Embed Size (px)

Citation preview

Company Presentation:

The Selenge Iron Ore Project

Robert WrixonManaging Director

Mongolia Investment Summit

30 October 2012

2

COMPETENT PERSON’S STATEMENTS AND DISCLAIMERS

Competent Persons’ Statements

The information in this presentation that relates to Exploration Results and Exploration Targets is based on information compiledand reviewed by Mr Kerry Griffin, who is a Member of the Australian Institute of Geoscientists. Mr Griffin has sufficientexperience which is relevant to the style of mineralisation and type of deposit under consideration and to the activity which he isundertaking to qualify as a Competent Person as defined in the 2004 Edition of the ‘Australasian Code for Reporting ofExploration Results, Mineral Resources and Ore Reserves’. Mr Griffin is the Technical Director of Haranga Resources Limitedand consents to the inclusion in this report of the matters based on his information, and information presented to him, in the formand context in which it appears.

The technical information contained in this announcement in relation to the JORC Compliant Resource for the BayantsogtDeposit has been reviewed by Mr Peter Ball of DataGeo Ltd, who is a member of the Australasian Institute of Mining andMetallurgy. Mr Ball has sufficient experience relevant to the style of mineralisation and type of deposit under consideration andto the activity which he is undertaking to qualify as a Competent Person as defined in the 2004 Edition of the ‘Australasian Codefor Reporting of Mineral Resources and Ore Reserves’. Mr Ball consents to the inclusion in this report of the matters based onhis information, and information presented to him, in the form and context in which it appears.

Exploration Targets

Exploration Targets are conceptual in nature and should not be construed as indicating the existence of a JORC Code compliantmineral resource. There is insufficient information to establish whether further exploration will result in the determination of amineral resource within the meaning of the JORC Code.

Forward Looking Statements

This presentation includes certain ‘forward looking statements’. All statements, other than statements of historical fact, areforward looking statements that involve various risks and uncertainties. There can be no assurances that such statements willprove accurate, and actual results and future events could differ materially from those anticipated in such statements.

Such information contained herein represents management’s best judgment as of the date hereof based on information currentlyavailable. The company does not assume the obligation to update any forward-looking statement.

3

OVERVIEW

Flagship Selenge Iron Ore Project – Four Primary Targets→ Initial JORC Resource at only one target (Bayantsogt: 33Mt)

→ 250-400Mt total Exploration Target at Selenge

→ Close to rail and road infrastructure, easy access to market

→ Next to Mongolia’s largest iron ore export mine (Eruu Gol: 5Mt production in 2012)

→ Aim is to drill out 75% of target area in 2012 – Drilling is ongoing

→ Excellent metallurgical properties yield a premium magnetite concentrate

→ MOU for 5Mtpa of rail capacity signed with Mongolian Government and Railway Authority

Supportive Major Investor: Lippo Group→ Lippo Group increased holding from 7.4% to 13.9% via $6m placement in March 2012

→ Subsequently increased their interest on market to 15.3%

Mongolian iron ore exports growing rapidly due to healthy margins and the market outlook for inland China remains strong

4

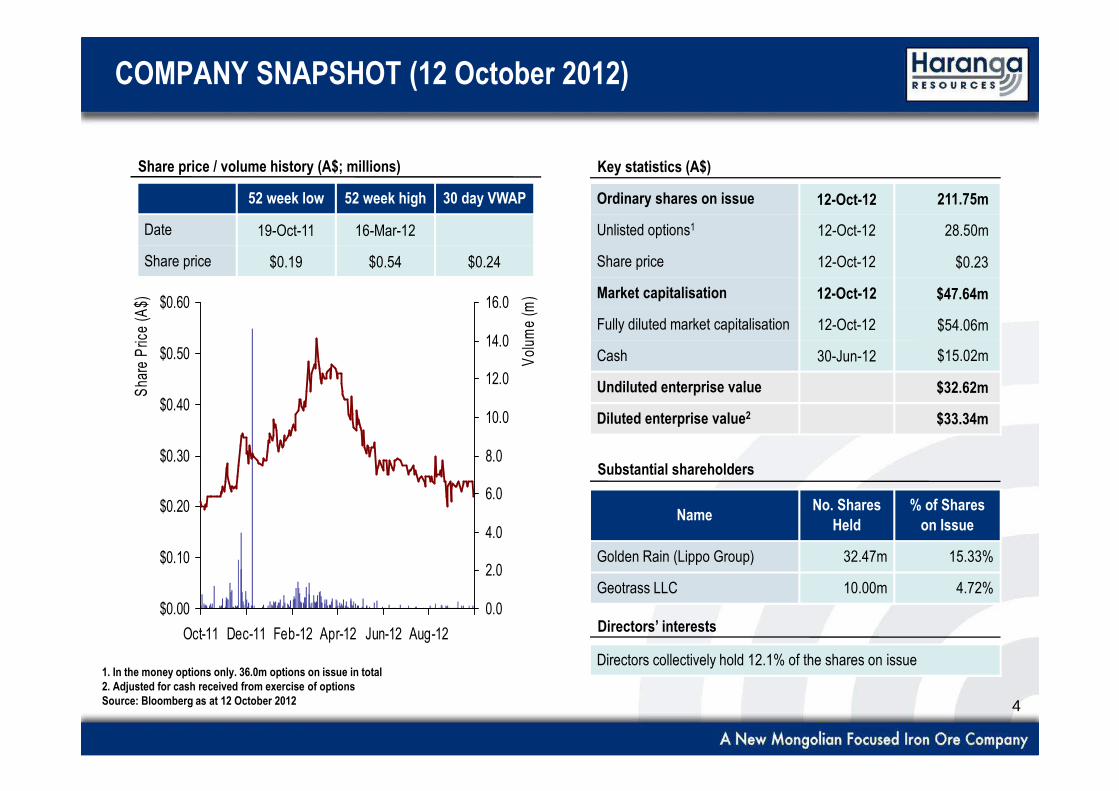

COMPANY SNAPSHOT (12 October 2012)

Key statistics (A$)Share price / volume history (A$; millions)

Substantial shareholders

NameNo. Shares

Held

% of Shares

on Issue

Golden Rain (Lippo Group) 32.47m 15.33%

Geotrass LLC 10.00m 4.72%

$0.00

$0.10

$0.20

$0.30

$0.40

$0.50

$0.60

Oct-11 Dec-11 Feb-12 Apr-12 Jun-12 Aug-12

Sha

re P

rice

(A$)

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

Vol

ume

(m)

Directors’ interests

Ordinary shares on issue 12-Oct-12 211.75m

Unlisted options1 12-Oct-12 28.50m

Share price 12-Oct-12 $0.23

Market capitalisation 12-Oct-12 $47.64m

Fully diluted market capitalisation 12-Oct-12 $54.06m

Cash 30-Jun-12 $15.02m

Undiluted enterprise value $32.62m

Diluted enterprise value2 $33.34m

Directors collectively hold 12.1% of the shares on issue

52 week low 52 week high 30 day VWAP

Date 19-Oct-11 16-Mar-12

Share price $0.19 $0.54 $0.24

1. In the money options only. 36.0m options on issue in total2. Adjusted for cash received from exercise of optionsSource: Bloomberg as at 12 October 2012

5

AN ASX LISTED MONGOLIAN COMPANY

Operating in Mongolia for almost three years

Listed on the ASX in December 2010→ IPO heavily marketed in Mongolia through CPS International and MICC

→ Over 200 Mongolian shareholders (almost 20% of investor base)

All key projects are joint ventures with Mongolian partners

Two Mongolian board members

23 of 25 employees are Mongolian nationals, all based in Mongolia

Over $20m invested in Mongolia to date

Currently running Mongolia’s largest drill program→ 35,000m of diamond drilling in 2012

6

CSR AND ENVIRONMENTAL STEWARDSHIP

Selenge is Mongolia’s largest drill program→ A social licence to operate is a must

HAR, VOR and Hunnu Coal jointly run one of Mongolia’s largest private student scholarship program

→ 15 students currently in the program, 6 are HAR students

→ 4 of the students are from the local community near Selenge

→ All students get summer work experience with HAR

New water bore to be donated to the local community

Haranga sponsored this year’s local summer festival

30,000 spruce, pine and birdcherry trees planted and protected in 10 different areas in the local soum

Exploration camp quality and drilling rehab as per western/Australian standard

7Source: CRU Strategies; Noble Group

Iron ore consumption/production forecast in China’s northern provinces(Million Tonnes at 20% Fe grade equivalent)

In 2012 China will mine 1Bt of raw iron ore at an average grade of 18% Fe

Providing only 1/3 of requirement – China is fundamentally short iron ore

8Source: CRU Strategies

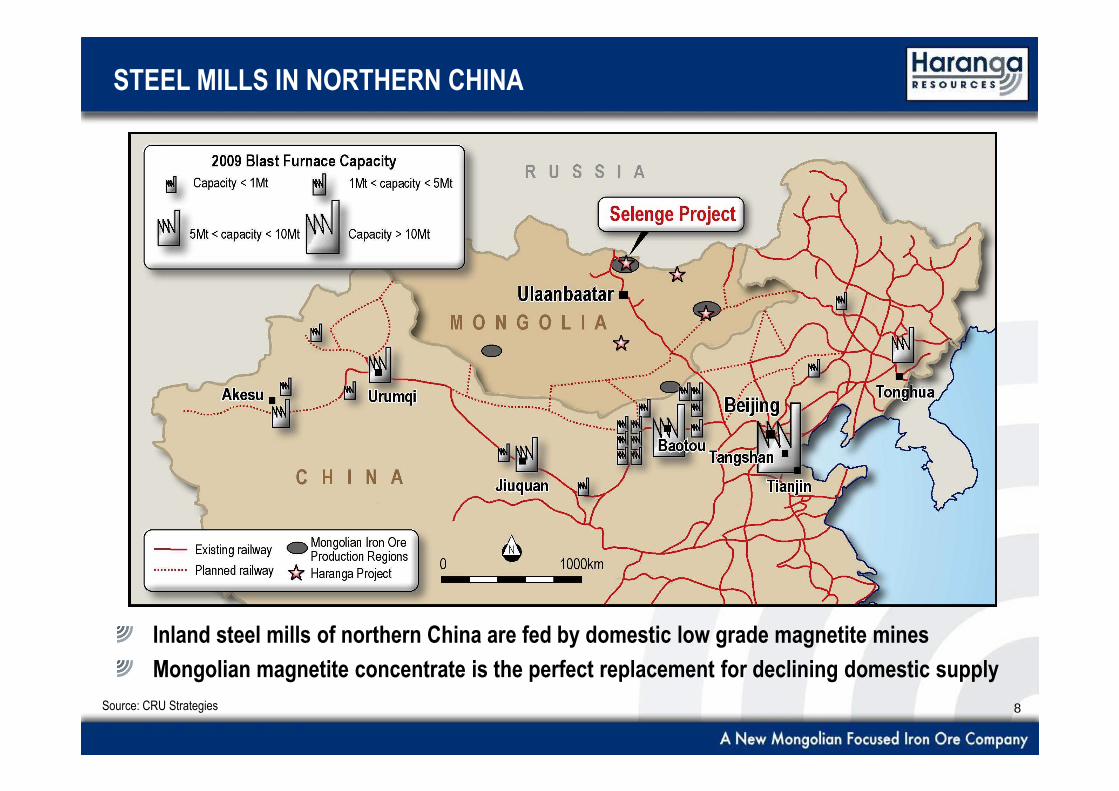

STEEL MILLS IN NORTHERN CHINA

Inland steel mills of northern China are fed by domestic low grade magnetite mines

Mongolian magnetite concentrate is the perfect replacement for declining domestic supply

9

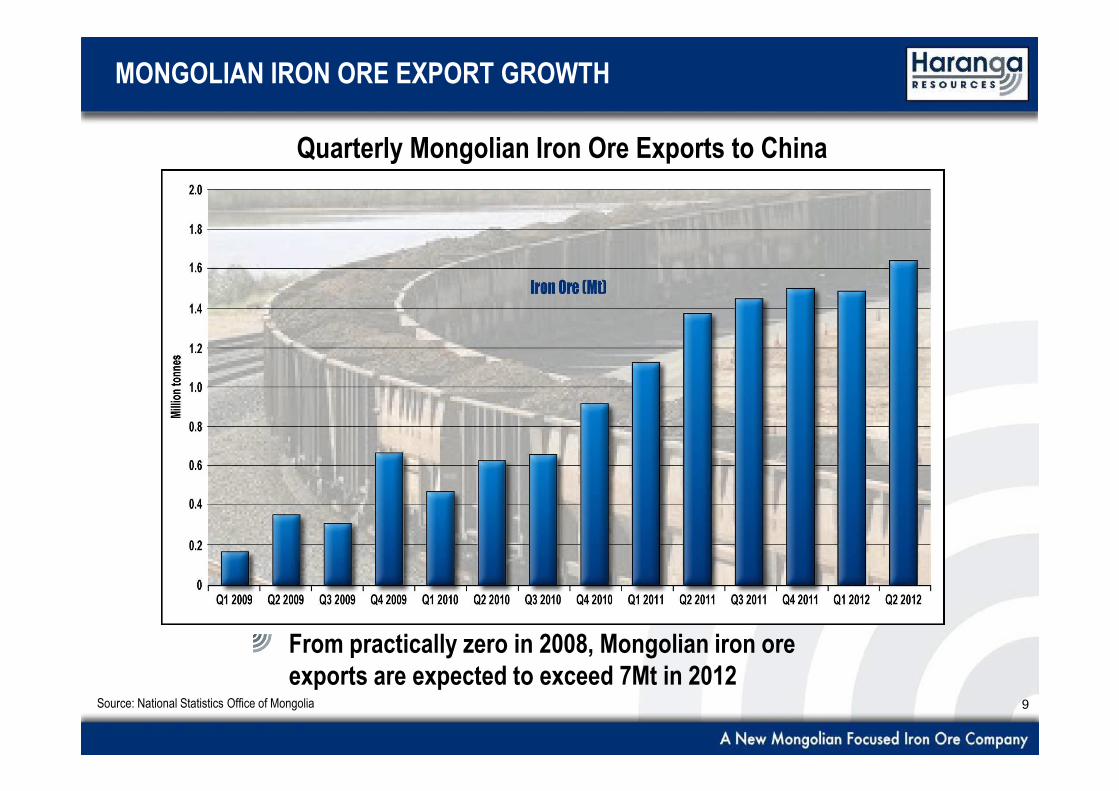

MONGOLIAN IRON ORE EXPORT GROWTH

Source: National Statistics Office of Mongolia

Quarterly Mongolian Iron Ore Exports to China

From practically zero in 2008, Mongolian iron ore exports are expected to exceed 7Mt in 2012

10

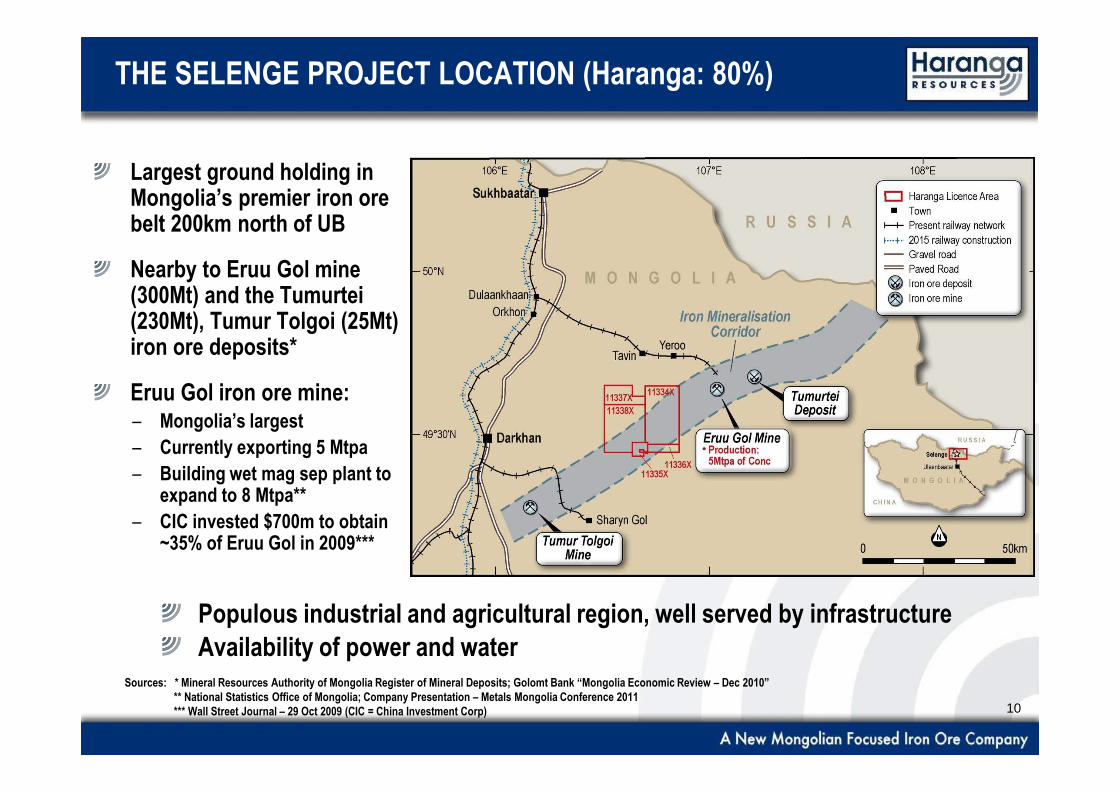

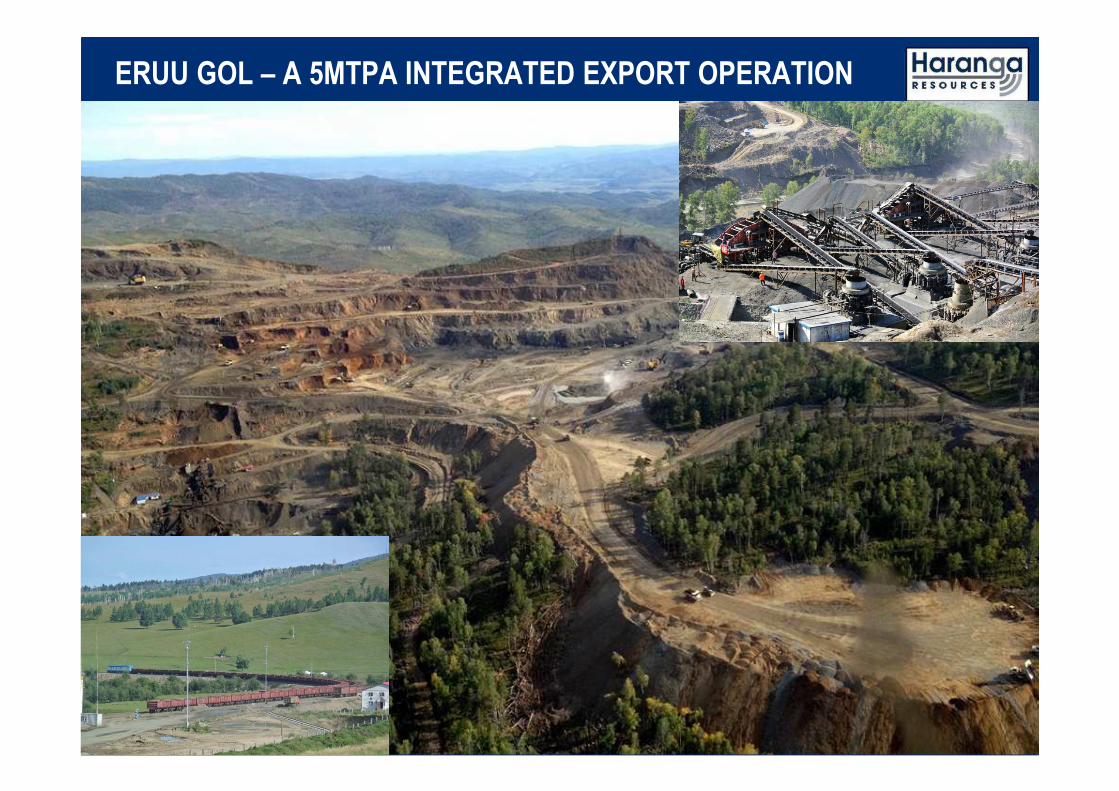

THE SELENGE PROJECT LOCATION (Haranga: 80%)

Largest ground holding in Mongolia’s premier iron ore belt 200km north of UB

Nearby to Eruu Gol mine (300Mt) and the Tumurtei(230Mt), Tumur Tolgoi (25Mt) iron ore deposits*

Eruu Gol iron ore mine:– Mongolia’s largest

– Currently exporting 5 Mtpa

– Building wet mag sep plant to expand to 8 Mtpa**

– CIC invested $700m to obtain ~35% of Eruu Gol in 2009***

Populous industrial and agricultural region, well served by infrastructure

Availability of power and waterSources: * Mineral Resources Authority of Mongolia Register of Mineral Deposits; Golomt Bank “Mongolia Economic Review – Dec 2010”

** National Statistics Office of Mongolia; Company Presentation – Metals Mongolia Conference 2011*** Wall Street Journal – 29 Oct 2009 (CIC = China Investment Corp)

11

ERUU GOL – A 5MTPA INTEGRATED EXPORT OPERATION

12

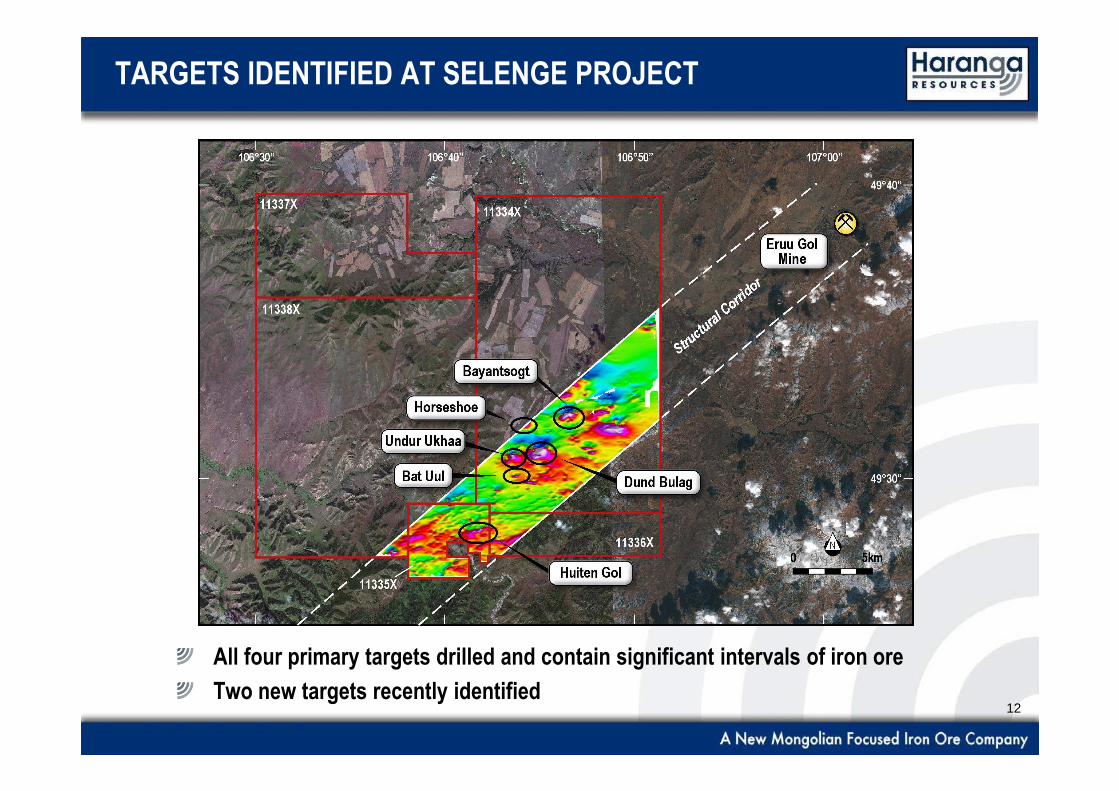

TARGETS IDENTIFIED AT SELENGE PROJECT

All four primary targets drilled and contain significant intervals of iron ore

Two new targets recently identified

13

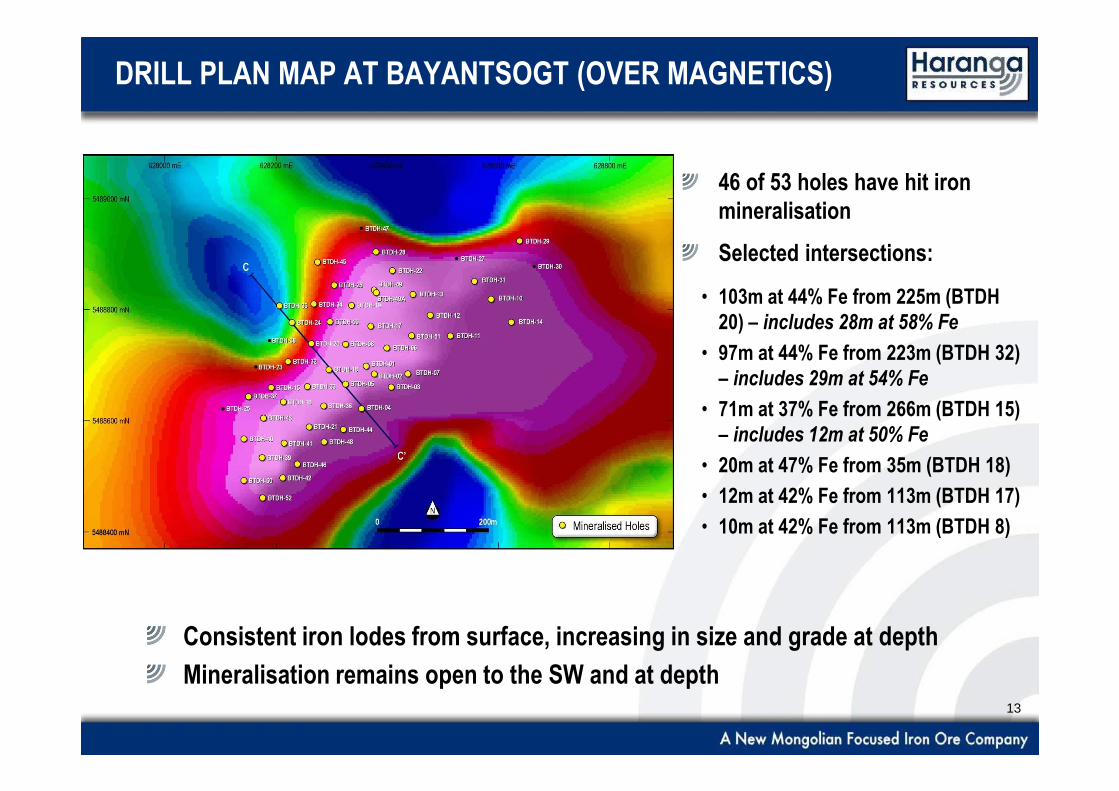

DRILL PLAN MAP AT BAYANTSOGT (OVER MAGNETICS)

46 of 53 holes have hit iron mineralisation

Selected intersections:

• 103m at 44% Fe from 225m (BTDH 20) – includes 28m at 58% Fe

• 97m at 44% Fe from 223m (BTDH 32) – includes 29m at 54% Fe

• 71m at 37% Fe from 266m (BTDH 15) – includes 12m at 50% Fe

• 20m at 47% Fe from 35m (BTDH 18)

• 12m at 42% Fe from 113m (BTDH 17)

• 10m at 42% Fe from 113m (BTDH 8)

Consistent iron lodes from surface, increasing in size and grade at depth

Mineralisation remains open to the SW and at depth

14

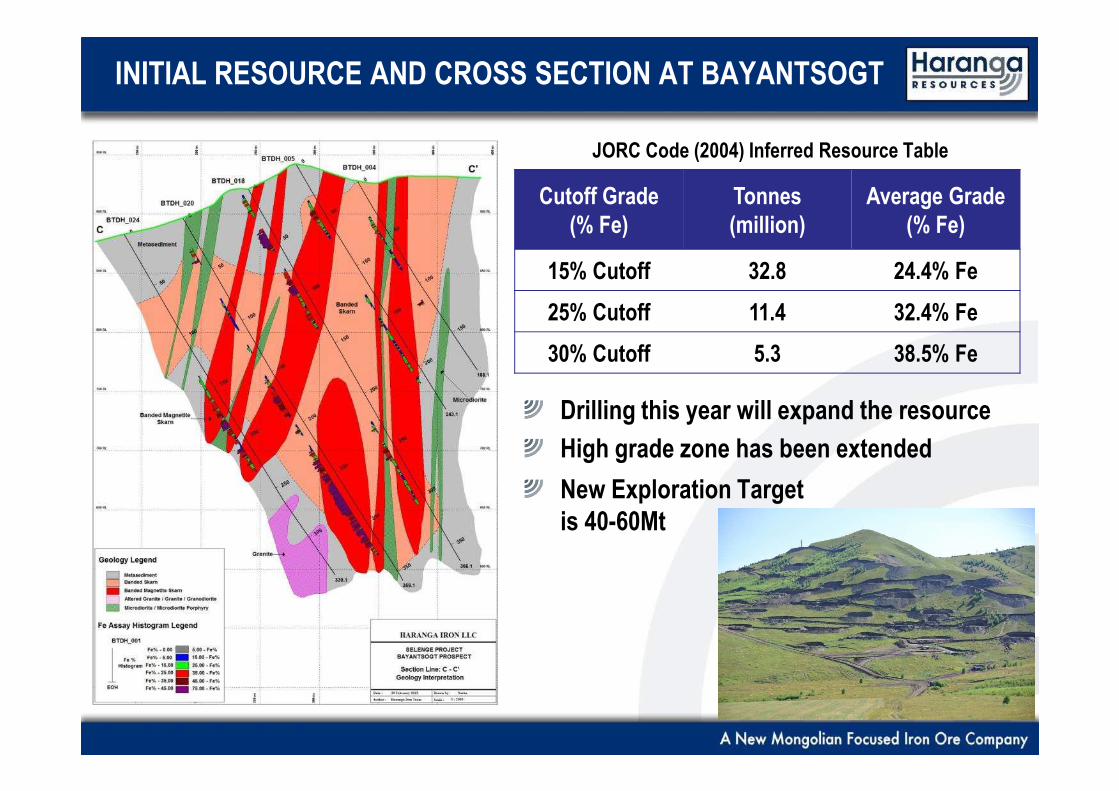

INITIAL RESOURCE AND CROSS SECTION AT BAYANTSOGT

Cutoff Grade(% Fe)

Tonnes(million)

Average Grade(% Fe)

15% Cutoff 32.8 24.4% Fe

25% Cutoff 11.4 32.4% Fe

30% Cutoff 5.3 38.5% Fe

Drilling this year will expand the resource

High grade zone has been extended

JORC Code (2004) Inferred Resource Table

New Exploration Target is 40-60Mt

15

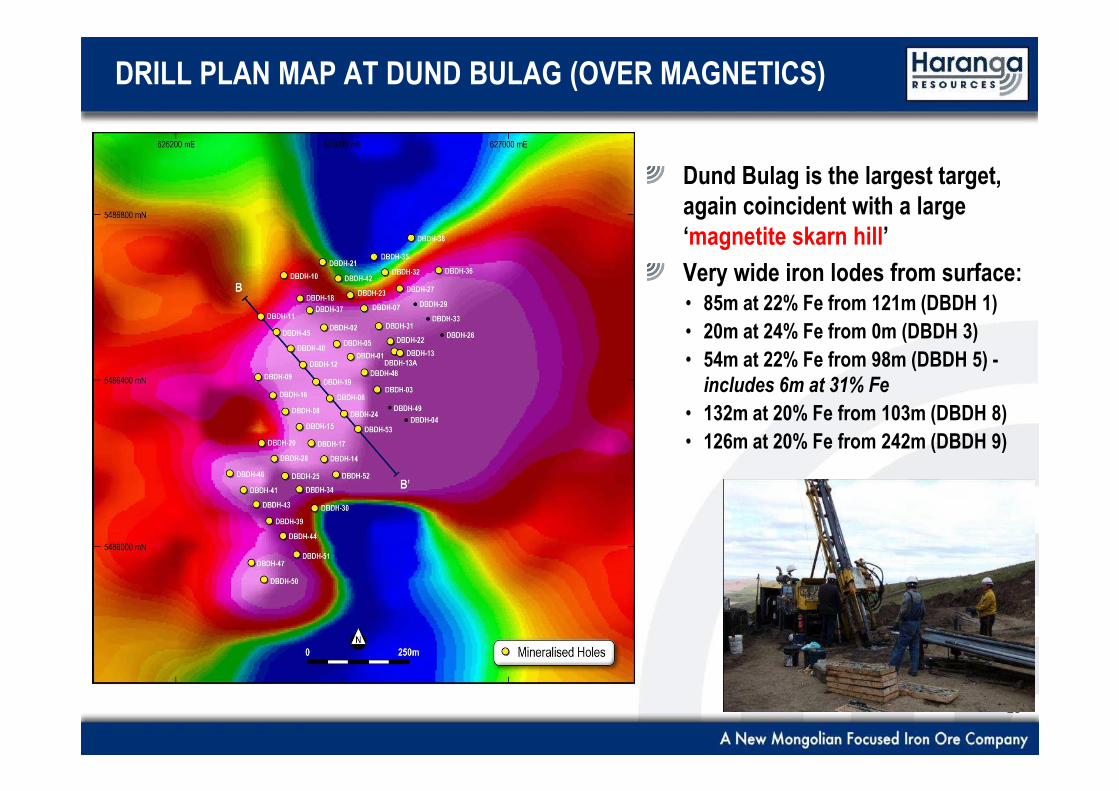

DRILL PLAN MAP AT DUND BULAG (OVER MAGNETICS)

Dund Bulag is the largest target, again coincident with a large ‘magnetite skarn hill’

Very wide iron lodes from surface:• 85m at 22% Fe from 121m (DBDH 1)

• 20m at 24% Fe from 0m (DBDH 3)

• 54m at 22% Fe from 98m (DBDH 5) -includes 6m at 31% Fe

• 132m at 20% Fe from 103m (DBDH 8)

• 126m at 20% Fe from 242m (DBDH 9)

16

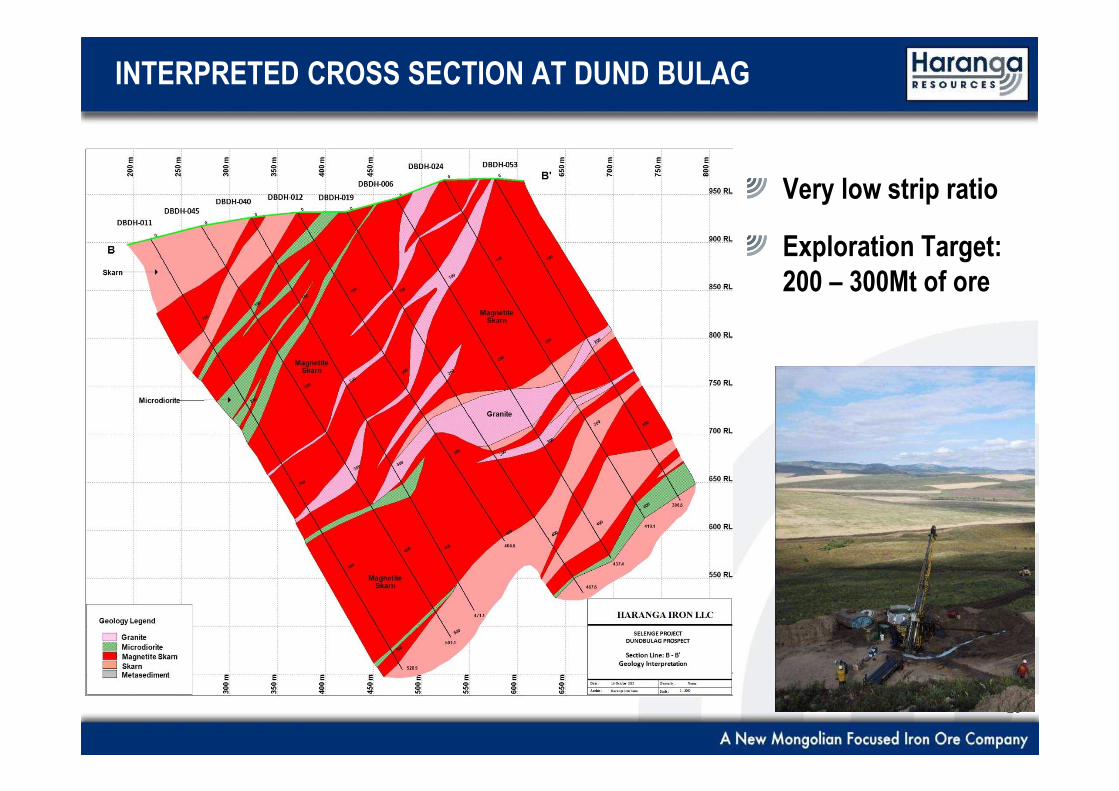

INTERPRETED CROSS SECTION AT DUND BULAG

Very low strip ratio

Exploration Target: 200 – 300Mt of ore

17

EXCELLENT METALLURGICAL PROPERTIES

Banded Magnetite Skarn mineralisation at Selenge:

Coarse grained with SiO2 primarily in separate bands

Far more easily beneficiated than typical Australian massive magnetites

Even the lower grade ore produces a 65-66% Fe concentrate at 75µm grind

High Fe and low impurities should allow premium pricing

Deposit/

Prospect

Average Raw

Fe Grade

AverageMass Yield

Fe

(%)SiO2

(%)Al2O3

(%)S

(%)P

(%)Bayantsogt 30.1% 29.1% 65.77 3.25 0.96 1.03 0.02

Dund Bulag 18.5% 18.0% 65.15 5.34 1.32 0.18 0.00

Huiten Gol 27.7% 29.8% 68.78 1.90 0.41 0.01 0.01

Summary of All DTR Testsfrom Every Metre of 2011 Mineralised Core

Average Concentrate Quality (75µm Grind, 10% Yield Cutoff)

18

INLAND CHINESE IRON ORE PRICES REMAIN STRONG

US$102/t

US$130/t

Source: AME Group Monthly Iron Ore Outlook October 2012

Monthly Average Spot Prices for Seaborne Imports vs Inland Domestic Iron Ore

19Source: CRU Strategies, Macquarie Bank, ProMet Engineers’ Techno-Economic Assessment on the Selenge Iron Ore Project

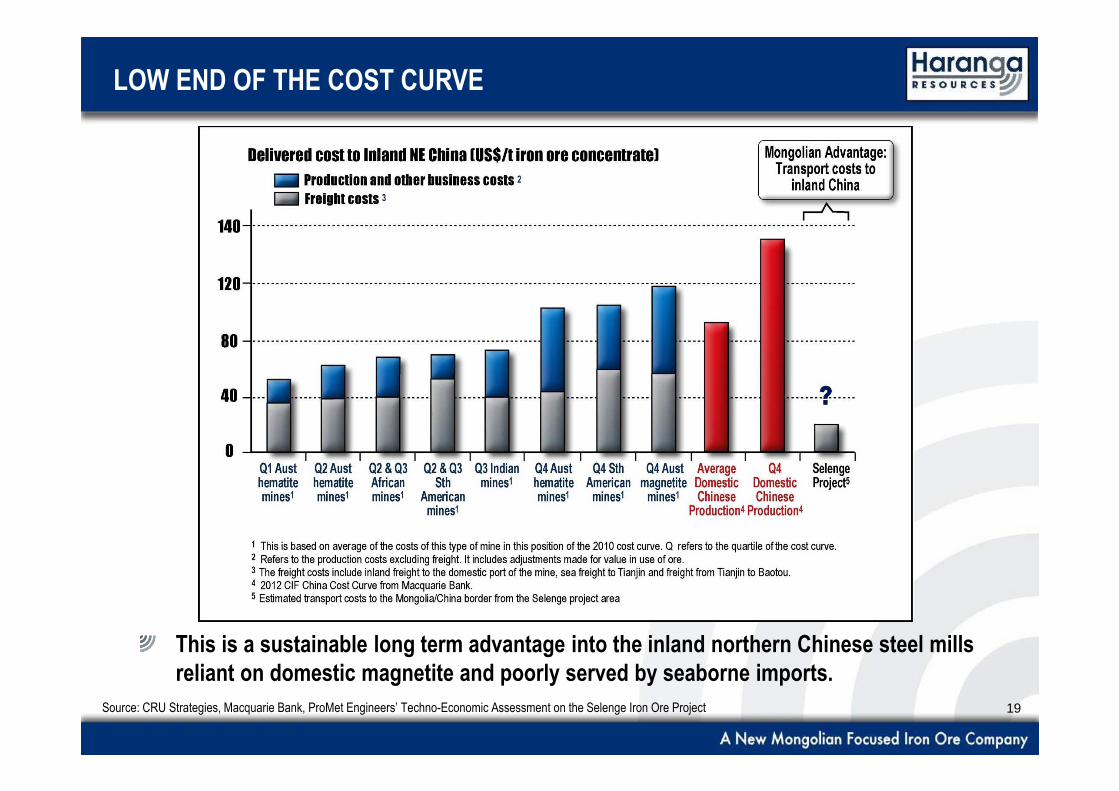

LOW END OF THE COST CURVE

This is a sustainable long term advantage into the inland northern Chinese steel mills reliant on domestic magnetite and poorly served by seaborne imports.

20

SUMMARY AND SELENGE PROJECT PLAN

China mines ~1Bt per year of iron ore, 18% Fe average→ Primarily magnetite mines - forecast decline in grade and tonnes

→ Growing demand and high prices for magnetite concentrate in inland northern China

Bayantsogt and Dund Bulag are well advanced→ High grade Huiten Gol and new discovery at Undur Ukhaa give further upside

→ Total Exploration target of 250 – 400Mt for the four drilled targets only

→ Excellent Met Results: 65-66% Fe concentrate achieved for all

Highly positive preliminary Scoping Study

Six month newsflow for Selenge Project→ 34,000m drill program ongoing, substantial resource uplift expected by April 2013

→ Mining Licence application underway – final submission before end 2012

→ More Met Testing: Coarser grind sizes and dry magnetic separation

→ Full feasibility study to commence in 2013

![Oslobođenje [broj 23664, 30.10.2012]](https://img.dokumen.tips/doc/110x75/577ce4f91a28abf1038f87b9/oslobodenje-broj-23664-30102012.jpg)