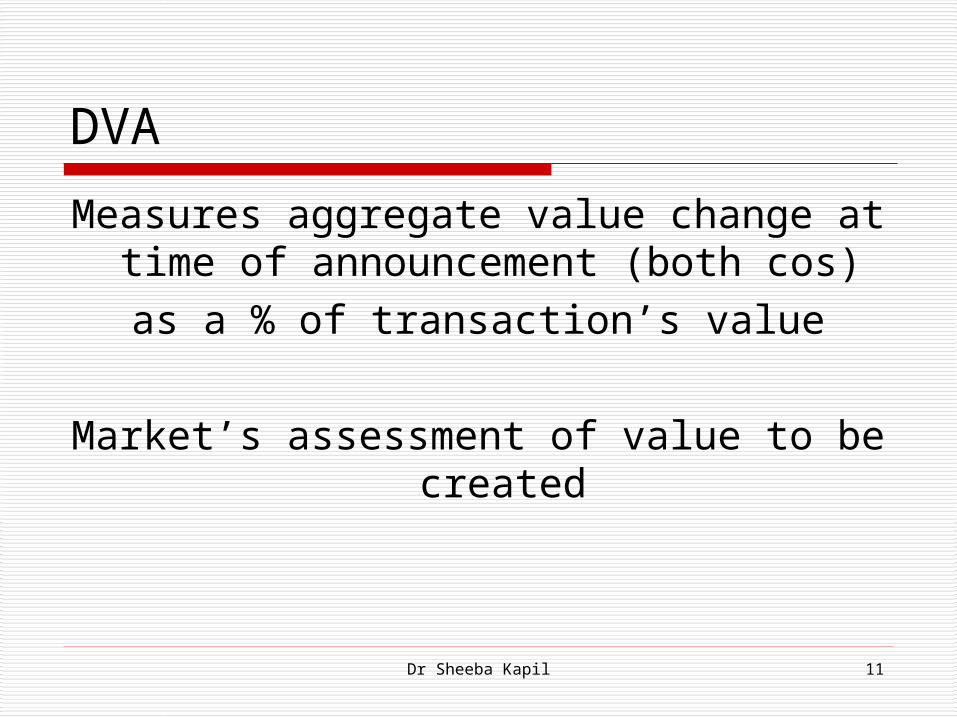

DVA

Measures aggregate value change at time of announcement (both cos)

as a % of transaction’s value

Market’s assessment of value to be created

Dr Sheeba Kapil 12

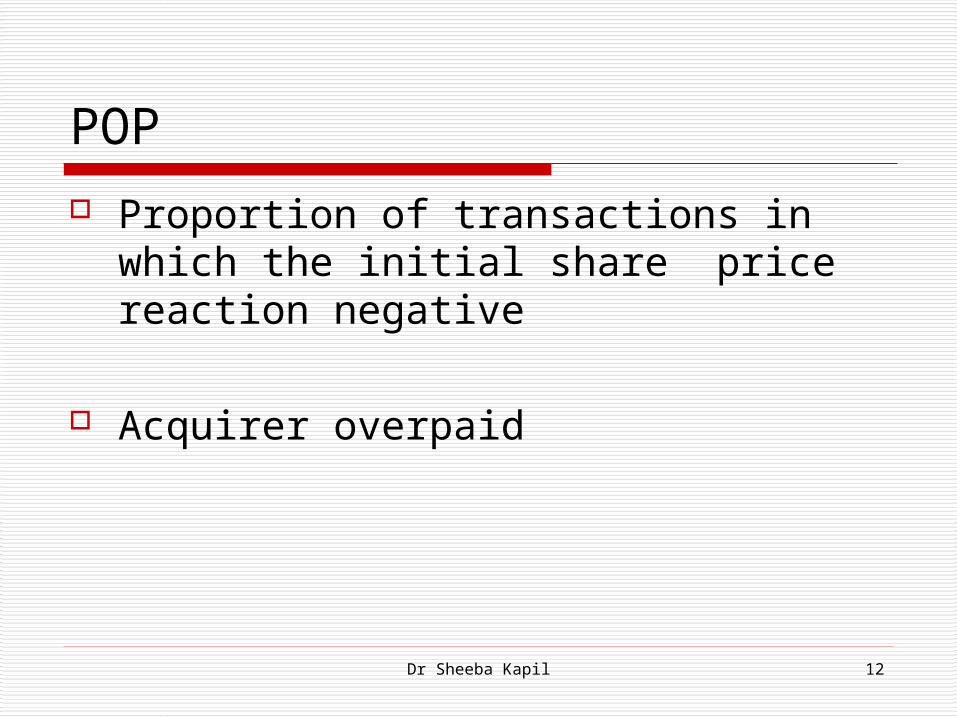

POP

Proportion of transactions in which the initial share price reaction negative

Acquirer overpaid

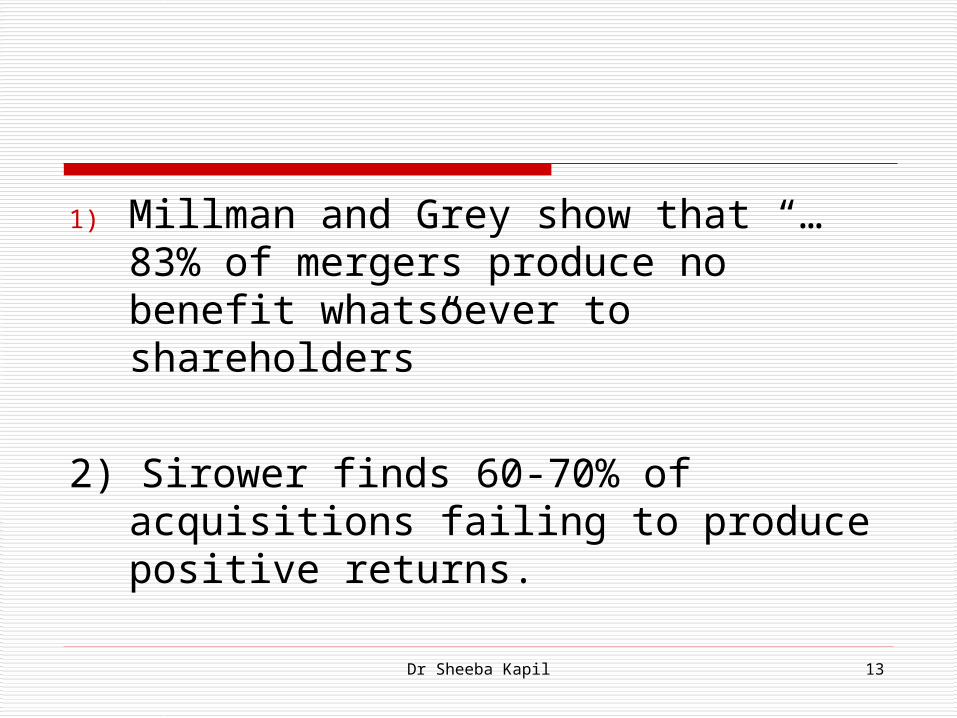

Dr Sheeba Kapil 13

1) Millman and Grey show that “…83% of mergers produce no benefit whatsoever to shareholders”

2) Sirower finds 60-70% of acquisitions failing to produce positive returns.

Dr Sheeba Kapil 14

TREND

LOWER DEAL PREMIUM

CASH DEAL PREFERRED

SECTORAL STUDY YET TO BE DONE

DVA POP

2006: 6.1% Av1996-06: 3.4%

57% 200665% (97-00)

Pure cash deal: 13.7% PC deal: 49% of Acq overpay

Pure stock deal: -3.3% PS deal: 69% of Acq overpay

Dr Sheeba Kapil 15

POPULAR TERMINOLOGIES

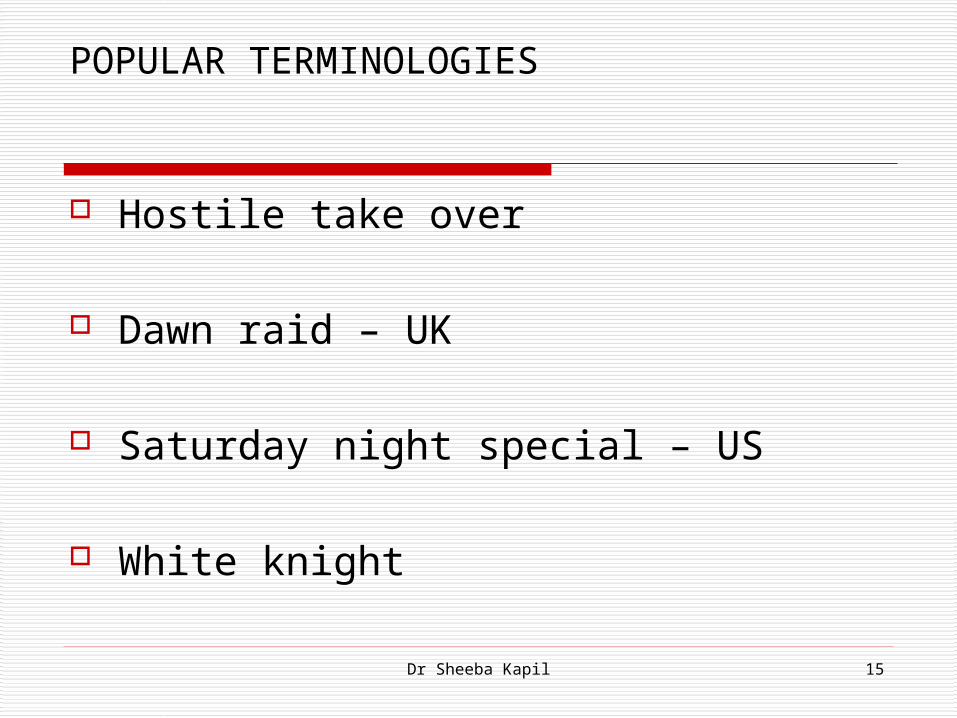

Hostile take over

Dawn raid – UK

Saturday night special – US

White knight

Dr Sheeba Kapil 16

Shark repellent

Golden parachute Greenmail/ goodbye kiss Macaroni defense Bank check preferred stock Poison pill (flip in PP, flip over PP) Lady macbeth Bankmail

Dr Sheeba Kapil 17

Types of M&A

Merger

A transaction where two firms agree to integrate their operations on a

relatively coequal basis because they have resources and capabilities that

together may create a stronger competitive advantage

Dr Sheeba Kapil 18

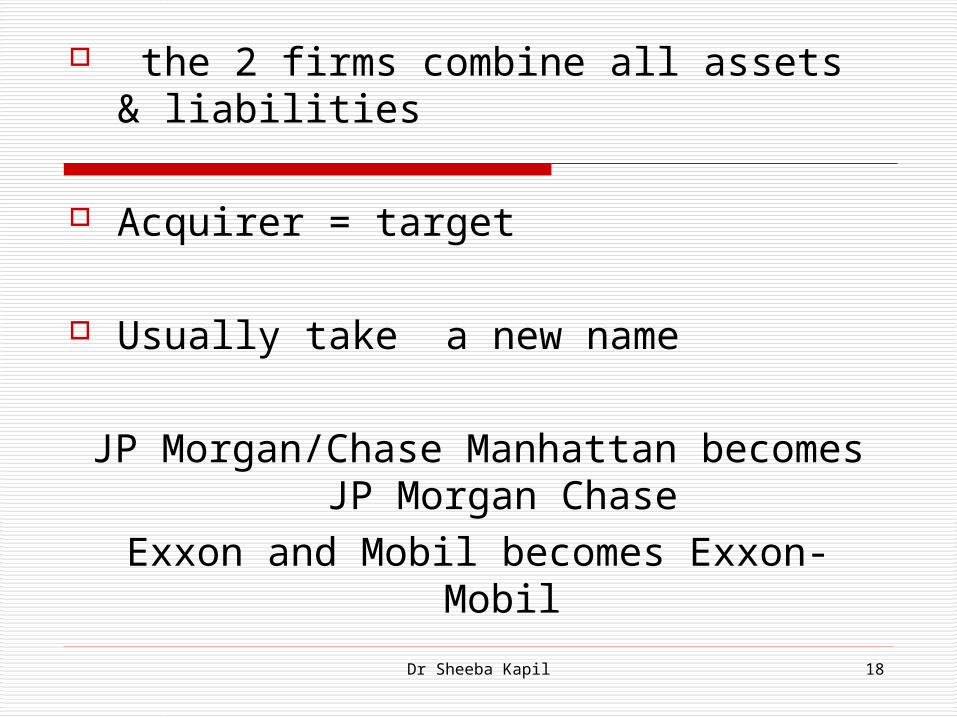

the 2 firms combine all assets & liabilities

Acquirer = target

Usually take a new name

JP Morgan/Chase Manhattan becomes JP Morgan Chase

Exxon and Mobil becomes Exxon-Mobil

Dr Sheeba Kapil 19

Target firm shares disappear Target shareholders get either

1) Shares in new firm2) Cash

Exchange Ratio = # shares in new firm given for each share of Target firm

Ex) # target = 250 million & ER = 1.25 # New = 1.25 x 250 M = 312.5 M

Buyer firm shares are kept as shares in new firm ( in effect their ER = 1).

Dr Sheeba Kapil 20

Combination of 2 firms- only one firm's identity survives

Statutory merger- in accordance with statutes of state in which it is incorpt.

Subsidiary merger- target becomes subsidiary of parent like GM & EDS

Horizontal merger

Vertical merger

Dr Sheeba Kapil 21

Acquisition

A transaction where one firm buys another firm with the intent of more effectively using a core competence

by making the acquired firm a subsidiary within its portfolio of

businesses

Dr Sheeba Kapil 22

Takeover

An acquisition where the target firm did not solicit the bid of the acquiring firm

IBM’s acquisition of Lotus in 1995; Oracle’s bid for PeopleSoft in 2003

Dr Sheeba Kapil 23

M&A Jargons

Corporate restructuring (asset/ financial)

Types

Operational - downsizing/downscoping

Financial – debt/equity (leverage effect )

Dr Sheeba Kapil 24

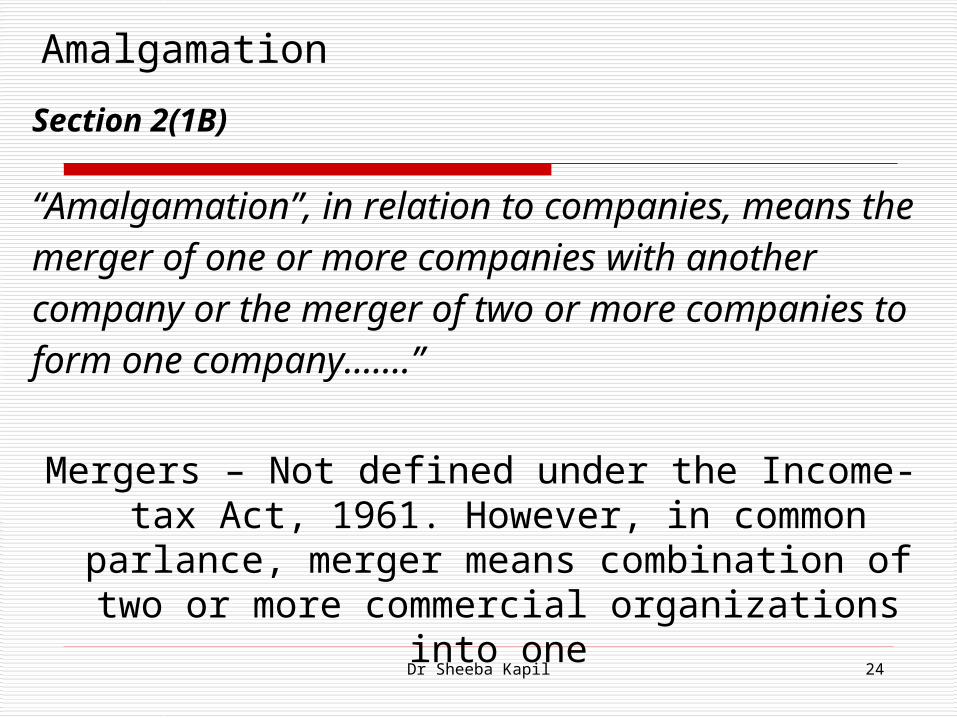

Amalgamation

Section 2(1B)

“Amalgamation”, in relation to companies, means the merger of one or more companies with another company or the merger of two or more companies to form one company…….”

Mergers – Not defined under the Income-tax Act, 1961. However, in common parlance, merger means

combination of two or more commercial organizations into one

Dr Sheeba Kapil 25

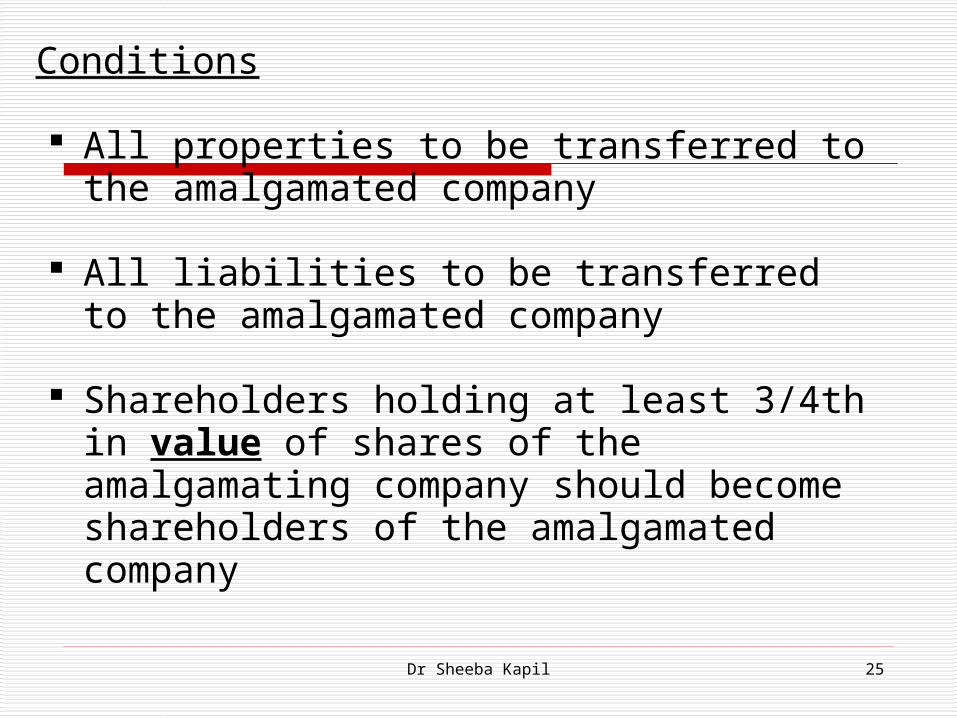

Conditions

All properties to be transferred to the amalgamated company

All liabilities to be transferred to the amalgamated company

Shareholders holding at least 3/4th in value of shares of the amalgamating company should become shareholders of the amalgamated company

Dr Sheeba Kapil 26

Types of mergers

Dr Sheeba Kapil 27

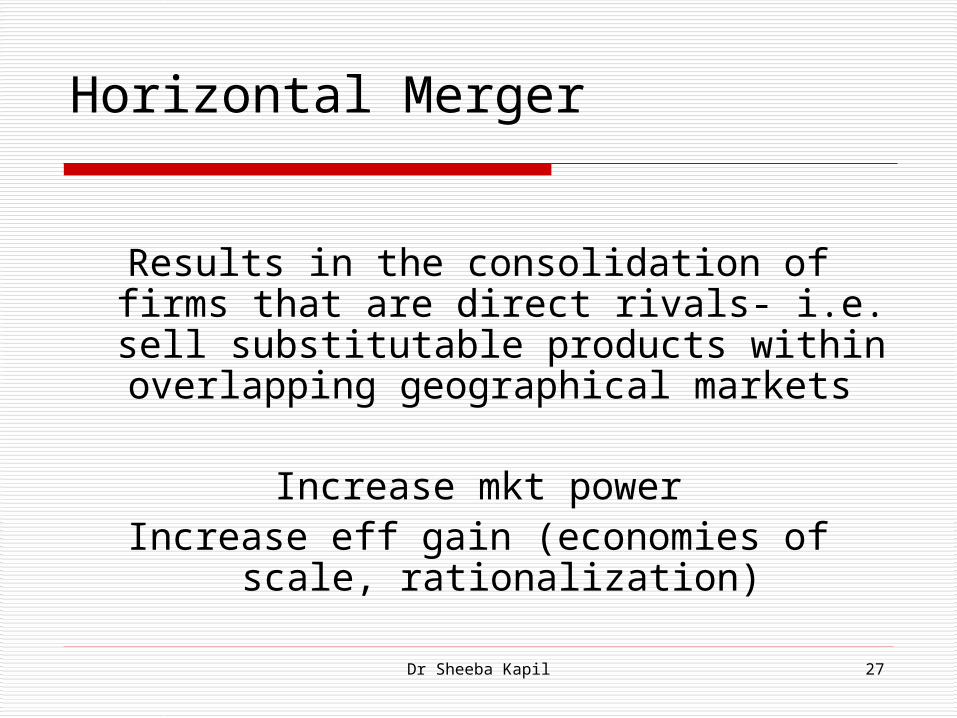

Horizontal Merger

Results in the consolidation of firms that are direct rivals- i.e. sell substitutable

products within overlapping geographical markets

Increase mkt powerIncrease eff gain (economies of scale,

rationalization)

Dr Sheeba Kapil 28

Contd….

Two firm same industry Seek economies of scale (BP & Amoco expected to save $2 bn p.a.

from operations) huge challenge of integration (Exxon & mobil, Helene-Curtis and unilever)

Dr Sheeba Kapil 29

Kuhn & motto (1999)

Increases prices, decreases consumer surplus

Always benefits the merging firm Increases outsider’s profits Increases producer surplus Reduces net welfare

Dr Sheeba Kapil 30

Vertical mergers

1. Two firms participate at difft stages of production or value chain

2. cos do not own operations in major segment of value chain

Forward integration- Merck-medcoBackward integration- Chevron’s oil- gulf oil,

America online- mapquest

Dr Sheeba Kapil 31

Conglomerate merger Consolidated firms may sell related products, share

marketing & distribution channels & production processes, or they may be wholly unrelated

Ciba-Geigy (contact lens, Ritalin, Maalox) & Sandoz(Gerber Baby Food, Ovaltine) - Novartis

US steel- marathon oil = USX AOL- time Warner PepsiCo- pizza hut Citicorp- travelers insurance P&G & clorox Cardinal healthcare - allegiance

Dr Sheeba Kapil 32

Product extension in conglomerate

Involve firms that sell non competing products use related marketing channels of production processes

Citicorp – travelers insurance

Pepsico – pizza hut

Dr Sheeba Kapil 33

Market extension

Join together firms that sell competing products in separate geographical

markets

Time warner- TCI SBC communications- pacific telesis

Dr Sheeba Kapil 34

Pure conglomerate

Such merger unites firms that have no obvious relationship of any kind

AT&T – hartford insuranceBankcorp of America- Hughes

electronicsR J Reynolds- burmah oil & gas

Dr Sheeba Kapil 35

Participants

Investment bankers – strategic & tactical advice Screen potential buyers & sellers Contact & negotiate Valuation Deal structuringGoldman Sachs (40%), Morgan

Stanley (26%), Merill Lynch (22%)

Dr Sheeba Kapil 36

LAWYERS Thomson financial securities data

corporation Sherman & sterling, meagher & flom Skadden Simpson thatcher & barlet Nishith Desai Associates

Dr Sheeba Kapil 37

Accountants

Tax structure Due diligence

Proxy solicitors

Georgeson & co D F king & co

Dr Sheeba Kapil 38

Reasons for AcquisitionsReasons for AcquisitionsReasons for AcquisitionsReasons for Acquisitions

Increased Market PowerIncreased Market PowerAcquisition intended to reduce the competitive balance of Acquisition intended to reduce the competitive balance of the industrythe industry

Overcome Barriers to EntryOvercome Barriers to EntryAcquisitions overcome costly barriers to entry which may make Acquisitions overcome costly barriers to entry which may make “start-ups” economically unattractive“start-ups” economically unattractive

Dr Sheeba Kapil 39

Increased Speed to MarketIncreased Speed to MarketClosely related to Barriers to Entry, allows market entry Closely related to Barriers to Entry, allows market entry in a more timely fashionin a more timely fashion

DiversificationDiversification

Quick way to move into businesses when firm currently lacks Quick way to move into businesses when firm currently lacks experience and depth in industryexperience and depth in industry

Reshaping Competitive ScopeReshaping Competitive ScopeReshaping Competitive ScopeReshaping Competitive ScopeFirms may use acquisitions to restrict its dependence on a Firms may use acquisitions to restrict its dependence on a single or a few products or marketssingle or a few products or markets

Dr Sheeba Kapil 40

Buying established businesses reduces risk of start-up Buying established businesses reduces risk of start-up venturesventures

Lower Cost and Risk of New Product DevelopmentLower Cost and Risk of New Product Development

Dr Sheeba Kapil 41

Problems with M&A

Only financial team (organizational team) Integration problem Inadequate evaluation of target Large amt debt Fail to achieve synergy Overly diversified

Dr Sheeba KapilDr Sheeba Kapil 4242

CASE EXAMPLE CASE EXAMPLE

Trend Indian Pharma sectorTrend Indian Pharma sector

The key feature of M&A activity has The key feature of M&A activity has been consolidation of indigenous been consolidation of indigenous

drug manufacturersdrug manufacturers

Dr Sheeba KapilDr Sheeba Kapil 4343

The Indian Pharmaceutical Sector - The Indian Pharmaceutical Sector - largest amongst the developing nations. largest amongst the developing nations.

In the organized sector of the Indian In the organized sector of the Indian Pharmaceutical industry there are about Pharmaceutical industry there are about 250-300 companies, controlling about 250-300 companies, controlling about 70% of the total output in value terms70% of the total output in value terms

The top 10 players accounting for one The top 10 players accounting for one third of the total market. third of the total market.

Dr Sheeba KapilDr Sheeba Kapil 4444

Indian pharmaceuticals market is Indian pharmaceuticals market is expected to expand to US$ 25 billion expected to expand to US$ 25 billion by 2010. by 2010.

The domestic industry is fragmented The domestic industry is fragmented with over 4,000 manufacturing units. with over 4,000 manufacturing units.

In such a scenario, consolidation is In such a scenario, consolidation is the only answer to survive in the the only answer to survive in the post patent regime post patent regime

Dr Sheeba KapilDr Sheeba Kapil 4545

The Indian pharma industry is known forThe Indian pharma industry is known for

superior biotech and drug synthesis superior biotech and drug synthesis skillsskills

generics, generics, cost-effectiveness and cost-effectiveness and competitiveness competitiveness high quality high quality vertically integrated manufacturing vertically integrated manufacturing

assets,assets, differentiated business modelsdifferentiated business modelsthat give it an edge that give it an edge

Dr Sheeba KapilDr Sheeba Kapil 4646

Dr Sheeba KapilDr Sheeba Kapil 4747

Reasons for M&AReasons for M&A

The lack of (R&D) productivity, The lack of (R&D) productivity, expiring patents, expiring patents, generic competition andgeneric competition and high profile product recalls high profile product recalls easy availability of capital and easy availability of capital and increased global interest in the increased global interest in the

pharmaceutical and biotech industry pharmaceutical and biotech industry

Dr Sheeba KapilDr Sheeba Kapil 4848

Reasons for Indian M&AReasons for Indian M&A Build critical mass in terms of marketing, Build critical mass in terms of marketing,

manufacturing and research manufacturing and research infrastructure infrastructure

Establish front end presence Establish front end presence Diversification into new areas: Tap other Diversification into new areas: Tap other

geographies / therapeutic segments / geographies / therapeutic segments / customers to enhance product life cycle customers to enhance product life cycle and build synergies for new products and build synergies for new products

Enhance product, technology and Enhance product, technology and intellectual property portfolio intellectual property portfolio

Catapulting market share Catapulting market share

Dr Sheeba KapilDr Sheeba Kapil 4949

The total Indian Pharmaceutical The total Indian Pharmaceutical Market is valued at US$ 8790 million Market is valued at US$ 8790 million with a growth rate of 8%. with a growth rate of 8%.

The market is predominantly a The market is predominantly a branded generic market branded generic market

Dr Sheeba KapilDr Sheeba Kapil 5050

Company Company RevRev % foreign sales % foreign sales

All All Foreign Foreign

North North America America

Europe Europe

RanbaxyRanbaxy 11741174 79%79% 36%36% 16%16%Cipla Cipla 539539 45%45% 1515 99Dr reddy’s labDr reddy’s lab 422422 65%65% 2222 1515Aurobindo pharma Aurobindo pharma 307307 11%11% NaNa NaNaNicholas piramal Nicholas piramal 276276 13%13% NaNa NaNaSun pharmaSun pharma 270270 13%13% NaNa NaNaWockhardt ltdWockhardt ltd 269269 60%60% 50% combined50% combinedLupin Lupin 263263 48%48% Na Na NaNa

Cadila ph.Cadila ph. 231231 25%25% Na Na NaNa

![Mergers & Acquisition[1]](https://img.dokumen.tips/doc/110x75/577cde161a28ab9e78ae5c2a/mergers-acquisition1.jpg)