Embed Size (px)

Citation preview

0

FTTH – The Service and Application Enabler

February 24, 2010

Alfredo BaptistaCTO

PROPRIETARYAny use of this material without specific permission of Portugal Telecom is strictly prohibited

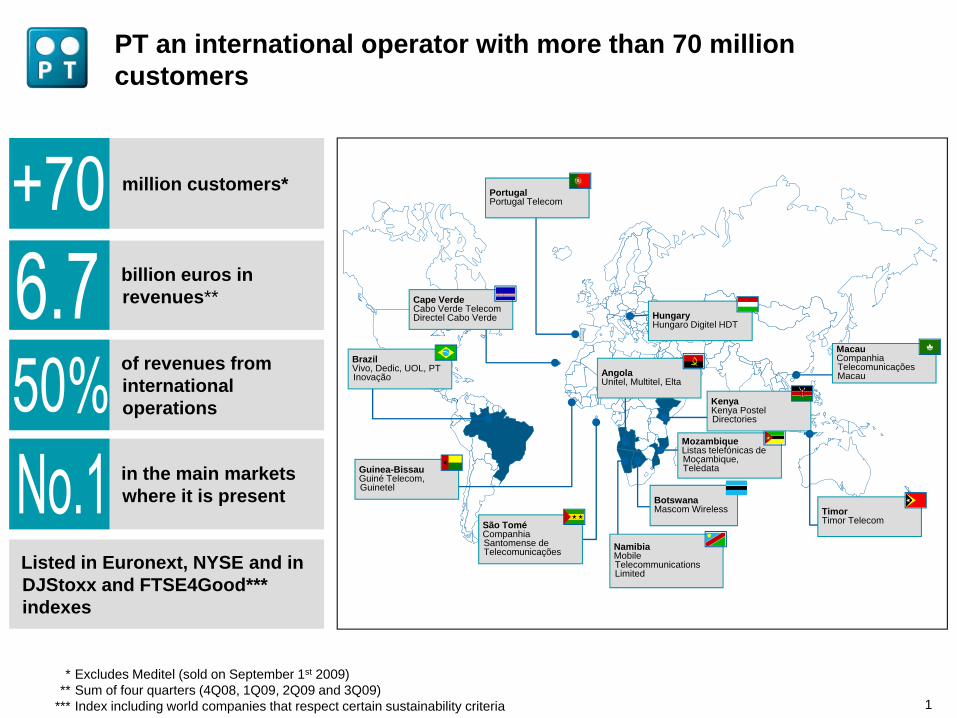

1

million customers*

billion euros in revenues**

of revenues from international operations

in the main markets where it is present

HungaryHungaro Digitel HDT

Cape VerdeCabo Verde TelecomDirectel Cabo Verde

BrazilVivo, Dedic, UOL, PT Inovação Angola

Unitel, Multitel, Elta

MozambiqueListas telefónicas de Moçambique, Teledata

KenyaKenya Postel Directories

MacauCompanhia Telecomunicações Macau

Guinea-BissauGuiné Telecom, Guinetel

São ToméCompanhia Santomense de Telecomunicações

TimorTimor Telecom

PortugalPortugal Telecom

NamibiaMobile Telecommunications Limited

BotswanaMascom Wireless

* Excludes Meditel (sold on September 1st 2009)** Sum of four quarters (4Q08, 1Q09, 2Q09 and 3Q09)

*** Index including world companies that respect certain sustainability criteria

PT an international operator with more than 70 million customers

Listed in Euronext, NYSE and in DJStoxx and FTSE4Good*** indexes

2

Strategy based on innovation and execution

Residential PersonalCorporate

Portugal

Leadership in all segments

SMBs

International

Growth and profitability

Brazil AfricaWholesale

Innovation Execution

Structured approach

Strategic partners

Human resources

Value creating projects

Operational optimization

Financial capacity

3

Agenda

A new paradigm for the sector

PT with a clear strategy for FTTH

Enabling the fibre potential

4

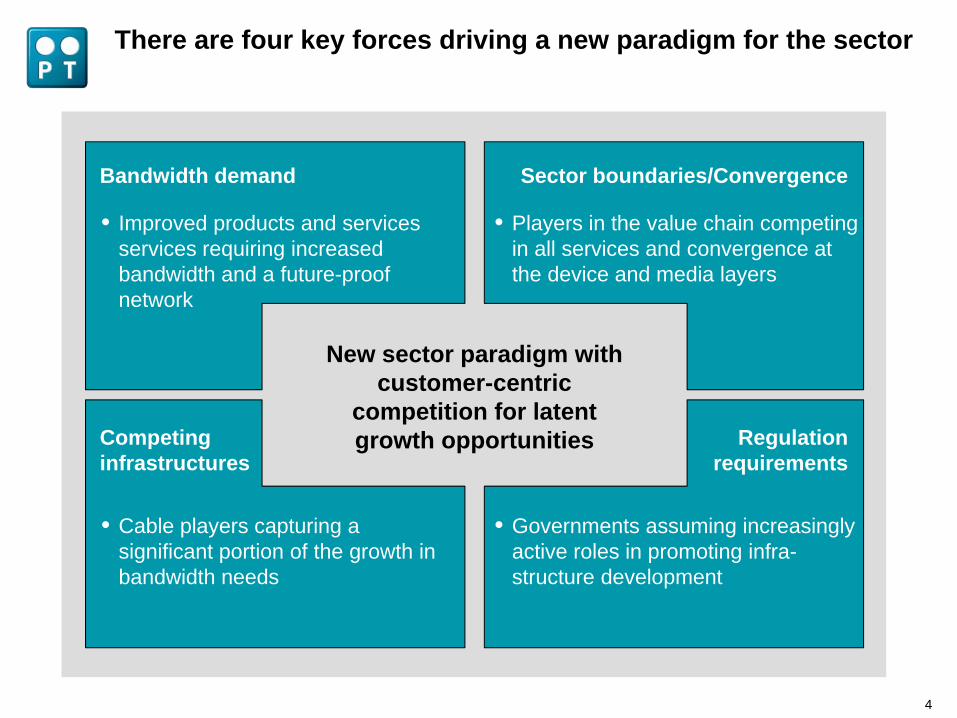

There are four key forces driving a new paradigm for the sector

Bandwidth demand Sector boundaries/Convergence

Competing infrastructures

Regulation requirements

New sector paradigm with customer-centric

competition for latent growth opportunities

• Improved products and services services requiring increased bandwidth and a future-proof network

• Players in the value chain competing in all services and convergence at the device and media layers

• Cable players capturing a significant portion of the growth in bandwidth needs

• Governments assuming increasingly active roles in promoting infra-structure development

5

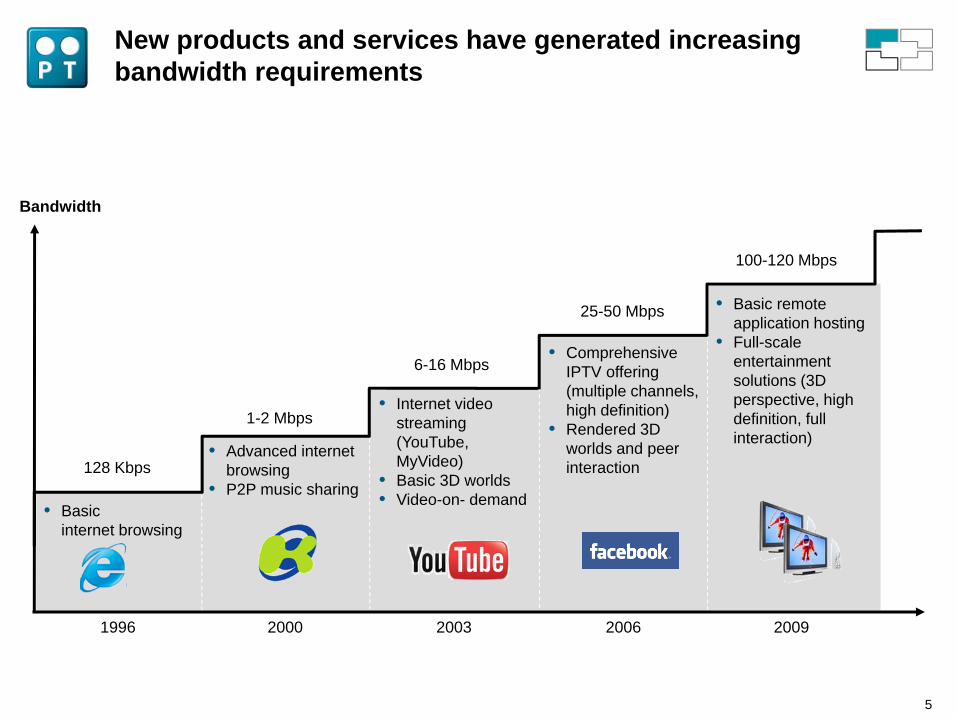

New products and services have generated increasing bandwidth requirements

Bandwidth

• Advanced internet browsing

• P2P music sharing• Basic

internet browsing

• Internet video streaming (YouTube, MyVideo)

• Basic 3D worlds• Video-on- demand

• Comprehensive IPTV offering (multiple channels, high definition)

• Rendered 3D worlds and peer interaction

• Basic remote application hosting

• Full-scale entertainment solutions (3D perspective, high definition, full interaction)

128 Kbps

1-2 Mbps

6-16 Mbps

25-50 Mbps

100-120 Mbps

2009 2006 2003 2000 1996

6

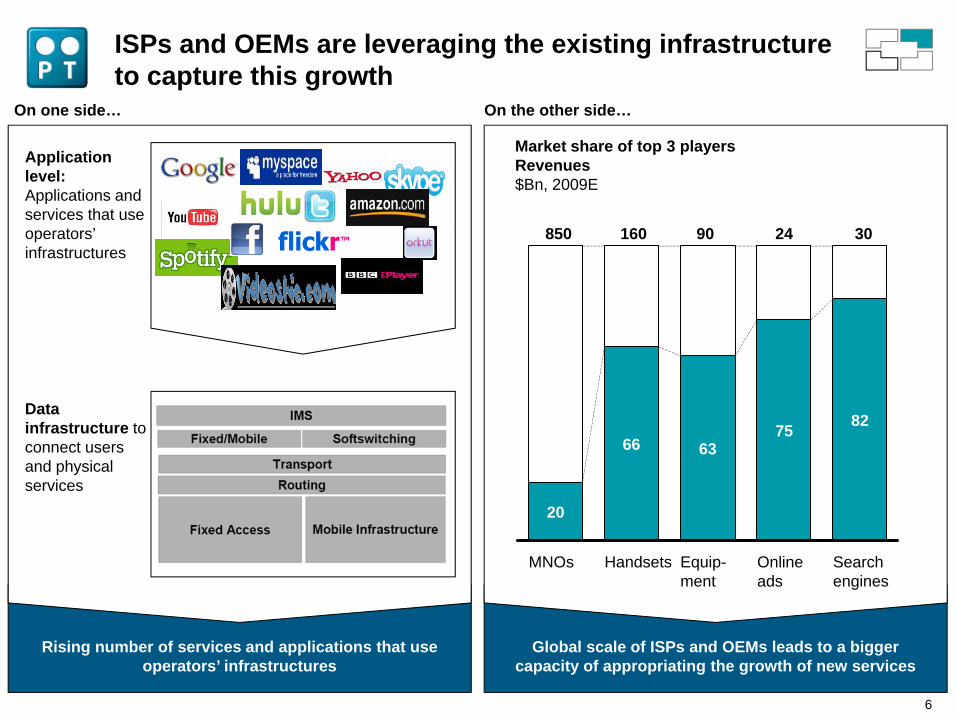

ISPs and OEMs are leveraging the existing infrastructure to capture this growth

Global scale of ISPs and OEMs leads to a bigger capacity of appropriating the growth of new services

Market share of top 3 playersRevenues$Bn, 2009E

850 160 90 24 30

Search engines

82

Onlineads

75

Equip-ment

63

Handsets

66

MNOs

20

Data infrastructure to connect users and physical services

Application level: Applications and services that use operators’ infrastructures

Rising number of services and applications that use operators’ infrastructures

On the other side…On one side…

7

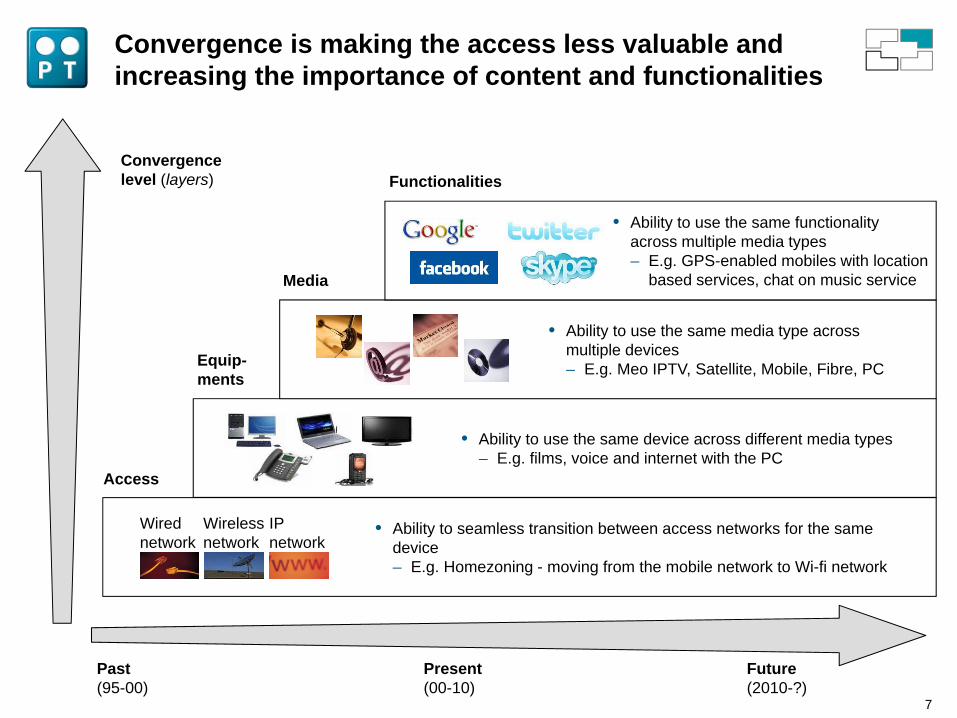

Convergence is making the access less valuable and increasing the importance of content and functionalities

Wired network

Wireless network

IP network

Functionalities

Media

Equip-ments

Access

• Ability to use the same media type across multiple devices– E.g. Meo IPTV, Satellite, Mobile, Fibre, PC

• Ability to use the same device across different media types – E.g. films, voice and internet with the PC

• Ability to seamless transition between access networks for the same device– E.g. Homezoning - moving from the mobile network to Wi-fi network

• Ability to use the same functionality across multiple media types– E.g. GPS-enabled mobiles with location

based services, chat on music service

Convergence level (layers)

Past(95-00)

Present(00-10)

Future(2010-?)

8

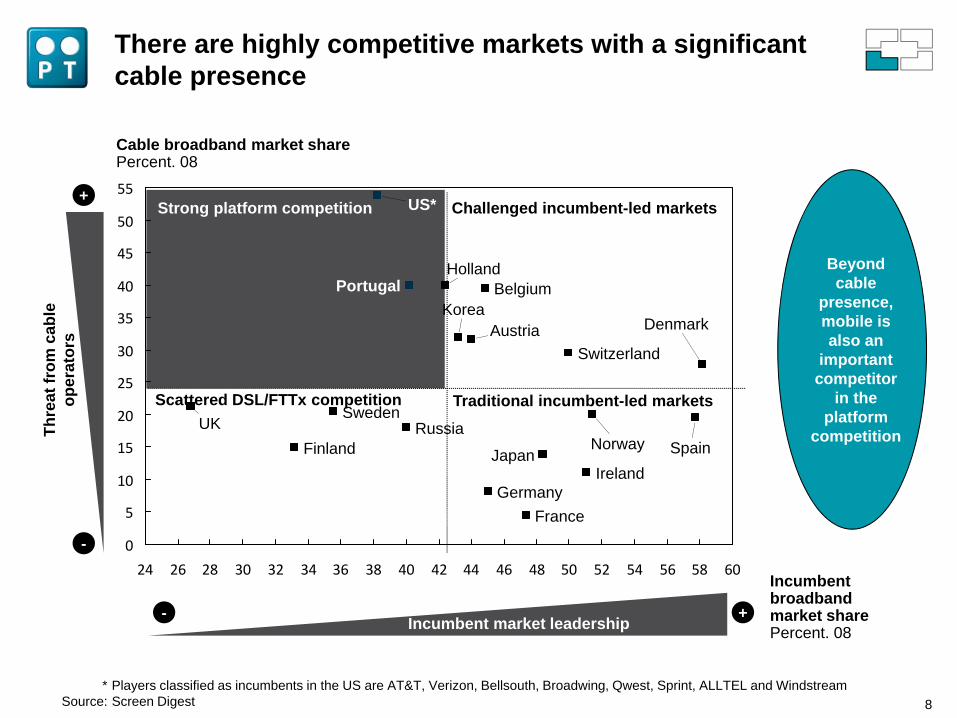

Traditional incumbent-led markets

0

5

10

15

20

25

30

35

40

45

50

55

24 26 28 30 32 34 36 38 40 42 44 46 48 50 52 54 56 58 60

Cable broadband market sharePercent. 08

Japan

Korea

Russia

US*

UK

Switzerland

Sweden

Spain

Portugal

Norway

Holland

IrelandGermany

Finland

France

Denmark

Belgium

Austria

* Players classified as incumbents in the US are AT&T, Verizon, Bellsouth, Broadwing, Qwest, Sprint, ALLTEL and WindstreamSource: Screen Digest

+

-

Thre

at fr

om c

able

op

erat

ors

Incumbent broadband market sharePercent. 08

+- Incumbent market leadership

There are highly competitive markets with a significant cable presence

Scattered DSL/FTTx competition

Challenged incumbent-led markets

Beyond cable

presence, mobile is also an

important competitor

in the platform

competition

Strong platform competition

9

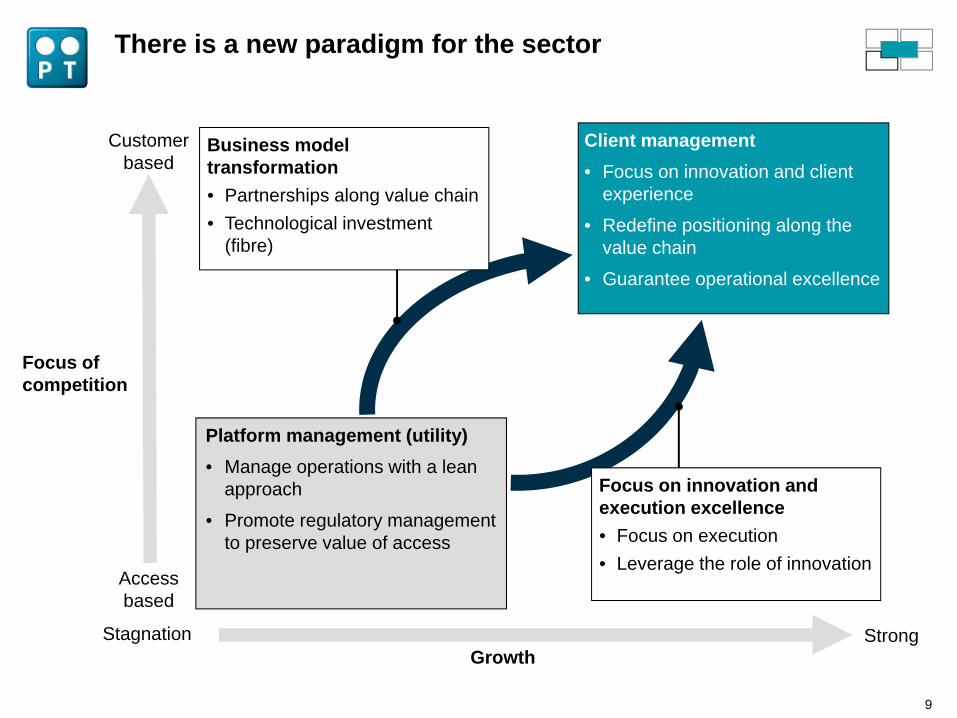

There is a new paradigm for the sector

Client management• Focus on innovation and client

experience

• Redefine positioning along the value chain

• Guarantee operational excellence

Platform management (utility)• Manage operations with a lean

approach

• Promote regulatory management to preserve value of access

Focus of competition

GrowthStagnation

Access based

Strong

Customer based

Focus on innovation and execution excellence• Focus on execution• Leverage the role of innovation

Business model transformation• Partnerships along value chain• Technological investment

(fibre)

10

Agenda

A new paradigm for the sector

PT with a clear strategy for FTTH

Enabling the fibre potential

11

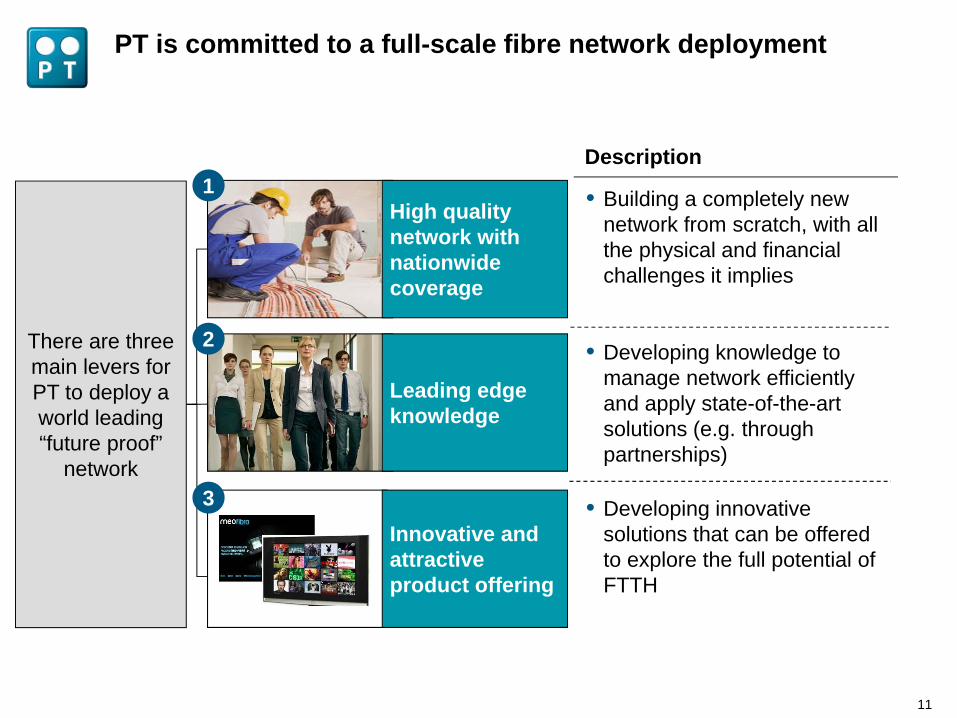

PT is committed to a full-scale fibre network deployment

Description

• Building a completely new network from scratch, with all the physical and financial challenges it implies

High quality network with nationwide coverage

• Developing knowledge to manage network efficiently and apply state-of-the-art solutions (e.g. through partnerships)

• Developing innovative solutions that can be offered to explore the full potential of FTTH

There are three main levers for PT to deploy a world leading “future proof”

network

1

Leading edge knowledge

2

Innovative and attractive product offering

3

12

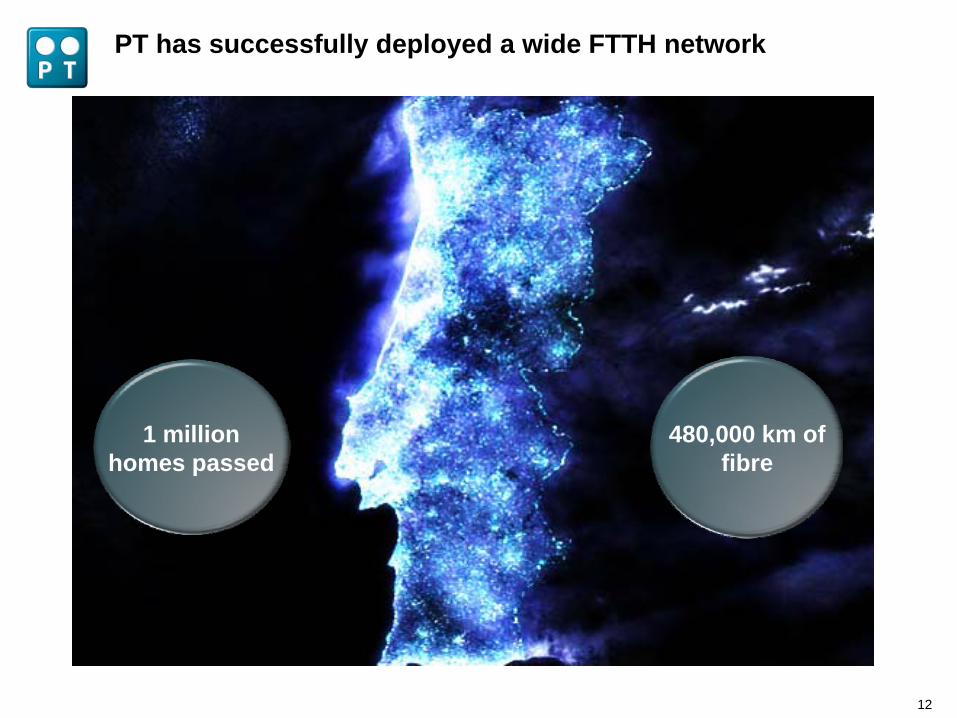

PT has successfully deployed a wide FTTH network

1 million homes passed

480,000 km of fibre

13

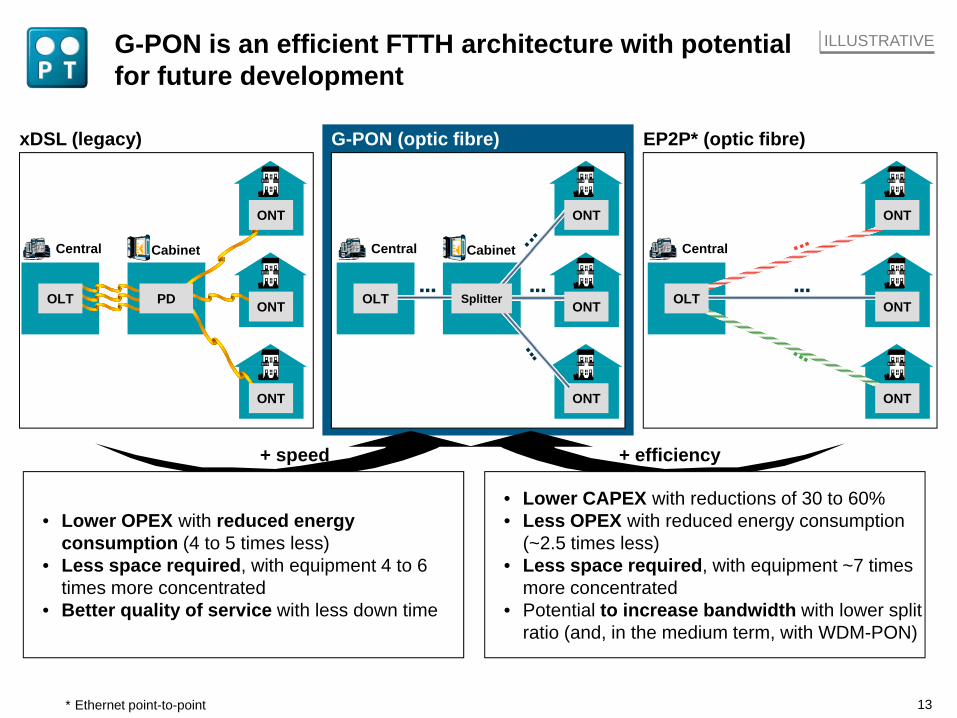

EP2P* (optic fibre)

G-PON is an efficient FTTH architecture with potential for future development

* Ethernet point-to-point

xDSL (legacy) G-PON (optic fibre)

Central Cabinet

ONT

ONT

ONT

OLT

Central

ONT

ONT

OLT

ONT

Central Cabinet

OLT

ONT

ONT

ONTPD Splitter

• Lower CAPEX with reductions of 30 to 60%• Less OPEX with reduced energy consumption

(~2.5 times less)• Less space required, with equipment ~7 times

more concentrated• Potential to increase bandwidth with lower split

ratio (and, in the medium term, with WDM-PON)

• Lower OPEX with reduced energy consumption (4 to 5 times less)

• Less space required, with equipment 4 to 6 times more concentrated

• Better quality of service with less down time

+ speed + efficiency

ILLUSTRATIVE

14

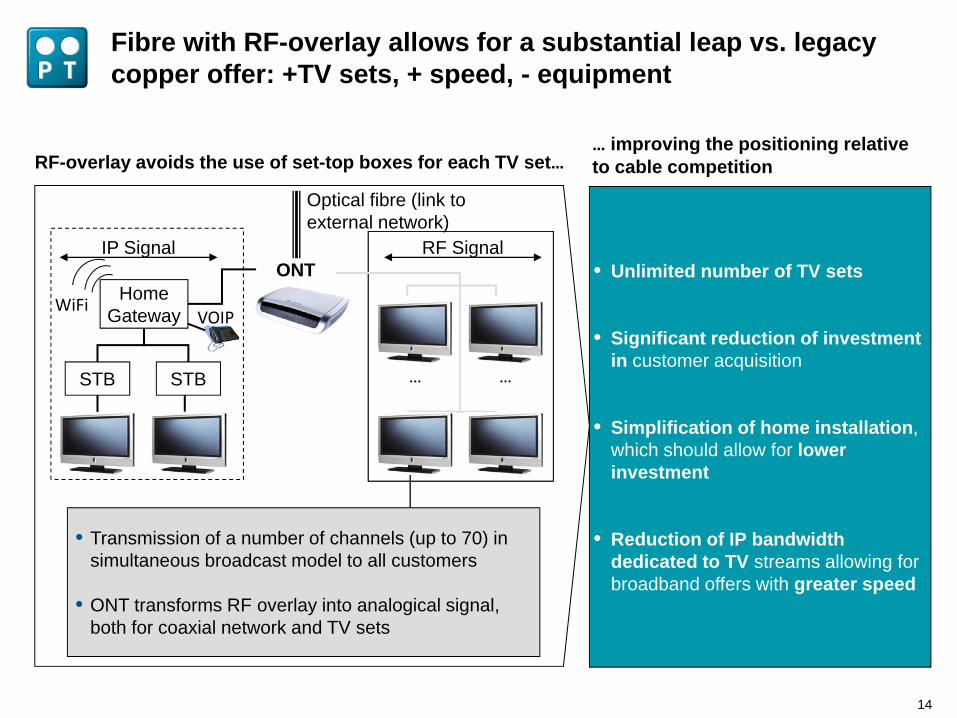

Fibre with RF-overlay allows for a substantial leap vs. legacy copper offer: +TV sets, + speed, - equipment

• Unlimited number of TV sets

• Significant reduction of investment in customer acquisition

• Simplification of home installation, which should allow for lower investment

• Reduction of IP bandwidth dedicated to TV streams allowing for broadband offers with greater speed

… improving the positioning relative to cable competitionRF-overlay avoids the use of set-top boxes for each TV set…

Optical fibre (link to external network)

IP Signal RF Signal

STB

• Transmission of a number of channels (up to 70) in simultaneous broadcast model to all customers

• ONT transforms RF overlay into analogical signal, both for coaxial network and TV sets

ONT

WiFiHome

Gateway VOIP

STB … …

15

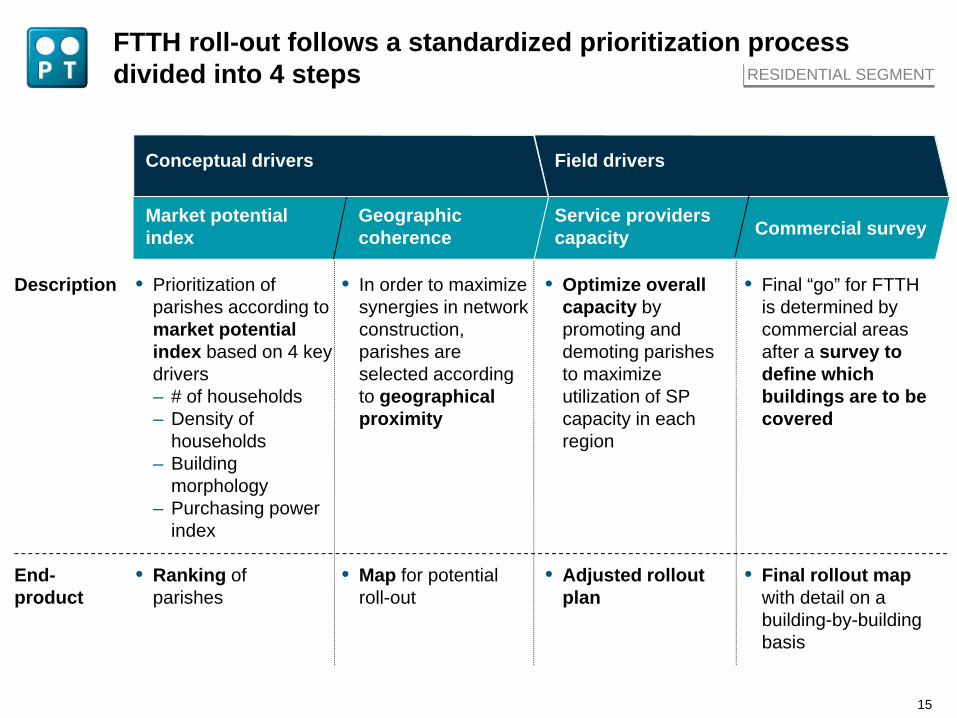

FTTH roll-out follows a standardized prioritization process divided into 4 steps

Market potential index

Geographic coherence

Field drivers

Service providers capacity Commercial survey

Description

End-product

• Prioritization of parishes according to market potential index based on 4 key drivers– # of households– Density of

households– Building

morphology– Purchasing power

index

• Ranking of parishes

• In order to maximize synergies in network construction, parishes are selected according to geographical proximity

• Map for potential roll-out

• Optimize overall capacity by promoting and demoting parishes to maximize utilization of SP capacity in each region

• Adjusted rollout plan

• Final “go” for FTTH is determined by commercial areas after a survey to define which buildings are to be covered

• Final rollout mapwith detail on a building-by-building basis

Conceptual drivers

RESIDENTIAL SEGMENT

16

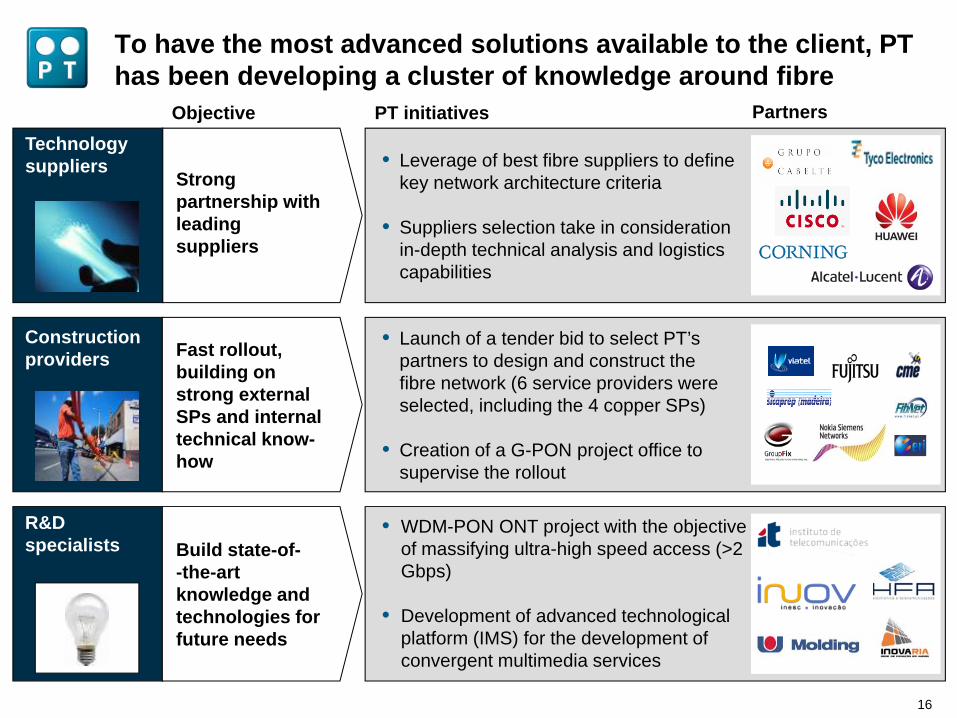

To have the most advanced solutions available to the client, PT has been developing a cluster of knowledge around fibre

Objective PT initiatives

Construction providers Fast rollout,

building on strong external SPs and internal technical know-how

Technologysuppliers

Strong partnership with leading suppliers

Partners

• Launch of a tender bid to select PT’s partners to design and construct the fibre network (6 service providers were selected, including the 4 copper SPs)

• Creation of a G-PON project office to supervise the rollout

• Leverage of best fibre suppliers to define key network architecture criteria

• Suppliers selection take in consideration in-depth technical analysis and logistics capabilities

Build state-of--the-art knowledge and technologies for future needs

R&D specialists

• WDM-PON ONT project with the objective of massifying ultra-high speed access (>2 Gbps)

• Development of advanced technological platform (IMS) for the development of convergent multimedia services

17

Agenda

A new paradigm for the sector

PT with a clear strategy for FTTH

Enabling the fibre potential

18

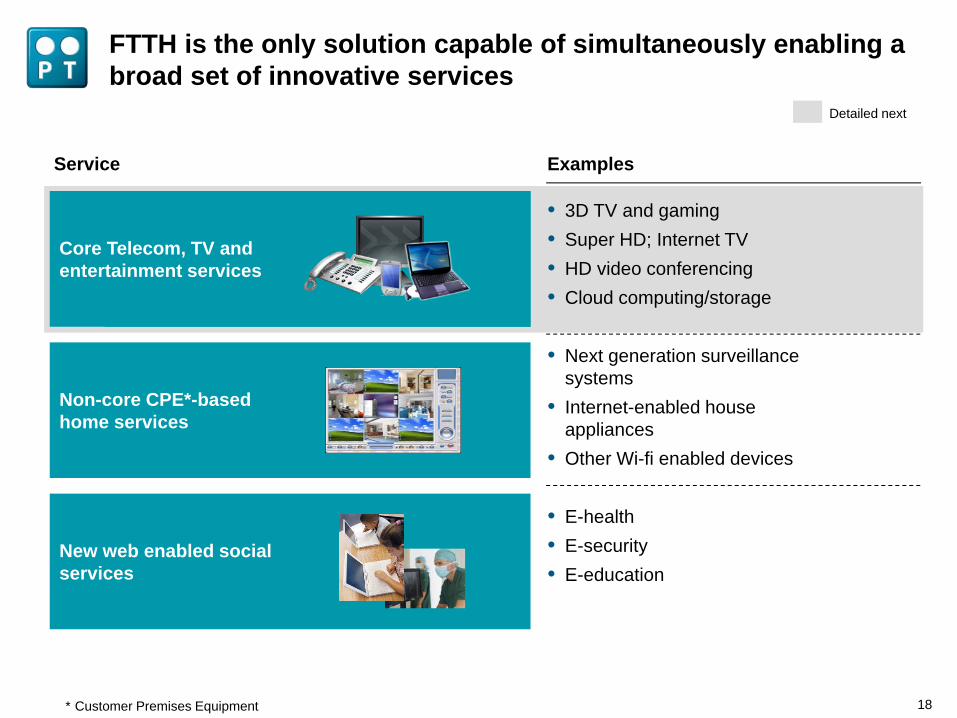

Non-core CPE*-based home services

New web enabled social services

Core Telecom, TV and entertainment services

FTTH is the only solution capable of simultaneously enabling a broad set of innovative services

* Customer Premises Equipment

Core Telecom, TV and entertainment services

Examples

• 3D TV and gaming • Super HD; Internet TV• HD video conferencing• Cloud computing/storage

• Next generation surveillance systems

• Internet-enabled house appliances

• Other Wi-fi enabled devices

• E-health• E-security• E-education

Service

Detailed next

19

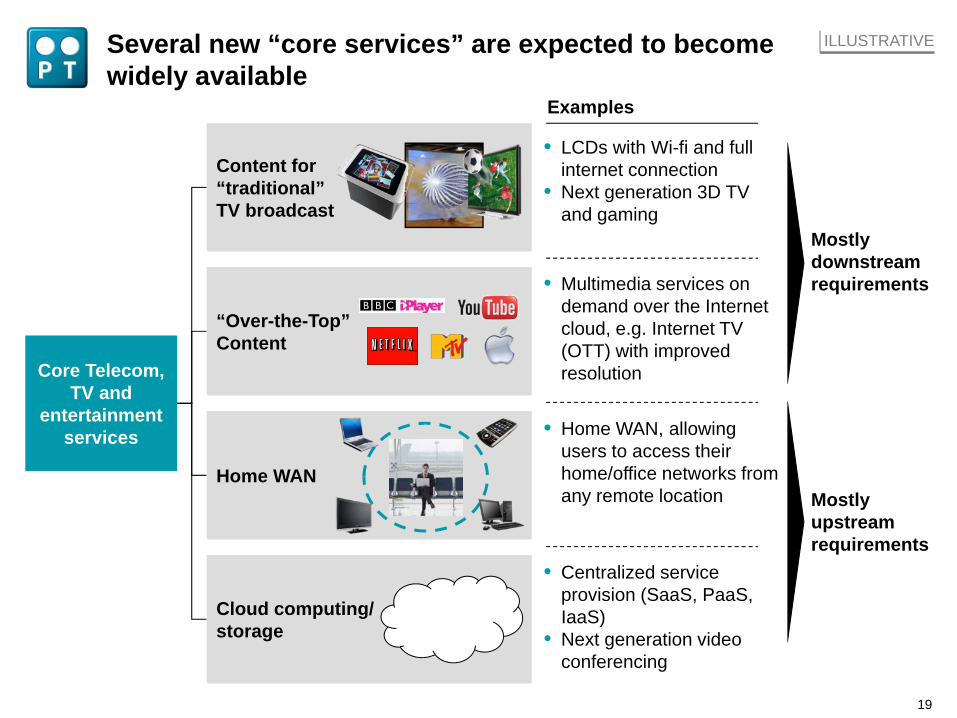

Core Telecom,TV and

entertainment services

“Over-the-Top”Content

Content for “traditional”TV broadcast

Cloud computing/storage

Home WAN

Examples

• LCDs with Wi-fi and full internet connection

• Next generation 3D TV and gaming

• Home WAN, allowing users to access their home/office networks from any remote location

• Multimedia services on demand over the Internet cloud, e.g. Internet TV (OTT) with improved resolution

• Centralized service provision (SaaS, PaaS, IaaS)

• Next generation video conferencing

Mostly downstream requirements

Mostly upstream requirements

Several new “core services” are expected to become widely available

ILLUSTRATIVE

20

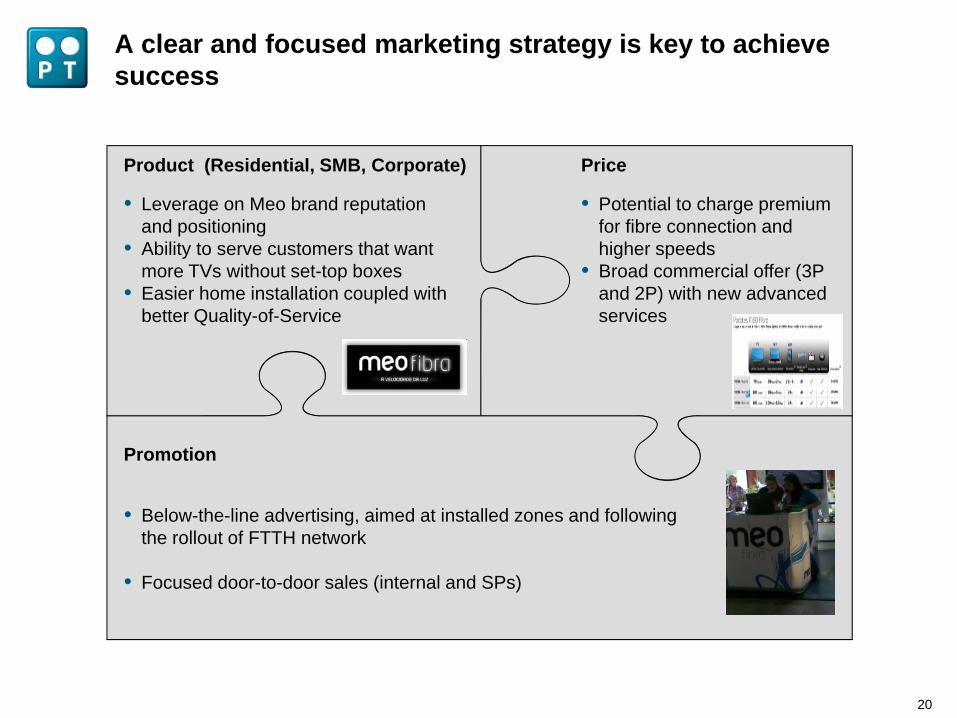

A clear and focused marketing strategy is key to achieve success

Product (Residential, SMB, Corporate) Price

Promotion

• Leverage on Meo brand reputation and positioning

• Ability to serve customers that want more TVs without set-top boxes

• Easier home installation coupled with better Quality-of-Service

• Potential to charge premium for fibre connection and higher speeds

• Broad commercial offer (3P and 2P) with new advancedservices

• Below-the-line advertising, aimed at installed zones and following the rollout of FTTH network

• Focused door-to-door sales (internal and SPs)

21

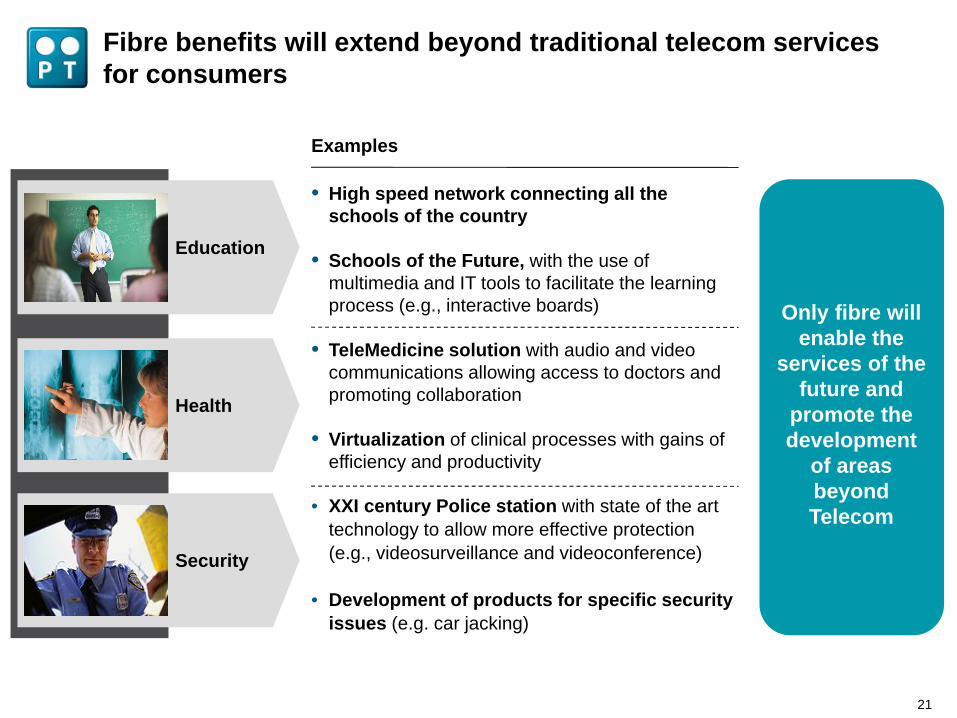

Fibre benefits will extend beyond traditional telecom services for consumers

Education

Health

Security

• High speed network connecting all the schools of the country

• Schools of the Future, with the use of multimedia and IT tools to facilitate the learning process (e.g., interactive boards)

• TeleMedicine solution with audio and video communications allowing access to doctors and promoting collaboration

• Virtualization of clinical processes with gains of efficiency and productivity

• XXI century Police station with state of the art technology to allow more effective protection (e.g., videosurveillance and videoconference)

• Development of products for specific security issues (e.g. car jacking)

Only fibre will enable the

services of the future and

promote the development

of areas beyond Telecom

Examples

22

Ambitious targets for the 2009-2011 triennium

Leadership Leadership in all segments and geographies

Sustainability Reference in the sector at a social, economic and environmental level

Performance Top-quartile performance in shareholder return and operational and financial results

International Two thirds of revenues from international business

Clients 100 million customers