Embed Size (px)

Citation preview

NanoMarkets, LC | PO Box 3840 | Glen Allen, VA 23058 | TEL: 804-270-1718 | FAX: 804-360-7259

www.nanomarkets.net

Conductive Coatings In

Electronics and Energy Markets Nano-507

Published January 2012

© NanoMarkets, LC

NanoMarkets, LC PO Box 3840 Glen Allen, VA 23058 Tel: 804-360-2967 Web: www.nanomarkets.net

NanoMarkets, LC | PO Box 3840 | Glen Allen, VA 23058 | TEL: 804-270-1718 | FAX: 804-360-7259

www.nanomarkets.net

Entire contents copyright NanoMarkets, LC. The information contained in this report is based

on the best information available to us, but accuracy and completeness cannot be guaranteed.

NanoMarkets, LC and its author(s) shall not stand liable for possible errors of fact or judgment.

The information in this report is for the exclusive use of representative purchasing companies

and may be used only by personnel at the purchasing site per sales agreement terms.

Reproduction in whole or in any part is prohibited, except with the express written permission

of NanoMarkets, LC.

NanoMarkets, LC | PO Box 3840 | Glen Allen, VA 23058 | TEL: 804-270-1718 | FAX: 804-360-7259

www.nanomarkets.net

Page | 3

Executive Summary

E.1 Key Opportunities for Conductive Coatings Firms

Many of the segments served by the conductive coatings business generate significant

revenues, but cannot reasonably be considered “opportunities,” because they are

characterized by low growth, possibly low profitability and established supply chains. However,

in the past decade two applications—displays and photovoltaics—have provided new ways for

conductive coatings firms to make money.

Today, these two segments account for two-thirds of the conductive coatings market, and

according NanoMarkets’ forecasts, this share held by the two segments together is not going to

change much throughout the eight-year period considered in this report. This fact alone

indicates that an ambitious conductive coatings executive in search of new business revenues

might begin with these sectors.

What one finds is that—although together these application areas will continue to take the

lion’s share of the revenues in the conductive coatings market—there are significant changes

afoot in both the display and PV sectors that will profoundly reshape the opportunity space for

conductive coatings.

E.1.1 Conductive Coatings and the Incredible Shrinking PV Market

The PV market has for the past several years seemed like God’s gift to the materials industry.

Partly thanks to government subsidies, the solar industry has grown dramatically, including a

significant growth spurt in 2010. The conductive coatings industry, in particular, has been able

to talk the PV industry into buying around $3.0 billion of their products in recent years.

NanoMarkets believes however, that the boom days seem to be over for the PV sector, as far as

the conductive coatings firms are concerned. We think that in most countries, many of the

subsidies that have supported the PV industry for a number of years are going to be reduced

significantly. When the Spanish government took this step a few years ago, the PV market in

Spain declined by 75 percent.

It is also important to remember that the PV industry is not entirely free from the influence of

low economic growth and a weak construction industry. According to a recent issue of The

Economist, there are still a number of important countries where residential real estate is

overvalued. These include Australia, Canada, France, Sweden, Spain and the U.K.

NanoMarkets, LC | PO Box 3840 | Glen Allen, VA 23058 | TEL: 804-270-1718 | FAX: 804-360-7259

www.nanomarkets.net

Page | 4

Bearing all of these facts in mind, NanoMarkets believes that sales of conductive coatings to the

PV industry are in slow but steady decline and will remain so for the whole of the period

considered in this report. We expect to see around $70 million knocked off the value of

conductive coating sales in the next couple of years, with this number rising to around $335

million over the entire period of our forecasts.

This reduction means that conductive coatings firms can no longer count on the PV sector to

provide new business revenues simply based on organic growth. But clearly, the decline that

we are talking about in this sector is not precipitous, and firms that are already established in

the PV sector are not going to see their PV business disappear overnight.

Also on the optimistic side of things, we think that internal technology transitions in the PV

industry will yield new opportunities for smart coatings firms that know where to look for them.

The most important factor here is that the ongoing shift in market share toward more TFPV is

changing the accepted landscape of demand for conductive coatings from that which is

dominant now, and is centered around crystalline silicon PV.

The main reason that this change is creating opportunity is that for the most part, the electrode

materials used in thin-film PV are not a settled matter. Therefore, a new supplier entering this

space is not battling an entrenched material and probably not an entrenched supplier either.

And this opportunity can only get better over time, since with subsidies removed, firms are

more likely to come up with innovative new types of solar panels with even more uncertain

electrode requirements.

Here, what NanoMarkets is seeing are near-term opportunities to offer lower-cost carbon

pastes, molybdenum coatings, aluminum, and silver-aluminum products, instead of silver. In

addition, alternative TCOs have already made significant inroads on ITO, as indicated by the use

of FTO in several PV types. We think that if/when patterning of transparent electrodes

becomes important, AZO has an excellent chance of gaining acceptance. Longer-term

opportunities could include the deployment of a broader range of nanometals and other

nanomaterials.

Even with these opportunities, we are not about to return to a situation where the conductive

coatings industry can expect easy money flowing from PV. Indeed, NanoMarkets believes that

what is happening now in conductive coatings will require a serious rethinking of how money is

going to be made in PV. What will be required will be a more active business development

program than before that is designed to convince TFPV players that costs can be reduced or

performance can be enhanced using a particular electrode material; most notably the former.

NanoMarkets, LC | PO Box 3840 | Glen Allen, VA 23058 | TEL: 804-270-1718 | FAX: 804-360-7259

www.nanomarkets.net

Page | 5

E.1.2 Saved by the Display: Conductive Coatings’ Future as a Display Material

None of these opportunities, we believe, should detract from the basic fact of life that pickings

for conductive coatings firms in the PV industry are going to be a lot slimmer than they were in

the past few years. As we have noted, not only are the overall markets for PV coatings likely to

decline somewhat during the coming decade, but the coatings makers are likely to have to pour

more money into selling into the PV space. Unless they can prove significant performance

advantages or vastly lowered cost, it is likely that margins are going to decline for conductive

coatings firms targeting the PV space.

Fortunately, we think the display industry is going to save the conductive coatings industry! Of

the $9.7 billion in extra revenue that we believe will be generated by the conductive coatings

industry over the forecast period, $6.0 billion (62 percent) will come from new sales of

conductive coatings into the display industry.

ITO replacement could be huge. . . or not: The short-term opportunity here lies in the

replacement of indium tin oxide (ITO) by less expensive (including less expensive to process)

and more resilient transparent conductor materials in displays. The materials that have been

proposed as ITO alternatives for displays include other TCOs, conductive polymers and inks

using nanomaterials of various kinds.

This trend has been noticeable for a few years now, but NanoMarkets believes that in the past

year or so there are signs that what might have been dismissed a year or so back as wishful

thinking by a few firms with a propensity for hyping the latest materials, is beginning to look

like a market opportunity that could someday be worth billions of dollars. What has changed is

that display products using transparent conductors other than ITO are actually appearing in the

market.

In addition, the firms that are pushing alternatives to ITO in the display industry seem to have

found a receptive market niche to try out their products in: the touch-screen sensor market.

This application has the advantage that ITO is not as entrenched as in the mainstream LCD

business, and there is also the positive factor that the underlying touch-screen display market is

growing fast.

Unfortunately, NanoMarkets believes that if ITO replacement is ever going to be a really

substantial market for the conductive coatings firms, these new materials are going to have to

break through into the mainstream LCD market, where ITO is entrenched; the touch-screen

sensor market just is not that big. As NanoMarkets has discussed in its coverage of the

transparent conductor market, 2011 was the first year that we saw some small signs of this

NanoMarkets, LC | PO Box 3840 | Glen Allen, VA 23058 | TEL: 804-270-1718 | FAX: 804-360-7259

www.nanomarkets.net

Page | 6

activity happening. If these signs grow in visibility in the next year, we may be looking at a huge

market opportunity for conductive coatings makers. But we urge caution; it is not that many

years ago that IGZO was supposed to take over from ITO in the LCD industry, with some firms

confidently asserting that it would rapidly take away as much as 30 to 70 percent of ITO’s

business. But nothing like that ever happened.

Beyond LCD: But while the possibility of ITO replacement in conventional displays has been

known and discussed for quite some time, we think that entirely new generations of displays

are about to rescue the conductive coatings firms from the problems that they face in the PV

sector. In exactly the way that PV once presented the conductive coatings business with a

substantial new market that emerged from “nowhere,” we think that the same thing will

happen in the display industry within a three- to five-year time span.

What we are thinking of here is what must happen if the display industry is to continue to grow

its profitability. The “LCD revolution” is coming to an end, since the industry is reaching near

saturation in its major addressable markets. As a result, the big display manufacturers are

looking toward the next big thing, and a slew of new display technologies have started to

emerge. In particular, these include OLED displays, e-paper, flexible displays and transparent

displays.

These display technologies were once the kind of thing that one only saw at trade shows, but

OLED displays and e-paper are now completely commercialized products, and it looks

increasingly as if flexible displays and transparent displays may follow in their footsteps.

Therefore, just as the emergence of the PV industry a decade ago rapidly opened up entirely

new revenue opportunities for the conductive coatings firms, we expect the new generations of

displays to do the same.

Again, we are mostly talking about ITO replacement, but not entirely. Both e-paper and OLED

displays are not back lit, so they only need one layer of transparent conductor. This

requirement means that less transparent conductor (ITO or otherwise) is needed, but new

kinds of opaque conductors will be used at the back of the display. Also, to the extent that

suppliers of novel transparent conductor firms may be disappointed that the new generations

of display may need less transparent conductor material than the older LCD displays, this

reduced consumption should be offset by the openness of the market to new ideas; an

openness that it is slow in coming in the traditional LCD sector.

Meanwhile, the arrival of the volume supply of transparent and flexible displays in the next few

years will certainly change the rules of engagement for conductive coatings makers.

NanoMarkets, LC | PO Box 3840 | Glen Allen, VA 23058 | TEL: 804-270-1718 | FAX: 804-360-7259

www.nanomarkets.net

Page | 7

Transparent displays—and transparent electronics in general—will probably mean the need for

an entirely new set of transparent materials, and conductive coatings firms will certainly be

able to tap into this opportunity if it emerges. Similarly, flexible displays mean that the

materials used will have to be flexible, and here NanoMarkets can see the ultimate reason for

wholesale ITO replacement—and hence the ultimate opportunity for ITO alternatives—

whatever ITO may be it is certainly not flexible.

A note on OLEDs: The OLED sector may be worth some special attention by conductive

coatings firms looking for new opportunities, because it is already quite large and promises to

be larger. Full color, active-matrix OLED displays have emerged in a big way in the last 18

months in smartphones, and OLED TVs seem (finally) ready for commercialization in the next

year or so. There is also some OLED-based lighting already on the market. Although these

products consist almost entirely of luxury lighting at the present time, large lighting panels for

offices seem like the next big thing in the OLED lighting market.

The good news for conductive coatings suppliers is that OLED makers have not only shown an

openness to getting rid of ITO, they have shown actual enthusiasm, at least at the R&D level,

where the OLED lighting sector in particular has dabbled with ITO alternatives. For TVs and

larger OLED lighting panels, we are talking about the consumption of quite large amounts of

conductive coatings per panel, which is another reason why OLEDs represent an opportunity for

conductive coatings makers.

However, there is plenty of skepticism in the industry about whether large panels—TVs or

lighting—will ever succeed in the market; some people think they present too many technical

problems, so there are probably some substantial risks involved for conductive coatings firms.

In summary, nothing is entirely settled yet in OLEDs. Although ITO is still the “default” choice for

most prototypes and initial products, a number of opportunities appear to present themselves

for conductive coatings manufacturers. AZO has emerged as the most likely contender to

replace ITO. The first attempt to substitute for ITO by PEDOT:PSS in OLEDs took place more

than a decade ago, and several carbon nanotube (CNT)-enabled OLED displays have been

demonstrated.

E.1.3 Other Opportunities for Conductive Coatings

As we have indicated, any serious consideration of the opportunities for conductive coatings

must focus on the PV and display sectors, but there are other areas that also warrant further

considerations. These sectors are smaller (although still sizeable), and they also do not have the

same dynamism that we have described for solar and displays.

NanoMarkets, LC | PO Box 3840 | Glen Allen, VA 23058 | TEL: 804-270-1718 | FAX: 804-360-7259

www.nanomarkets.net

Page | 8

EMI, RFI and ESD: A good example of such a sector is that represented by the demand for

conductive coatings of all kinds for EMI/RFI shielding and ESD protection. These sectors are

really two different categories, and we have shown them as such in our forecasts. But from the

perspective of an opportunity analysis, they have a lot in common.

First, both the EMI/RFI and ESD sectors are expected to see quite strong growth during the

eight years for which we forecast revenues, although the ESD sector is a lot smaller than the

EMI/RFI sector. And in both cases, the opportunities are fairly immediate. Also, in both cases,

the market is being driven by long-term trends.

In the case of EMI/RFI, more materials of this kind are needed as wireless

communications moves towards ubiquity.

In the case of ESD, the onward march of Moore’s Law means that more ESD protection

is required in packaging for electronics parts.

These stories are not new, however; they continue to drive the opportunities in this space, but

there are no fundamental changes of the kind that we have described for the display and PV

spaces.

The trend in EMI/RFI shielding coatings is toward increased use of both vacuum-deposited

metal coatings and new thermal and plasma spray coatings. Both of these options offer cost

advantages over conventional plated coatings, which can be messy and wasteful. Both vacuum-

deposited and thermal spray metal coatings offer greater flexibility in material content and

better performance with respect to coating uniformity than conventional plated coatings.

Low-end ESD coating applications are best left to the low-cost commodity antistats, either in

coating form or in the form of bulk-loaded materials. However, there are opportunities in

higher-end ESD protection coatings, especially for those that require transparency, for both

metal oxides and ICPs. CNT-based coatings for ESD applications may also have promise, but

they remain too expensive to be viable options today.

It should be noted that throughout the EMI/RFI and ESD sectors, coatings represent only one

approach. They are in competition with many other approaches, such as tapes, foils, wires, and

bulk-additives of various kinds.

Energy storage: Energy storage is another sector where NanoMarkets foresees new

opportunities for conductive coatings going forward. Obviously, as a product, batteries have

been around a long time, but with the rising cost of energy, there are now more economic

reasons to store energy. In addition, mobile communications and the hope for a growing

NanoMarkets, LC | PO Box 3840 | Glen Allen, VA 23058 | TEL: 804-270-1718 | FAX: 804-360-7259

www.nanomarkets.net

Page | 9

demand for electric vehicles also promote the market for energy storage devices with higher

energy densities.

Energy storage devices of all varieties make use of conductive coatings of all types, and it is

quite clear that there will be considerable opportunities for coatings makers in this space that

can demonstrate that their materials can lead to improved performance in energy storage

devices of various kinds.

However, while NanoMarkets agrees with this assessment, there are also reasons to curb

enthusiasm a little with respect to this sector.

For one thing, we are talking—as with the ESD/EMI/RFI sector—about ongoing driving

forces and not about radical new changes that will throw up entirely novel

opportunities.

In addition, some of the expectations of the recent past have not been met. Fuel cells

and EVs are the obvious examples here, and their mediocre market performance

obviously impacts the opportunities for conductive coatings going forward.

Nonetheless, newer products—potentially at least—constitute large markets, and they often

have entirely new materials requirements for the electrodes that they use. In the short-to-

medium term time frame, a few particular opportunities stand out:

New electrode materials for lithium-ion batteries. This battery type is the dominant one

used in consumer electronics and power tools, and is being widely touted for use in EVs.

To the extent that new electrode materials can help to improve on energy densities,

power densities, time between charges, etc., there is a high value opportunity to be

exploited here by conductive coatings firms.

In solid electrolytic capacitors (SECs), trends toward ever-lower ESR values and package

sizes are leading to the need for better carbon, silver, metal oxide and ICP coatings.

Meanwhile, development of conductive nanomaterial coatings capable of uniformly and

completely impregnating SEC anode bodies could be disruptive to the entrenched

technologies, which are electrochemically formed metal oxides or in situ polymerized

ICPs.

In supercapacitors, just as in batteries, the business opportunities for conductive

coatings lie in those that can enable higher energy storage capacities and faster

discharge times. This need implies opportunities for a variety of nano-structured

NanoMarkets, LC | PO Box 3840 | Glen Allen, VA 23058 | TEL: 804-270-1718 | FAX: 804-360-7259

www.nanomarkets.net

Page | 10

conductive materials, especially CNTs, graphenes, and the like, and could be an entry

point for these (relatively) new materials.

In the longer term, NanoMarkets believes that there will probably be emerging opportunities

for more exotic materials to become widely used in this space. One type of material that we

think bears watching is ultra-high surface area carbon nanomaterials (CNTs, graphene, etc.),

which are a natural fit, as are RedOx active inherently conductive polymers (ICPs) that improve

double layer capacitance.

E.1.4 Happy Days: “Nanocoatings” are Here at Last!

The vast majority of the revenues generated in the conductive coating space over the next eight

years will be made with materials that are fairly conventional in nature and which—at worst—

may need some technical upgrading or some market repositioning. By way of a measure of the

importance of such materials, our projections suggest that 97 percent of the revenues from

conductive materials will come from these mundane materials in 2012, and that their share will

still be very significant—84 percent—by the end of the forecast period.

However, this reduction is a substantial decline and—if NanoMarkets’ analysis is correct—it is

largely accounted for by the rise of nanomaterials. This change is important. Although the

potentially high performance of nanomaterials and the reasons for them are regularly discussed

in the literature, and have been for many years, NanoMarkets believes we are now seeing real

signs of opportunities for these materials appear in the conductive space.

These signs are of two kinds. First, our projections suggest that the revenues available to firms

from the “conductive nanocoatings” space will soon become large enough to attract the

attention of both large specialty chemical companies and hopeful start-ups. Thus, by 2016, we

expect revenues from nanometal coatings to have reached $665 million, growing to $1.4 billion

by the end of the forecast period. The equivalent numbers for carbon nanomaterials are

roughly $525 million and $1.1 billion.

But there is another reason for conductive coatings firms to be excited about the arrival of

“conductive nanocoatings.” These materials—at the early phase of their evolution—are open

to more room for innovation, and there is also more room to establish intellectual property

positions than with most of the conductive coatings discussed in this report. These advantages

should be reflected in higher margins for firms supplying these materials throughout the period

under consideration in this report.

NanoMarkets, LC | PO Box 3840 | Glen Allen, VA 23058 | TEL: 804-270-1718 | FAX: 804-360-7259

www.nanomarkets.net

Page | 11

The specifics of the applications in which these conductive nanocoatings may find a home are

discussed more fully in the main body of this report. Here we note that the biggest opportunity

for nanomaterial coatings will be in the ITO-replacement market, although carbon

nanomaterials will also be especially important in the energy storage markets.

Meanwhile, graphene is on everyone’s watch list at the present time, and it seems likely that it

will play some role in conductive coatings going forward. However, we would caution readers

against being ultra-bullish on this material. In assessing the potential for graphene, the

disappointments along the way to the commercialization of carbon nanotubes should be taken

into consideration.

E.2 Firms to Watch in the Conductive Coatings Industry

The conductive coatings industry is a large and fragmented industry, including hundreds of

businesses and a large number of links in the value chain.

E.2.1 Notable End Users of Conductive Coatings

Starting at the user end of this chain, we think that—given the rapidly growing importance of

the display sector for conductive coatings—Samsung is going to be a key factor shaping this

market. This firm now not only has a large share of the display market, but is by far the most

innovative display firm in terms of both using new materials and commercializing new display

technologies.

Any clear direction taken by Samsung in areas that are of relevance to the conductive coatings

industry should be taken as a strong indication of where the market is headed. The reader

should be especially attentive to the use by Samsung of ITO alternatives, and of how the firm is

using coating materials in its transparent and flexible display products.

There are really no other firms as important in other sectors of the conductive coatings industry

as Samsung is in the display sector. However, there are also some influential thin-film solar

panel firms whose choices of materials for electrodes could help stabilize a rather fluid market,

in terms of materials choices. An obvious example here is First Solar, but Global Solar could

also prove to be an important influencer.

E.2.2 The Conductive Coatings Market and Large Specialty Chemical Firms

Many of the best known names in the chemical industry are players in the conductive coatings

space. These companies include Heraeus, DuPont, Cookson Electronics, Evonik and Bayer, to

name but a few. Several of these firms operate successfully in several market segments that we

analyze in this report, and we expect them to continue do so.

NanoMarkets, LC | PO Box 3840 | Glen Allen, VA 23058 | TEL: 804-270-1718 | FAX: 804-360-7259

www.nanomarkets.net

Page | 12

However, the shifting sands that make up today’s conductive coatings market are going to

require these firms to be nimble in both their R&D and marketing efforts in a way that hasn’t

been required since the rise of the PV industry a decade ago. These firms are now going to

have to reposition themselves as suppliers to the display industry, and those that already have

ties to the display industry are in the best position to take advantage of the current situation in

the conductive coatings market. An obvious example of such a company is DuPont.

In general, the highest-usage materials—metals and conventional carbon—are supplied by

large firms with (usually) long histories in their respective markets. Cabot Corporation, for

example, has been supplying carbon black materials for decades.

An interesting question is the degree to which these large firms will be able to capitalize on the

opportunities for “nanocoatings.” Several of them are clearly trending in that direction with

strong activity in the emerging materials areas. Examples here are Heraeus’ and Cookson’s

conductive polymer programs or Bayer’s carbon nanotube businesses.

E.2.3 Opportunities for Start-Ups

NanoMarkets believes that, going forward, the conductive coatings space is one that will be

fertile ground for start-ups. On the one hand, we have the grand shift from PV to displays,

which creates the possibility for a firm to brand itself as a “next-generation display materials”

supplier. Such firms have a chance of success because they can be more nimble than the large

specialty chemical companies and occupy this new next-generation materials space before the

big businesses can get there.

On the other hand, we now have the rapid emergence of “nanocoatings,” which enables IP to

be created, and which is exactly the protection that a small firm needs to compete in the

market and garner funding. With all of these issues in mind, NanoMarkets believes that a new

breed of firm may emerge that fits this pattern. An important example of where such an event

has already happened is the case of Cambrios, and this firm should be watched as a sort of

pointer to what we think will become an increasingly common business strategy. What

Cambrios does and how it succeeds may have implications that go well beyond the nanosilver

coatings that it is currently selling.

As we have already mentioned, it is hard to avoid the graphene meme. Vorbeck Materials is

the only firm that seems to have focused primarily on the development of a commercial

ink/coating, and it has received some funding recently. Finally, in the area of conductive

polymers, only Heraeus stands out as a leader; it is more actively pursuing sophisticated,

higher-margin markets for its PEDOT-based ICPs than any of the other ICP suppliers. (Although

NanoMarkets, LC | PO Box 3840 | Glen Allen, VA 23058 | TEL: 804-270-1718 | FAX: 804-360-7259

www.nanomarkets.net

Page | 13

we must concede that Enthone’s acquisition of the Ormecon business may bode well for the

expansion of PANI-based ICPs into large markets.)

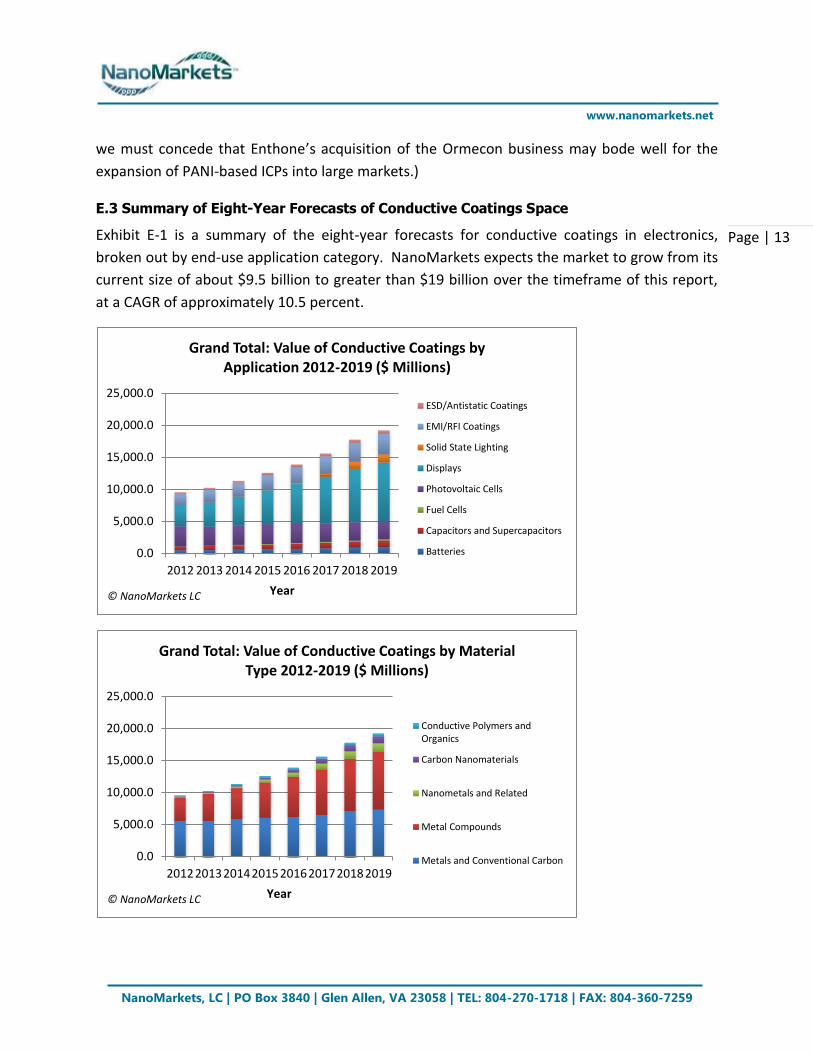

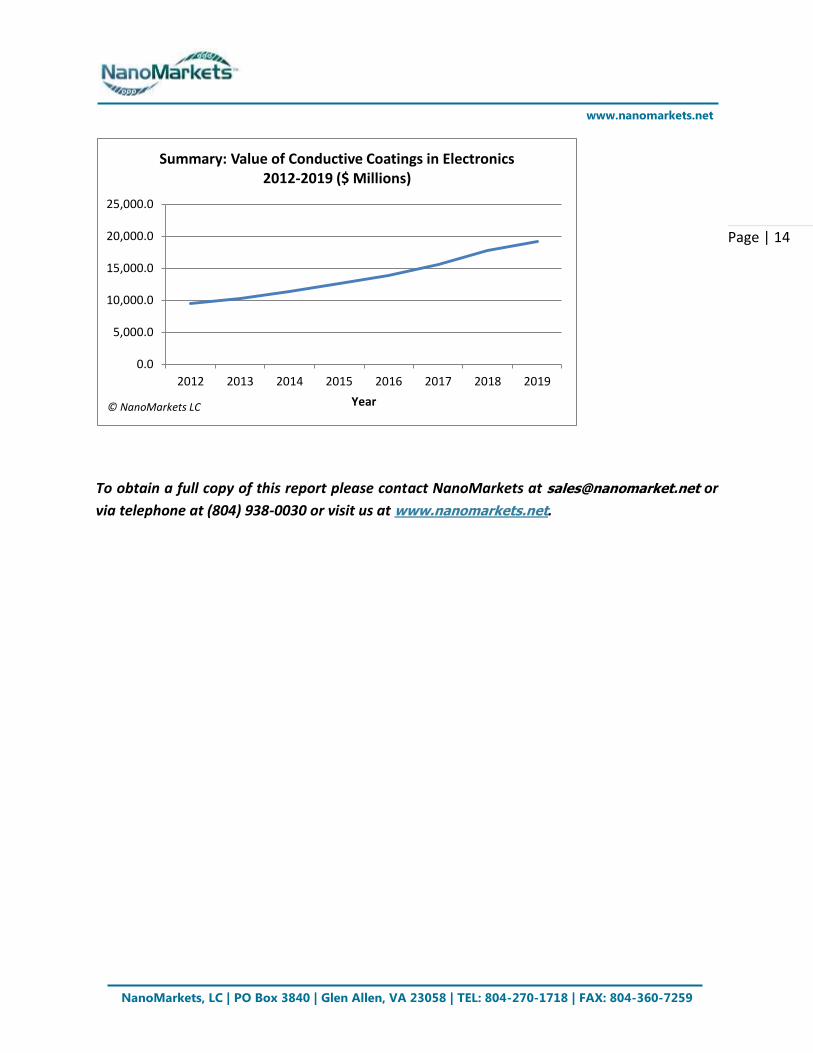

E.3 Summary of Eight-Year Forecasts of Conductive Coatings Space

Exhibit E-1 is a summary of the eight-year forecasts for conductive coatings in electronics,

broken out by end-use application category. NanoMarkets expects the market to grow from its

current size of about $9.5 billion to greater than $19 billion over the timeframe of this report,

at a CAGR of approximately 10.5 percent.

0.0

5,000.0

10,000.0

15,000.0

20,000.0

25,000.0

2012 2013 2014 2015 2016 2017 2018 2019

Year

Grand Total: Value of Conductive Coatings by Application 2012-2019 ($ Millions)

ESD/Antistatic Coatings

EMI/RFI Coatings

Solid State Lighting

Displays

Photovoltaic Cells

Fuel Cells

Capacitors and Supercapacitors

Batteries

© NanoMarkets LC

0.0

5,000.0

10,000.0

15,000.0

20,000.0

25,000.0

20122013201420152016201720182019

Year

Grand Total: Value of Conductive Coatings by Material Type 2012-2019 ($ Millions)

Conductive Polymers andOrganics

Carbon Nanomaterials

Nanometals and Related

Metal Compounds

Metals and Conventional Carbon

© NanoMarkets LC

NanoMarkets, LC | PO Box 3840 | Glen Allen, VA 23058 | TEL: 804-270-1718 | FAX: 804-360-7259

www.nanomarkets.net

Page | 14

To obtain a full copy of this report please contact NanoMarkets at [email protected] or

via telephone at (804) 938-0030 or visit us at www.nanomarkets.net.

0.0

5,000.0

10,000.0

15,000.0

20,000.0

25,000.0

2012 2013 2014 2015 2016 2017 2018 2019

Year

Summary: Value of Conductive Coatings in Electronics 2012-2019 ($ Millions)

© NanoMarkets LC