Embed Size (px)

Citation preview

+

The Principles of Valuation of Merges and Takeovers

AOL-Time Warner Analysis

Chompunud Phiromjit 15659

Thi Trang Nhung Nguyen 15714

Thien Ai Nguyen 15838

+Agenda

Definition

Types of Merger and Acquisition

Motives for Merger and Acquisition

Mechanics of a Merger

Merger Gains and Cost

Q&A

2

+Definition

Merger: Two relative equal-sized companies mutually decide

to pool their interest to form a single corporation

33

+Definition

Acquisition: when companies purchase one another, sometimes under

hostile circumstance

4

+Types of M&A

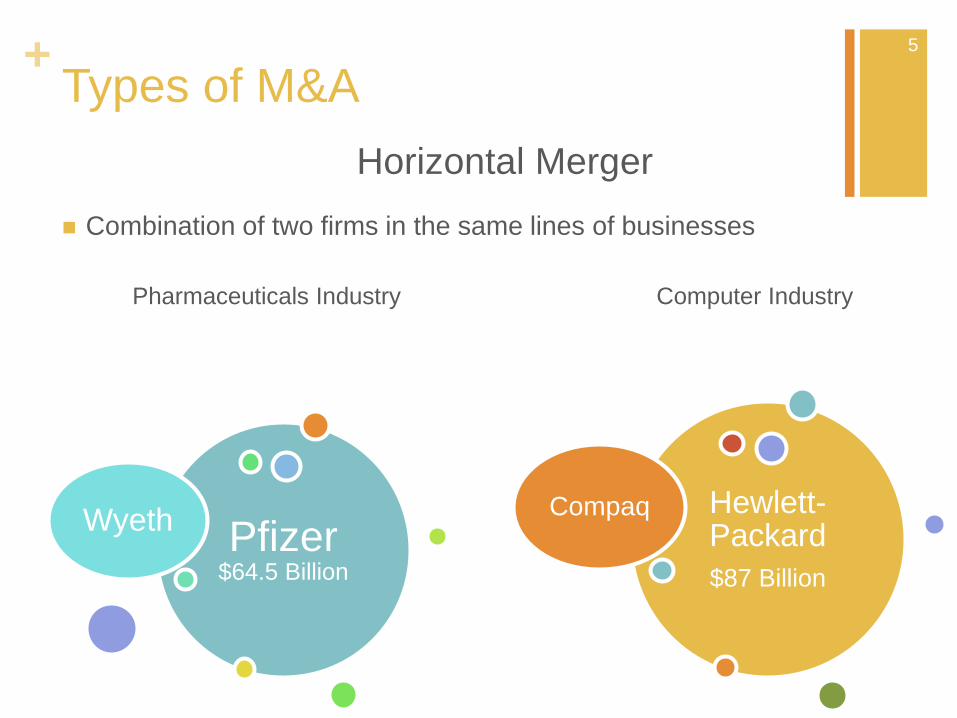

Pfizer $64.5 Billion

Wyeth

Horizontal Merger

Combination of two firms in the same lines of businesses

Pharmaceuticals Industry Computer Industry

Hewlett-Packard

$87 Billion

Compaq

5

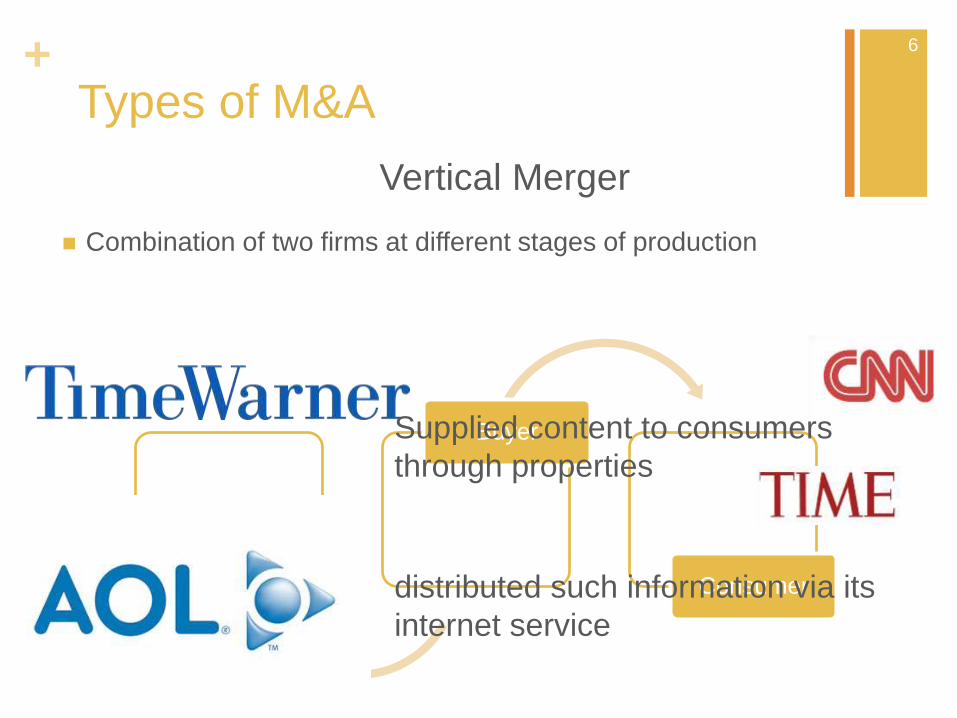

+Types of M&A

Vertical Merger

Combination of two firms at different stages of production

Source of Raw Materials

Buyer

Consumer

Supplied content to consumers

through properties

distributed such information via its

internet service

6

+Types of M&A

Conglomerate Merger

Combination of two firms in unrelated lines of businesses

7

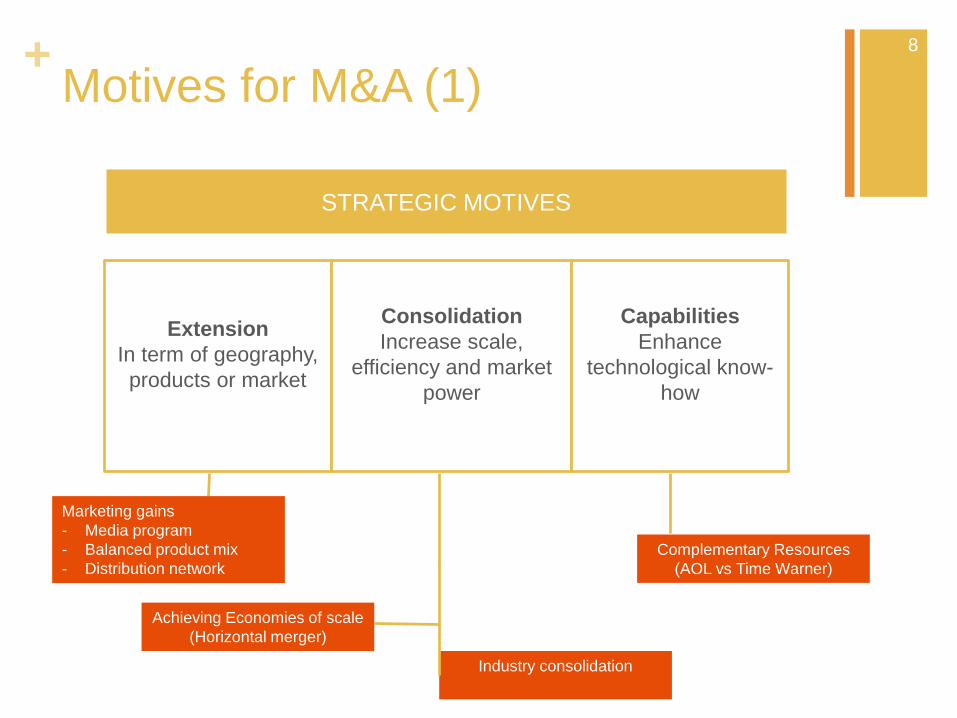

+Motives for M&A (1)

STRATEGIC MOTIVES

Extension

In term of geography,

products or market

Consolidation

Increase scale,

efficiency and market

power

Capabilities

Enhance

technological know-

how

8

Achieving Economies of scale

(Horizontal merger)

Industry consolidation

Complementary Resources

(AOL vs Time Warner)

Marketing gains

- Media program

- Balanced product mix

- Distribution network

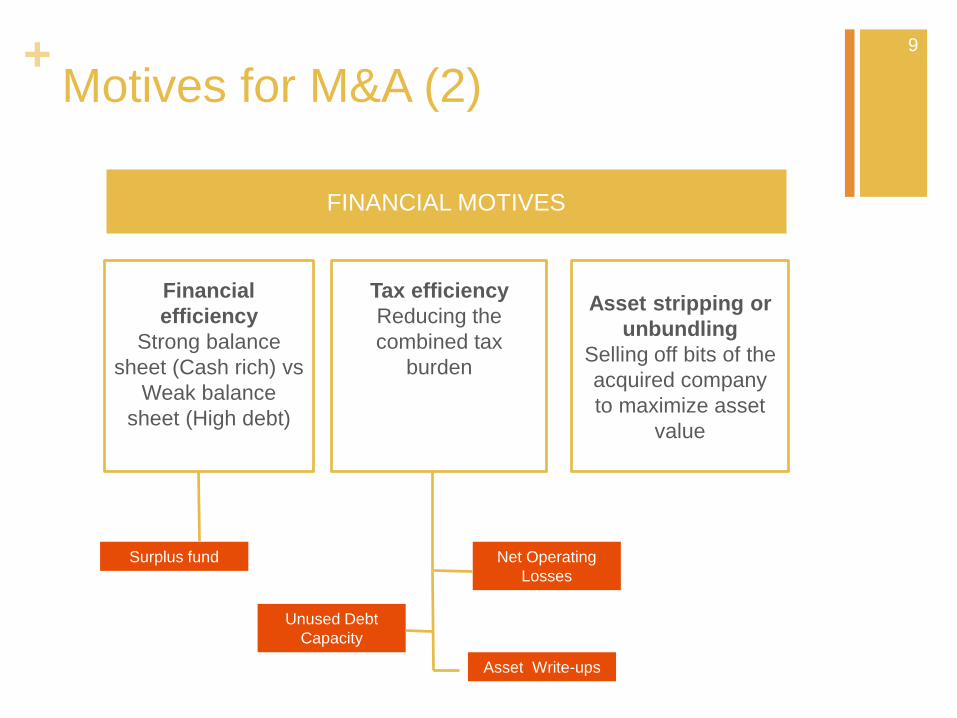

+Motives for M&A (2)

FINANCIAL MOTIVES

Financial

efficiency

Strong balance

sheet (Cash rich) vs

Weak balance

sheet (High debt)

Tax efficiency

Reducing the

combined tax

burden

Asset stripping or

unbundling

Selling off bits of the

acquired company

to maximize asset

value

9

Surplus fund Net Operating

Losses

Unused Debt

Capacity

Asset Write-ups

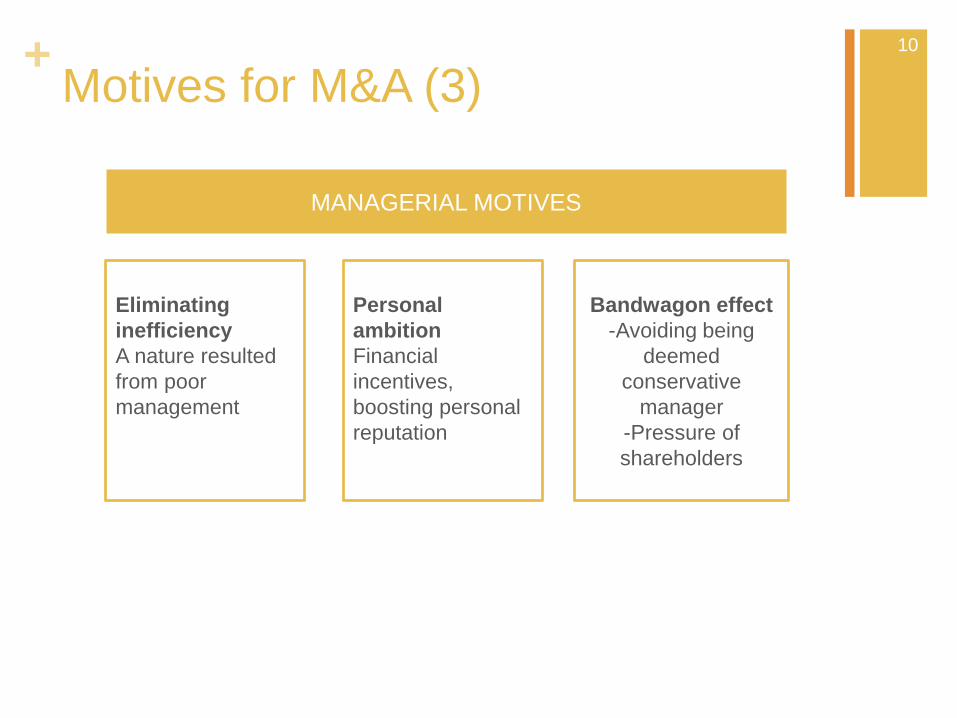

+Motives for M&A (3)

MANAGERIAL MOTIVES

Personal

ambition

Financial

incentives,

boosting personal

reputation

Bandwagon effect

-Avoiding being

deemed

conservative

manager

-Pressure of

shareholders

10

Eliminating

inefficiency

A nature resulted

from poor

management

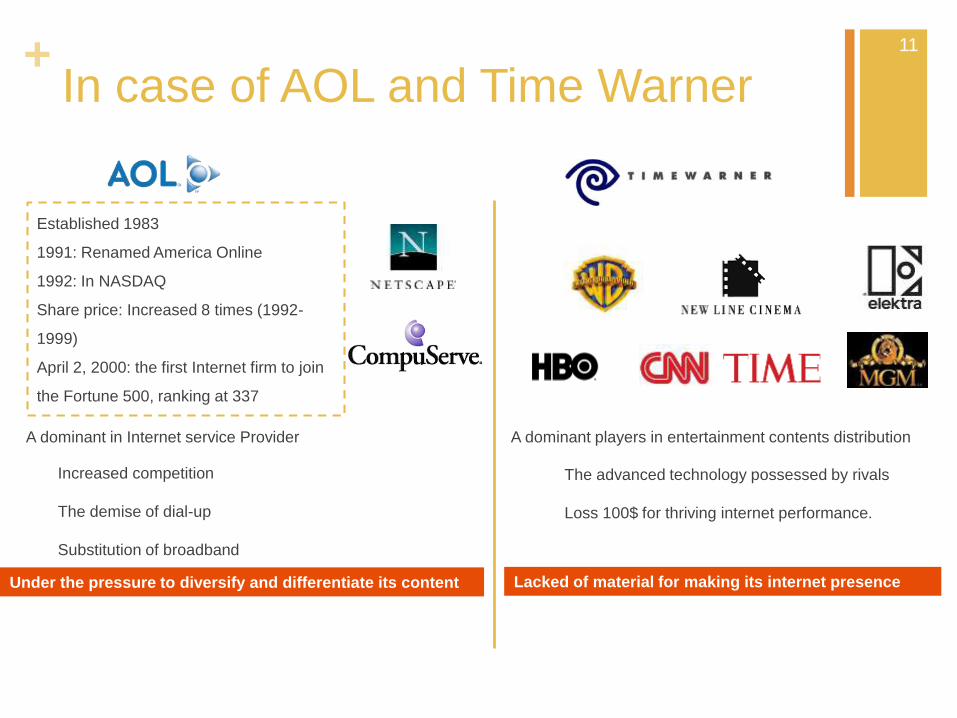

+In case of AOL and Time Warner

A dominant players in entertainment contents distribution

Lacked of material for making its internet presence

A dominant in Internet service Provider

Increased competition

The demise of dial-up

Substitution of broadband

Under the pressure to diversify and differentiate its content

11

The advanced technology possessed by rivals

Loss 100$ for thriving internet performance.

Established 1983

1991: Renamed America Online

1992: In NASDAQ

Share price: Increased 8 times (1992-

1999)

April 2, 2000: the first Internet firm to join

the Fortune 500, ranking at 337

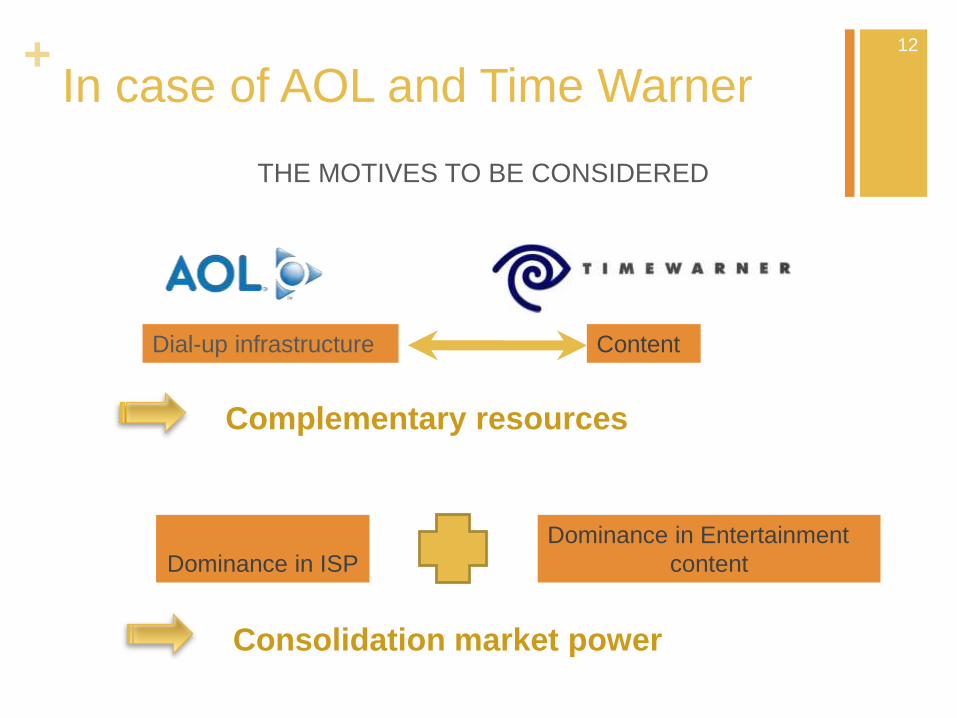

+In case of AOL and Time Warner

THE MOTIVES TO BE CONSIDERED

Complementary resources

12

Dial-up infrastructure Content

Dominance in ISP

Dominance in Entertainment

content

Consolidation market power

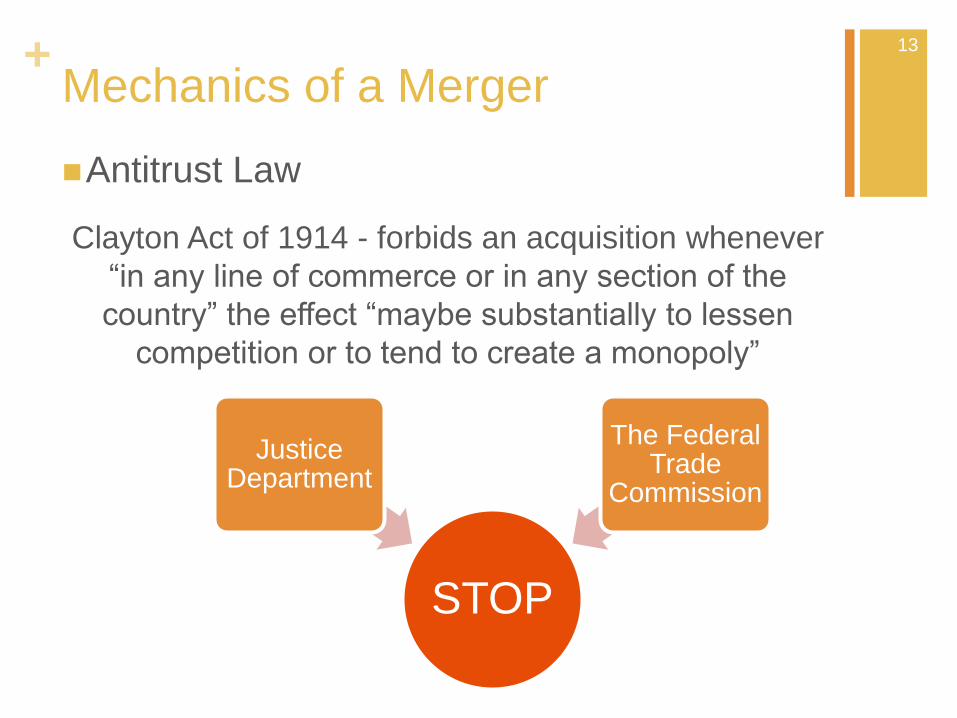

+Mechanics of a Merger

Antitrust Law

Clayton Act of 1914 - forbids an acquisition whenever

“in any line of commerce or in any section of the

country” the effect “maybe substantially to lessen

competition or to tend to create a monopoly”

STOP

Justice Department

The Federal Trade

Commission

13

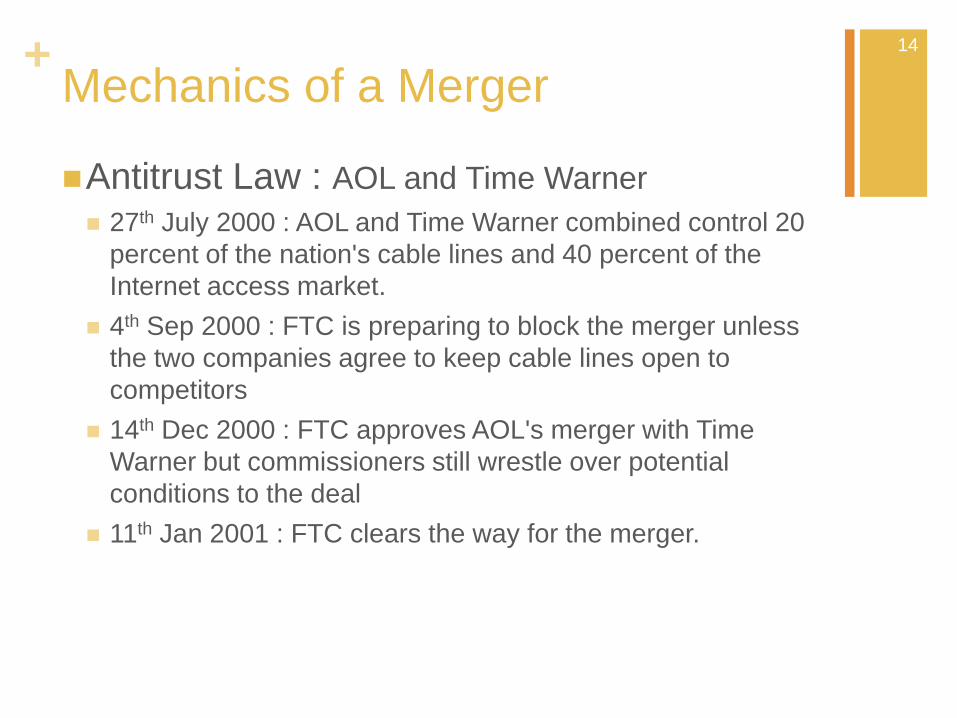

+Mechanics of a Merger

Antitrust Law : AOL and Time Warner

27th July 2000 : AOL and Time Warner combined control 20

percent of the nation's cable lines and 40 percent of the

Internet access market.

4th Sep 2000 : FTC is preparing to block the merger unless

the two companies agree to keep cable lines open to

competitors

14th Dec 2000 : FTC approves AOL's merger with Time

Warner but commissioners still wrestle over potential

conditions to the deal

11th Jan 2001 : FTC clears the way for the merger.

14

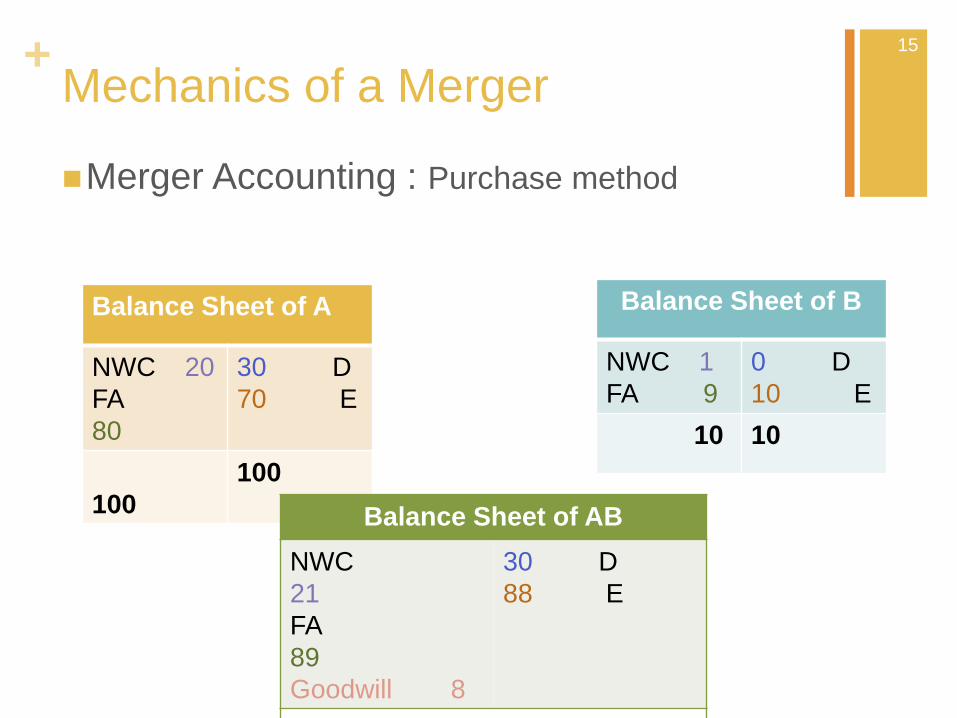

+

Merger Accounting : Purchase method

Mechanics of a Merger

Balance Sheet of A

NWC 20

FA

80

30 D

70 E

100

100

Balance Sheet of B

NWC 1

FA 9

0 D

10 E

10 10

Balance Sheet of AB

NWC

21

FA

89

Goodwill 8

30 D

88 E

118 118

15

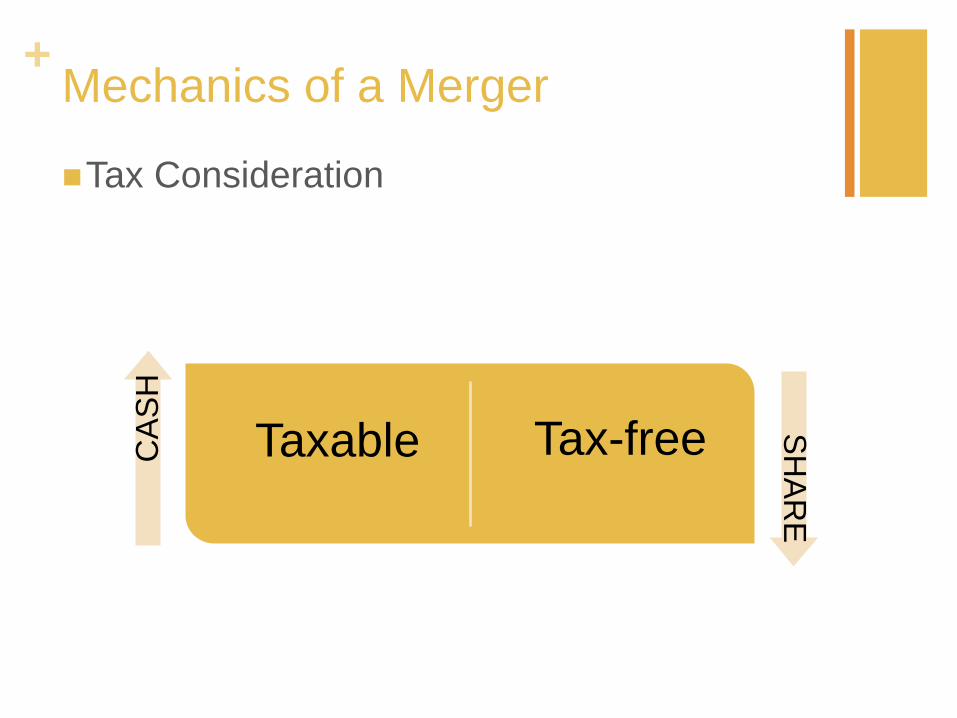

+

Tax Consideration

Mechanics of a Merger

Taxable Tax-freeCA

SH

SH

AR

E

+Evaluating bids

Cost of merger: premium that buyer pays over the seller’s

stand-alone value, equals Target shareholders’ gain

Stand-alone value

- Intrinsic/present value (PV)

- Market value (MV) (May be wrong estimated)

17

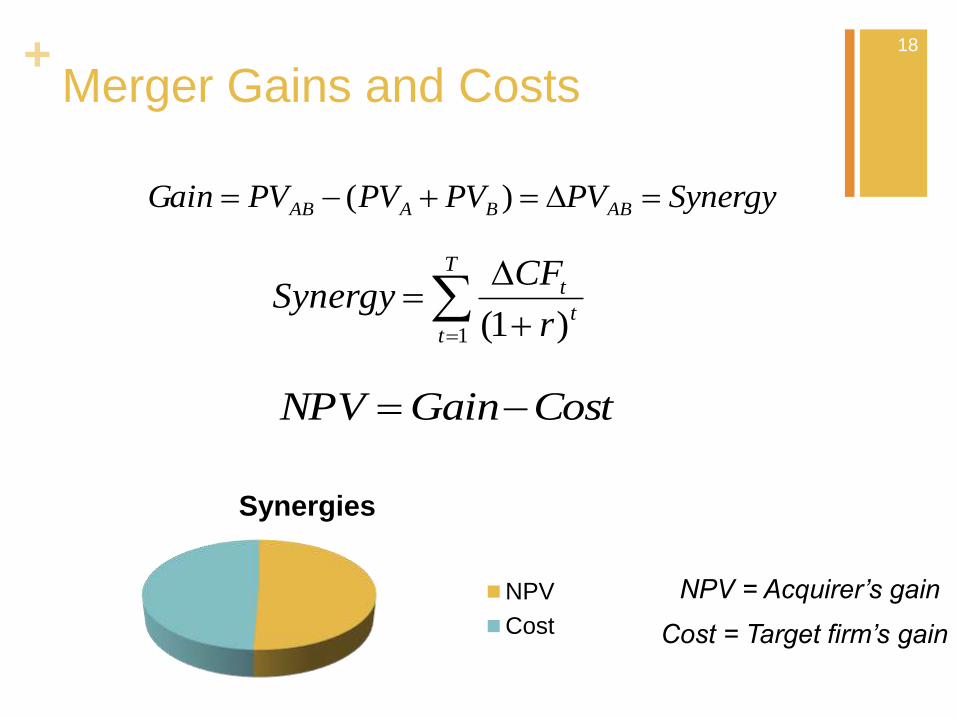

+Merger Gains and Costs

SynergyPVPVPVPVGain ABBAAB )(

T

tt

t

r

CFSynergy

1 )1(

NPV = Acquirer’s gain

Synergies

NPV

Cost Cost = Target firm’s gain

CostGainNPV

18

18

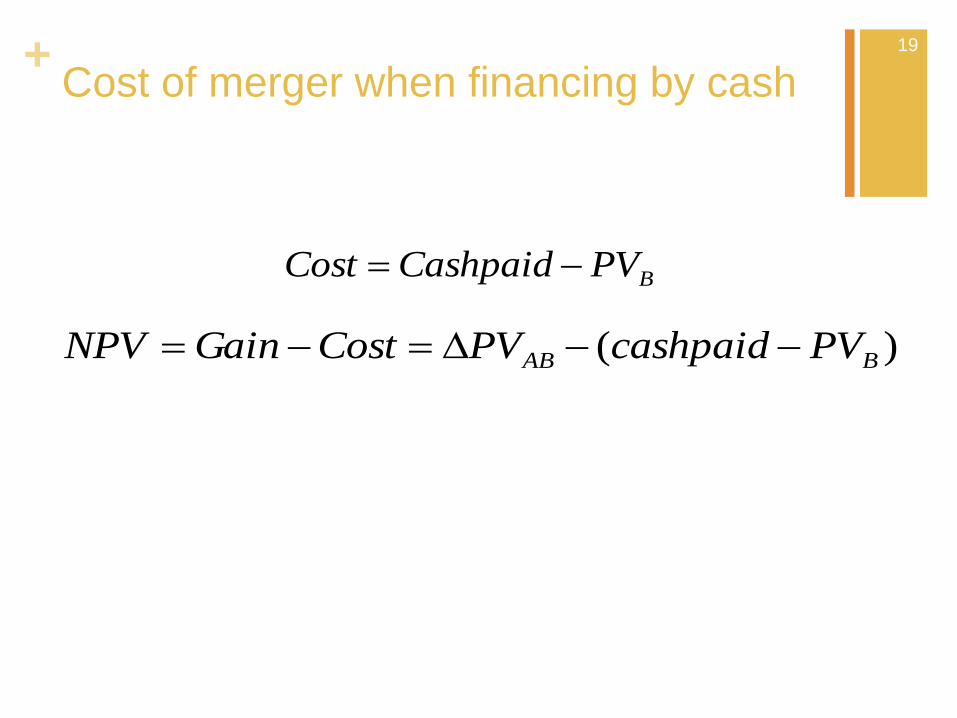

+Cost of merger when financing by cash

BPVCashpaidCost

)( BAB PVcashpaidPVCostGainNPV

19

19

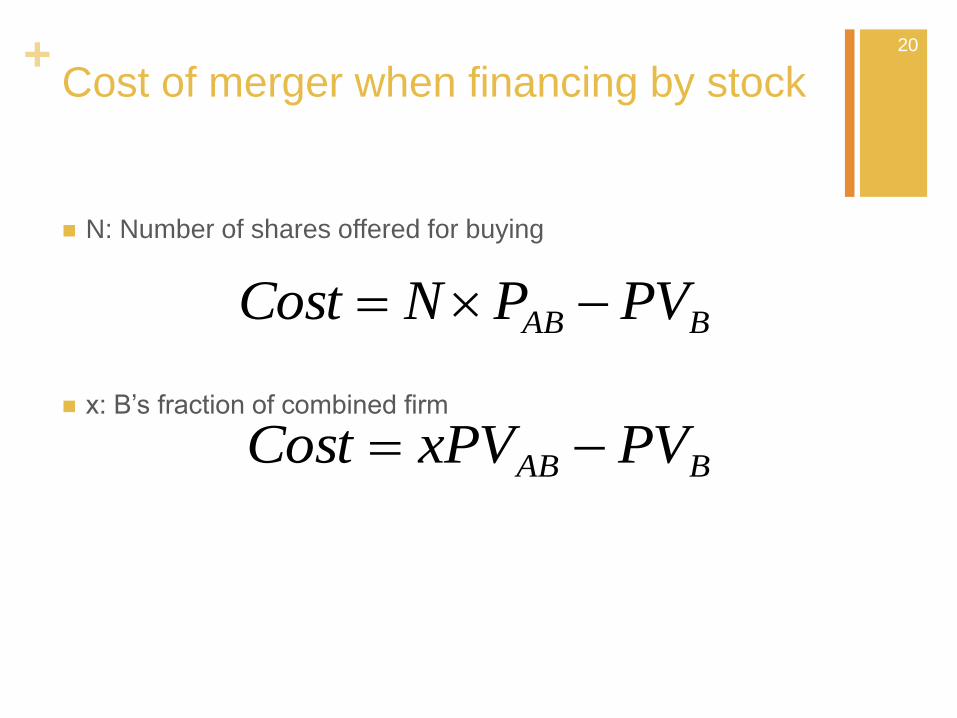

+Cost of merger when financing by stock

N: Number of shares offered for buying

x: B’s fraction of combined firm

20

BAB PVPNCost

BAB PVxPVCost

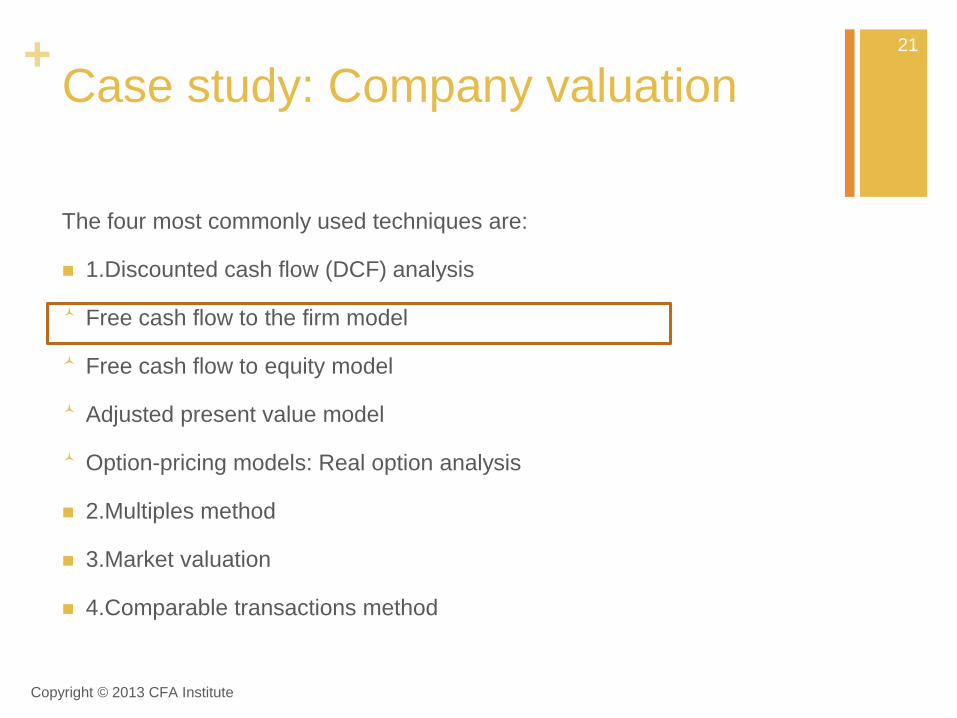

+Case study: Company valuation

The four most commonly used techniques are:

1.Discounted cash flow (DCF) analysis

Free cash flow to the firm model

Free cash flow to equity model

Adjusted present value model

Option-pricing models: Real option analysis

2.Multiples method

3.Market valuation

4.Comparable transactions method

Copyright © 2013 CFA Institute

21

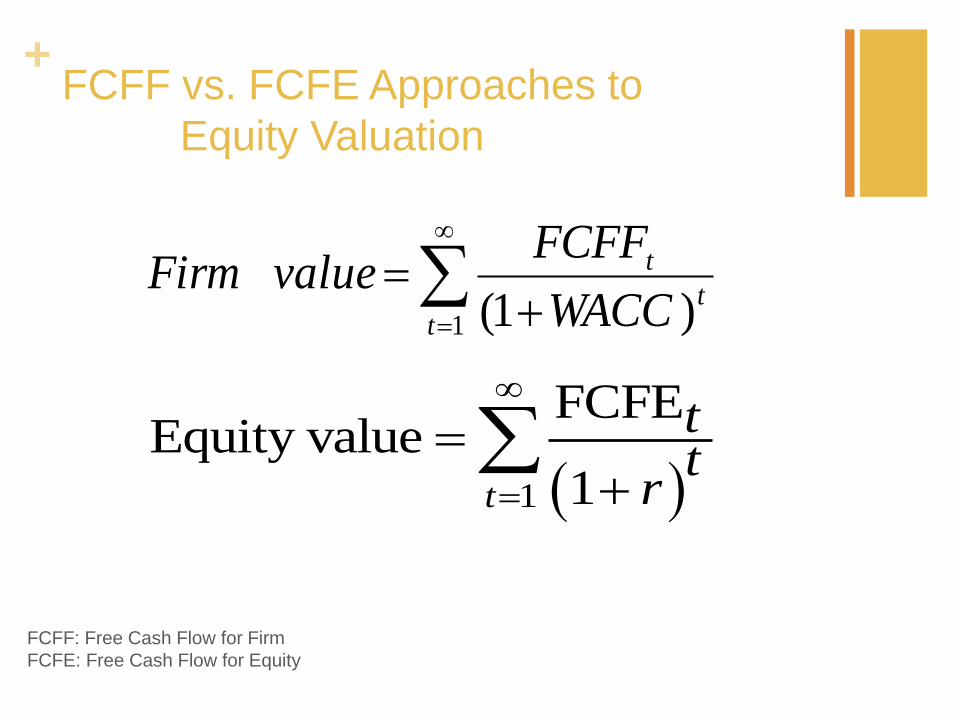

+FCFF vs. FCFE Approaches to

Equity Valuation

1

FCFEEquity value

1

t

tt

r

22

1 )1(tt

t

WACC

FCFFvalueFirm

FCFF: Free Cash Flow for Firm

FCFE: Free Cash Flow for Equity

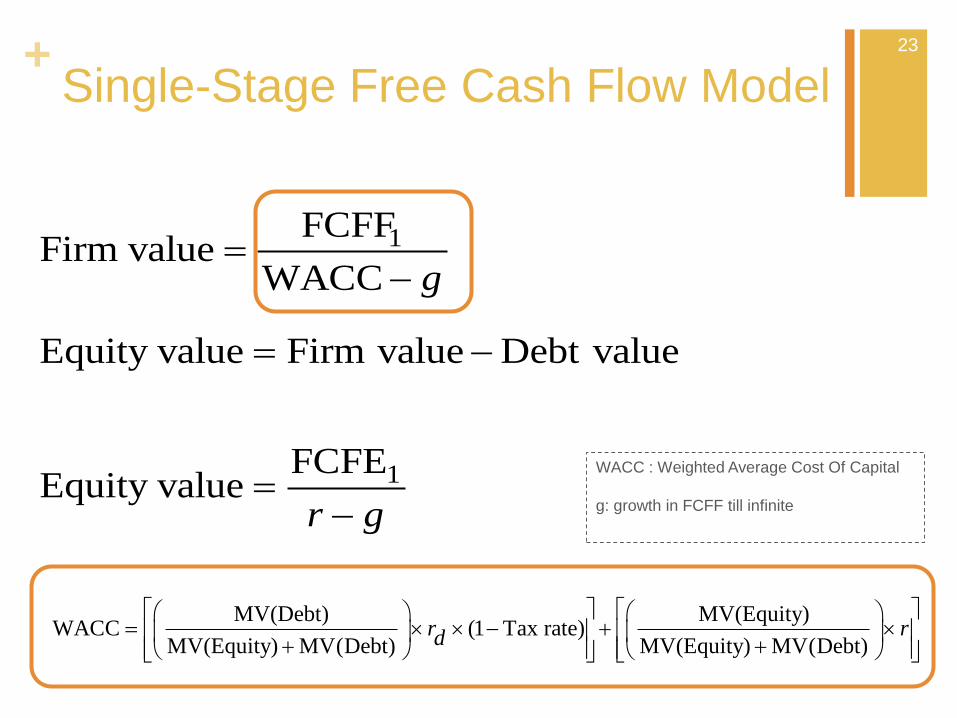

+

1

1

FCFF

Firm valueWACC

Equity value Firm value Debt value

FCFEEquity value

g

r g

MV(Debt) MV(Equity)WACC (1 Tax rate)

MV(Equity) MV(Debt) MV(Equity) MV(Debt)

r rd

23

23

WACC : Weighted Average Cost Of Capital

g: growth in FCFF till infinite

Single-Stage Free Cash Flow Model

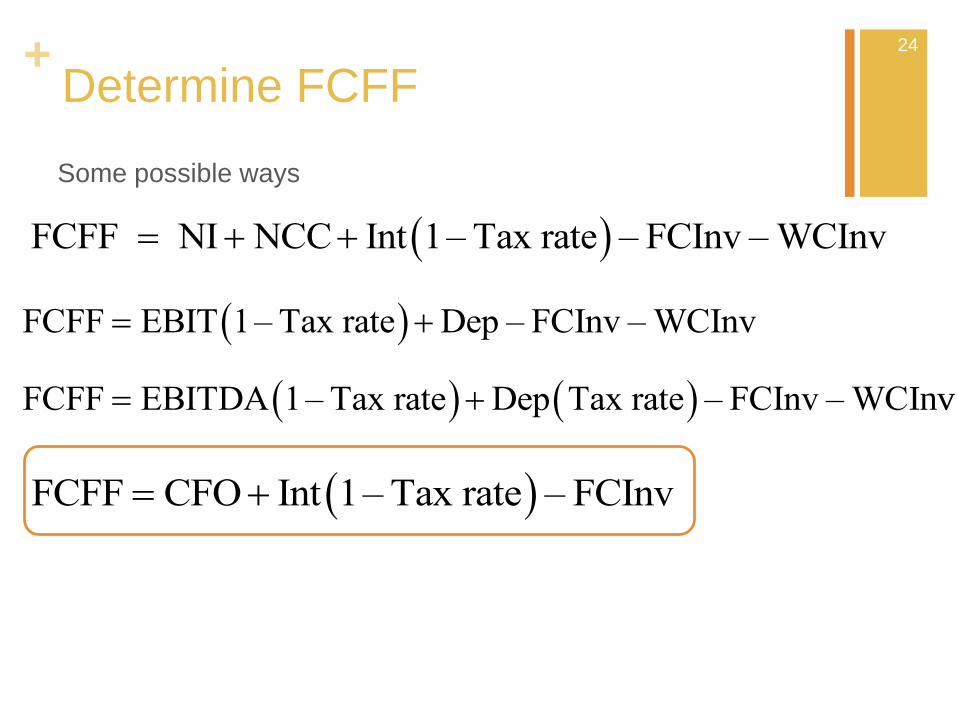

+Determine FCFF

Some possible ways

24

FCFF NI NCC Int 1– Tax rate – FCInv – WCInv

FCFF EBIT 1– Tax rate Dep – FCInv – WCInv

FCFF EBITDA 1– Tax rate Dep Tax rate – FCInv – WCInv

FCFF CFO Int 1– Tax rate – FCInv

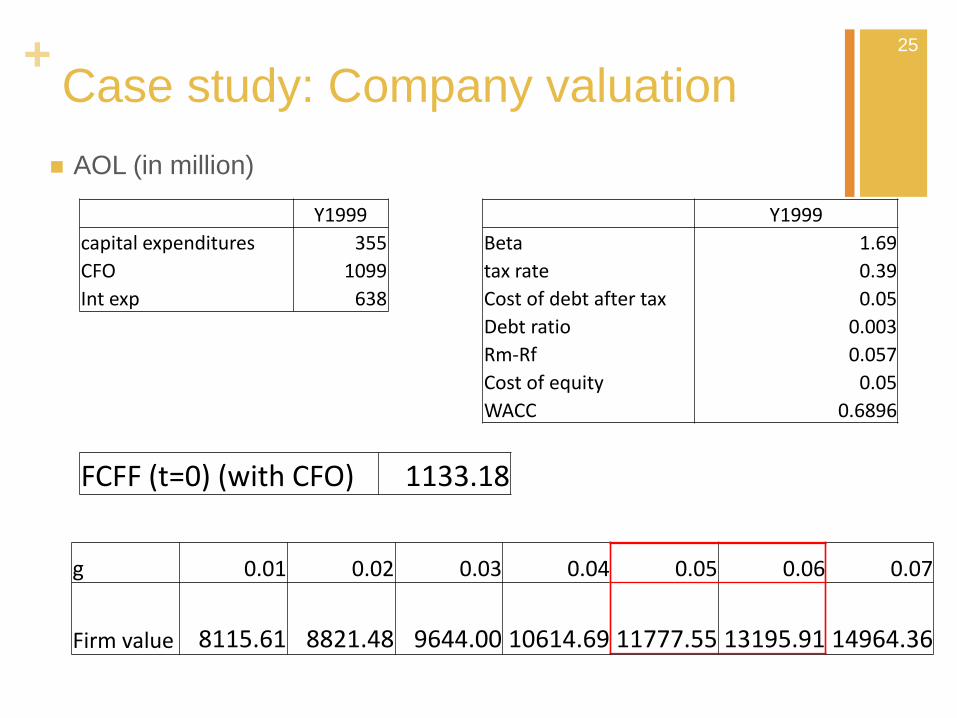

+Case study: Company valuation

AOL (in million)

Y1999 Y1999

capital expenditures 355 Beta 1.69

CFO 1099 tax rate 0.39

Int exp 638 Cost of debt after tax 0.05

Debt ratio 0.003

Rm-Rf 0.057

Cost of equity 0.05

WACC 0.6896

FCFF (t=0) (with CFO) 1133.18

g 0.01 0.02 0.03 0.04 0.05 0.06 0.07

Firm value 8115.61 8821.48 9644.00 10614.69 11777.55 13195.91 14964.36

25

25

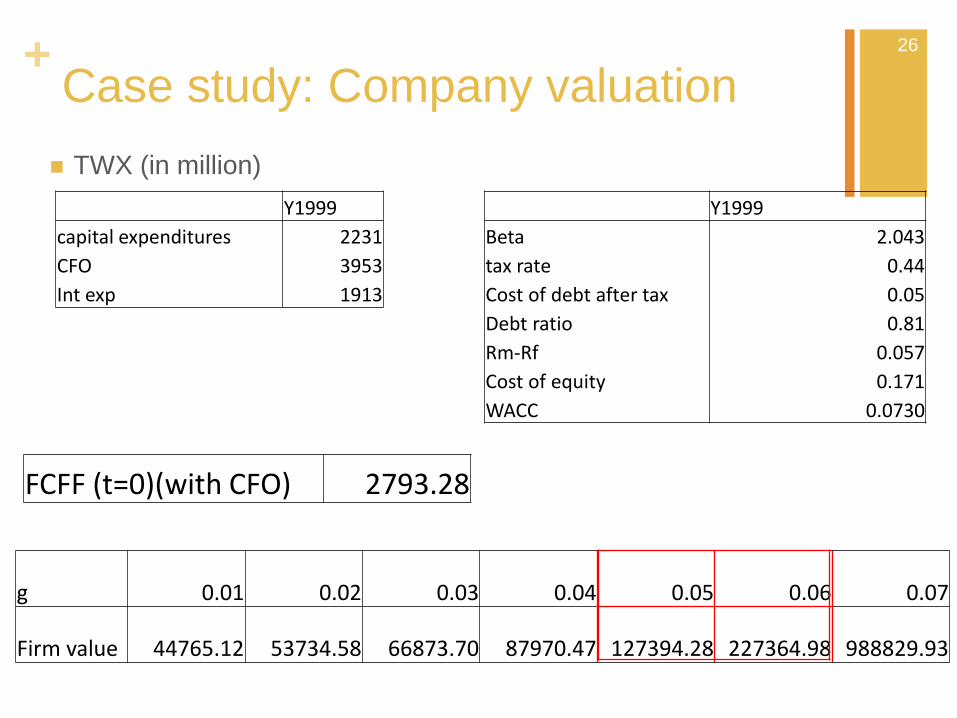

+Case study: Company valuation

TWX (in million)

26

Y1999 Y1999

capital expenditures 2231 Beta 2.043

CFO 3953 tax rate 0.44

Int exp 1913 Cost of debt after tax 0.05

Debt ratio 0.81

Rm-Rf 0.057

Cost of equity 0.171

WACC 0.0730

FCFF (t=0)(with CFO) 2793.28

g 0.01 0.02 0.03 0.04 0.05 0.06 0.07

Firm value 44765.12 53734.58 66873.70 87970.47 127394.28 227364.98 988829.93

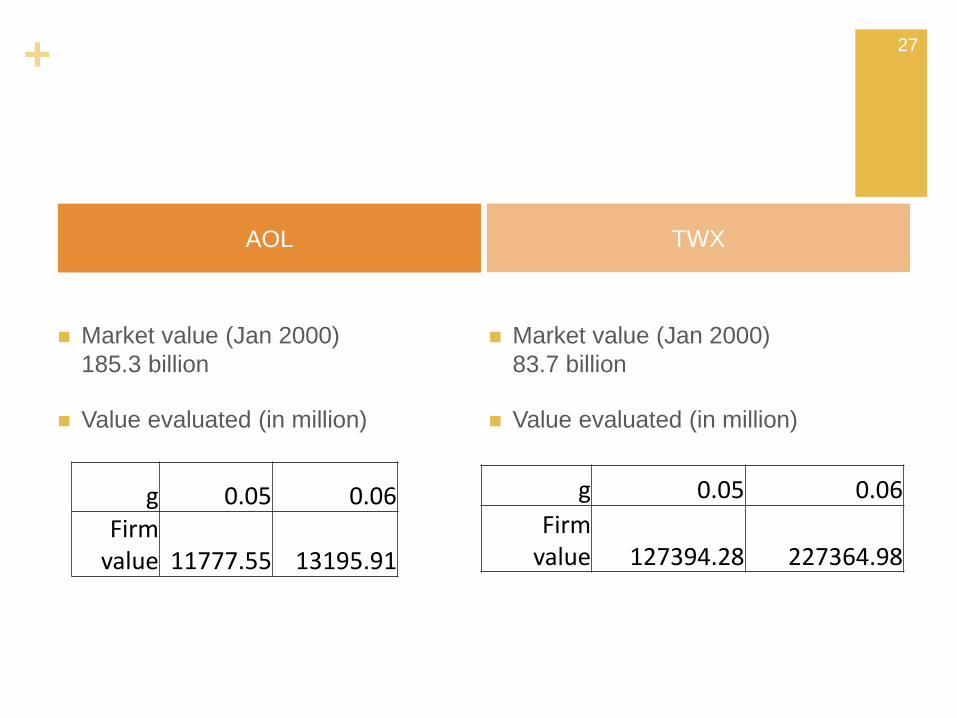

+

AOL TWX

Market value (Jan 2000)

185.3 billion

Value evaluated (in million)

Market value (Jan 2000)

83.7 billion

Value evaluated (in million)

g 0.05 0.06Firm

value 11777.55 13195.91

g 0.05 0.06

Firm value 127394.28 227364.98

27

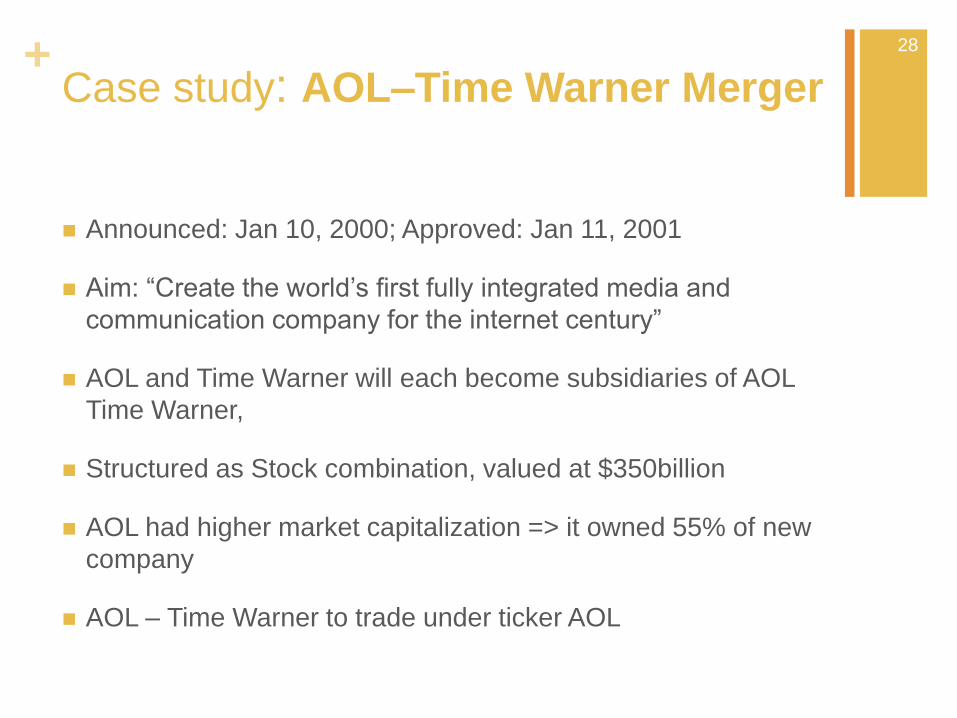

+Case study: AOL–Time Warner Merger

Announced: Jan 10, 2000; Approved: Jan 11, 2001

Aim: “Create the world’s first fully integrated media and

communication company for the internet century”

AOL and Time Warner will each become subsidiaries of AOL

Time Warner,

Structured as Stock combination, valued at $350billion

AOL had higher market capitalization => it owned 55% of new

company

AOL – Time Warner to trade under ticker AOL

28

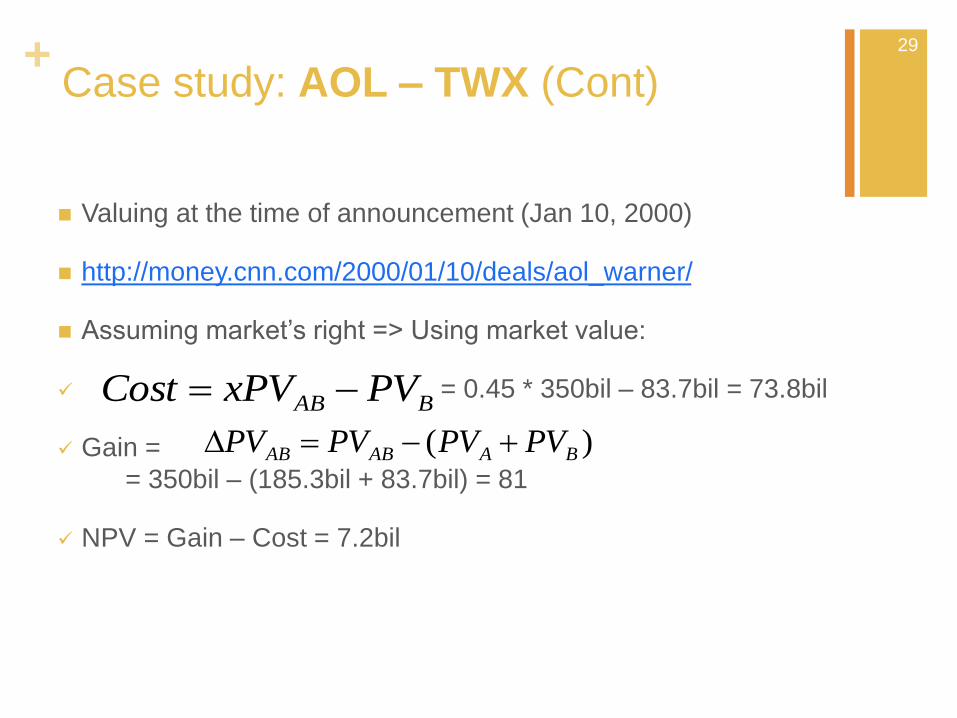

+Case study: AOL – TWX (Cont)

Valuing at the time of announcement (Jan 10, 2000)

http://money.cnn.com/2000/01/10/deals/aol_warner/

Assuming market’s right => Using market value:

= 0.45 * 350bil – 83.7bil = 73.8bil

Gain =

= 350bil – (185.3bil + 83.7bil) = 81

NPV = Gain – Cost = 7.2bil

BAB PVxPVCost

)( BAABAB PVPVPVPV

29

29

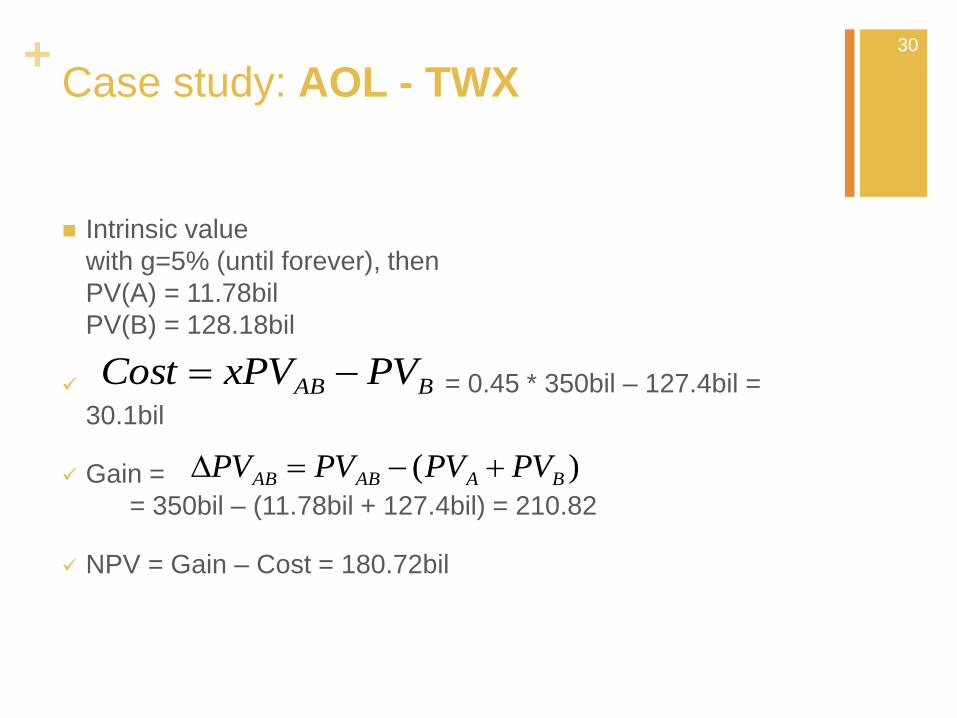

+Case study: AOL - TWX

Intrinsic value

with g=5% (until forever), then

PV(A) = 11.78bil

PV(B) = 128.18bil

= 0.45 * 350bil – 127.4bil =

30.1bil

Gain =

= 350bil – (11.78bil + 127.4bil) = 210.82

NPV = Gain – Cost = 180.72bil

30

BAB PVxPVCost

)( BAABAB PVPVPVPV

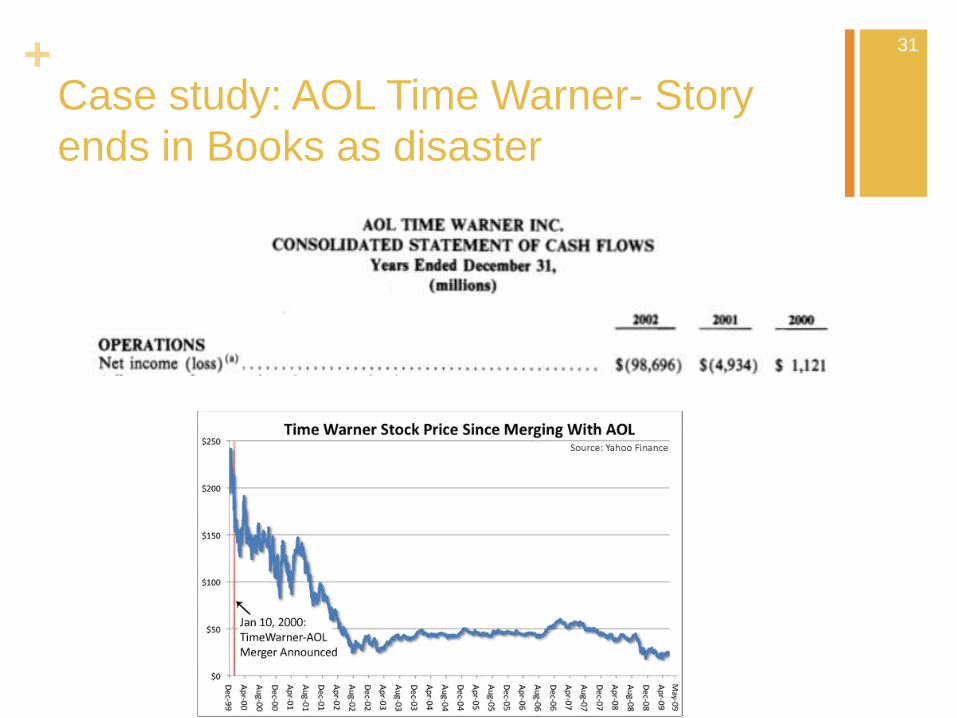

+Case study: AOL Time Warner- Story

ends in Books as disaster

31

+

Q & A

32

+Reference

Book

Brealey R.A., Myers S.C., Allen F. (2011) Principles of Corporate Finance,10th edition, McGraw Hill,

P.792-816

Stephen, A.Ross, Randolph W.Westerfield (2002) Fundamentals of Corporate Finance, 6th Edition,

McGaw Hill, P.846-854

Newyork University (Fall 2009), AOL-Time Warner: Leadership in Organizations, Newyork University

David Hillier, M.Grinblatt, S.Titman (2012) Financial Markets and Corporate Strategy, 2nd Edition, McGraw

Hill, P.646-675.

33

+Reference

Website Hewlett-Packard (2001) Hewlett-Packard and Compaq agree to merge, creating $87 billion global technology leader,

Available from http://www8.hp.com/us/en/hp-news/press-release.html?id=230610#.U3-QKFiSxy8 [Accessed 21 May

2014]

Investopedia (2009) The wonderful world of Mergers , Available from

http://www.investopedia.com/articles/stocks/09/merger-acquisitions-types.asp [Accessed 15 May 2014]

Washingtonpost (2005) Timeline: AOL and Time Warner, Available from http://www.washingtonpost.com/wp-

dyn/content/article/2005/10/28/AR2005102800747_pf.html [Accessed 20 May 2014]

Federal Communications Commission (2014) America Online-Time Warner Merger Page, Available from

http://www.fcc.gov/encyclopedia/america-online-time-warner-merger-page [Accessed 20 May 2014]

Boston College (2005) Valuation Techniques, Available from

http://www.bc.edu/clubs/bcfa/docs/vault/Valuation%20Techniques.pdf [Accessed 23 May 2014]

CFA Institute (2010) Free Cash Flow Valuation, Available from

http://www.cfainstitute.org/learning/products/publications/inv/Documents/equity_chapter4.pptx [Accessed 21 May 2015]

Business Insider (2009) Chart of the day: AOL Time Warner’s Marriage Made in Hell, Available from

http://www.businessinsider.com/chart-of-the-day-time-warner-aol-2009-5 , [Accessed 19 May 2014]

+

The Newyork times (2009) 10th Anniversary of AOL-Time Warner Merger, Available from

http://www.nytimes.com/interactive/2010/01/11/business/20100111-merger-timeline.html?_r=0 [Accessed 19 May

2014]

McGraw Hill (2007) Behavioral Corporate Finance, Available from http://highered.mcgraw-

hill.com/sites/dl/free/0072848650/315497/Chap10.ppt [Accessed 18 May 2014]

Imaa Institute (?) Statistics Merger and Acquisition, Available from http://www.imaa-institute.org/statistics-mergers-

acquisitions.html#TopMergersAcquisitions_Worldwide [Accessed 18 May 2014]

CNN (2000) That’s AOL folks, Available from http://money.cnn.com/2000/01/10/deals/aol_warner/ [Accessed 20

May 2014]