Embed Size (px)

Citation preview

Dealerships Are Far Too Valuable To Be Sold Any Other Way

Presentation to Bank of America National Accounts ClientsHalf Moon Bay, California

September 17, 2014

Table of Contents

I. Introduction to Kerrigan Advisors

II. Today’s Auto Retail Market

IV. Buyer’s Market Perspective

V. Seller’s Market Perspective

III. The Kerrigan Blue Sky Charts

VI. Q&A

3

Busch Push

Our focus is on sellers. We work with our clients to develop the best sale’s strategy to maximize value.

We are industry experts with deep knowledge of today's buy/sell market and over $2 billion* of transaction experience.

Our sales process is highly professional, actively managed, competitive, and, most important, discreet.

We do not take listings or build “inventory”; rather, we focus on a select number of client engagements each year.

We Serve Sellers. We Know Buyers.Kerrigan Advisors Sell-Side Services

Serving clients in the most important business decision of their lives: The Sale

Focused on Sellers

Experienced, Industry Experts

High-Level of Service

Engaged Clients, Not Listings

* Includes transaction experience in auto retail, investment banking and private equity industry

SUCCESSFULSALE

OFDEALERSHIP

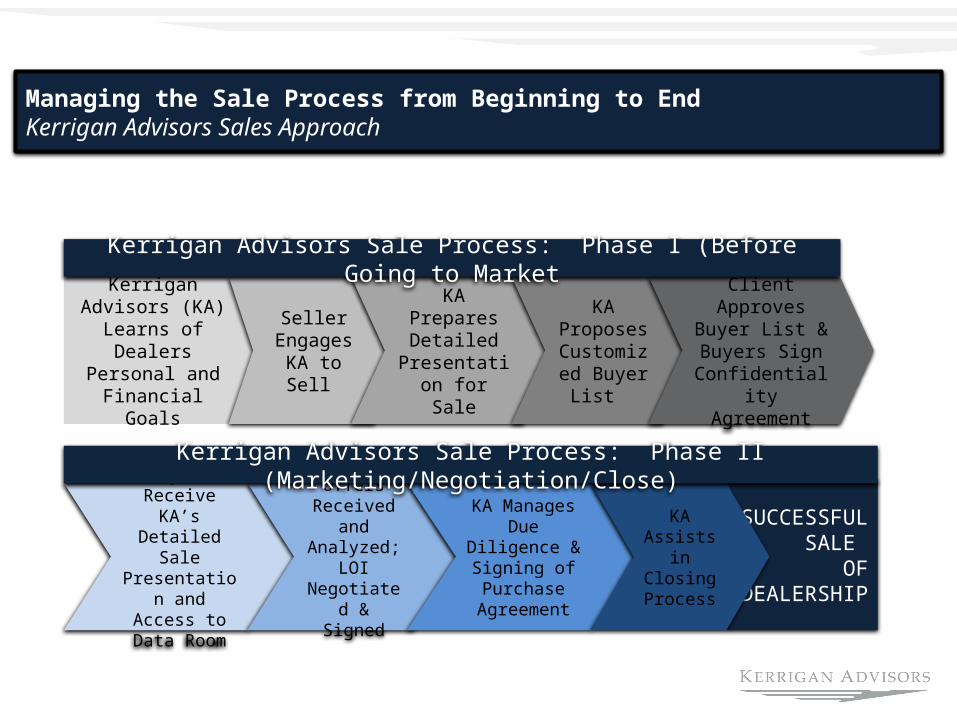

Managing the Sale Process from Beginning to EndKerrigan Advisors Sales Approach

Kerrigan Advisors (KA) Learns of

Dealers Personal and Financial Goals

Seller Engages KA

to Sell

KA Prepares Detailed

Presentation for Sale

KA Proposes Customized Buyer List

Client Approves Buyer List & Buyers Sign

Confidentiality Agreement

Buyers Receive KA’s Detailed

Sale Presentation and Access to

Data Room

Offers Received and Analyzed; LOI Negotiated &

Signed

KA Manages Due Diligence &

Signing of Purchase

Agreement

KA Assists in Closing Process

Kerrigan Advisors Sale Process: Phase I (Before Going to Market

Kerrigan Advisors Sale Process: Phase II (Marketing/Negotiation/Close)

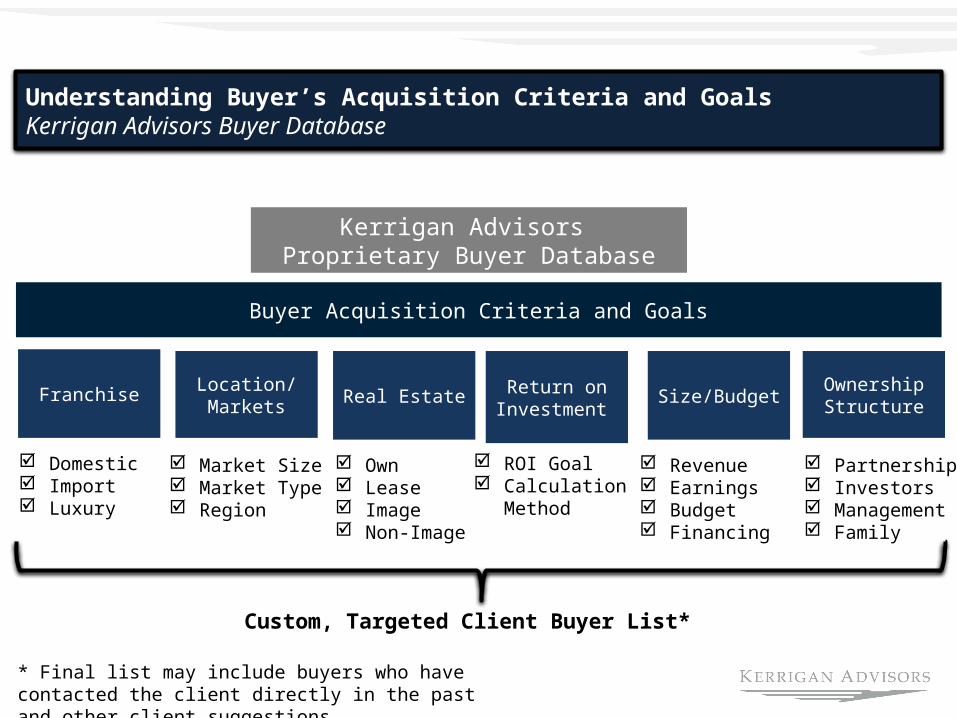

Understanding Buyer’s Acquisition Criteria and GoalsKerrigan Advisors Buyer Database

Kerrigan Advisors Proprietary Buyer Database

Size/BudgetOwnership Structure

Return on Investment

Real EstateLocation/Markets

Franchise

Buyer Acquisition Criteria and Goals

Domestic Import Luxury

Market Size Market Type Region

Own Lease Image Non-Image

ROI Goal Calculation

Method

Revenue Earnings Budget Financing

Partnership Investors Management Family

Custom, Targeted Client Buyer List*

* Final list may include buyers who have contacted the client directly in the past and other client suggestions

II. Today’s Auto Retail Market

9

“The automotive sector and its record over the past few years is resilience defined. Out of crisis, a phoenix has arisen. The auto industry’s ability to reinvent itself is one of the most remarkable stories I’ve seen in my 27 years in business.”

Penny Pritzker, US Secretary of Commerce

Resilience Defined – Auto Retail’s Rebound Exceeds ExpectationsSurpassed a 17.5M SAAR in August!

10

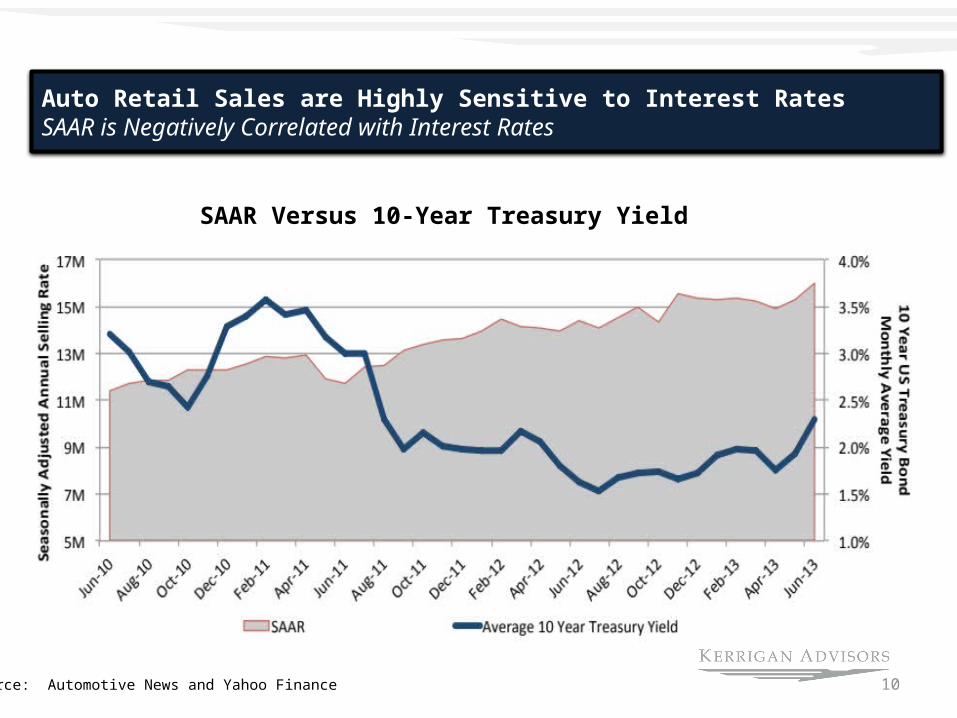

Auto Retail Sales are Highly Sensitive to Interest RatesSAAR is Negatively Correlated with Interest Rates

Source: Automotive News and Yahoo Finance

SAAR Versus 10-Year Treasury Yield

11

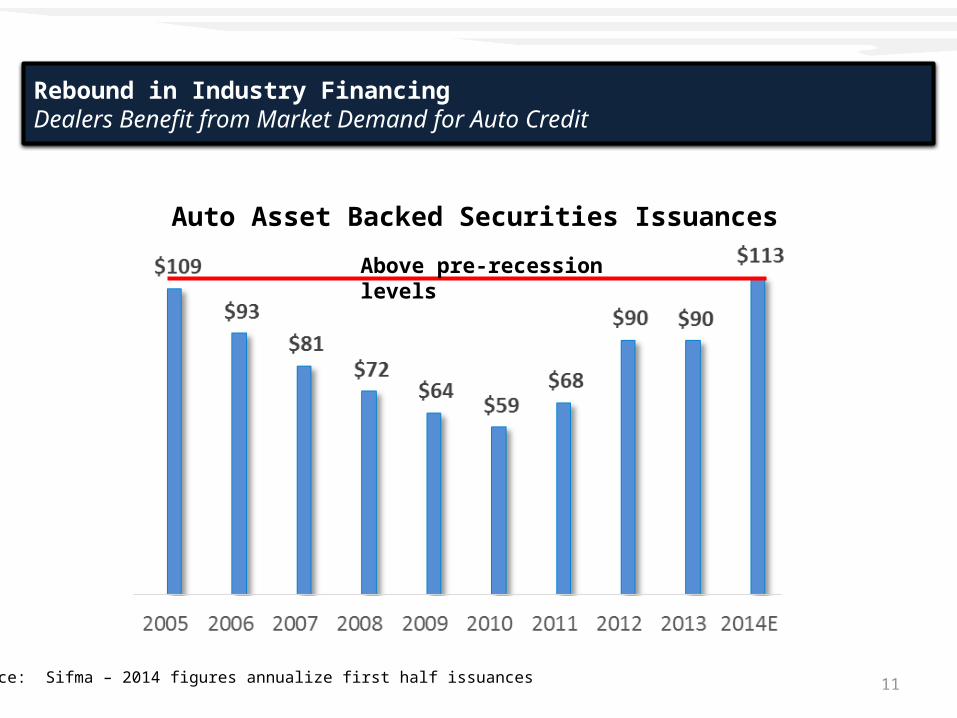

Auto Asset Backed Securities Issuances

Source: Sifma – 2014 figures annualize first half issuances

Rebound in Industry FinancingDealers Benefit from Market Demand for Auto Credit

Above pre-recession levels

12

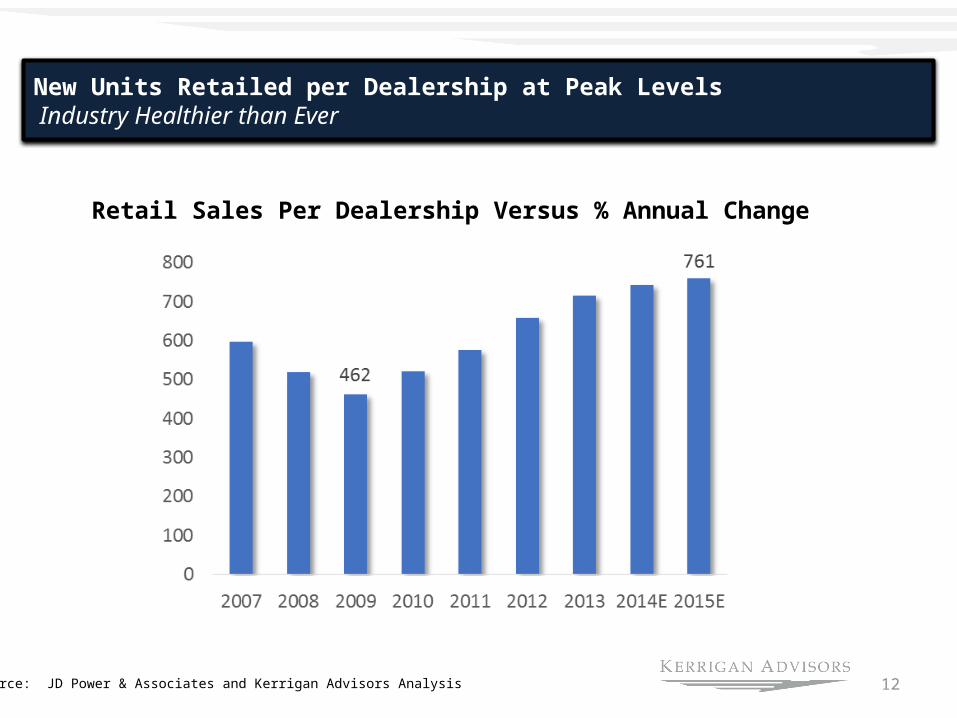

New Units Retailed per Dealership at Peak Levels Industry Healthier than Ever

Source: JD Power & Associates and Kerrigan Advisors Analysis

Retail Sales Per Dealership Versus % Annual Change

13

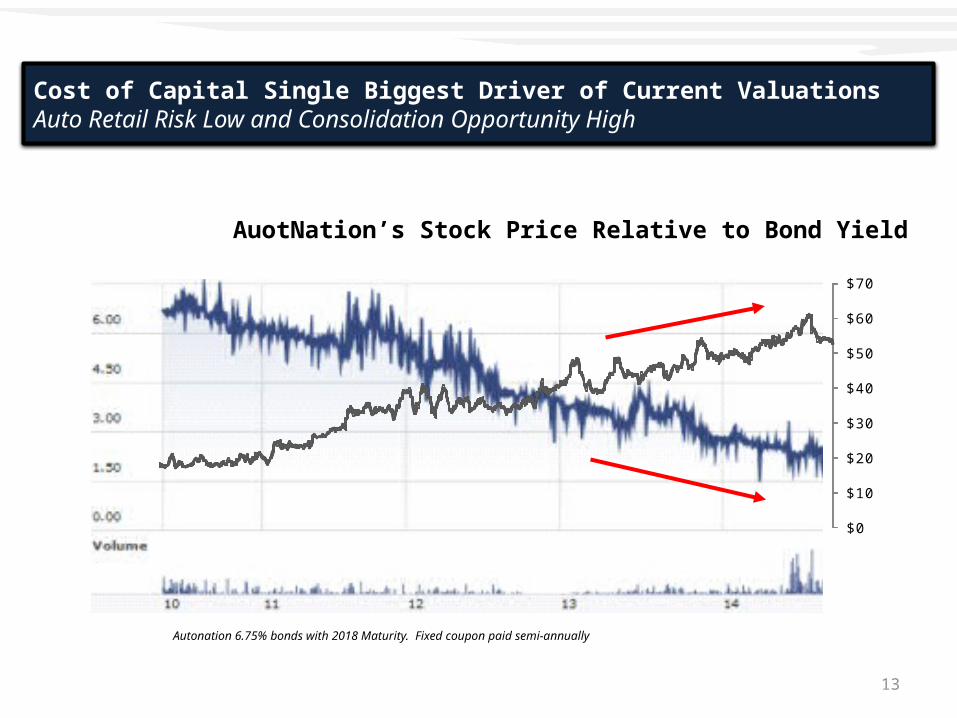

Cost of Capital Single Biggest Driver of Current ValuationsAuto Retail Risk Low and Consolidation Opportunity High

$0

$10

$20

$30

$40

$50

$60

$70

AuotNation’s Stock Price Relative to Bond Yield

Autonation 6.75% bonds with 2018 Maturity. Fixed coupon paid semi-annually

14

Kerrigan Advisors Blue Sky Multiples

15

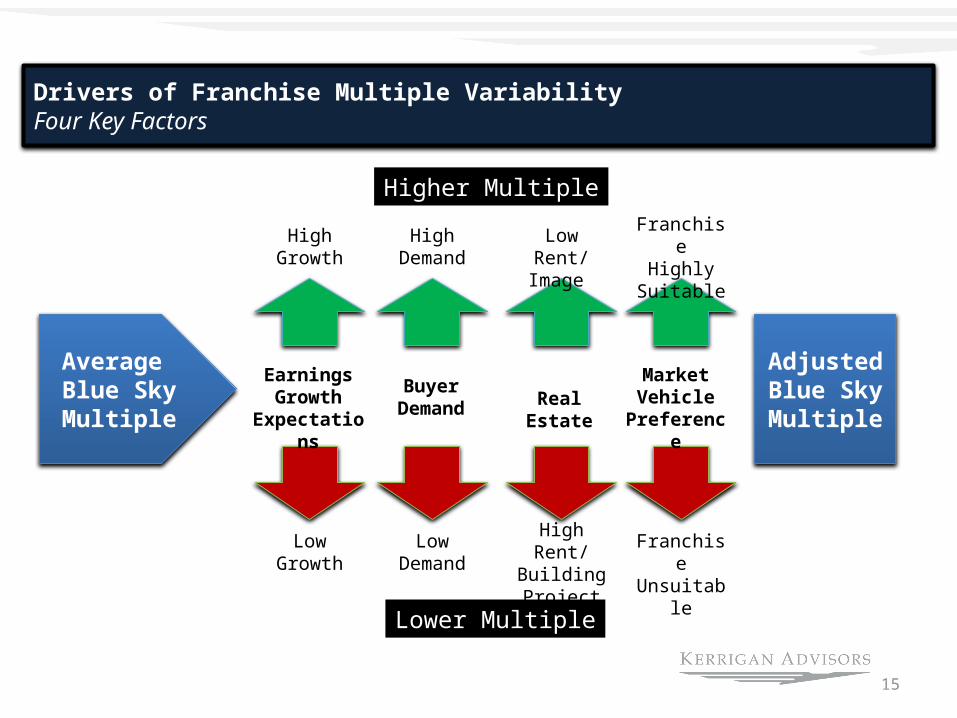

Drivers of Franchise Multiple VariabilityFour Key Factors

Average Blue Sky Multiple

AdjustedBlue Sky Multiple

Earnings Growth

Expectations

Buyer Demand Real Estate

Market Vehicle

Preference

Higher Multiple

Lower Multiple

LowGrowth

LowDemand

High Rent/Building Project

FranchiseUnsuitable

FranchiseHighly

Suitable

HighGrowth

HighDemand

Low Rent/Image

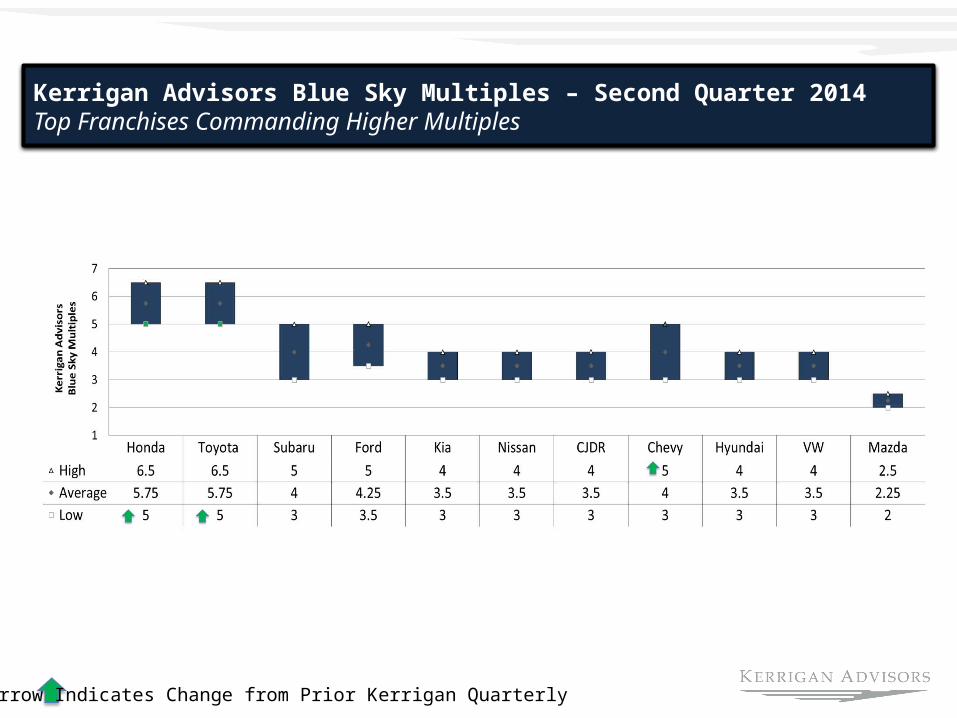

Kerrigan Advisors Blue Sky Multiples – Second Quarter 2014Top Franchises Commanding Higher Multiples

Arrow Indicates Change from Prior Kerrigan Quarterly

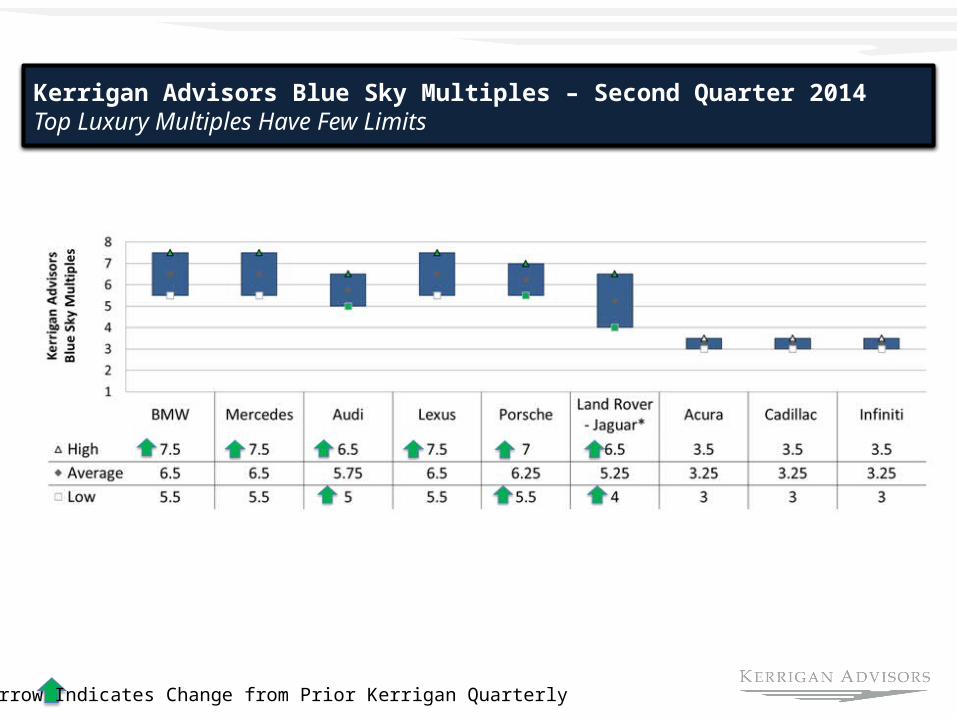

Kerrigan Advisors Blue Sky Multiples – Second Quarter 2014Top Luxury Multiples Have Few Limits

Arrow Indicates Change from Prior Kerrigan Quarterly

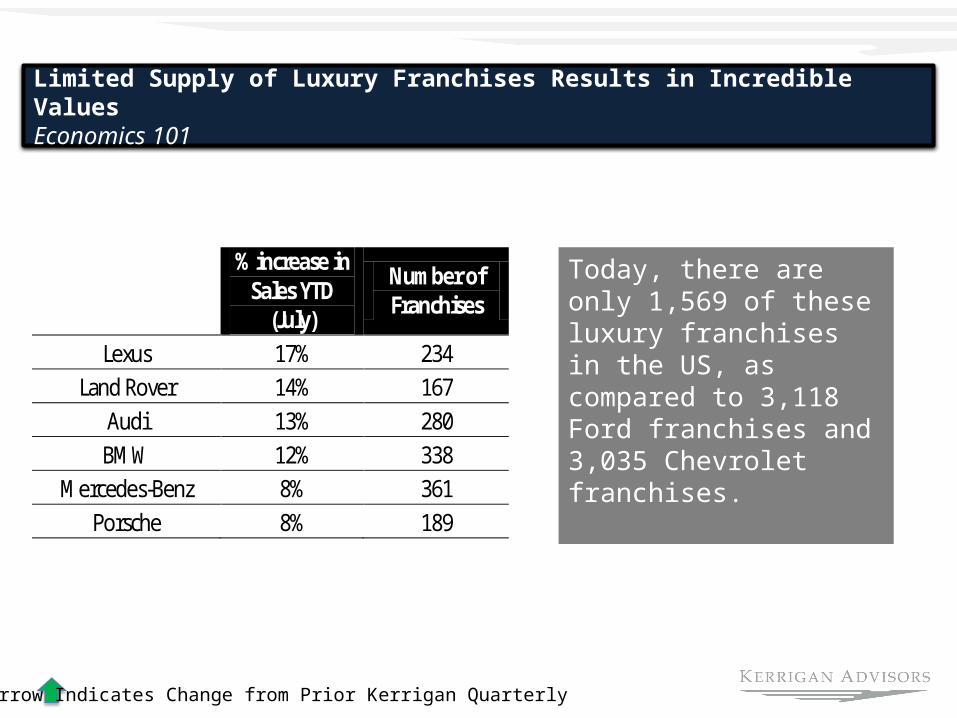

Limited Supply of Luxury Franchises Results in Incredible ValuesEconomics 101

Arrow Indicates Change from Prior Kerrigan Quarterly

% increase in Sales YTD

(July)

Number of Franchises

Lexus 17% 234 Land Rover 14% 167

Audi 13% 280 BMW 12% 338

Mercedes-Benz 8% 361 Porsche 8% 189

Today, there are only 1,569 of these luxury franchises in the US, as compared to 3,118 Ford franchises and 3,035 Chevrolet franchises.

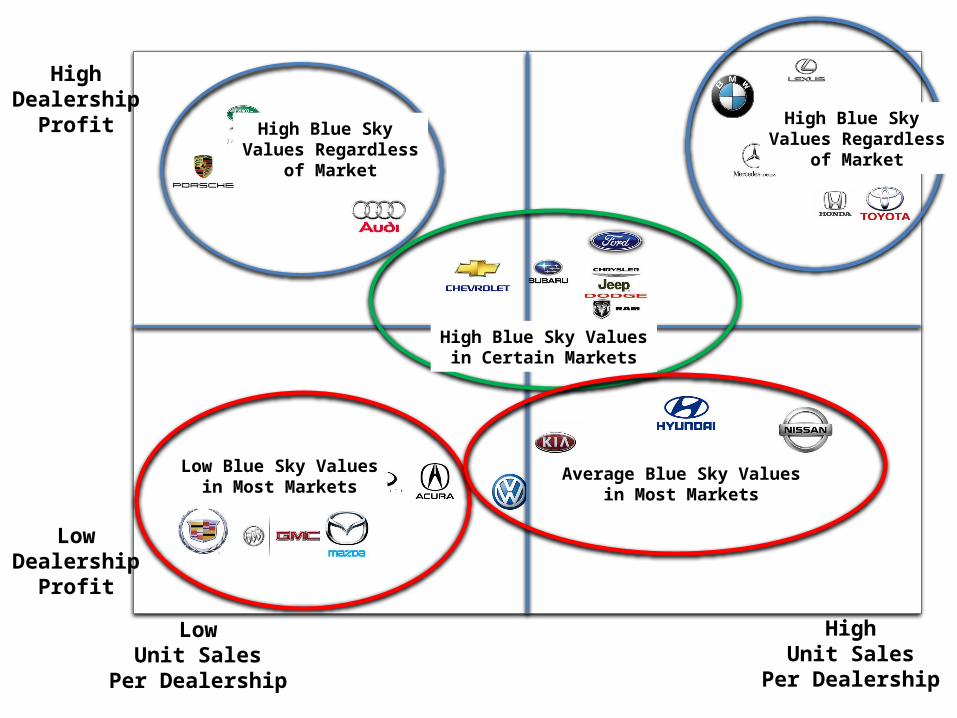

LowUnit Sales

Per Dealership

Some

HighDealership

Profit

LowDealership

Profit

HighUnit Sales

Per Dealership

High Blue Sky Values Regardless

of Market

High Blue Sky Valuesin Certain Markets

High Blue Sky Values Regardless

of Market

Low Blue Sky Valuesin Most Markets

Average Blue Sky Valuesin Most Markets

20

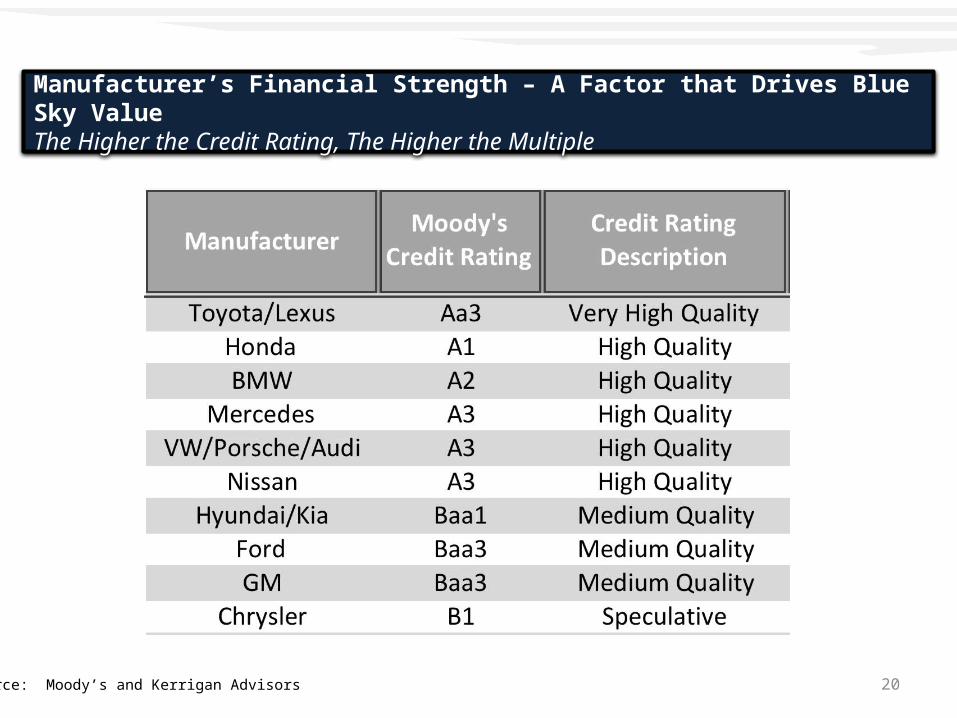

Manufacturer’s Financial Strength – A Factor that Drives Blue Sky ValueThe Higher the Credit Rating, The Higher the Multiple

Source: Moody’s and Kerrigan Advisors

21

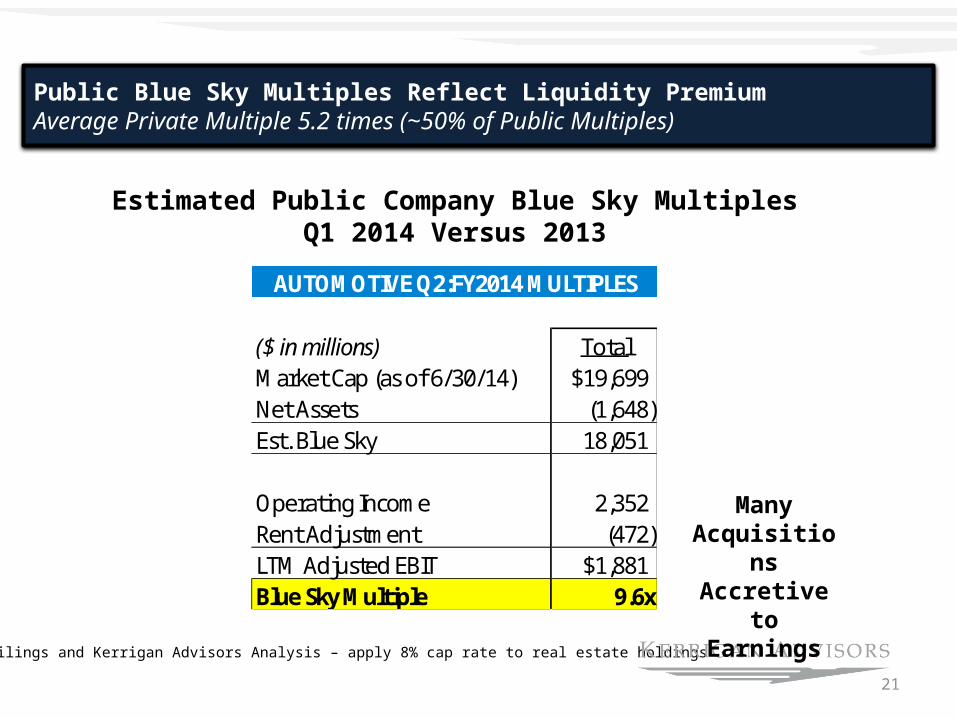

Source: SEC Filings and Kerrigan Advisors Analysis – apply 8% cap rate to real estate holdings

Estimated Public Company Blue Sky MultiplesQ1 2014 Versus 2013

Public Blue Sky Multiples Reflect Liquidity PremiumAverage Private Multiple 5.2 times (~50% of Public Multiples)

AUTOMOTIVE Q2:FY2014 MULTIPLES AUTOMOTIVE Q1:FY2014 MULTIPLES

($ in millions) TotalMarket Cap (as of 6/30/14) $19,699Net Assets (1,648) Est. Blue Sky 18,051

Operating Income 2,352 Rent Adjustment (472) LTM Adjusted EBIT $1,881Blue Sky Multiple 9.6x

Many Acquisitions Accretive to

Earnings

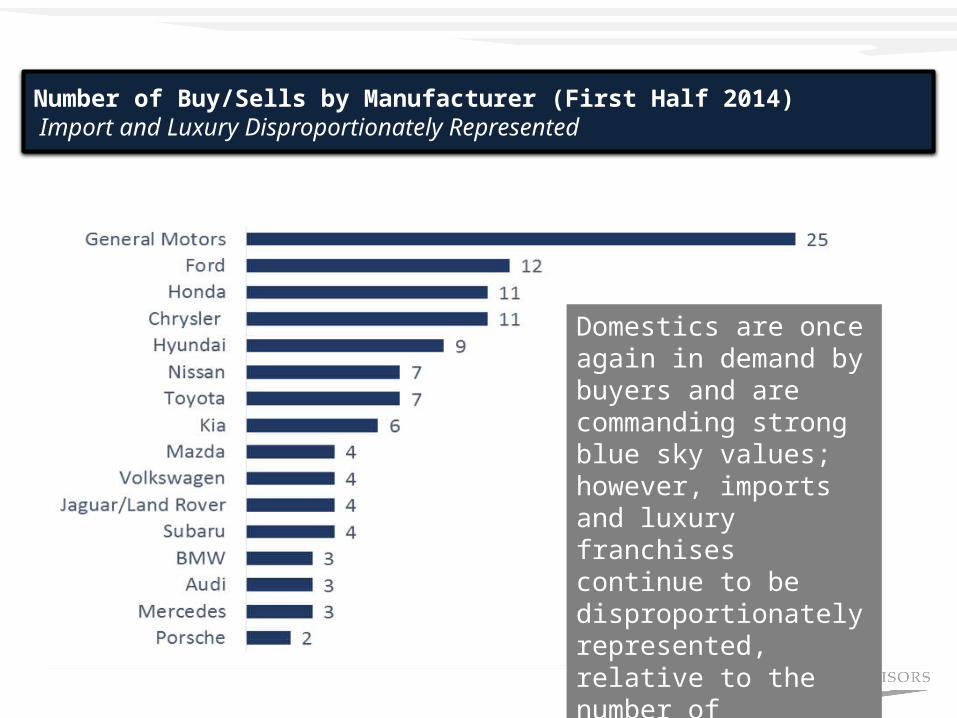

Number of Buy/Sells by Manufacturer (First Half 2014) Import and Luxury Disproportionately Represented

Domestics are once again in demand by buyers and are commanding strong blue sky values; however, imports and luxury franchises continue to be disproportionately represented, relative to the number of franchises.

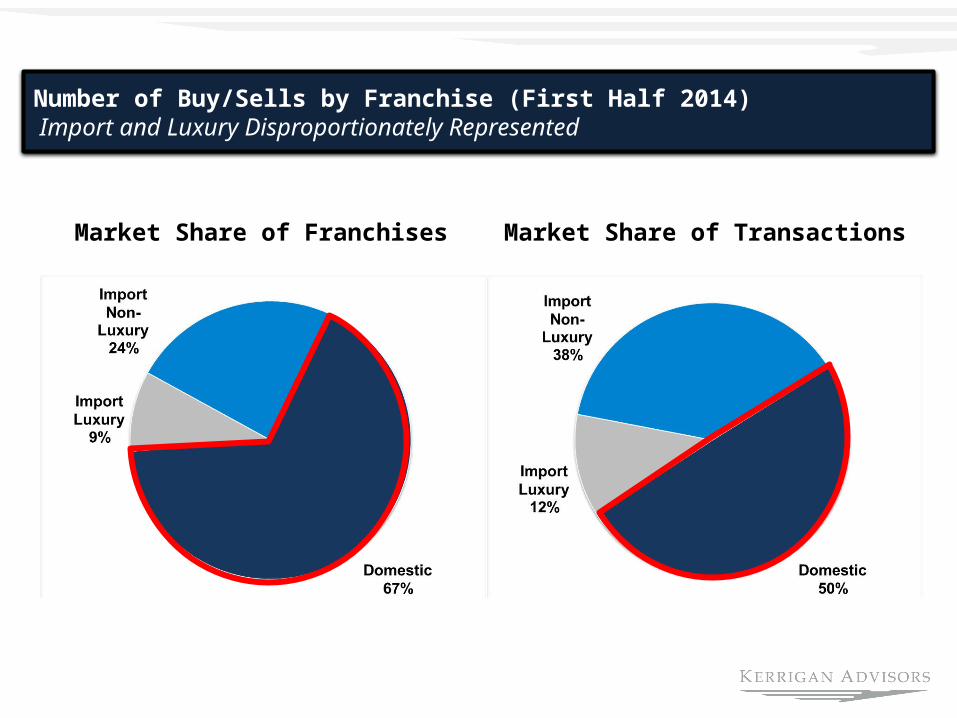

Number of Buy/Sells by Franchise (First Half 2014) Import and Luxury Disproportionately Represented

Market Share of Franchises Market Share of Transactions

24

Buyers Well Positioned With Lots of Support

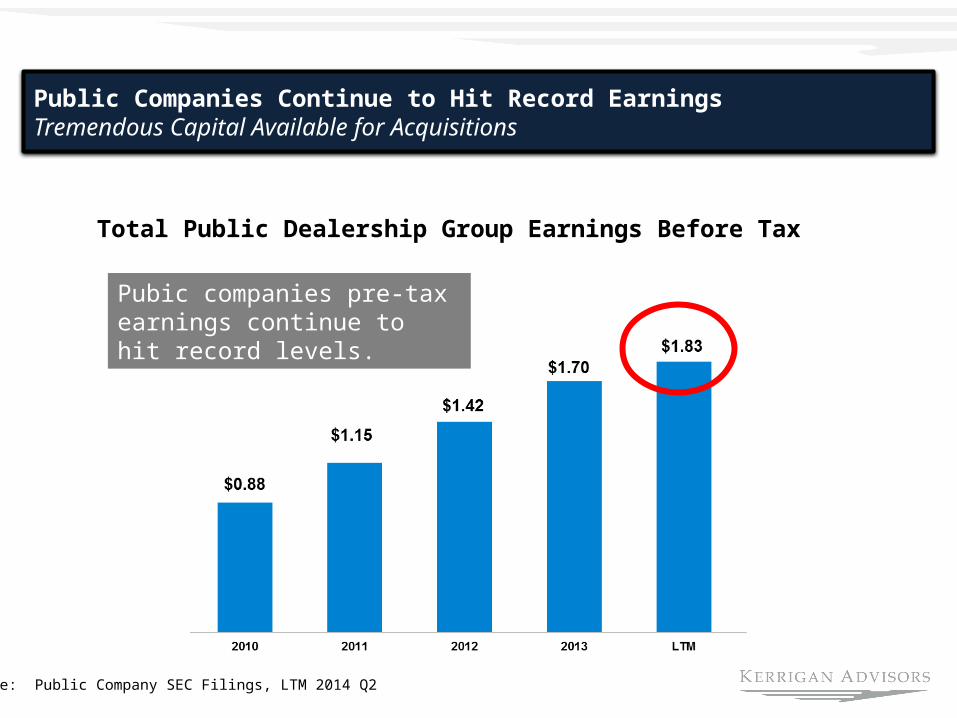

Public Companies Continue to Hit Record Earnings Tremendous Capital Available for Acquisitions

Source: Public Company SEC Filings, LTM 2014 Q2

Total Public Dealership Group Earnings Before Tax

Pubic companies pre-tax earnings continue to hit record levels.

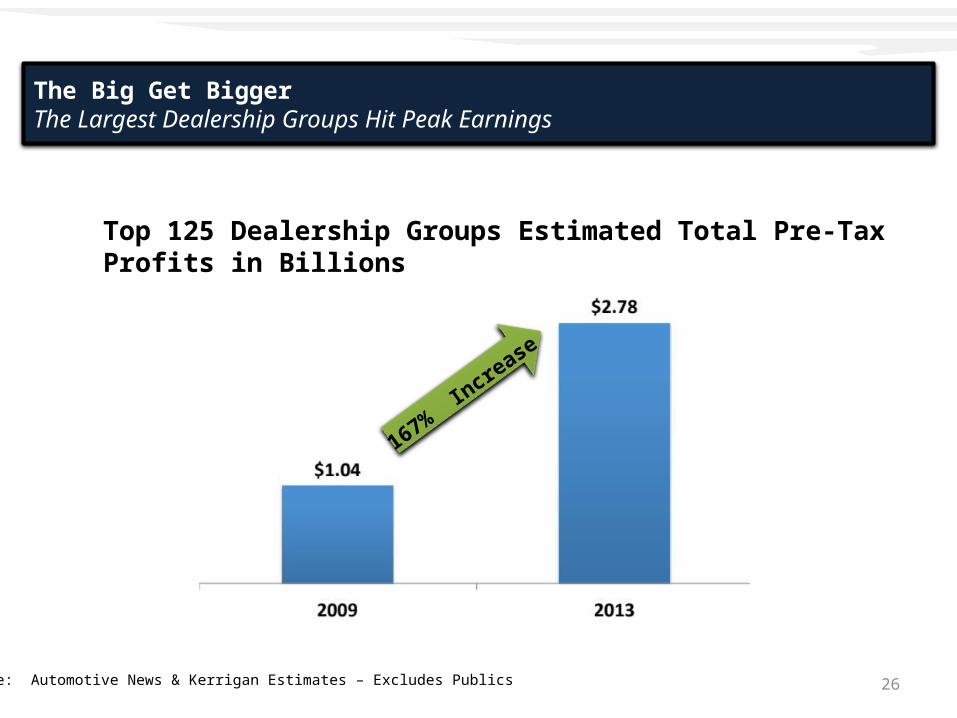

26Source: Automotive News & Kerrigan Estimates – Excludes Publics

Top 125 Dealership Groups Estimated Total Pre-Tax Profits in Billions

167% Increase

The Big Get BiggerThe Largest Dealership Groups Hit Peak Earnings

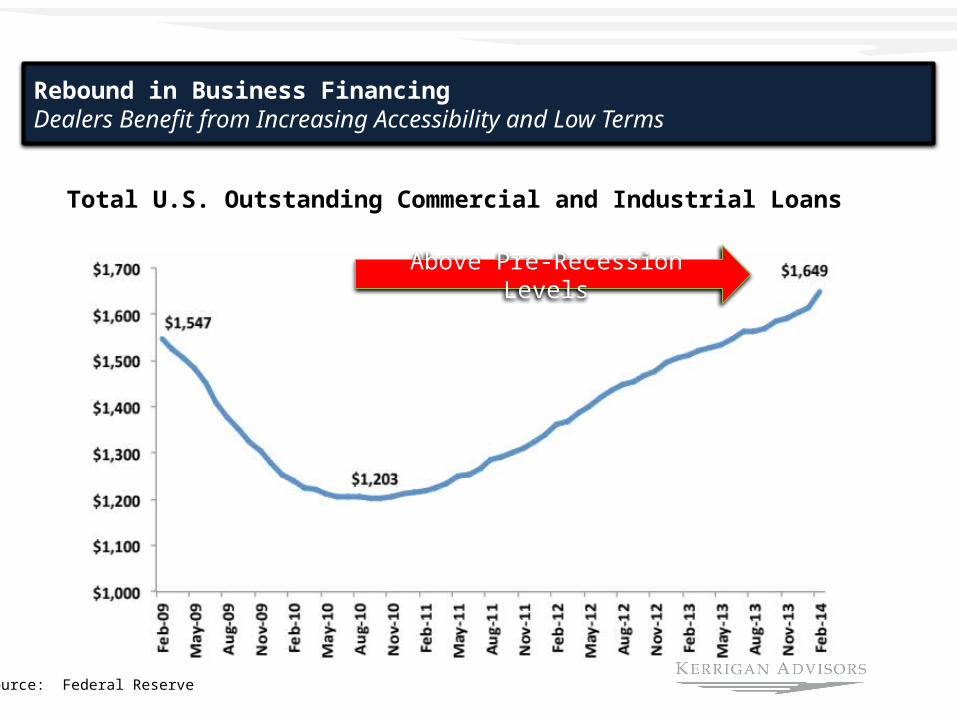

Rebound in Business FinancingDealers Benefit from Increasing Accessibility and Low Terms

Source: Federal Reserve

Total U.S. Outstanding Commercial and Industrial Loans

Above Pre-Recession Levels

28

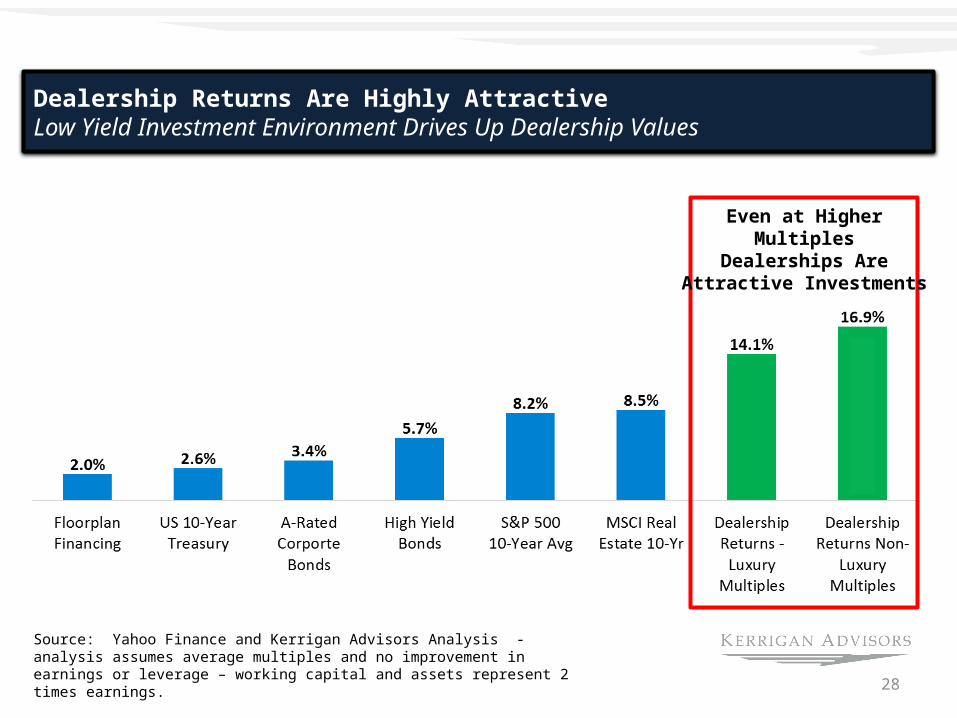

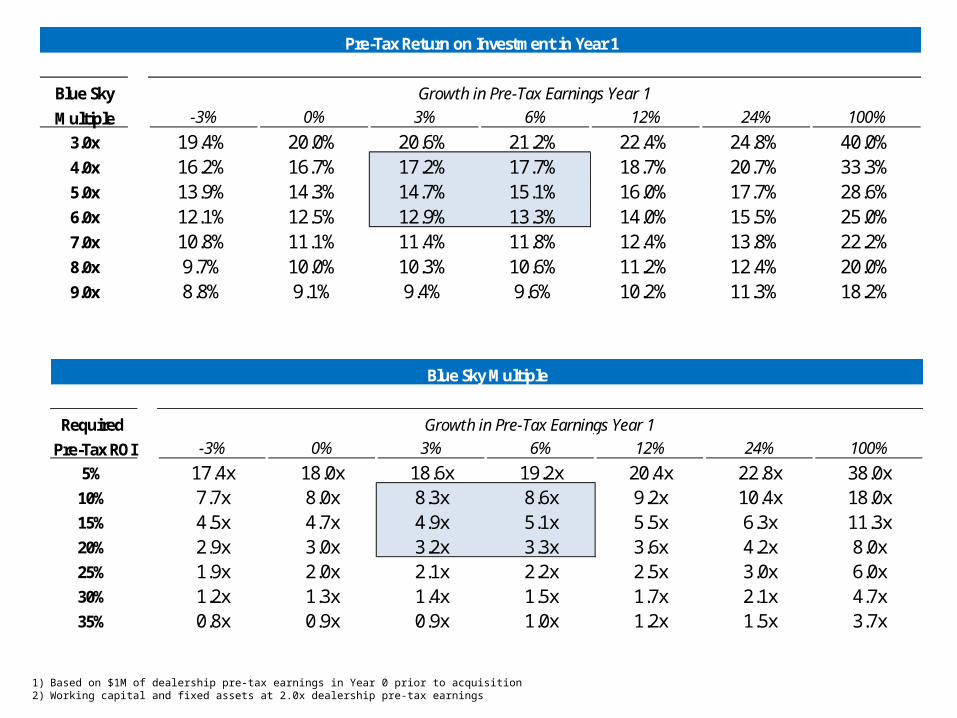

Dealership Returns Are Highly AttractiveLow Yield Investment Environment Drives Up Dealership Values

Source: Yahoo Finance and Kerrigan Advisors Analysis - analysis assumes average multiples and no improvement in earnings or leverage – working capital and assets represent 2 times earnings.

Even at Higher MultiplesDealerships Are Attractive

Investments

1) Based on $1M of dealership pre-tax earnings in Year 0 prior to acquisition 2) Working capital and fixed assets at 2.0x dealership pre-tax earnings

Pre-Tax Return on Investment in Year 1

Blue Sky Growth in Pre-Tax Earnings Year 1Multiple # -3% 0% 3% 6% 12% 24% 100%

3.0x ## 19.4% 20.0% 20.6% 21.2% 22.4% 24.8% 40.0%4.0x ## 16.2% 16.7% 17.2% 17.7% 18.7% 20.7% 33.3%5.0x ## 13.9% 14.3% 14.7% 15.1% 16.0% 17.7% 28.6%6.0x ## 12.1% 12.5% 12.9% 13.3% 14.0% 15.5% 25.0%7.0x ## 10.8% 11.1% 11.4% 11.8% 12.4% 13.8% 22.2%8.0x ## 9.7% 10.0% 10.3% 10.6% 11.2% 12.4% 20.0%9.0x ## 8.8% 9.1% 9.4% 9.6% 10.2% 11.3% 18.2%

10.0x ## 8.1% 8.3% 8.6% 8.8% 9.3% 10.3% 16.7%

Blue Sky Multiple

Required Growth in Pre-Tax Earnings Year 1Pre-Tax ROI # -3% 0% 3% 6% 12% 24% 100%

5% ## 17.4x 18.0x 18.6x 19.2x 20.4x 22.8x 38.0x10% ## 7.7x 8.0x 8.3x 8.6x 9.2x 10.4x 18.0x15% ## 4.5x 4.7x 4.9x 5.1x 5.5x 6.3x 11.3x20% ## 2.9x 3.0x 3.2x 3.3x 3.6x 4.2x 8.0x25% ## 1.9x 2.0x 2.1x 2.2x 2.5x 3.0x 6.0x30% ## 1.2x 1.3x 1.4x 1.5x 1.7x 2.1x 4.7x35% ## 0.8x 0.9x 0.9x 1.0x 1.2x 1.5x 3.7x

30

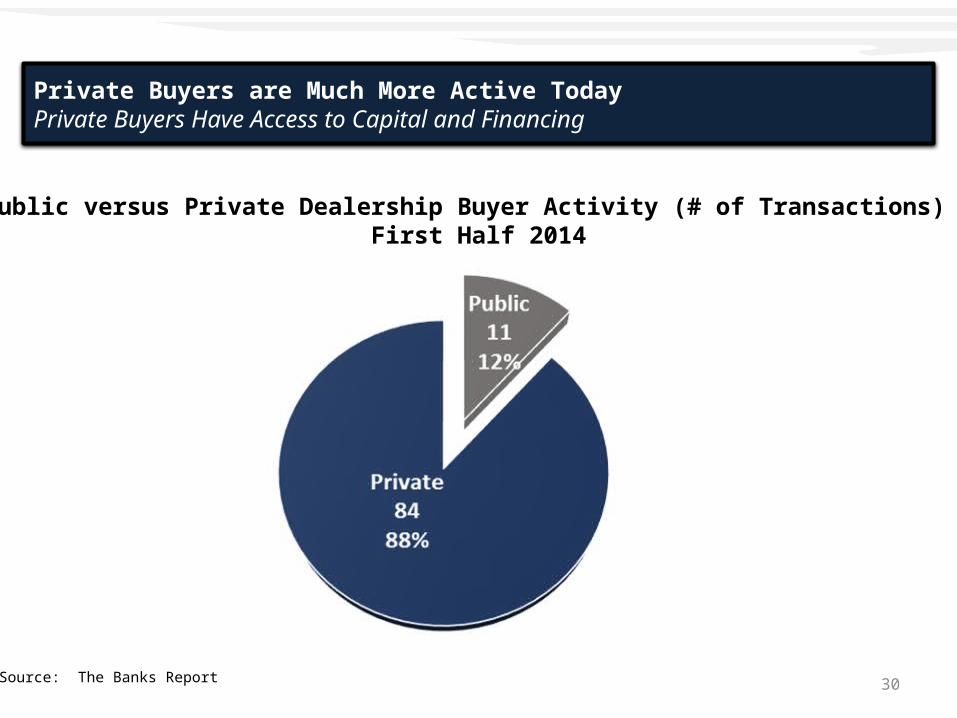

Private Buyers are Much More Active TodayPrivate Buyers Have Access to Capital and Financing

Source: The Banks Report

Public versus Private Dealership Buyer Activity (# of Transactions) First Half 2014

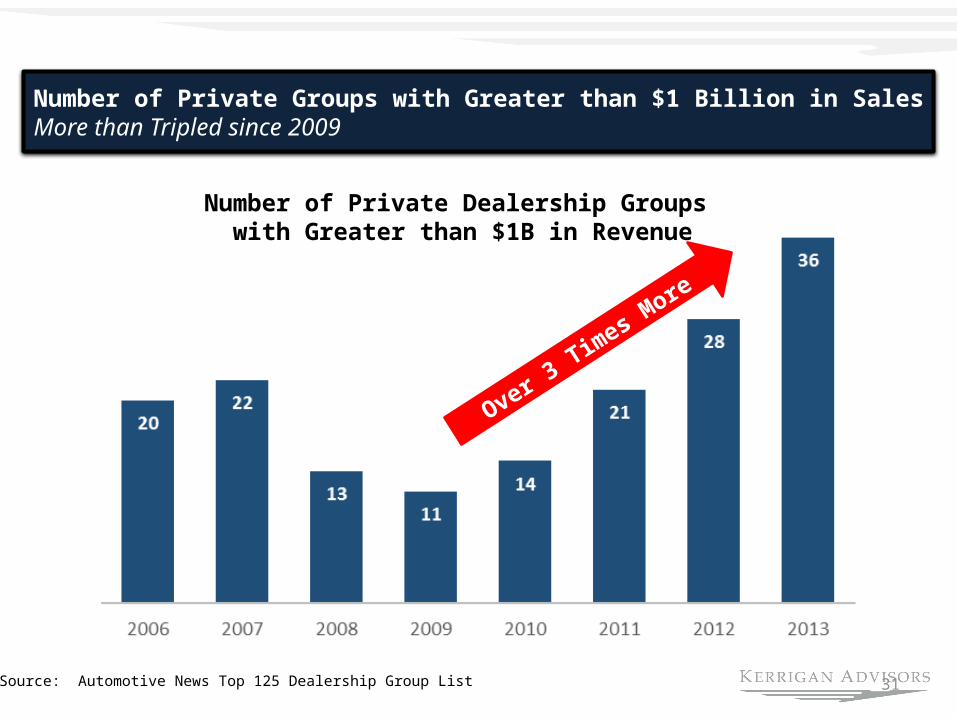

Number of Private Groups with Greater than $1 Billion in SalesMore than Tripled since 2009

31Source: Automotive News Top 125 Dealership Group List

Number of Private Dealership Groups with Greater than $1B in Revenue

Over 3 Times More

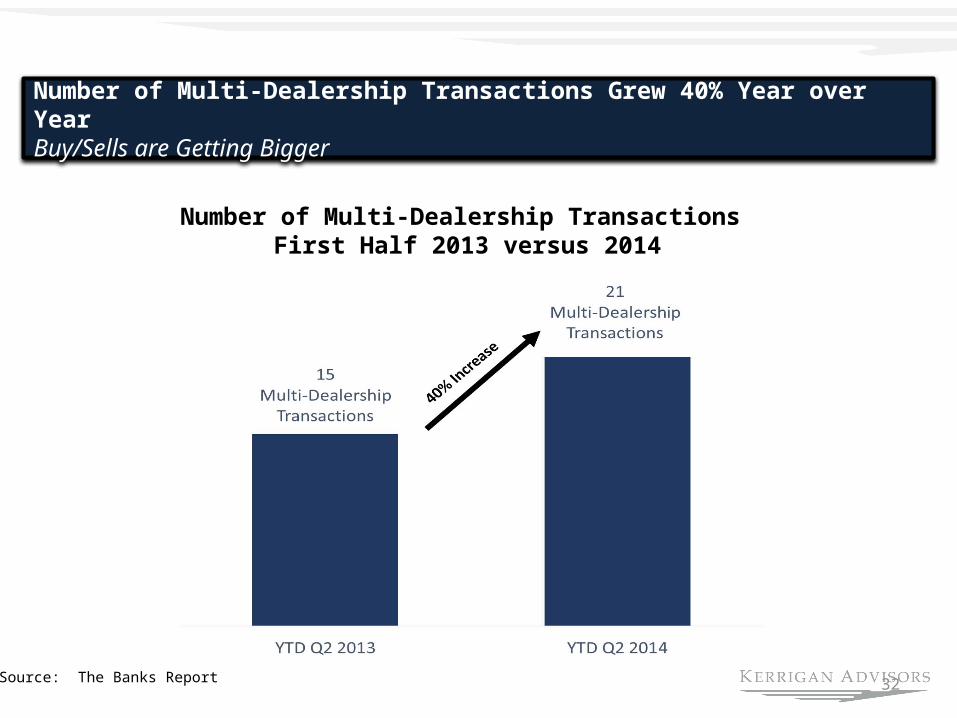

Number of Multi-Dealership Transactions Grew 40% Year over YearBuy/Sells are Getting Bigger

32Source: The Banks Report

Number of Multi-Dealership Transactions First Half 2013 versus 2014

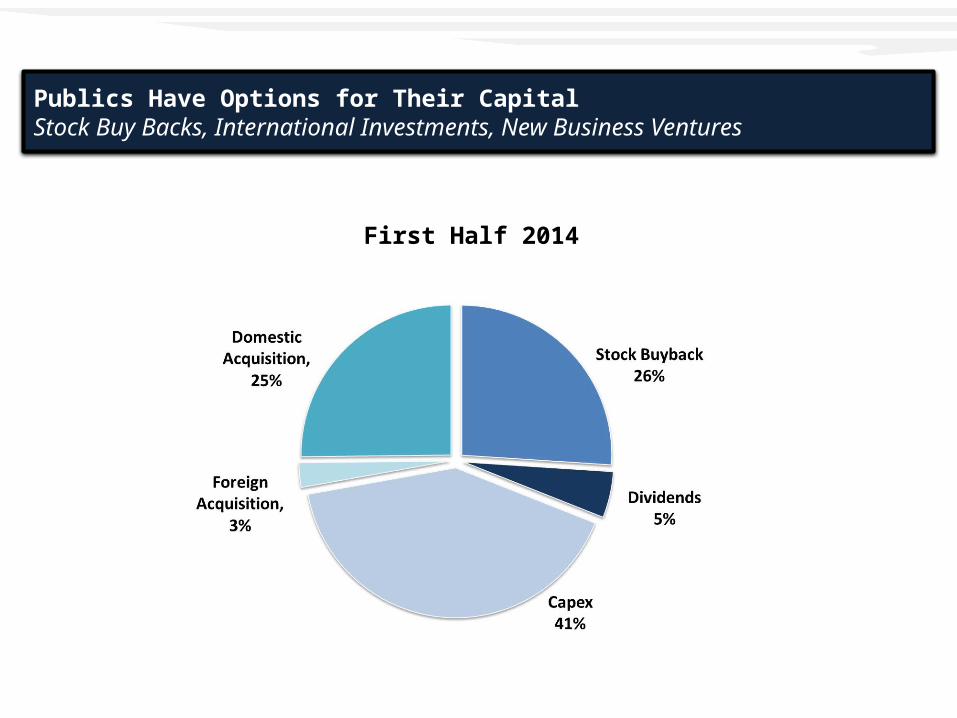

Publics Have Options for Their CapitalStock Buy Backs, International Investments, New Business Ventures

First Half 2014

34

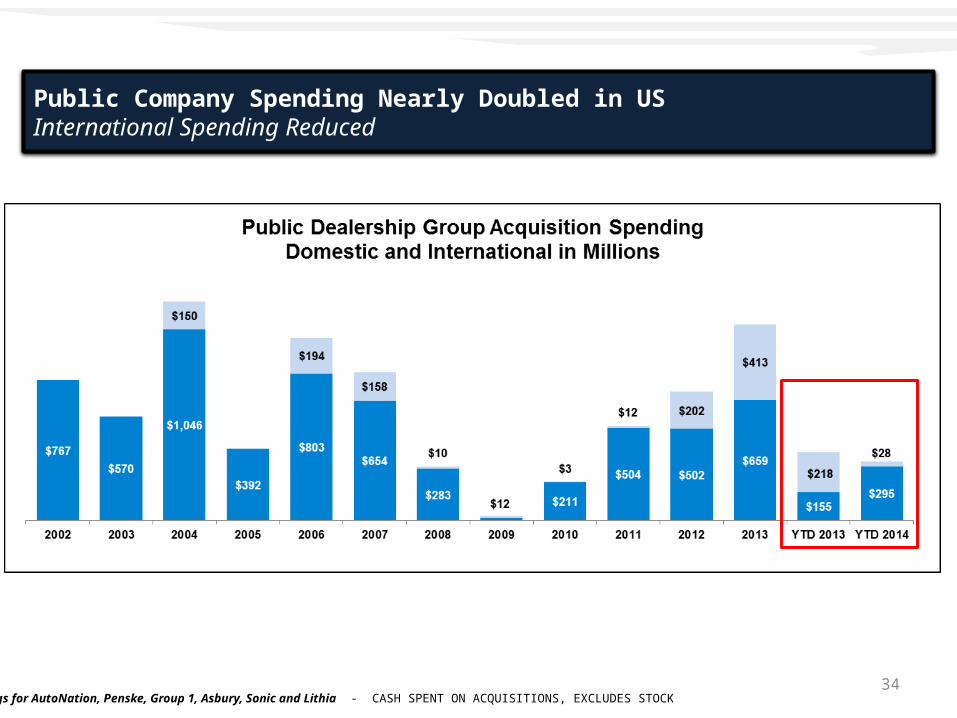

Public Company Spending Nearly Doubled in USInternational Spending Reduced

SEC Filings for AutoNation, Penske, Group 1, Asbury, Sonic and Lithia - CASH SPENT ON ACQUISITIONS, EXCLUDES STOCK

Source: Public SEC Filings

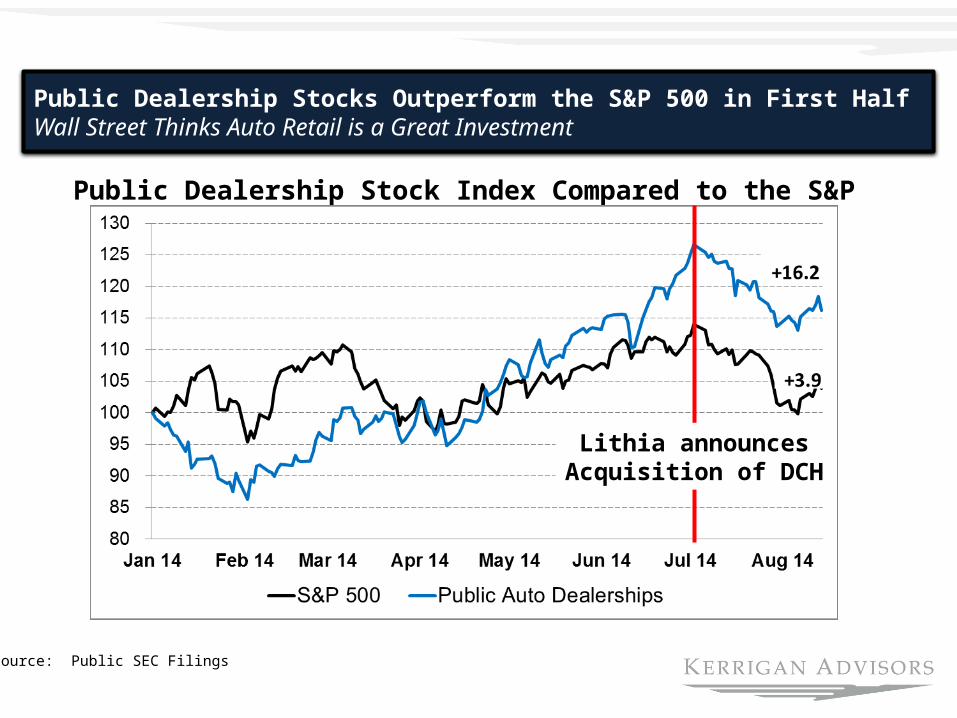

Public Dealership Stock Index Compared to the S&P

Public Dealership Stocks Outperform the S&P 500 in First HalfWall Street Thinks Auto Retail is a Great Investment

Lithia announcesAcquisition of DCH

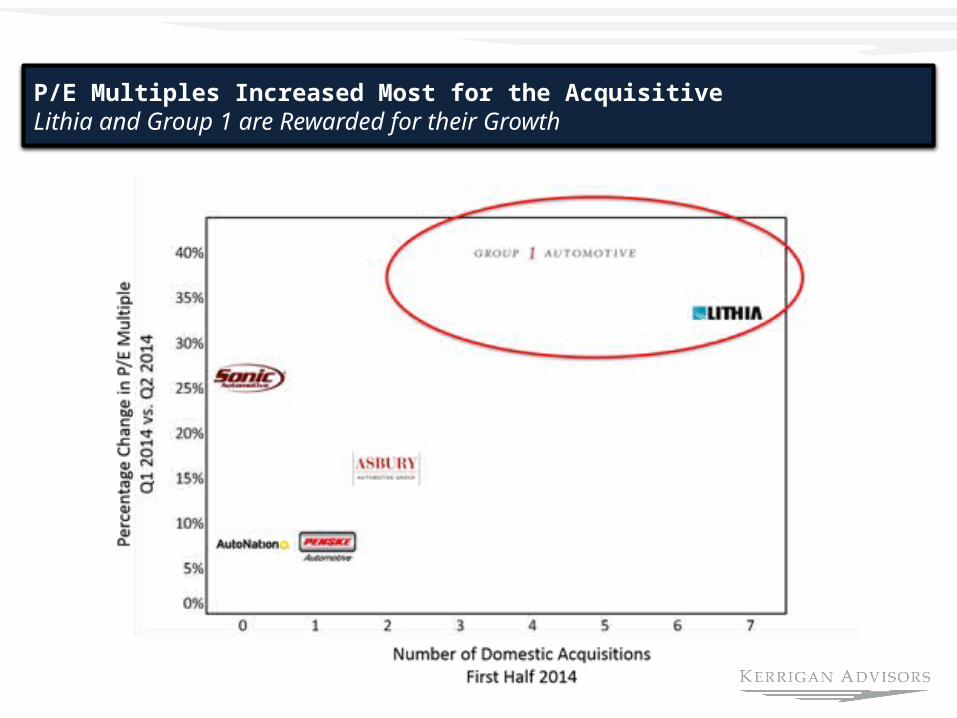

P/E Multiples Increased Most for the AcquisitiveLithia and Group 1 are Rewarded for their Growth

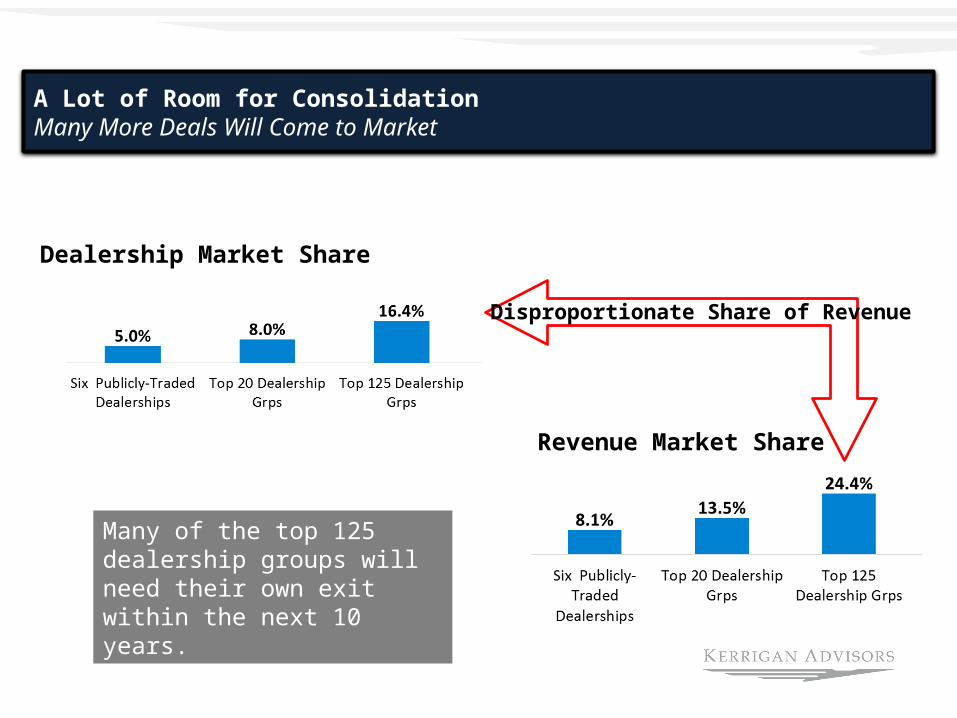

A Lot of Room for ConsolidationMany More Deals Will Come to Market

Revenue Market Share

Dealership Market Share

Many of the top 125 dealership groups will need their own exit within the next 10 years.

Disproportionate Share of Revenue

38

Sellers Are Enjoying a Great Winning Streak

Dealer Optimism IndexBeing a Dealer Still the Happiest Place on Earth – But Not As Happy as 2011

39Source: NADA

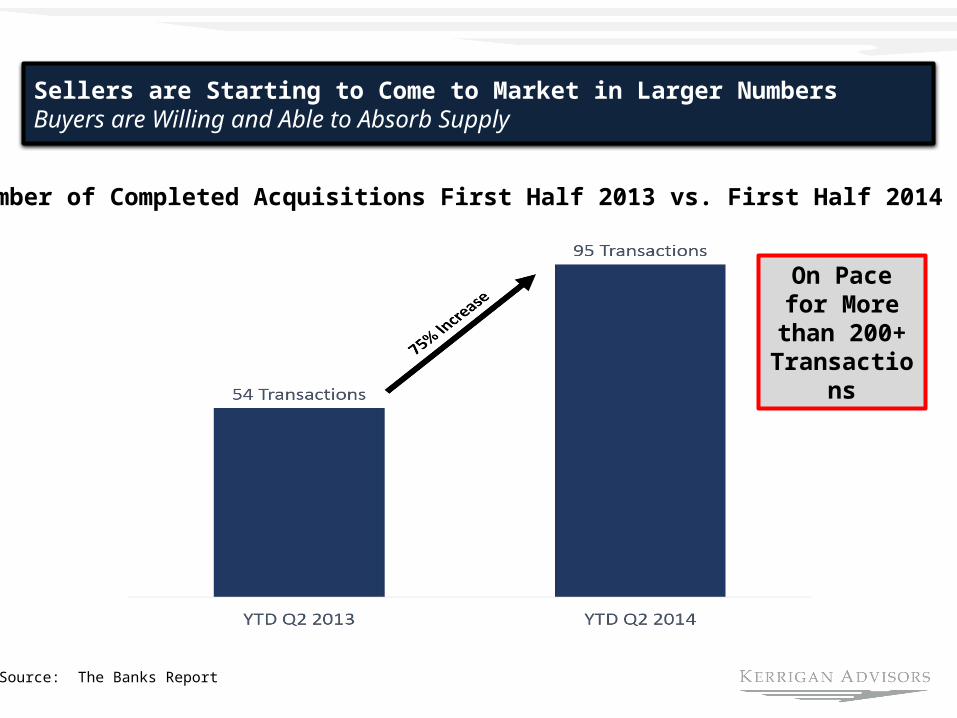

Sellers are Starting to Come to Market in Larger NumbersBuyers are Willing and Able to Absorb Supply

Source: The Banks Report

Number of Completed Acquisitions First Half 2013 vs. First Half 2014

On Pace for More than

200+ Transactions

41

17 Million Peak Sales Means Slower Growth Sales Rebound Near Completion

Source: Automotive News and Kerrigan Advisors Analysis/Estimates

42

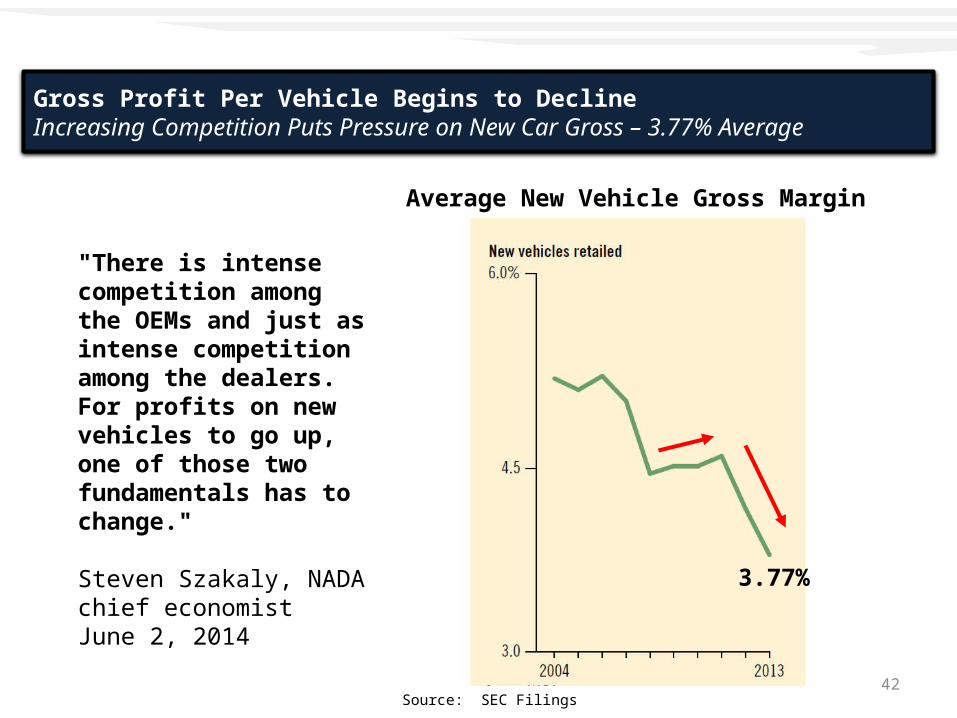

Gross Profit Per Vehicle Begins to DeclineIncreasing Competition Puts Pressure on New Car Gross – 3.77% Average

Source: SEC Filings

Average New Vehicle Gross Margin

"There is intense competition among the OEMs and just as intense competition among the dealers. For profits on new vehicles to go up, one of those two fundamentals has to change."

Steven Szakaly, NADA chief economist June 2, 2014 3.77%

43

Average Dealership Earnings Near Peak LevelsGrowth Slowing

Source: NADA and Kerrigan Advisors Analysis – 2014E based on First Half Results

Average Dealership Earnings Vs. Annual Earnings Growth Rate

44

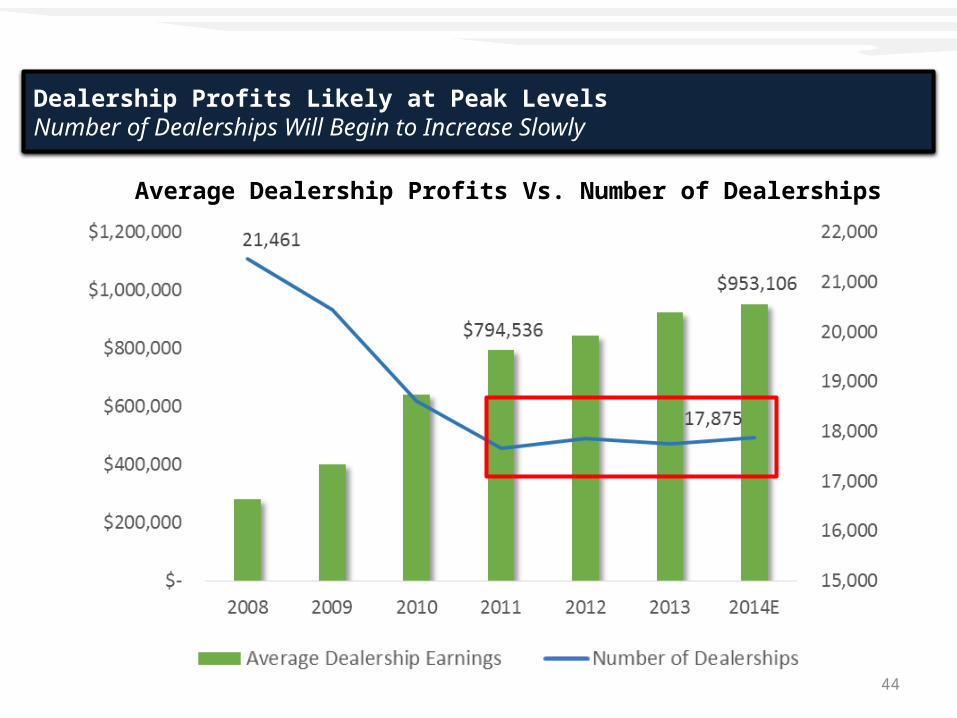

Dealership Profits Likely at Peak LevelsNumber of Dealerships Will Begin to Increase Slowly

Average Dealership Profits Vs. Number of Dealerships

45

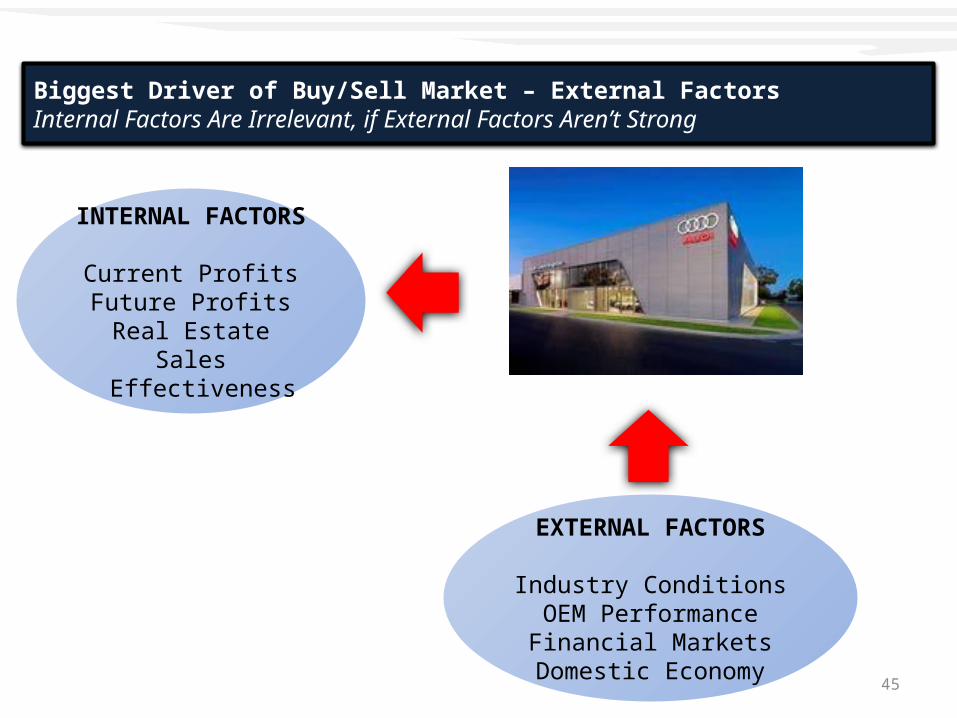

EXTERNAL FACTORS

Industry ConditionsOEM PerformanceFinancial Markets

Domestic Economy

INTERNAL FACTORS

Current ProfitsFuture Profits

Real EstateSales Effectiveness

Source: NADA

Biggest Driver of Buy/Sell Market – External FactorsInternal Factors Are Irrelevant, if External Factors Aren’t Strong

46

47

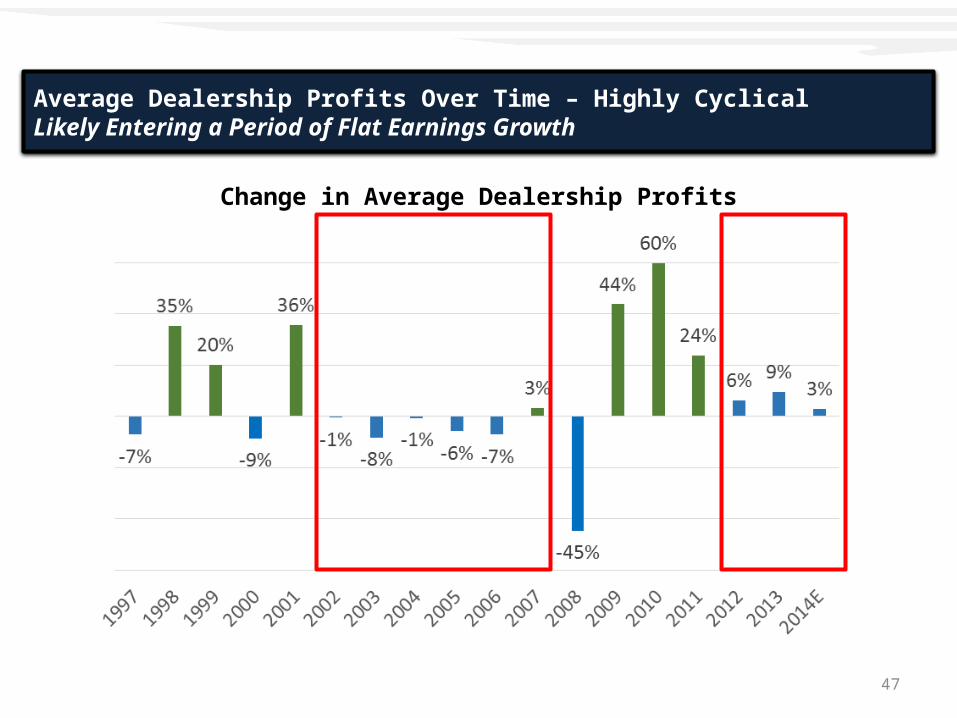

Average Dealership Profits Over Time – Highly CyclicalLikely Entering a Period of Flat Earnings Growth

Change in Average Dealership Profits

48

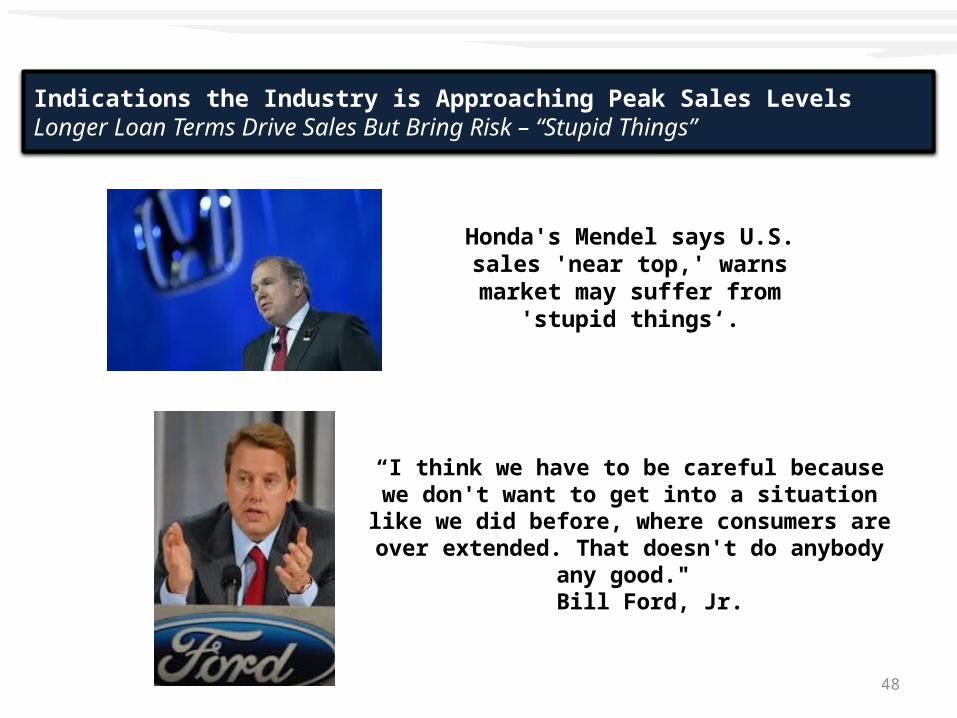

Honda's Mendel says U.S. sales 'near top,' warns market may suffer

from 'stupid things‘.

“I think we have to be careful because we don't want to get into a situation like we did before, where consumers are over extended.

That doesn't do anybody any good." Bill Ford, Jr.

Indications the Industry is Approaching Peak Sales LevelsLonger Loan Terms Drive Sales But Bring Risk – “Stupid Things”

49

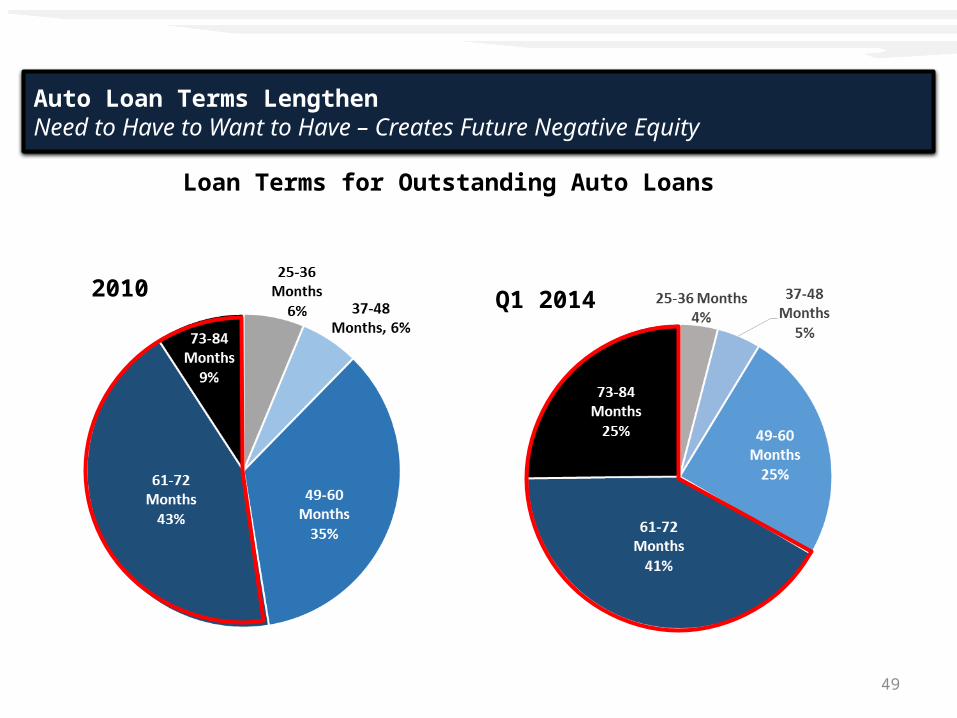

Auto Loan Terms LengthenNeed to Have to Want to Have – Creates Future Negative Equity

Loan Terms for Outstanding Auto Loans

2010 Q1 2014

50

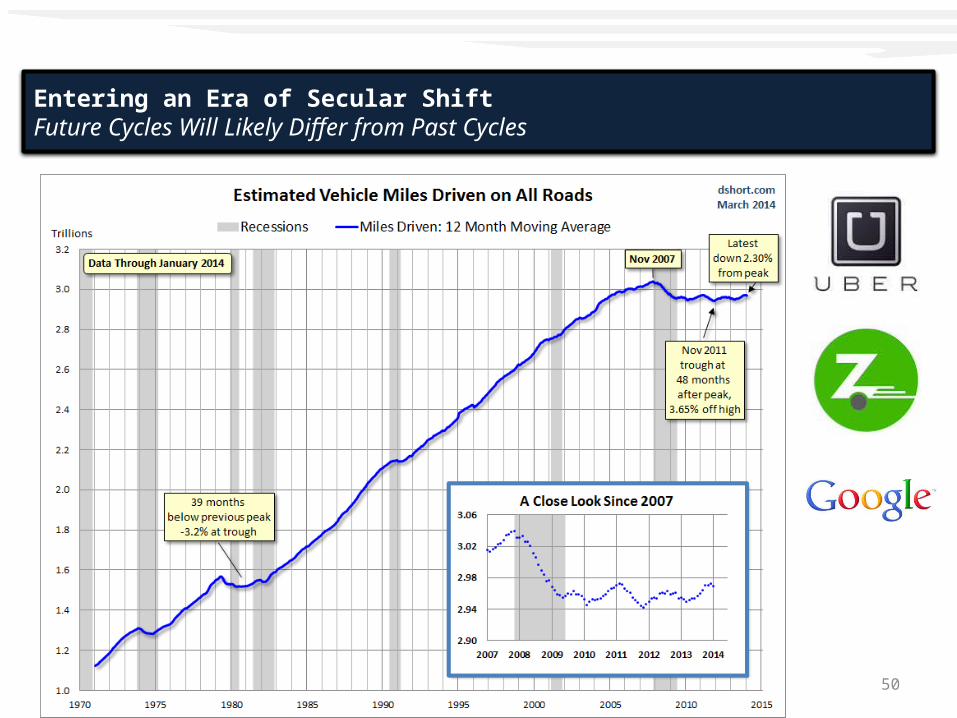

Entering an Era of Secular Shift Future Cycles Will Likely Differ from Past Cycles

51

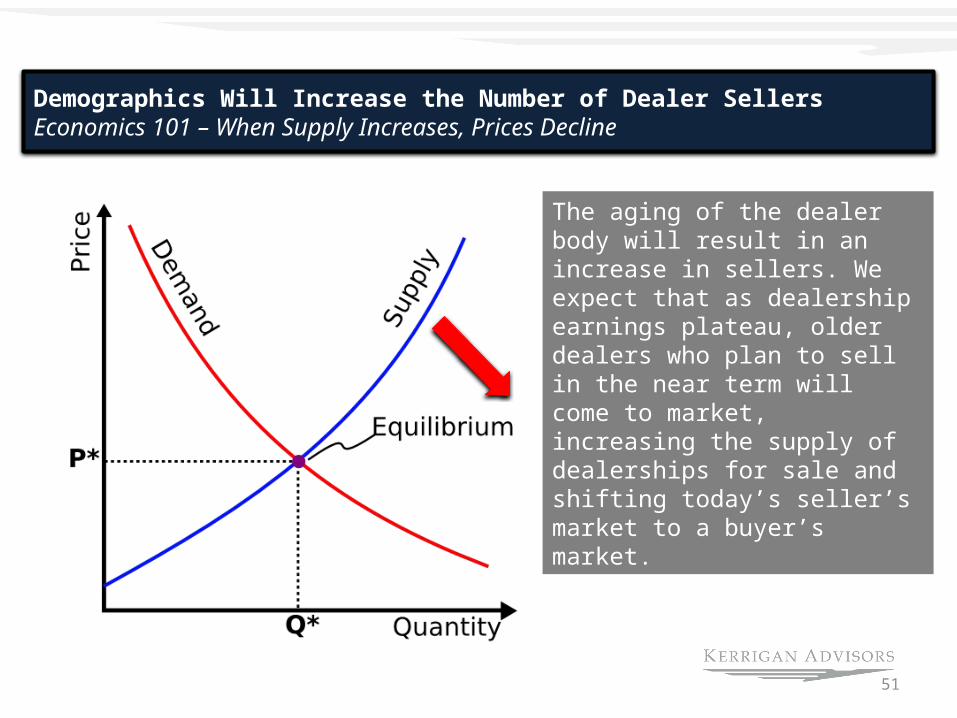

Demographics Will Increase the Number of Dealer SellersEconomics 101 – When Supply Increases, Prices Decline

The aging of the dealer body will result in an increase in sellers. We expect that as dealership earnings plateau, older dealers who plan to sell in the near term will come to market, increasing the supply of dealerships for sale and shifting today’s seller’s market to a buyer’s market.

52

Q & A

53

Erin Kerrigan, Founder and Managing Director

Today’s Auto Retail MarketBuyers’ Considerations Sellers’ ConsiderationsThe Presidio Blue Sky MultiplesValuation MethodsQ&A

Today’s Auto Retail MarketBuyers’ Considerations Sellers’ ConsiderationsThe Presidio Blue Sky MultiplesValuation MethodsQ&A

Erin Kerrigan is Managing Director of Kerrigan Advisors, which she founded in 2014. Kerrigan Advisors is a national dealership brokerage firm focused on providing a limited number of sellers, a high level of client service. Prior to founding Kerrigan Advisors, Ms. Kerrigan headed Presidio Automotive. During her time at Presidio, the firm represented dealer clients in numerous multi-million dollar transactions. Prior to Presidio, she was a Senior Vice President at AutoStar, a subsidiary of iStar Financial (NYSE: SFI), where she led transaction origination. Ms. Kerrigan is a recognized industry expert on dealership valuation, real estate and buy/sells, and is a frequent speaker at leading auto retail events and conferences, including NADA (#1 speaker in 2012), American Institute of Certified Public Accountants (AICPA), National Association of Dealer Counsel (NADC), Auto Team America’s Buy/Sell Summit and DrivingSales’ President’s Club. She has also been a key note speaker for events hosted by American Honda Motor Company, Audi of America, Bank of America, US Trust, Ohio Automobile Dealer Association, Colorado Automobile Dealer Association, and SunTrust Bank. Ms. Kerrigan has also led webinars for NADA and Automotive News and she writes a monthly column for Dealer Magazine.

Ms. Kerrigan graduated from Northwestern University with a BA in History and International Studies and the UCLA Anderson School of Business with an MBA. She is a member of Northwestern University’s Council of One Hundred, a select group of leading female professional alumnae who mentor current students and alumnae. She lives in Newport Beach, California with her husband and three children.

Erin KerriganFounder and Managing PartnerKerrigan Advisors [email protected] (office)949-439-6768 (cell)