Embed Size (px)

Citation preview

C1 BankC1 BankSBA LENDINGSBA LENDING

CorC Corporate Partner of the Miami Heat

AGENDAAGENDA

INTRODUCTIONINTRODUCTION ELIGIBILITYELIGIBILITY USE OF PROCEEDSUSE OF PROCEEDS GENERAL CREDIT CRITERIAGENERAL CREDIT CRITERIA LOAN TO VALUE AND AMORTIZATIONLOAN TO VALUE AND AMORTIZATION QUICK GUIDE TO 7A AND 504 PROGRAMQUICK GUIDE TO 7A AND 504 PROGRAM C1 BANK’S SBA TEAMC1 BANK’S SBA TEAM

ELIGIBILITYELIGIBILITY

US CITIZEN OR PERMANENT RESIDENT ALIENUS CITIZEN OR PERMANENT RESIDENT ALIEN MUST BE A FOR PROFIT ENTITYMUST BE A FOR PROFIT ENTITY NO RELIGIOUS AFFILIATIONSNO RELIGIOUS AFFILIATIONS NO GAMBLING OR ADULT ENTERTAINMENT BUSINESSESNO GAMBLING OR ADULT ENTERTAINMENT BUSINESSES REAL ESTATE MUST BE 51% OWNER OCCUPIED (60% FOR NEW CONSTRUCTION)REAL ESTATE MUST BE 51% OWNER OCCUPIED (60% FOR NEW CONSTRUCTION) SIZE STANDARDS ARE MAXIMUM TANGIBLE NET WORTH OF $15 MILLION AND SIZE STANDARDS ARE MAXIMUM TANGIBLE NET WORTH OF $15 MILLION AND

MAXIMUM TWO YEAR NET AVERAGE INCOME AFTER FEDERAL INCOME TAX OF MAXIMUM TWO YEAR NET AVERAGE INCOME AFTER FEDERAL INCOME TAX OF $5 MILLION$5 MILLION

ADDITIONAL CRITERIA MAY APPLY BASED ON LOAN REQUEST AND STRUCTURE, ADDITIONAL CRITERIA MAY APPLY BASED ON LOAN REQUEST AND STRUCTURE, INCLUDING SITUATIONS FREQUENTLY ENCOUNTERED:INCLUDING SITUATIONS FREQUENTLY ENCOUNTERED:__ FULLY SECURED PROVISION__ FULLY SECURED PROVISION__ REFINANCE CRITERIA__ REFINANCE CRITERIA__ EXCESS LIQUIDITY GUIDELINES__ EXCESS LIQUIDITY GUIDELINES

USE OF PROCEEDSUSE OF PROCEEDS

Real Estate Purchase or RefinanceReal Estate Purchase or Refinance Real Estate New ConstructionReal Estate New Construction Business Acquisition FinancingBusiness Acquisition Financing Business Expansion FinancingBusiness Expansion Financing Business Start-up FinancingBusiness Start-up Financing Equipment Purchase and/or RefinanceEquipment Purchase and/or Refinance Working CapitalWorking Capital Or…a combination of any of the above.Or…a combination of any of the above.

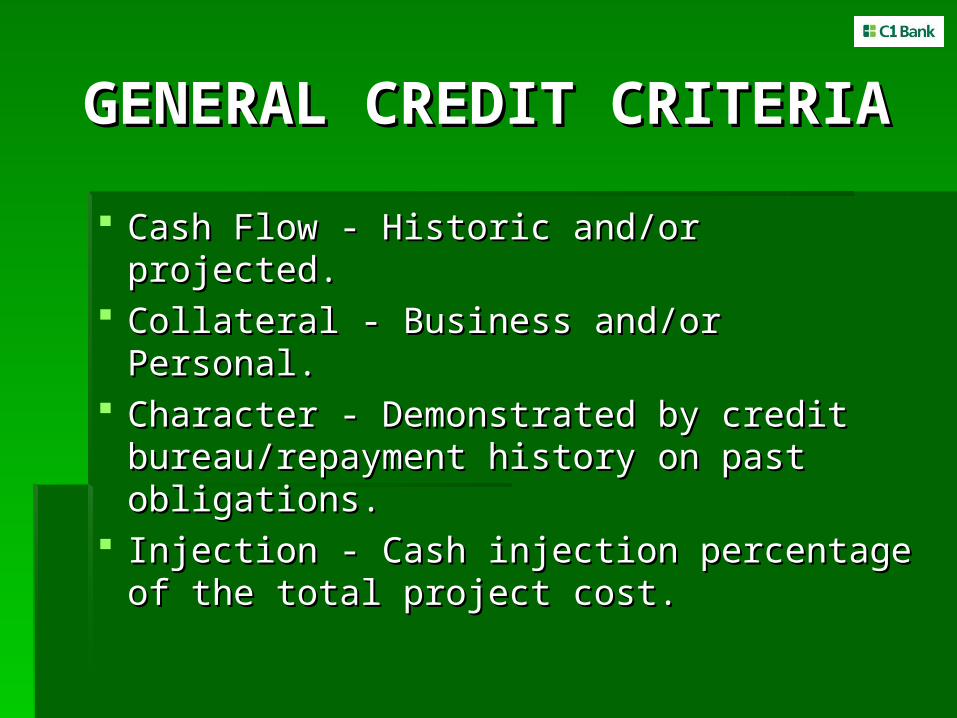

GENERAL CREDIT CRITERIAGENERAL CREDIT CRITERIA

Cash Flow - Historic and/or projected.Cash Flow - Historic and/or projected. Collateral - Business and/or Personal.Collateral - Business and/or Personal. Character - Demonstrated by credit Character - Demonstrated by credit

bureau/repayment history on past bureau/repayment history on past obligations.obligations.

Injection - Cash injection percentage of the Injection - Cash injection percentage of the total project cost. total project cost.

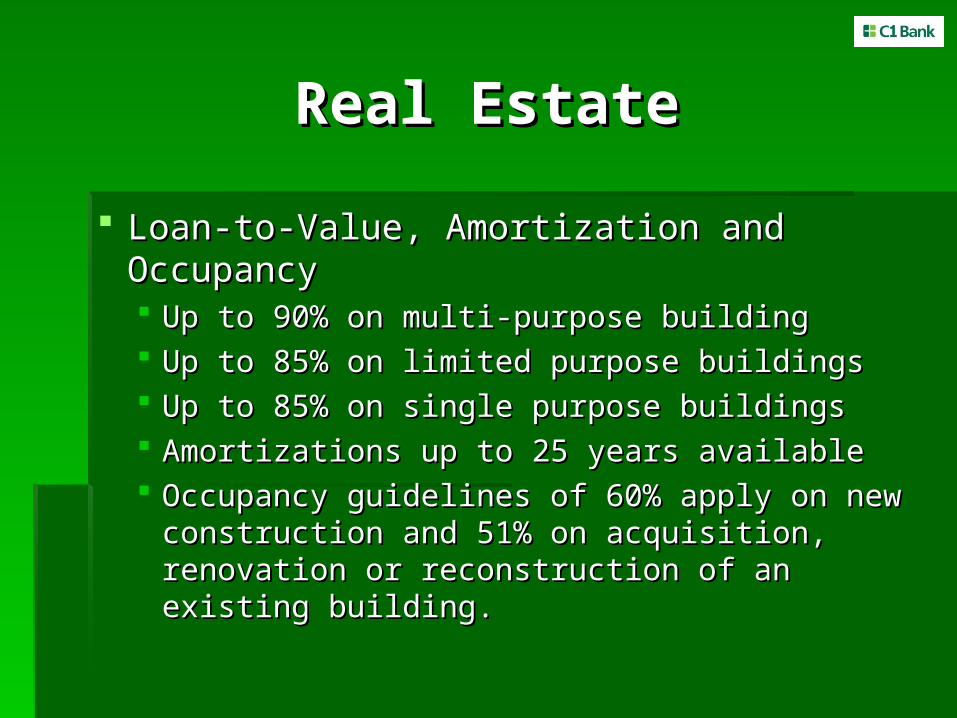

Real EstateReal Estate

Loan-to-Value, Amortization and OccupancyLoan-to-Value, Amortization and Occupancy Up to 90% on multi-purpose buildingUp to 90% on multi-purpose building Up to 85% on limited purpose buildingsUp to 85% on limited purpose buildings Up to 85% on single purpose buildingsUp to 85% on single purpose buildings Amortizations up to 25 years availableAmortizations up to 25 years available Occupancy guidelines of 60% apply on new Occupancy guidelines of 60% apply on new

construction and 51% on acquisition, renovation construction and 51% on acquisition, renovation or reconstruction of an existing building.or reconstruction of an existing building.

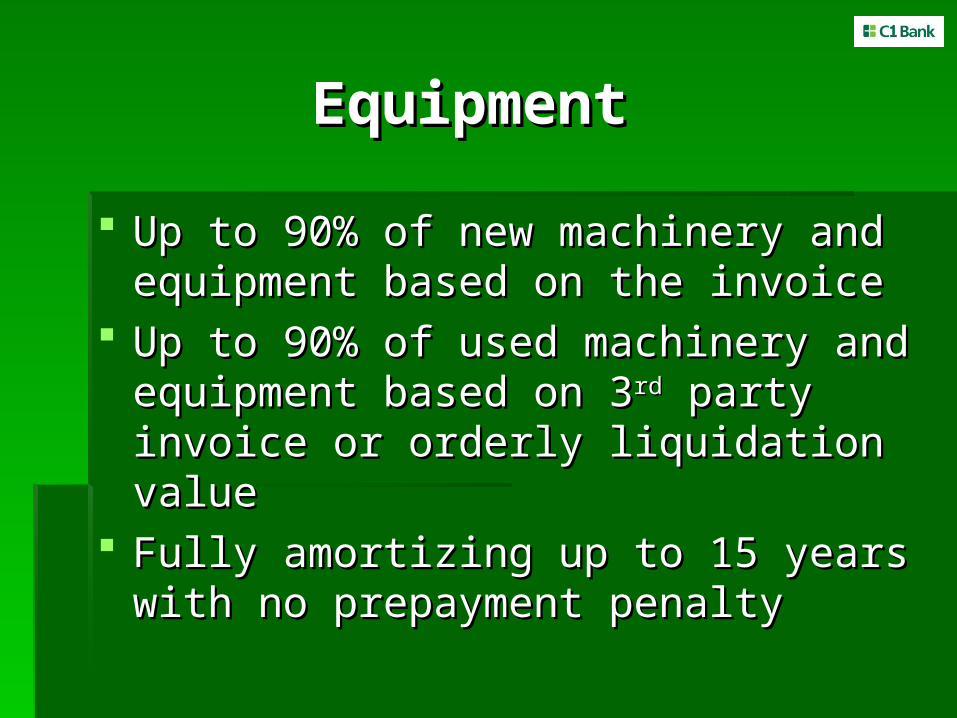

EquipmentEquipment Up to 90% of new machinery and equipment Up to 90% of new machinery and equipment

based on the invoicebased on the invoice Up to 90% of used machinery and equipment Up to 90% of used machinery and equipment

based on 3based on 3rdrd party invoice or orderly party invoice or orderly liquidation valueliquidation value

Fully amortizing up to 15 years with no Fully amortizing up to 15 years with no prepayment penaltyprepayment penalty

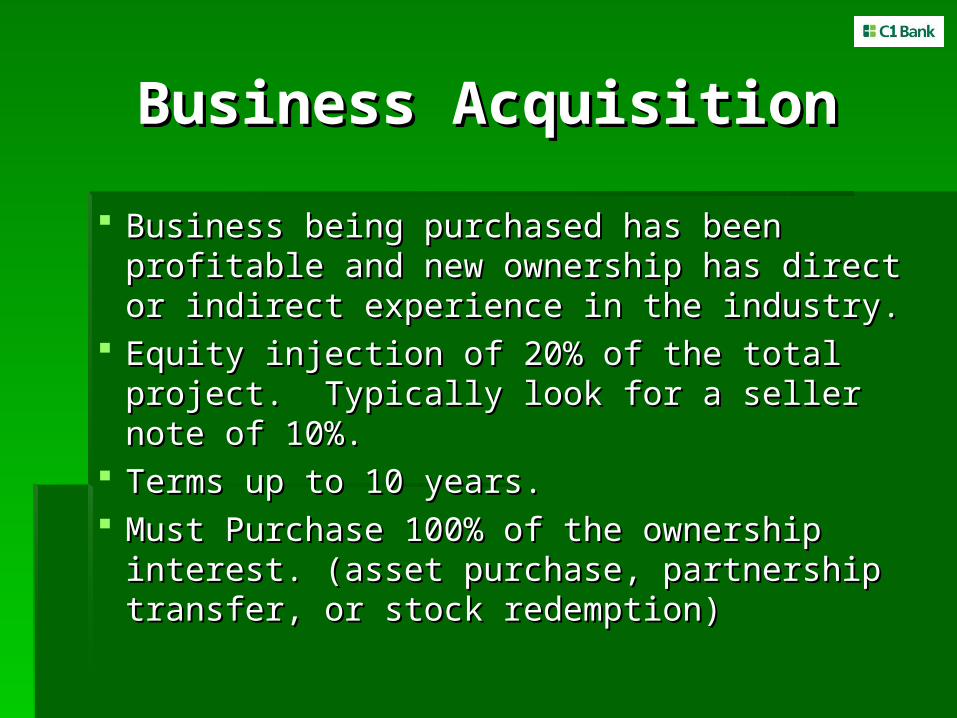

Business AcquisitionBusiness Acquisition

Business being purchased has been profitable and Business being purchased has been profitable and new ownership has direct or indirect experience in new ownership has direct or indirect experience in the industry.the industry.

Equity injection of 20% of the total project. Equity injection of 20% of the total project. Typically look for a seller note of 10%.Typically look for a seller note of 10%.

Terms up to 10 years.Terms up to 10 years. Must Purchase 100% of the ownership interest. Must Purchase 100% of the ownership interest.

(asset purchase, partnership transfer, or stock (asset purchase, partnership transfer, or stock redemption)redemption)

Start-Up BusinessStart-Up Business

Ownership/management team typically Ownership/management team typically needs direct experience in the industry.needs direct experience in the industry.

30% cash injection of the total project.30% cash injection of the total project. Dollar for dollar collateral from outside of Dollar for dollar collateral from outside of

the business to serve as a secondary source the business to serve as a secondary source of repayment.of repayment.

Involve your C1 Bank SBA professional in Involve your C1 Bank SBA professional in the process and relax…the process and relax…

What do we need to get started?What do we need to get started? 3 Years Business Tax Returns3 Years Business Tax Returns Interim Financial StatementsInterim Financial Statements Up-To-Date Personal Financial StatementUp-To-Date Personal Financial Statement Current Debt ScheduleCurrent Debt Schedule We will immediately determine SBA eligibility, We will immediately determine SBA eligibility,

matching it with the bank’s current credit policy matching it with the bank’s current credit policy to determine our ability to proceed.to determine our ability to proceed.

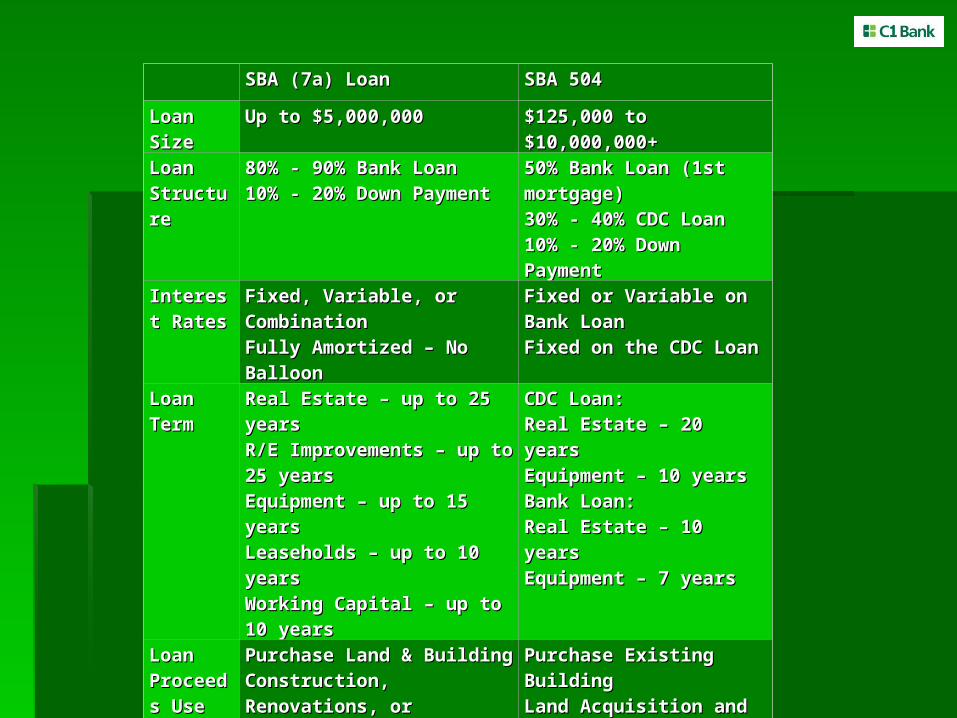

SBA (7a) LoanSBA (7a) Loan SBA 504SBA 504

Loan Loan SizeSize

Up to $5,000,000Up to $5,000,000 $125,000 to $10,000,000+$125,000 to $10,000,000+

Loan Loan StructureStructure

80% - 90% Bank Loan80% - 90% Bank Loan10% - 20% Down Payment10% - 20% Down Payment

50% Bank Loan (1st mortgage)50% Bank Loan (1st mortgage)30% - 40% CDC Loan30% - 40% CDC Loan10% - 20% Down Payment10% - 20% Down Payment

Interest Interest RatesRates

Fixed, Variable, or CombinationFixed, Variable, or CombinationFully Amortized – No BalloonFully Amortized – No Balloon

Fixed or Variable on Bank LoanFixed or Variable on Bank LoanFixed on the CDC LoanFixed on the CDC Loan

Loan Loan TermTerm

Real Estate – up to 25 yearsReal Estate – up to 25 yearsR/E Improvements – up to 25 R/E Improvements – up to 25 yearsyearsEquipment – up to 15 yearsEquipment – up to 15 yearsLeaseholds – up to 10 yearsLeaseholds – up to 10 yearsWorking Capital – up to 10 yearsWorking Capital – up to 10 years

CDC Loan:CDC Loan:Real Estate – 20 yearsReal Estate – 20 yearsEquipment – 10 yearsEquipment – 10 yearsBank Loan:Bank Loan:Real Estate – 10 yearsReal Estate – 10 yearsEquipment – 7 yearsEquipment – 7 years

Loan Loan Proceeds Proceeds UseUse

Purchase Land & BuildingPurchase Land & BuildingConstruction, Renovations, orConstruction, Renovations, orLeasehold ImprovementsLeasehold ImprovementsFurniture and FixturesFurniture and FixturesMachinery and EquipmentMachinery and EquipmentInventory and Working CapitalInventory and Working CapitalRefinance Existing DebtRefinance Existing Debt

Purchase Existing BuildingPurchase Existing BuildingLand Acquisition andLand Acquisition andGround Up ConstructionGround Up ConstructionExpansion of Existing BuildingExpansion of Existing BuildingBuilding ImprovementsBuilding ImprovementsEquipment (no rolling stock)Equipment (no rolling stock)

C1 Bank’s SBA TEAMC1 Bank’s SBA TEAM

Ruben Alfaras, SBA ManagerRuben Alfaras, SBA ManagerMichael Bernstein, Business Development OfficerMichael Bernstein, Business Development Officer

Javier Jorge, Business Development OfficerJavier Jorge, Business Development OfficerTeressa Galloway, SBA Loan ProcessorTeressa Galloway, SBA Loan Processor

Andrew Ralph, SBA UnderwriterAndrew Ralph, SBA UnderwriterCarmie Snider, SBA Underwriting ConsultantCarmie Snider, SBA Underwriting Consultant