Embed Size (px)

Citation preview

special report:MaiNteNaNce2013

DeceMBer 2013

Keeping maintenance in-house continues to be the preferred option for most of Europe’s larger short-haul operators, as is the case when it comes to deciding where to place continuing airworthiness management responsibilities. Meanwhile, used serviceable parts prove that money can be saved when airlines recycle and reuse

SPECIAL REPORT MAINTENANCE

flightglobal.com/airlines December 2013 | Airline Business | 27

28 In or out? EASA will allow airlines to fully outsource continuing airworthiness management responsibilities, but carriers are still keen to keep them in-house

34 Second life Airlines are increasingly finding ways to make huge maintenance

savings by employing used serviceable parts in their overhaul programmes

36 Maintaining control Short-haul airframe maintenance in Europe remains a largely in-house activity, despite the rise of the low-cost carriers

CONTENTS

All our special reports are available online atflightglobal.com/airlines

Luft

hans

a Te

chni

k

flightglobal.com/ab28 | Airline Business |

maintenance strategy

RepoRtMichael Gubisch london

Start-up airlines commonly sub-contract part of their continuing airworthiness management duties to external specialists to keep overheads low and focus on flight

operations. But as their businesses mature and fleets grow, some carriers move the office-based engineering jobs back in-house for greater process control and independence.

No matter whether tasks such as mainte-nance planning or service bulletin and airworthiness directive reviewing are subcontracted to external engineering bureaus or not, the airlines must still have a continuing airworthiness management organ-isation (CAMO) approval, as they remain ulti-mately responsible for their aircraft’s service-ability. The operators must ensure oversight of their MRO partners, keep technical records up to date and conduct all mandatory report-ing to regulators.

However, EASA has been proposing a rule change which would allow carriers to con-tract all continuing airworthiness manage-ment responsibility including all regulatory reporting to external agencies.

Airlines would no longer need to have a CAMO approval, but would be required to implement control procedures to ensure that the contractors fulfilled their obligations.

insourcinGEasyJet insourced all continuing airworthi-ness management activities in February 2010, after a number of tasks had previously been conducted through the budget carrier’s MRO partner SR Technics. When the insourcing decision was taken in 2009, EasyJet had grown from an initial operation with two wet-leased Boeing 737s in 1995 to around 160 aircraft. This has since expanded to nearly 220 Airbus A320-family aircraft.

Today, the fleet technical management department comprises 42 staff members, who are conducting all continuing airworthiness management tasks, including maintenance planning, modification design, aircraft soft-ware control and mandatory reliability pro-grammes to prove that the airline’s MRO arrangements are effective.

Insourcing continuing airworthiness management has clearly created cost savings for engineering projects, says Swaran Sidhu, EasyJet’s head of fleet technical management. But more importantly, he adds, building up the in-house capabilities has led to greater independence and process control, and c reated an appetite among the team for inno-vation, greater efficiency and continuously improving the technical operations. “We are master of our own destiny rather than having to rely on others to build up intelligence,” he

says. For example, the duration of reviewing modifications, such as galley changes, has been cut from up to 100 days to around 20 days today due to lean production methods. The greater in-house engineering competence has also put EasyJet, which tenders most of its MRO requirements on the open market, in a much stronger position versus maintenance providers, because the airline can make better informed judgements about the contractor’s work. Fleet growth and the urge for independ-ence have been EasyJet’s main drivers to build up its fleet technical management capabili-

ties. Continuing airworthiness management was initially outsourced because the airline wanted to establish its network and brand.

“It made sense to contract continuing air-worthiness management out to specialised MROs, because they offered tailored [support] package solutions that we were looking for,” says Sidhu. “It was also about keeping simplicity at the forefront and predictability of the cost base.”

As the fleet grew in size, however, continu-ing airworthiness management became more demanding and outsourcing the tasks in

december 2013

in or out?EASA plans to permit airlines to fully outsource their continuing airworthiness management responsibilities, but carriers and authorities see clear advantages in keeping engineering expertise in-house

EasyJet’s brought all continuing airworthiness management activities in-house in 2010

ABU_291113_028-031.indd 28 2013-11-28 12:41

flightglobal.com/ab | Airline Business | 29

question did not automatically mean greater simplicity anymore. “Managing outsourced products presents different challenges, such as managing MRO oversight and influencing change itself, and maintaining a lean cost base,” says Sidhu. Ensuring adequate over-sight became more difficult with the existing small team and the engineers wanted to have more control.

STRATEGIC REVIEWEasyJet’s growth prompted the executive team to undertake a strategic review of the airline’s technical capabilities, which led to the deci-sion to set up a full fleet technical manage-ment department in-house. The preparations took about a year, with the switchover being made in February 2010.

Robert Nyenhuis, vice-president aircraft engineering at Lufthansa Technik, agrees that as airlines expand their fleets and networks, they typically come to a point where the exist-ing maintenance arrangements are reviewed. The German MRO provider conducts contin-uing airworthiness management services for a number of external customers and has had clients that later took the work in-house.

When a carrier grows, the maintenance tasks become more complex, often new IT systems need to be implemented, and the ways in which the technical work is organised change, says Nyenhuis.

EasyJet took about a year to set up the required department and prepare the transfer of technical data from SR Technics to the airline’s Luton headquarters. Moving that information across was a central challenge, says Sidhu, especially as the airline and MRO provider employed different IT systems.

Recruiting the required talent for the fleet technical management department was per-haps even more complex. Initially, the airline employed temporary contractors as it was not yet clear how many and what kind of special-ists were necessary to look after the fleet. However, when Sidhu joined EasyJet in early 2010, he says it became quickly evident that the core team needed to be directly employed on a permanent basis. “We need to replace the contracted workforce with our own people for two reasons: firstly to prevent the loss of intelligence when people leave the organisa-tion [and] secondly to establish a harmonised culture that would deliver the objectives,” he

says. “People come from different organisa-tions with different cultures and thinking in their mind,” he adds. For this to be adapted to the airline’s own environment takes time. As a result, EasyJet replaced all temporary staff with its own engineers by 2011, with about half of the contractors taking the carrier’s offer for permanent employment.

However, there are also airlines that con-tinue to outsource continuing airworthiness management tasks even after becoming more established. Hungarian budget carrier Wizz Air, for example, has extended its fleet techni-cal management agreement with Lufthansa Technik. Whether or not such co-operations continue depends on customer experience with the service provider, says Nyenhuis.

KNOWLEDGE POOLOperators contract Lufthansa Technik not just to outsource certain continuing airworthiness management tasks, he says, but, crucially, to tap into the MRO group’s knowledge pool from handling a number of different carriers. “Due to many customers, we are relatively large and provide a great depth [of engineer-ing experience]. This is a benefit for smaller airlines which, even if they wanted to conduct all CAM in-house, they could not achieve this [capability] depth themselves. Building that up and employing the necessary staff would be too expensive,” Nyenhuis says.

Small airlines almost always look for part-nerships to fulfil their continuing airworthi-ness management duties. “There are virtually no low-cost carriers that try to start up and do everything themselves,” he says. But as airlines try to reduce their costs, larger opera-tors also evaluate the benefits of external spe-cialists against their own engineering teams, even if outsourcing is only considered for individual tasks or projects, he adds.

A further benefit of using external engineer-ing consultants is to gain independent advice in negotiations with original equipment man-ufacturers. The OEMs are building up their product support businesses and trying to con-trol the aftermarket by, for example, gathering operational data from their equipment and restricting access to technical information. However, aircraft maintenance is “very dynamic” and frequently brings up surprise issues that demand quick solutions, says Nyenhuis. If airlines are left to deal with the OEMs on their own when the manufacturer is responsible both for the cause and remedy of a problem, the situation becomes difficult for the operators. He says: “The question always comes up: Who represents the airlines before the OEMs, when the operators have neither a critical solicitor nor their own [technical] competence anymore?”

The central challenge of a fleet technical management partnership is to set up an inter-face between the airline and service provider

December 2013

Easy

Jet

flightglobal.com/ab30 | Airline Business |

MAINTENANCE STRATEGY

that allows appropriate levels of control and transparency. The relationship is not limited to the engineering bureau completing certain technical tasks, which the operator takes in turn to the regulator for approval. The airline must instead have oversight of its engineering partner, as the carrier remains responsible for its fleet’s airworthiness.

All relevant technical data must therefore be directed to the airline in real time so the carrier can verify that its aircraft are in good operating condition ahead of departure. The objective is to give the operator “active con-trol through direct involvement” with the engineering partner, says Nyenhuis. But if that is not achieved, there is likely to be trou-ble between the carrier and regulator, and the airline will seek other solutions such as insourcing, he says.

December 2013

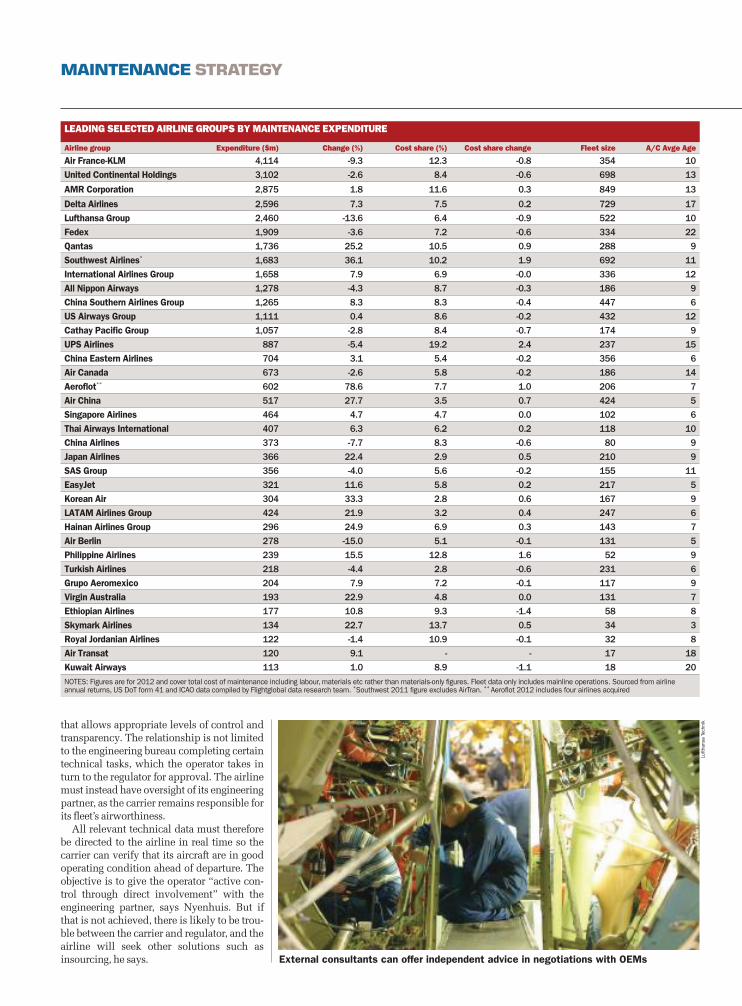

LEADING SELECTED AIRLINE GROUPS BY MAINTENANCE EXPENDITURE

Airline group Expenditure ($m) Change (%) Cost share (%) Cost share change Fleet size A/C Avge Age

Air France-KLM 4,114 -9.3 12.3 -0.8 354 10

United Continental Holdings 3,102 -2.6 8.4 -0.6 698 13

AMR Corporation 2,875 1.8 11.6 0.3 849 13

Delta Airlines 2,596 7.3 7.5 0.2 729 17

Lufthansa Group 2,460 -13.6 6.4 -0.9 522 10

Fedex 1,909 -3.6 7.2 -0.6 334 22

Qantas 1,736 25.2 10.5 0.9 288 9

Southwest Airlines* 1,683 36.1 10.2 1.9 692 11

International Airlines Group 1,658 7.9 6.9 -0.0 336 12

All Nippon Airways 1,278 -4.3 8.7 -0.3 186 9

China Southern Airlines Group 1,265 8.3 8.3 -0.4 447 6

US Airways Group 1,111 0.4 8.6 -0.2 432 12

Cathay Pacific Group 1,057 -2.8 8.4 -0.7 174 9

UPS Airlines 887 -5.4 19.2 2.4 237 15

China Eastern Airlines 704 3.1 5.4 -0.2 356 6

Air Canada 673 -2.6 5.8 -0.2 186 14

Aeroflot** 602 78.6 7.7 1.0 206 7

Air China 517 27.7 3.5 0.7 424 5

Singapore Airlines 464 4.7 4.7 0.0 102 6

Thai Airways International 407 6.3 6.2 0.2 118 10

China Airlines 373 -7.7 8.3 -0.6 80 9

Japan Airlines 366 22.4 2.9 0.5 210 9

SAS Group 356 -4.0 5.6 -0.2 155 11

EasyJet 321 11.6 5.8 0.2 217 5

Korean Air 304 33.3 2.8 0.6 167 9

LATAM Airlines Group 424 21.9 3.2 0.4 247 6

Hainan Airlines Group 296 24.9 6.9 0.3 143 7

Air Berlin 278 -15.0 5.1 -0.1 131 5

Philippine Airlines 239 15.5 12.8 1.6 52 9

Turkish Airlines 218 -4.4 2.8 -0.6 231 6

Grupo Aeromexico 204 7.9 7.2 -0.1 117 9

Virgin Australia 193 22.9 4.8 0.0 131 7

Ethiopian Airlines 177 10.8 9.3 -1.4 58 8

Skymark Airlines 134 22.7 13.7 0.5 34 3

Royal Jordanian Airlines 122 -1.4 10.9 -0.1 32 8

Air Transat 120 9.1 - - 17 18

Kuwait Airways 113 1.0 8.9 -1.1 18 20NOTES: Figures are for 2012 and cover total cost of maintenance including labour, materials etc rather than materials-only figures. Fleet data only includes mainline operations. Sourced from airline annual returns, US DoT form 41 and ICAO data compiled by Flightglobal data research team. *Southwest 2011 figure excludes AirTran. ** Aeroflot 2012 includes four airlines acquired

External consultants can offer independent advice in negotiations with OEMs

Lufth

ansa

Tec

hnik

flightglobal.com/ab | Airline Business | 31

EASA has been facing strong opposition to its proposed rule change that would allow commercial air transport operators to out-source all continuing airworthiness manage-ment responsibility, including all dealings with authorities. Airlines would no longer need their own CAMO approval, but would instead be mandated to implement supervi-sory measures under a new continuing air-worthiness control exposition manual to ensure that their external service providers fulfil their responsibility.

AFTERMARKET PROGRAMMESA key driver behind the new rules have been the aircraft manufacturers, as the change would allow the OEMs to include continuing airworthiness management services in their aftermarket programmes. But much head-wind has come from some of Europe’s national aviation authorities, which interpret EASA’s proposal differently. Germany’s LBA, for example, pursues a strict line of the pre-sent regulations, where airlines need to remain fully responsible for their aircraft’s air-worthiness. The rule change could help small carriers which “may find it difficult to have the full in-house expertise” to manage the continuing airworthiness of their fleets, the European authority says in its notice of pro-posed amendment from July 2010. Another advantage would be that operators which are dry-leasing aircraft for a short-term period can outsource the necessary continuing air-

worthiness management work to a specialist, if the type in question is not covered under the airline’s existing CAMO approval.

EASA argues that the new regulation will improve the current situation where a num-ber of operators have been found to subcon-tract continuing airworthiness management services with “inadequate oversight resources and with no active control of the activities”.

The new regulation would improve author-ity oversight of continuing airworthiness management service providers, claims EASA.

Today, an airline can subcontract tasks to external engineering agencies which do not need to have a CAMO approval of their own. However, if a carrier outsources all continu-ing airworthiness management services under the new rules, the service provider would need to be certificated and audited by the authorities. Meanwhile, airlines will still have the option to conduct conventional fleet technical management under their own CAMO approval. Nevertheless, the rule has not been approved because doubts remain among national aviation authorities and air-lines over whether the new regulation will guarantee adequate CAMO control.

“There will really be a split of responsibil-ity” between operators and their continuing airworthiness management service providers, says Jorge Leite, vice-president quality and safety at the maintenance arm of Portuguese flag carrier TAP. “It is more like an oversight of the CAMO rather than in-house quality management” that airlines would need to conduct. Yet, some of the proposal’s splitting and sharing of responsibilities are not clear, he says.

Leite agrees that small carriers with limited resources could benefit from the rule change. But he is convinced that the ability to manage aircraft airworthiness is a central part of an airline’s business and having that engineering capability in house pays dividends both oper-ationally and in customer perception terms. “People don’t like the word outsource, because it almost gives a sense that you are discharging your responsibility. For a medium or large airline that can afford to have the CAMO [activities] inside, I think it is a benefit for the business and image,” he says.

Lufthansa Technik is in favour of the EASA proposal, unsurprisingly given that it is a third-party continuing airworthiness manage-ment service provider based on the engineer-ing department for its parent fleet, but Nyen-huis nevertheless says that the regulatory change is very complex. “There is much emo-tion involved. But I firmly believe that it will come. On the one side, this is based on indus-trial reasons, because the OEMs have a keen interest in it and are strongly pushing for it. On the other, operators have the possibility to further strengthen their technical competence and save money,” he says.

Nyenhuis is also convinced that the proposal does not need significant further revising to overcome any prevailing reserva-tions. “The proposal has now a maturity degree that doesn’t requiring much more finessing. I don’t think we need to go around in circles much more.”

EASA, meanwhile, declines to comment. ■

December 2013

SELECTED CIVIL MAINTENANCE PROVIDERS WITH AIRFRAME/ENGINE CAPABILITIES

Company Country Revenues ($m) Change (%)

GE Engine Services USA 6,900 -4.2%

Pratt & Whitney USA 6,312 -6.0%

Rolls-Royce Aerospace UK 5,577 3.8%

Lufthansa Technik AG Germany 5,177 -9.5%

Air France Industries-KLM Engineering France 4,043 -7.1%

Honeywell Aerospace USA 2,947 4.2%

AMR Corporation USA 2,875 1.8%

Goodrich Corporation USA 2,447 1.0%

MTU Maintenance Germany 1,684 7.9%

ST Aerospace Singapore 1,622 5.5%

SR Technics Holding Switzerland 1,179 -5.6%

US Airways USA 1,111 0.4%

Singapore Airlines Singapore 921 -1.7%

HAECO China, Hong Kong 752 13.1%

Sabena Technics France 613 -

Delta TechOps USA 600 -7.7%

Ameco Beijing China 488 14.8%

Turkish Technic Turkey 468 -4.5%

Embraer Brazil 451 -31.6%

AAR Corporation USA 450 6.6%

Timco USA 255 21.4-

TAP Maintenance & Engineering Portugal 240 9.6%

Malaysia Airlines E&M Malaysia 130 -11.0%

NOTES: 2012 revenues for airline groups include service for in-house carrier and third parties. Estimates have been used where commercial maintenance revenues are not published. SOURCE: Airline Business research, annual reports, US DoT form 41 and ICAO. All changes based on US dollar figures

In-sourcing often offers cost benefits

To sign up for a trial of Flightglobal Pro’s maintenance feed, visit: flightglobal.com/MRO

Lufth

ansa

Tec

hnik

flightglobal.com/ab34 | Airline Business |

As airlines look to widen their profit margins, aircraft mainte-nance is a line item where opera-tors have opportunities to cut costs. Some of these airlines are

finding substantial savings through used ser-viceable parts procured from a previously used engine and refurbished to the standard of a new part. This material can save money on airlines’ cost of ownership when it comes to engine repairs.

The world market for used serviceable material is worth $3 billion, says Canaccord Genuity analyst Ken Herbert in a recent research note. An estimated 90% of material for older engines, such as the General Electric CF6-80C2, the CFM International CFM56-3B and the Pratt & Whitney JT8D, falls into this category, but Herbert notes that retirements of narrowbody engines will begin to make addi-tional material available to the market.

“Many OEMs [original equipment manu-facturers] have been forced to reduce their forecast for spare parts sales at least once or twice during the year, with the emergence of the [used serviceable material] market most often cited as the source of underper-formance,” says Herbert.

According to the Flightglobal Fleet Fore-cast, recently published by the Ascend Advi-sory team, 2,780 passenger jets are expected to be removed from service over the next five years. Between 2018 and 2022, an additional 3,840 jets will be retired. Ascend estimates that 55% of passenger aircraft delivered since 2008 represent those used for replacement.

cost savingsAirlines are paying more attention to sourcing used serviceable material to save on costs in more instances than aircraft on ground (AOG) emergencies or parts shortages, shows a sur-vey of airlines published by consulting firm Oliver Wyman in April.

Two-thirds of airlines that responded to the survey indicated that they have been using more used serviceable parts in the past three years. By comparison, only 8% said they declined the use of these parts.

More than 70% of airlines responding to the survey said they were “actively seeking out” used serviceable material, with almost 50% saying that the material was part of a comprehensive parts strategy.

“Airlines are getting better at managing this market in a more sophisticated way, and they’re using it more proactively as a cost sav-ings lever,” says Oliver Wyman partner Chris Spafford.

RepoRtkristin majcher washington dc

Pratt & Whitney provides used serviceable material at more than 30 locations

december 2013

SECOND LIFEAirlines are making significant savings on maintenance by giving a new lease of life to used serviceable parts. This section of the market is growing as more and more carriers become aware of the financial benefits of sourcing such material and reusing their own

prat

t & w

hitn

ey

maINtENaNCE SparES

ABU_291113_034-035.indd 34 2013-11-27 18:06

flightglobal.com/ab | Airline Business | 35

Southwest Airlines is an example of an air-line finding savings from used material. This year, the Dallas-based carrier opted to change the maintenance contract for the CFM56-3 engines from a power-by-the-hour agreement to an end-of-life programme with MTU, which harvests its engines for serviceable material and puts it back into the fleet.

“On the -3 side, the engines that are going to MTU, we are tearing down a lot of our owned engine assets that we don’t need for spares,” says Amanda Gower, manager of Southwest’s powerplant supply chain. “So they’ll tear the engines down for us to piece-part level and make the parts servicea-ble and put them in a customer-owned prop-erty stock so those will be fed directly back into our engines.”

Gower does not disclose how much the air-line is saving from employing this strategy, but says that “it’s a big number”.

“With the -3 programme, it’s all about mini-mising expense on exiting fleets,” says Gower. “So if we have an opportunity in the industry or in the market to go and buy a serviceable engine with green time that is cheaper than doing a full overhaul, then we’re looking at those options, as well as we’re looking at leas-ing engines from the market to run out the green time.”

A number of new partnerships between lessors, maintenance, repair and overhaul (MRO) providers and airlines are combining the sourcing of used material with repairs to increase options for airlines wanting to use it in their own engines.

One of the most significant recent deals is Lufthansa Technik’s intent to acquire a 15% stake in International Lease Finance’s (ILFC)

AeroTurbine, with a future option to increase that stake to 19.9%. Under the agreement, which is pending regulatory approval, Flor-ida-based AeroTurbine would supply Luf-thansa Technik with used serviceable aircraft and engine components for the MRO com-pany to repair for eventual sale.

STEADY SUPPLYOne of the benefits of the agreement is that it ensures an MRO firm has predictable access to parts, which can be difficult in the spot market nature of the business, says AeroTurbine senior vice-president Joshua Abelson.

With parts costs making up 70% of the cost of engine overhauls, MROs could be spending $600 million to $2 billion per year depending on the size of the operation and the types of component services they offer, he notes.

Rockwell Collins’ Intertrade has also recently moved into providing used servicea-ble material to the market by working with a network of repair stations to part out engines and re-certify used serviceable parts to be used as spares or replacement parts.

The company is focusing on tearing down engines and providing material for newer-generation engines, such as the CFM56-5B and -7B and International Aero Engines

V2500-A5. Other potential aircraft types include the Pratt & Whitney PW4000 and CF6-80 market, it says.

OEMs are looking to offer used serviceable material to their customers as well, and are increasingly formalising partnerships with lessors specialising in engine material.

Engine manufacturer Pratt & Whitney is sourcing used serviceable material in its repairs as its customers try to reduce costs. Pratt & Whitney provides used serviceable material at more than 30 locations, including its network of MRO facilities, on-site cus-tomer locations and warehouse sites. To pro-cure some of these parts, Pratt & Whitney has partnered with TES Aviation Group, a firm specialising in material sales, engine leasing and engine management.

TES, which works with several engine OEMs, is providing material for Pratt & Whit-ney’s PW4000-100 engines, which used to power recently retired Airbus A330 models. The engine manufacturer is using the material to repair engines at its Eagle Services Asia engine overhaul facility.

General Electric offers used serviceable material programmes for the CF6 and CF34 models and is expanding the offering to other engine types as they age.

Material for engines such as the CF6-80C2 has increased “dramatically” over the past two to three years due to teardowns. In the past this material was very limited, says Andy Morganthaler, marketing manager at GE Avia-tion Services. GE estimates the cost savings of used serviceable material to be between 15% and 20% per shop visit. It says it has seen fill rates of up to 80-90% of serviceable content in CFM56-3 engines per shop visit. By compari-son, serviceable material has made up to 60% of the CF-80C2 and less than 50% of the CF34-3 models.

While OEMs are making more of a push into the aftermarket by offering this material as part of their overhauls, third-party MROs are offering alternatives to combat rising costs of new spares, including Delta TechOps.

“For an airline, one of the biggest problems is the 8% OEM cost increase, at least, that you get every year,” said Delta Air Lines chief executive Richard Anderson at the MRO Americas show in Atlanta in April.

To mitigate these cost increases, Delta is using alternatives such as using parts manu-facturer approval (PMA) spares made by a non-OEM company and performing its own designated engineering repairs (DER) to restore material it finds in engines on the mar-ket, which it then parts out. ■

Parts costs make up some 70% of the overall cost of engine overhauls

“For an airline, a big problem is the annual 8%

OEM cost increase”RICHARD ANDERSON

Delta Air Lines chief executive

December 2013

GE

GE

flightglobal.com/ab36 | Airline Business |

The competitive landscape of the European short-haul market has changed drastically over the past few years as low-cost carriers have continued to expand, but airframe maintenance remains largely an in-house activity

MAINTENANCE EUROPE

MAINTAINING CONTROL

REPORTMICHAEL GUBISCH LONDON

An overview of Europe’s in- service Airbus A320s and Boe-ing 737s shows that much of the region’s narrowbody fleet is not available to third-party mainte-

nance, repair and overhaul providers, with the majority of large airlines conducting airframe MRO in-house.

The 20 largest narrowbody operators held around two-thirds of Europe’s approximately 3,230-strong 737 and A320 fleet at the end of the third quarter 2013, Flightglobal’s Ascend Online database shows. This group ranges from Ryanair with just over 300 737-800s at the top of the list to UK carrier Jet2, which has 38 legacy and current-generation 737s.

The figures illustrate how far Ryanair and EasyJet have left the former flag carriers behind in the wider European short-haul mar-ket. Ryanair is the largest European narrow-body operator by a wide margin, with 9.3% of the continent’s 737/A320 fleet. The Irish budget carrier has nearly 40% more aircraft than its nearest rival, EasyJet, and twice as many as Europe’s fourth-largest narrowbody operator, Turkish Airlines. Nevertheless, with its 217 A320s, EasyJet still has more aircraft than the combined single-aisle fleets of Air France and KLM.

However, despite the rise of the low-cost carriers, there does not seem to be much change in terms of third-party airframe main-tenance – at least at the top of the table. All but one of the six largest narrowbody opera-

tors conduct base maintenance in-house. Ryanair has three hangars – Prestwick in the UK, Hahn airport in Germany and Kaunas in Lithuania – where it carries out C-checks. Air France, British Airways, Lufthansa and Turk-ish Airlines look after their mainline and group aircraft through in-house technical departments.

OUTSOURCED OPERATIONSOnly EasyJet tenders its maintenance on the open market. Heavy maintenance has been contracted to SR Technics in a long-term agreement until 2020, while everything else, including C-checks, has been packaged under the airline’s equalised maintenance regime into similarly-sized overnight checks that are completed by a number of partners. These include SR Technics, Lufthansa Technik and Virgin Atlantic’s engineering base at London Gatwick, as well as EasyJet’s own hangar at its London Luton base.

Two-thirds of the aircraft used by Europe’s 20 largest narrowbody operators are main-tained by MRO providers that are either part

of the airlines or their parent groups. For example, Vueling’s A320s are serviced by Iberia Maintenance. The remainder are avail-able to third-party MRO specialists, but this segment also includes a number of long-term arrangements. Alitalia, for instance, has con-tracted its former, Naples-based technical division Atitech – which today is an inde-pendent company – to support the carrier’s A320 fleet until 2020.

More business potential for third-party MRO providers has been created among small and medium-sized airlines, which do not have sufficient economies of scale to make in-house technical operations cost-effective. Finnair is a prime example of this develop-ment, as the Nordic carrier has gradually shut down its airframe, component and engine overhaul departments over the past three years, with much of that work being out-sourced to SR Technics.

Meanwhile, low-cost carriers such as Norwegian, central European operator Wizz Air and Pegasus Airlines in Turkey grew their networks by concentrating on operations, while maintenance was contracted to third-party MRO providers.

The average age of Europe’s 737/A320 fleet is just over nine years. Low-cost operators that have rapidly expanded over the last two decades, and airlines in growth markets such as Russia and Turkey, have much younger fleets than their network carrier rivals. New aircraft not only require less MRO than older

Share of the European narrowbody fleet operated

by Ryanair

9.3%

December 2013

Regionals subject

flightglobal.com/ab10 | Airline Business | February 2012

Flightglobal InsightQuadrant House, The Quadrant, Sutton, Surrey, SM2 5AS, UKTel: +44 20 8652 8724 Email: [email protected] Web: www.flightglobal.com/insight