Embed Size (px)

Citation preview

Insight. Oversight. Foresight. SMMichigan Texas Florida

2014 Tax Update

Carrie Koshkin, JDChris Haas, CPAClifton Teague, CPARichard Beutelschies, CPA

Our Tax Experts

Chris Haas, CPA• Shareholder in the Tax Group with more than 10 years’ experience• Areas of expertise: domestic tax, employee benefit plans, FAS 109 disclosures and FIN 48

disclosures

Clifton Teague, CPA• Shareholder in the Tax Group with more than 25 years’ experience• Areas of expertise: domestic and international tax

Richard Beutelschies, CPA• Shareholder in the Tax Group with more than 35 years’ experience• Areas of expertise: domestic tax, business valuation and tax incentives

Carrie Koshkin, JD • Shareholder in the International Tax Group with nearly 15 years’ experience• Areas of expertise: international tax compliance and planning

Insight. Oversight. Foresight. SM

Federal TaxChris Haas

Federal Tax

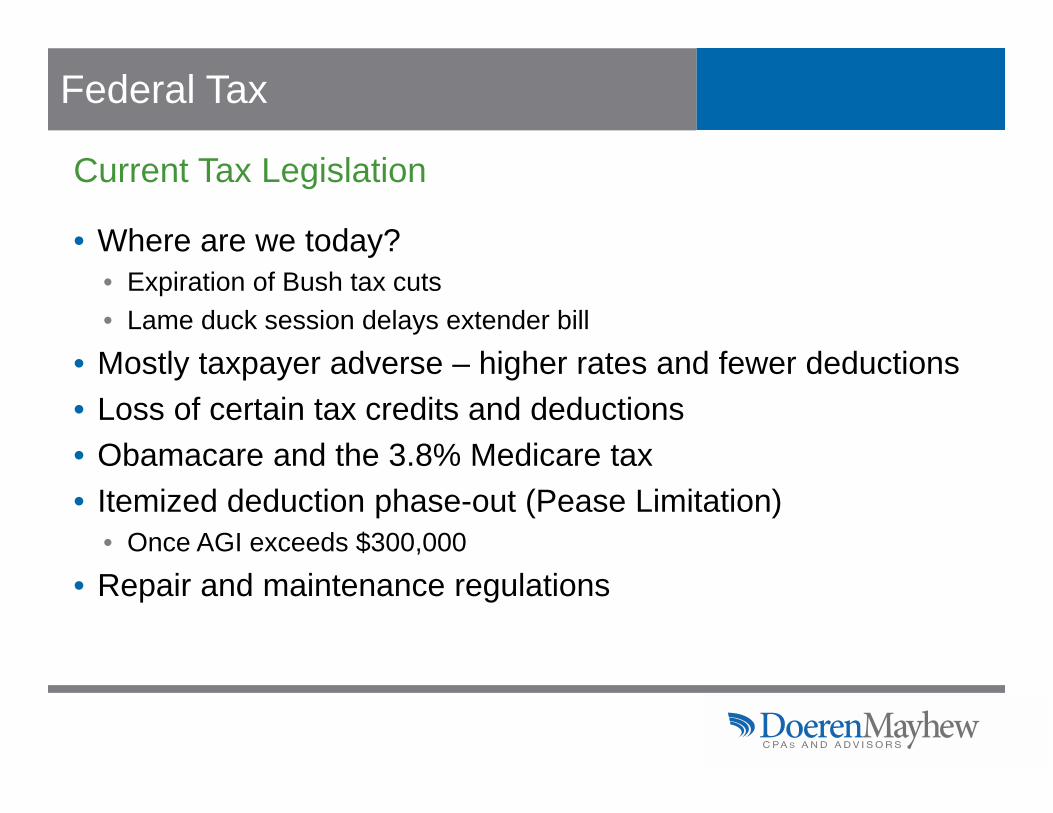

• Where are we today?• Expiration of Bush tax cuts • Lame duck session delays extender bill

• Mostly taxpayer adverse – higher rates and fewer deductions• Loss of certain tax credits and deductions • Obamacare and the 3.8% Medicare tax• Itemized deduction phase-out (Pease Limitation)

• Once AGI exceeds $300,000

• Repair and maintenance regulations

Current Tax Legislation

Federal Tax

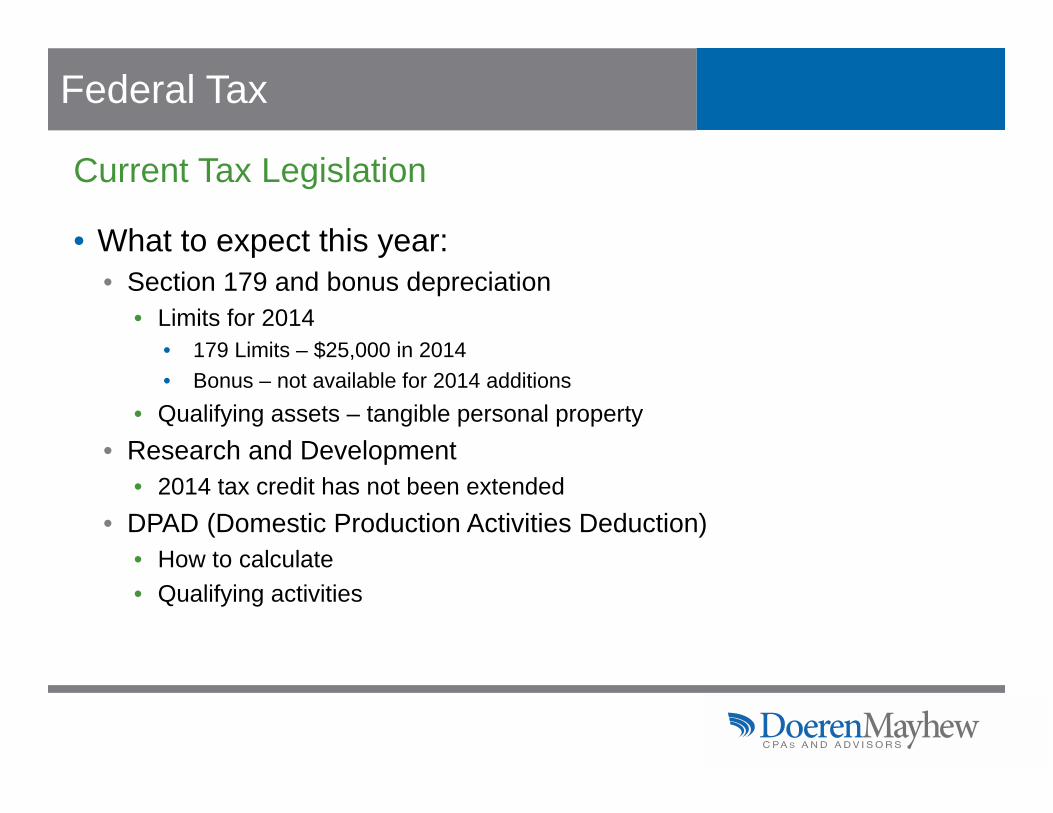

• What to expect this year:• Section 179 and bonus depreciation

• Limits for 2014• 179 Limits – $25,000 in 2014• Bonus – not available for 2014 additions

• Qualifying assets – tangible personal property• Research and Development

• 2014 tax credit has not been extended• DPAD (Domestic Production Activities Deduction)

• How to calculate• Qualifying activities

Current Tax Legislation

Federal Tax

• Medicare Tax of 3.8%• High earners – additional .9% on wages over $200,000 for single

taxpayers, $250,000 for married filing joint• Investment income subject to tax – capital gains, dividends, interest• Passive activity income is typically subject to additional tax• Active income from trade or business is exempt• Real estate professionals exempt

Current Tax Legislation

Federal Tax

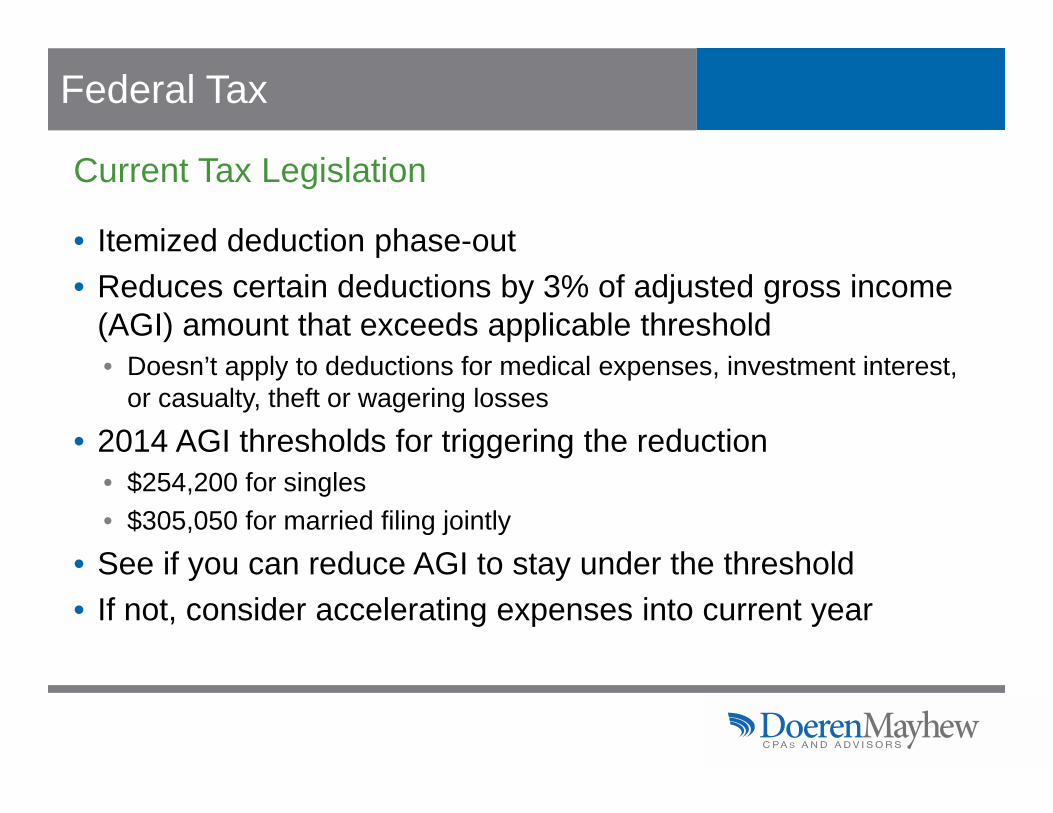

• Itemized deduction phase-out• Reduces certain deductions by 3% of adjusted gross income

(AGI) amount that exceeds applicable threshold• Doesn’t apply to deductions for medical expenses, investment interest,

or casualty, theft or wagering losses

• 2014 AGI thresholds for triggering the reduction• $254,200 for singles• $305,050 for married filing jointly

• See if you can reduce AGI to stay under the threshold• If not, consider accelerating expenses into current year

Current Tax Legislation

Federal Tax

• Itemized deduction example:• Taxpayer with AGI of $2 million has a 10-year commitment to donate

$100,000 annually to a qualified charitable organization. In this scenario, the taxpayer would lose $51,000 ($2 million – $300,000 * 3%) in charitable donations each year for 10 years. That’s $510,000 in lost deductions!

• How do we minimize the impact?• Accelerate future contributions into current year to avoid losing deductions in

future years• Reduce current-year tax liability

Current Tax Legislation

Federal Tax

• IRS repair and maintenance regulations:• Costs incurred to acquire, produce or improve tangible property

must be depreciated• Costs incurred on incidental repairs and maintenance can be

expensed and immediately deducted

• Key provisions of the final regulations make distinguishing between repairs and improvements simpler• Routine maintenance safe harbor• Small business safe harbor• Materials and supplies

• Make sure you’re taking all of the repair and maintenance deductions you’re entitled to

Current Tax Legislation

Federal Tax

• Projecting income• Defer income to next year

• If using cash method of accounting, defer billing for products or services• If using accrual method, delay shipping products or delivering services

• Accelerate deductible expenses into current year• If cash-basis taxpayer, pay down accounts payable prior to 12/31• Charge expenses on a credit card and deduct them in the year charged

• Take the opposite approach• May save you more tax if it’s likely you’ll be in a higher bracket next year

Tax Planning

Federal Tax

• Section 179 expensing election• Allows you to deduct rather than depreciate asset purchases• New or used assets qualify, such as:

• Equipment• Furniture• Off-the-shelf computer software

• The 2014 expensing limit is $25,000• Break begins to phase out dollar-for-dollar when total asset

acquisitions for the tax year exceed $200,000• Can’t reduce net income below zero to create a net operating loss

• 50% bonus depreciation• Expired 12/31/13, with a few exceptions• Congress may revive it

Tax Planning

Federal Tax

• Restricted stock• Income recognition normally deferred until stock is no longer

subject to risk of forfeiture or you sell it• You then pay tax on stock’s FMV at your ordinary-income rate

• Make Sec. 83(b) election to recognize ordinary income when you receive stock, which may be beneficial if:• The income would be negligible or• The stock is likely to appreciate significantly before income would

otherwise be recognized• Election allows you to:

• Convert future appreciation from ordinary income to long-term capital gains income

• Defer it until stock is sold

Tax Planning

Federal Tax

• Section 83(b) example: • Taxpayer A sold his business to a publicly traded company on 11/30/11

in exchange for cash and $1 million of stock that was scheduled to vest in equal thirds over the next 3 years. Instead of waiting to recognize the income as each third vested, taxpayer made an 83(b) election within 30 days and recognized $1M of ordinary income in 2011 at a price per share of $32. The stock A received has appreciated considerably and now trades for $64 per share. If A had waited to recognize the income as the shares vested he would have paid tax on a substantially greater amount of ordinary income.

Tax Planning

Federal Tax

• Disadvantages of Sec. 83(b) election• You must prepay tax in the current year, which could also trigger or

increase exposure to: • The 39.6% ordinary-income tax rate • The additional 0.9% Medicare tax

• Prepaid taxes can’t be refunded if you eventually forfeit the stock or sell it at a decreased value

• When you sell the shares, any gain will be included in net investment income and could trigger or increase your liability for the 3.8% net investment income tax (NIIT)

Tax Planning

Federal Tax

Tax Planning

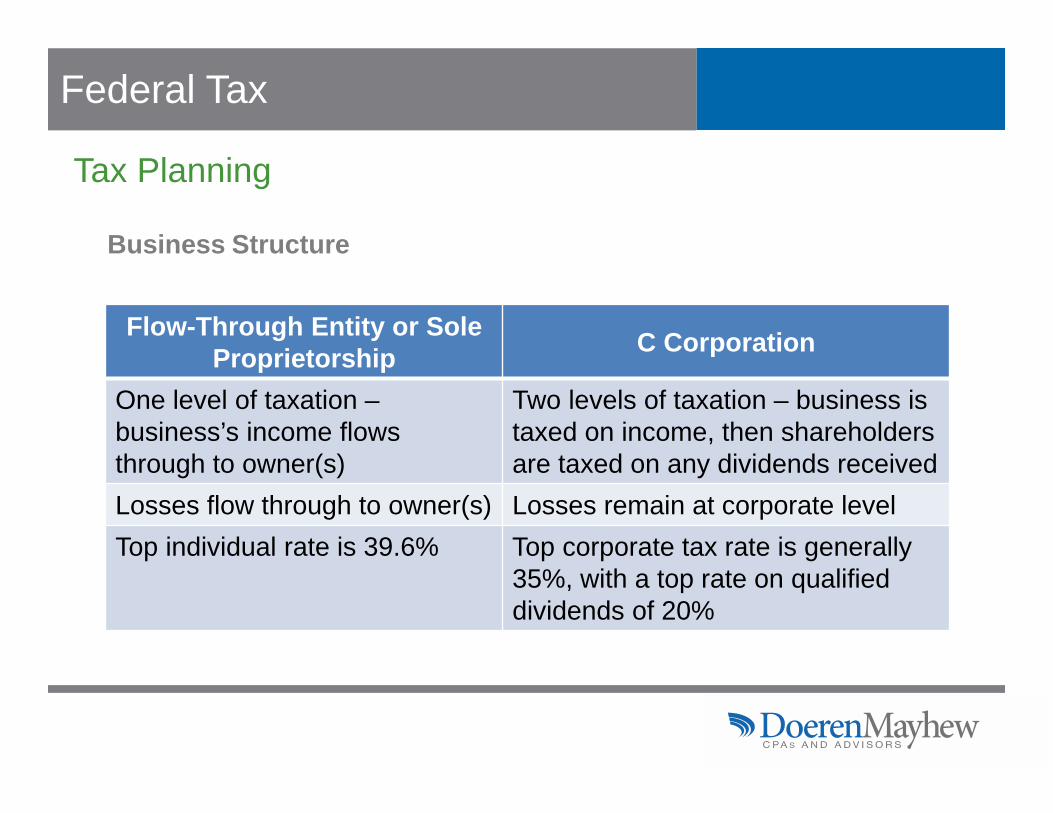

Business Structure

Flow-Through Entity or Sole Proprietorship C Corporation

One level of taxation –business’s income flows through to owner(s)

Two levels of taxation – business is taxed on income, then shareholders are taxed on any dividends received

Losses flow through to owner(s) Losses remain at corporate levelTop individual rate is 39.6% Top corporate tax rate is generally

35%, with a top rate on qualified dividends of 20%

Federal Tax

• Sale or acquisition• Tax consequences can have a major impact on the transaction’s

success – or failure• Asset vs. stock sale

• Sellers typically prefer a stock sale• Buyers typically prefer an asset sale

• Tax-deferred transfer vs. taxable sale • Generally better to postpone tax• Some advantages to a taxable sale

Tax Planning

Federal Tax

• Installment sales• Often used when buyer

• Lacks sufficient cash • Pays a contingent amount based on the business’s performance

• Also used when seller wants to spread gain over a number of years• Could help avoid triggering the 3.8% net investment income tax• Could also help avoid 20% long-term capital gains rate

• Can backfire on the seller• Must report depreciation recapture in year of sale• If tax rates increase, overall tax could be more

Tax Planning

Federal Tax

• Home-related deductions• Property tax deduction

• Pay tax when it’s most beneficial• Isn’t deductible for alternative minimum tax (AMT) purposes

• Mortgage interest deduction• Up to combined total of $1 million of mortgage debt• Deduct points paid related to principal residence

• Home equity debt interest deduction• Debt limit of $100,000 on debt used for any purpose• Consider using home equity debt to pay off credit cards or auto loans

Real Estate

Federal Tax

• Home rental rules• If you rent out principal residence or second home for fewer than

15 days:• Don’t need to report the income• Can’t deduct expenses directly associated with the rental

• If you rent out principal residence or second home for 15 days or more:• Must report the income • May be able to deduct rental expenses• Whether home is classified as rental

property for tax purposes affects deduction

Real Estate

Federal Tax

• Home sales• When selling principal residence, you can exclude up to $250,000

($500,000 for joint filers) of gain• To support tax basis, keep thorough records• You must meet certain tests, and gain that’s allocable to a period of

“nonqualified” use generally isn’t excludable • Gain qualifying for exclusion will also be excluded from

the 3.8% net investment income tax (NIIT)• Losses on principal residence generally aren’t deductible • Second homes are ineligible for gain exclusion

• Consider converting to rental use before selling• It can then be considered a business asset

Real Estate

Federal Tax

• Tax deferral strategies• Installment sale

• Defer gains by spreading over several years as you receive the proceeds

• Ordinary gain is recognized in year of sale, even if no cash is received

• Section 1031 exchange • Exchange one real estate investment for another• Defer paying tax on gain until you sell replacement property

Real Estate

Federal Tax

• Estate tax• Rate is 40%

• Scheduled to remain at that level• Exemption increased to $5.34 million for 2014

• Will continue to be adjusted for inflation annually• Review your estate plan in light of the changing exemption

• Avoid unintended tax consequences• Make the most of available exemption• Ensure assets will be distributed according to your wishes

Tax-Smart Gifting

Federal Tax

• Gift tax follows estate tax exemption and rate• Any gift tax exemption used during life reduces

estate tax exemption available at death• Exclude certain gifts of up to $14,000 per recipient

each year• $28,000 per recipient if your spouse splits gift with you or you’re giving

community property

Tax-Smart Gifting

Federal Tax

• What is GST (Generation Skipping Tax)?• Generally applies to transfers made to people two generations or

more below you• Is in addition to any gift or estate tax due• Follows the estate tax exemption and rate• GST tax exemption can be a valuable tax-saving tool

• Grandparents can use it to make transfers to grandchildren and avoidany tax at their children’s generation

Tax-Smart Gifting

Federal Tax

• Plan gifts carefully• Pay tuition and medical expenses

• Payments won’t be treated as a taxable gift if you make them directly to the provider

• Make gifts to charity• Donations to qualified charities aren’t subject to gift taxes and may

provide an income tax deduction• Gift ownership interest in closely held business or family

limited partnership

Tax-Smart Gifting

Federal Tax

• Leverage your annual exclusions and lifetime exemption, because interests may be eligible for valuation discounts• For example: If discounts total 30%, you can gift an ownership interest

equal to as much as $20,000 tax-free because the discounted value doesn’t exceed the $14,000 annual exclusion

• The IRS may challenge the value, so a professional, independent valuation is strongly recommended

• With a family limited partnership (FLP), you fund the FLP and then gift limited partnership interests, which may be eligible for a discount

Tax-Smart Gifting

Insight. Oversight. Foresight. SM27

International TaxCarrie Koshkin

International Tax

• Advisors in multiple jurisdictions must work together• Leverage global resources – Moore Stephens network• Every jurisdiction is unique – No “one-size-fits-all” answer

• Not always best to follow what you’ve done in other jurisdictions• Not always best to follow what other companies are doing

Remember

International Tax

• Aligning Global Structure With Business Strategy• Export Incentive: IC-DISC• Transfer Pricing• Foreign Tax Credits• Upcoming Regulations and Proposals

Topics of Discussion

International Tax

• Entity Classification Elections• Aside from certain types of entities that must be taxed in the U.S. as

corporations, Entity Classification Elections allow entities to choose their tax classification, i.e., partnership, corporation, disregarded entity.

Aligning Structure With Strategy

International Tax

• Deferral vs. Flow-through Structures • One factor in deciding which to use is determining where the group

needs cash.• If the group is likely to reinvest the earnings of the foreign operations

back into the foreign operations, a corporate structure can help defer U.S. tax until the cash is repatriated to the U.S. (absent certain types of income that fall under the U.S. anti-deferral rules)

• If the parent company needs the cash back in the U.S., it may choose to set up a flow-through structure with partnerships and DREs. This requires earnings of the foreign entity to roll into the U.S. parent and be taxed currently.

Aligning Structure With Strategy

International Tax

• IC-DISC (Interest Charge Domestic International Sales Corporation) is paid a commission by the related party.

• IC-DISC is not taxed on the commission income.• The related party receives a deduction for this commission

payment.• The IC-DISC is deemed to make dividend distributions to its

shareholders, which are taxed at the dividend rate.

Export Incentives – IC-DISC

International Tax

Export Incentives – IC-DISC

Owner

Operating Company IC-DISC

Qualified Dividend Tax Rate of 20%

Income Tax Rate of 39.6%

International Tax

• Qualifications:• Qualified Export Property Test – At least 95% of the total assets must be

qualified export assets at the end of the tax year. • These are assets used in the furtherance of generating qualified export receipts.

• Qualified Export Receipts Test – At least 95% of the foreign trade gross receipts for the tax year must be “qualified export receipts.” • Qualified export receipts include receipts from sales, leases, subleases or rental of

“export property.” • Export property is:

• Non-depletable property manufactured, produced or grown in the U.S. by a person other than an IC-DISC.

• Sold, leased or rented for direct consumption or disposition outside of the U.S., or to an unrelated person for delivery outside the U.S. within one year.

• Not more than 50% of the fair market value of such property is attributable to articles imported into the U.S.

Export Incentives – IC-DISC

International Tax

• Section 482 of the Internal Revenue Code authorizes the IRS to distribute, apportion or allocate gross income, deductions, credits and/or allowances between or among businesses that are owned or controlled directly or indirectly by the same interests.

• Section 482 is intended to prevent related parties from shifting income to low-tax jurisdictions by requiring arm’s length pricing be used when engaging in transactions between commonly controlled entities.

Transfer Pricing

International Tax

• Requirements• The “best method” rule• Comparability analysis• The arm’s length range• Contemporaneous documentation

• Penalties• The 20% penalty• The increased 40% penalty

Transfer Pricing

International Tax

• U.S. provides a credit for foreign taxes• Only applies to foreign income taxes.• Limited to taxes actually paid OR U.S. tax on foreign-sourced income.

• If foreign tax is higher than the U.S. tax on this income, then it will not be 100% credited.

• Sourcing rules may differ by jurisdiction.• Best to optimize your tax position locally rather than relying on the

Foreign Tax Credit completely.

Foreign Tax Credit

International Tax

• Section 367(a) gain recognition final regulations.• Section 956 regulations on loans by CFC to foreign

partnerships.• Section 905(c) final regulations on FTC determination. • Section 871(m) guidance on equity swap payments.• Section 987 foreign currency rules.• Section 367(d) rules on transfers of intangibles offshore.

Upcoming Regulations

International Tax

• Would change the tax rate to 25%.• Includes a sort of territorial system of international corporate

tax, but with a minimum 15% tax on certain “intangible income” earned through CFCs.

• Would authorize a 95% DRD on the foreign-source portion of dividends received by a domestic corporation from a specified 10%-owned foreign corporation, in some cases.• Losses on the sale of a specified 10%-owned foreign sub would be

reduced by the amount of any 95% DRD previously claimed.

Camp International Tax Reform Proposal

International Tax

• Section 902 would be repealed – This means no FTC would be allowed for taxes imposed on dividends eligible for the 95% DRD.

• Section 904 would be modified to allocate only directly allocable deductions to foreign-source income.

• Subpart F income would include a new category for “foreign base company intangible income.”

• Existing foreign corporation earnings of certain 10%-owned foreign subs as of the close of the entity’s last taxable year would be subject to a forced repatriation tax.

Camp International Tax Reform Proposal

Insight. Oversight. Foresight. SM

State TaxClifton Teague

State Tax

• Automotive repair shops

• Heavy construction equipment rental businesses

• Companies renting and leasing certain tangible property under SIC 7359 (most notably, industrial trucks, oilfield equipment, oil-well drilling equipment, tools and office equipment)

• Change adopted in 2013

Unexpected Taxpayers Allowed to Use the .5% Reduced Retail Rate

State Tax

• Taxpayers are allowed to switch to or from the COGS method on amended tax returns.

Switching Computational Methods

Fed COGS vs Texas Franchise COGS

• 2013 legislation allows taxpayers to deduct direct and indirect labor costs (as well as associated costs) that the taxpayer may or may not have capitalized as inventory costs. A similar rule also applies to long-term construction contracts.

State Tax

• Companies increasing their inventory bases may want to consider deducting purchases instead of COGS. This is an annual election.

Purchases Instead of COGS

Other COGS Often Identified as Other Expenses on TR

• Indirect costs up to 4% of revenue.

• Quality control, inspection and warranty costs.

• Research and development costs as identified in IRC Section 174.

State Tax

Other COGS continued

• Licensing, franchise and royalty costs for trademarks and other intellectual property relating to the finished product or manufacturing process.

• Costs of renting or leasing equipment and facilities.

• Repair and maintenance costs for equipment and facilities.

• Insurance on equipment, facilities and finished goods.

• Property taxes on equipment, facilities and finished goods.

• Utilities consumed to produce and store finished goods.

State Tax

• Outgoing freight and shipping is excluded. Net receipts with costs.

• Interest.

• Officer costs.

• Income taxes.

• Strike Costs and idle facilities.

Items to be Excluded

State Tax

Franchise Tax Report Year

For Accounting Years Ending In 179 Dollar Limit Property Acquisition

Threshold

2008 2007 $112,000 $450,000

2009 2008 $115,000 $460,000

2010 2009 $120,000 $480,000

2011 and beyond 2010 and beyond $25,000 $200,000

Bonus Depreciation and Section 179

• No bonus is allowed • Section 179 limits:

State Tax

• Oilfield services that constitute construction, improvement, remodeling, repair or industrial maintenance of oil and gas wells can be included in COGS for allowable costs.

• This exception for the use of COGS by a service provider is consistent with Section 171.1012(i): “ A taxable entity furnishing labor or materials to a project for the construction, improvement, remodeling, repair, or industrial maintenance of real property is considered to be the owner of that labor or materials and may include the costs, as allowed by this section, in the computation of costs of goods sold.”

Oilfield Services

State Tax

• The Newpark decision has greatly expanded the type of companies that would qualify for the oilfield services exception as well as other companies providing services related to other types of real property.

• Prior to Newpark, only companies that physically touched or made a change to the property could qualify for this exception. The 3rd Court of Appeals concluded that the company’s activities must be essential and direct to the construction, repair … of the property.

Other Services Related to Real Property

State Tax

• Labor to install tangible personal property outside of the manufacturing process, unless part of "construction, improvement, remodeling, repair or industrial maintenance of real property," is not allowed as part of the COGS deduction.

Installation of Personal Property

Oil and Gas Wells

• The assets associated with wells are generally real property, but segregation occurs in certain production and gathering assets.

State Tax

• Contractors can exclude payments to subcontractors on work related to the construction, improvement and maintenance of real property if:

• The contractor has a contract with either the customer or subcontractor.• The subcontractor is paid only after the contractor is paid.

• The requirement that the subcontractor be physically engaged in the design, construction, remodeling or repair of real property has been dropped after the decision in the Newparkappeal. The Titan case, which is currently in appeal challenges the Comptroller’s position regarding the first two requirements.

Treatment of Subcontractors

Thank You!

For more information, please contact:Clark Whitley Business Development ManagerPhone: [email protected]

Join us in January for more tax insight:Doeren Mayhew 2015 Conference• Jan. 22, 2015, 1:30 – 4:30 p.m.• 3 hours of CPE• dmconference2015.eventbrite.com