Embed Size (px)

Citation preview

This report is solely for the use of Zinnov Client and Zinnov Personnel. No Part of it may be quoted, circulated or reproduced for distribution outside the client organization without prior written approval from Zinnov.

Global Service Providers Ratings -2015Engineering R&D ServicesNovember, 2015

Global Engineering R&D Landscape

Key Trends in Global Engineering & RD Services

GSPR – 2015 Rating

$614 Billion G500 R&D spend in

2015

Global Engineering R&D Landscape

Key Trends in Global Engineering & RD Services

GSPR – 2015 Rating

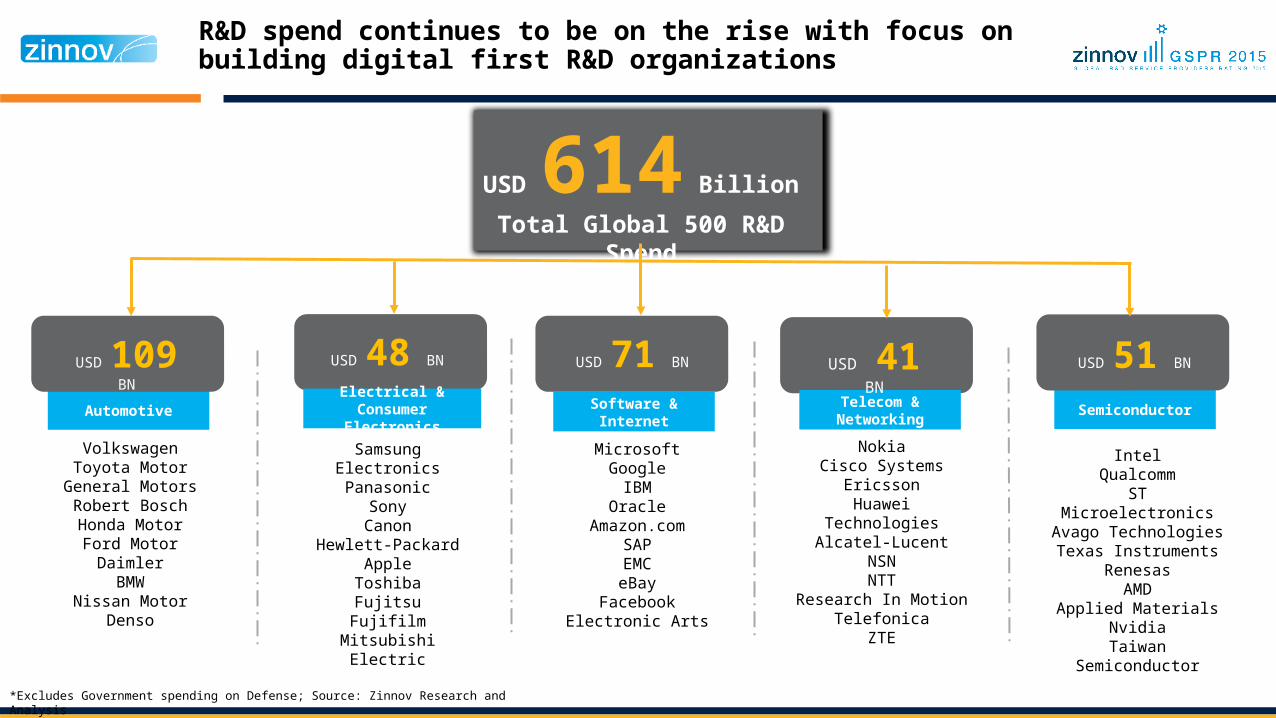

NokiaCisco Systems

EricssonHuawei Technologies

Alcatel-LucentNSNNTT

Research In MotionTelefonica

ZTE

R&D spend continues to be on the rise with focus on building digital first R&D organizations

Semiconductor

IntelQualcomm

ST MicroelectronicsAvago TechnologiesTexas Instruments

RenesasAMD

Applied MaterialsNvidiaTaiwan

Semiconductor

*Excludes Government spending on Defense; Source: Zinnov Research and Analysis

USD 51 BN

Telecom & Networking

USD 41 BN

Software & InternetMicrosoftGoogle

IBMOracle

Amazon.comSAPEMCeBay

FacebookElectronic Arts

USD 71 BN

Samsung ElectronicsPanasonic

SonyCanon

Hewlett-PackardApple

ToshibaFujitsuFujifilm

Mitsubishi Electric

Automotive

VolkswagenToyota Motor

General MotorsRobert BoschHonda MotorFord Motor

DaimlerBMW

Nissan MotorDenso

USD 48 BNUSD 109 BN

USD 614 BillionTotal Global 500 R&D

Spend

Electrical &Consumer Electronics

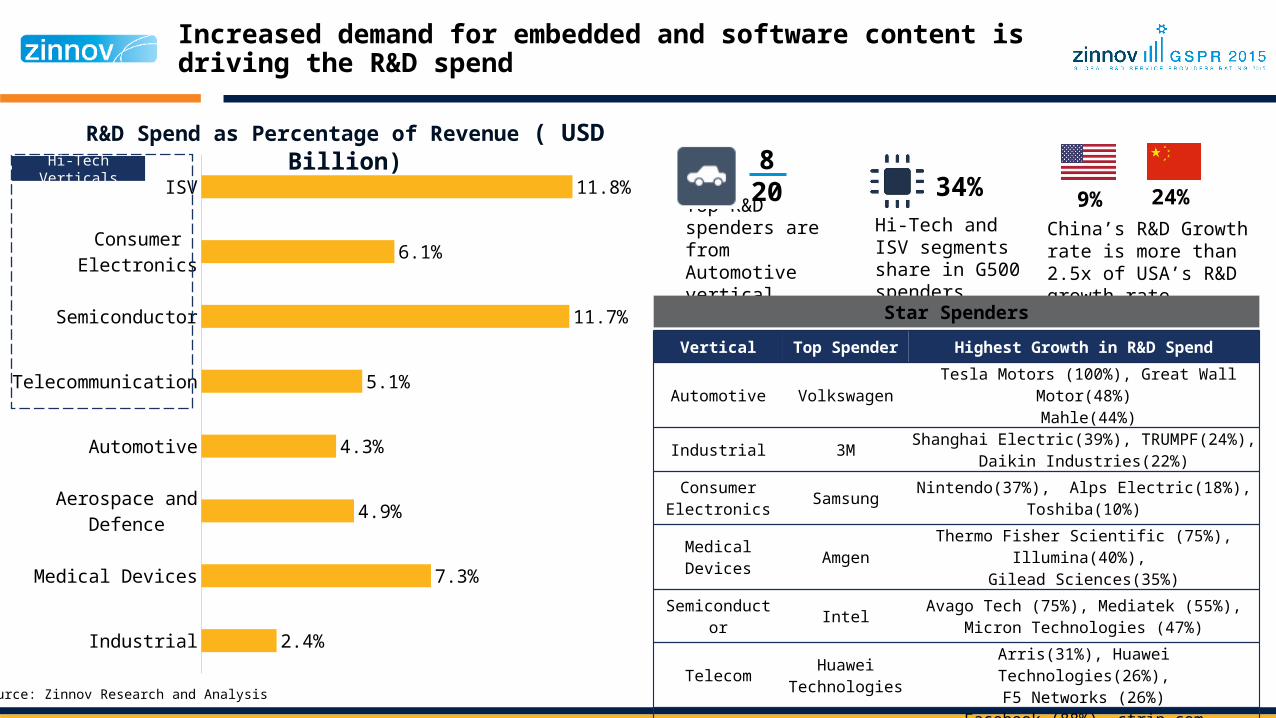

Vertical Top Spender Highest Growth in R&D Spend

Automotive Volkswagen Tesla Motors (100%), Great Wall

Motor(48%) Mahle(44%)

Industrial 3M Shanghai Electric(39%), TRUMPF(24%), Daikin Industries(22%)

Consumer Electronics Samsung Nintendo(37%), Alps Electric(18%),

Toshiba(10%)

Medical Devices Amgen

Thermo Fisher Scientific (75%), Illumina(40%),

Gilead Sciences(35%)Semiconduct

or Intel Avago Tech (75%), Mediatek (55%), Micron Technologies (47%)

Telecom Huawei Technologies

Arris(31%), Huawei Technologies(26%),F5 Networks (26%)

ISV MicrosoftFacebook (88%), ctrip.com

international(82%),Baidu(66%)

Source: Zinnov Research and Analysis

Industrial

Medical Devices

Aerospace and Defence

Automotive

Telecommunication

Semiconductor

Consumer Electronics

ISV

2.4%

7.3%

4.9%

4.3%

5.1%

11.7%

6.1%

11.8%

R&D Spend as Percentage of Revenue ( USD Billion)

Top R&D spenders are from Automotive vertical

820

Hi-Tech and ISV segments share in G500 spenders

34% China’s R&D Growth

rate is more than 2.5x of USA’s R&D growth rate

24% 9%

Star Spenders

Hi-Tech Verticals

Increased demand for embedded and software content is driving the R&D spend

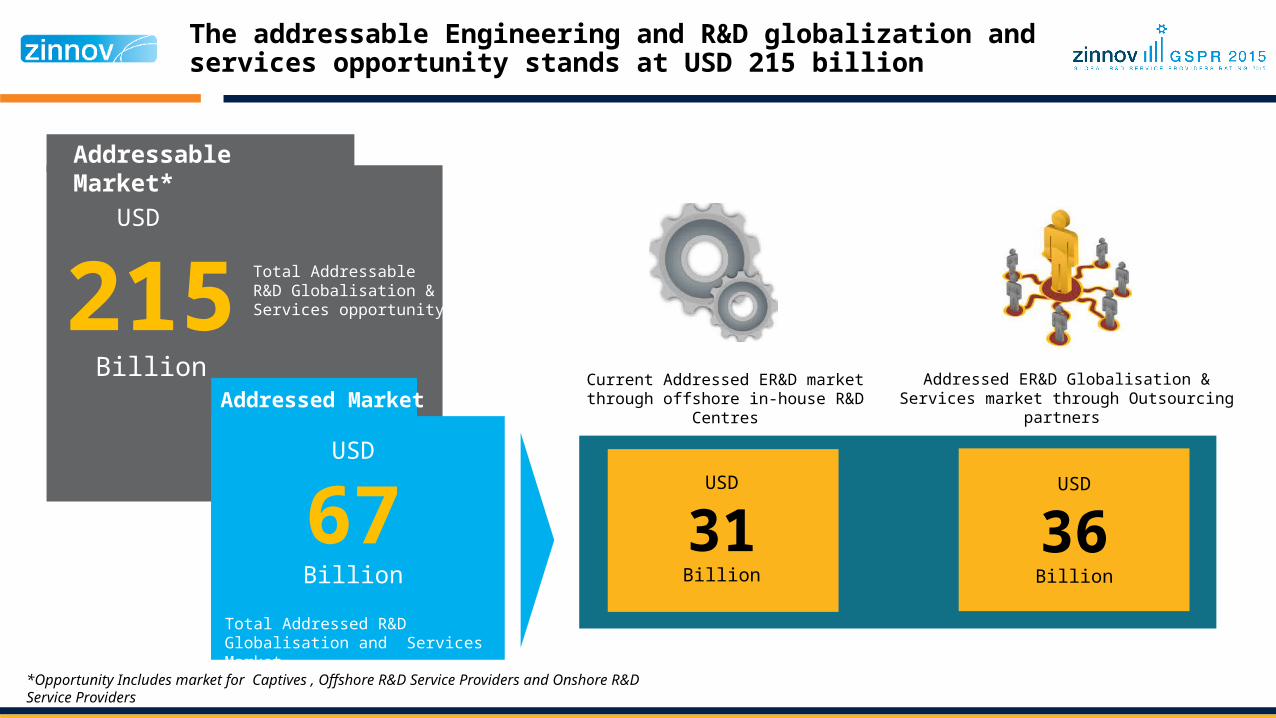

The addressable Engineering and R&D globalization and services opportunity stands at USD 215 billion

Current Addressed ER&D market through offshore in-house R&D Centres

Addressed ER&D Globalisation & Services market through Outsourcing partners

*Opportunity Includes market for Captives , Offshore R&D Service Providers and Onshore R&D Service Providers

USD

215 Billion

Addressable Market*

Total Addressable R&D Globalisation & Services opportunity

USD

67Billion

Total Addressed R&D Globalisation and Services Market

USD

31Billion

USD

36Billion

Addressed Market

*Opportunity Includes market for Captives , Offshore R&D Service Providers and Onshore R&D Service Providers

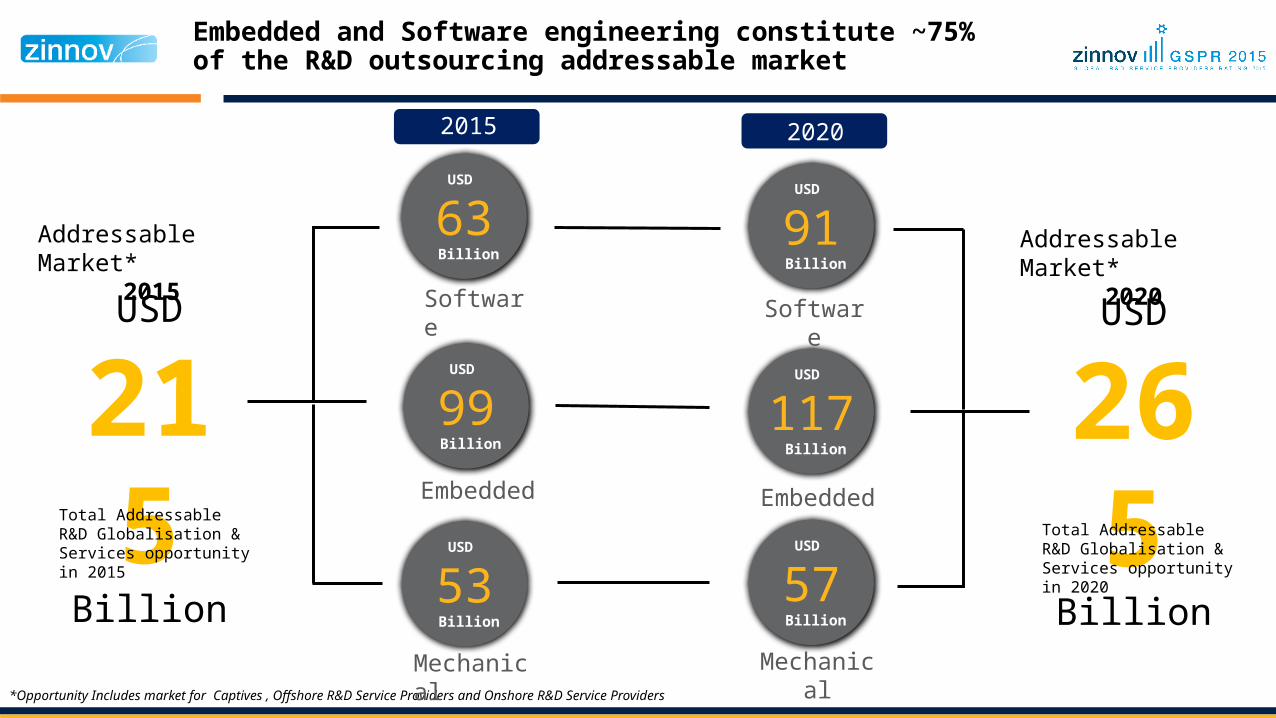

USD

63 Billion

SoftwareUSD

215

Billion

Total Addressable R&D Globalisation & Services opportunity in 2015

USD

53 Billion

USD

99 Billion

Embedded

Mechanical

USD

91 Billion

USD

117 Billion

USD

57 Billion

20202015

USD

265

Billion

Total Addressable R&D Globalisation & Services opportunity in 2020

Addressable Market*

2015

Addressable Market*

2020Software

Embedded

Mechanical

Embedded and Software engineering constitute ~75% of the R&D outsourcing addressable market

R&D Globalization as a phenomenon is here to stay with locations in emerging economies being the hotspot

12.25 BnIndia

9.7 BnChina

2.3 BnSouth Africa

3.1 BnBrazil

0.9 BnEastern Europe

G500 globalisation intensity

Billion

USD

Overall R&D Globalisation in

Emerging Economies

7.6%Growth Rate over 2014

India continues to be the most preferred destinations for setting up of newer captives as well as development of existing ones

Aerospace and Defence2%

Automotive9%

Computer Periph-erals9%

Consumer Electron-ics7%

Energy1%

Industrial3%

Medical Devices4%

Semiconductors12%Software & Internet

35%

Telecom and Networking

14%

Others4%

Vertical level split of India CaptivesAround 40% of the overall R&D globalisation is based out of India

Of all new offshore technology centres were set up in India

The growth for the existing captives in India is greater than overall growth

USD12.3 Bn

8.3%

Growth

69%

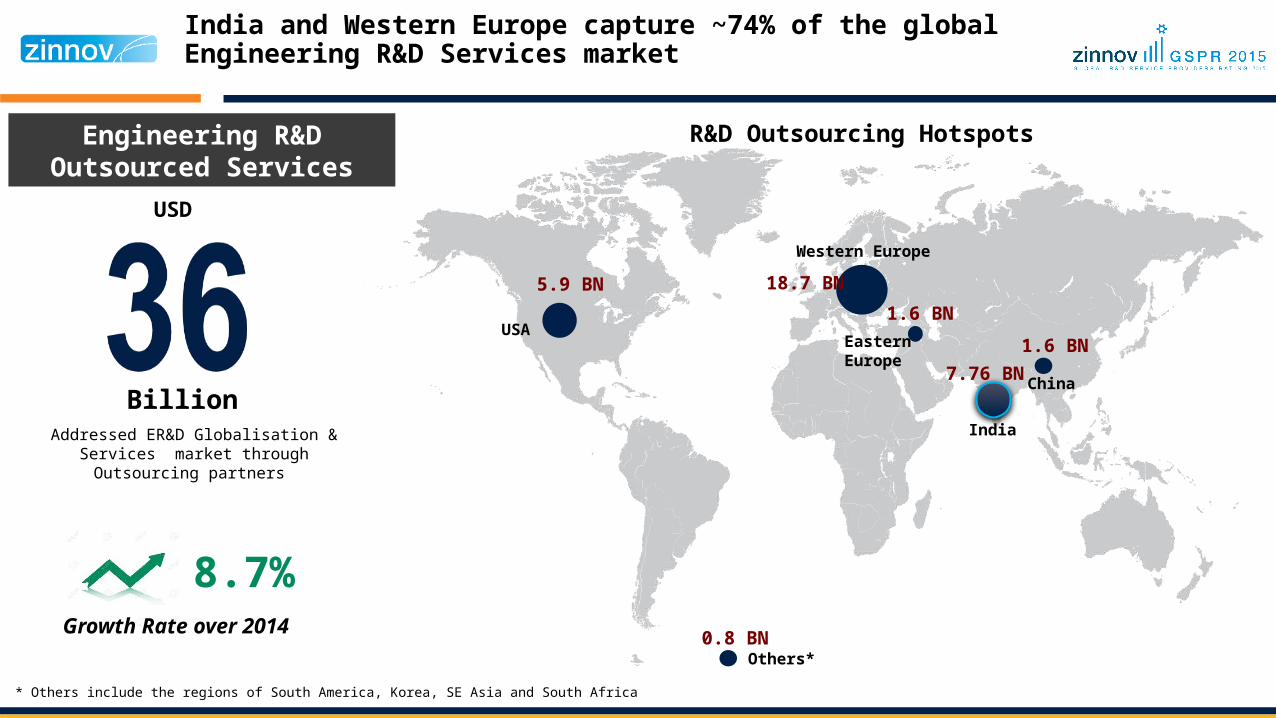

India and Western Europe capture ~74% of the global Engineering R&D Services market

7.76 BN

1.6 BN

18.7 BN1.6 BN

5.9 BN

China

India

Eastern Europe

Western Europe

USA

R&D Outsourcing HotspotsEngineering R&D Outsourced Services

Addressed ER&D Globalisation & Services market through Outsourcing

partners

Billion

USD

8.7%0.8 BN

Others*

* Others include the regions of South America, Korea, SE Asia and South Africa

Growth Rate over 2014

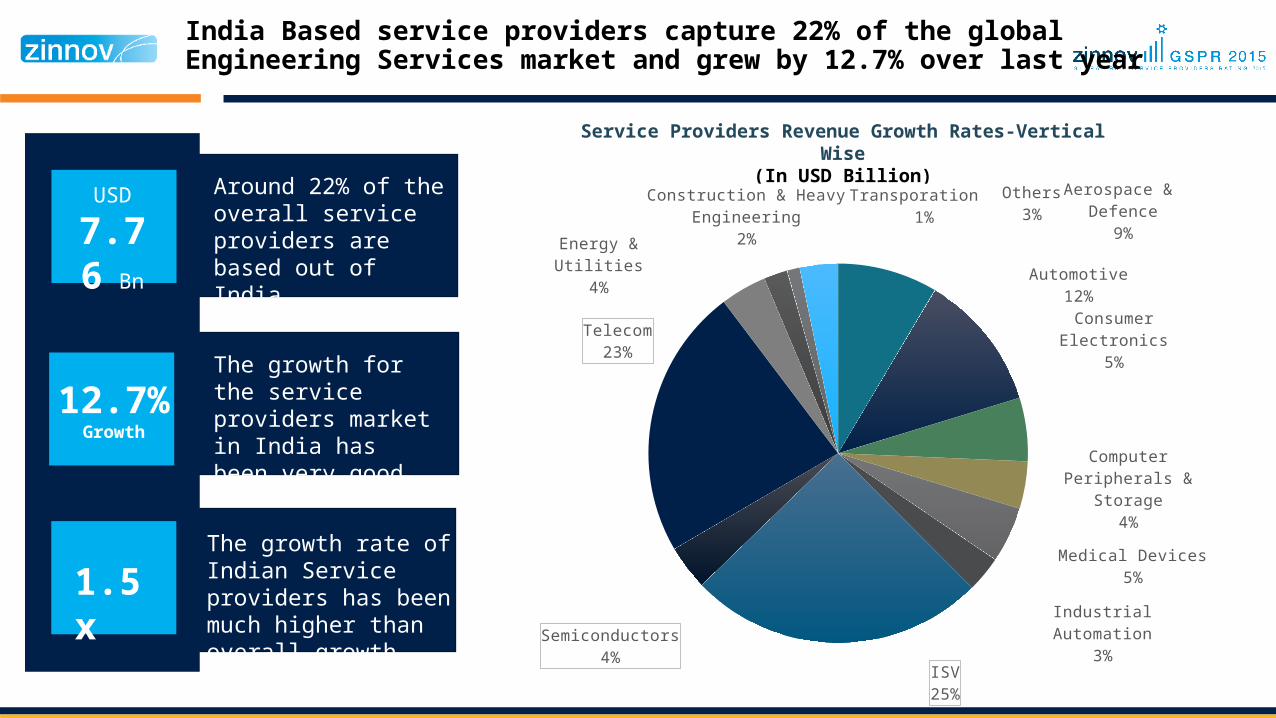

India Based service providers capture 22% of the global Engineering Services market and grew by 12.7% over last year

Service Providers Revenue Growth Rates-Vertical Wise

(In USD Billion)Aerospace &

Defence9%

Automotive12%Consumer Elec-

tronics5%

Computer Pe-ripherals & Stor-

age4%

Medical Devices5%

Industrial Automa-tion3%

ISV25%

Semiconductors4%

Telecom23%

Energy & Utilities4%

Construction & Heavy En-gineering

2%

Transporation 1%

Others3%

Around 22% of the overall service providers are based out of India

The growth rate of Indian Service providers has been much higher than overall growth

The growth for the service providers market in India has been very good

USD7.76 Bn

12.7%

Growth

1.5x

FY 2014 FY 2015 FY 2020

$6.887 Bn $7.76 Bn

$14.9 Bn$11.312 Bn

$12.25 Bn

$22.9 Bn

Service Providers

In-houseR&D CentersService

Providers

In-houseR&D Centers

Service Providers

In-houseR&D Centers

Product Engineering Services Growth Rate ( In USD Billions)

FY 2014 FY 2015 FY 2020(E)

9.89%

13.7%

Growth rateGrowth rate(Expected)USD

18.2Billion

USD

20Billion

USD

38Billion

India’s ER&D globalization and services market is expected to reach $38 Billion by 2020

8.3%

12.67% 13.97%

13.3%

Global Engineering R&D LandscapeEngineering Services is getting re-

defined

Key Trends in Global Engineering & RD Services

GSPR – 2015 Rating

FIVEKey trends in Global Engineering R&D Services

The drivers for outsourcing have changed tremendously over the last year and some newer trends have emerged

4

123

Service Providers are building end-to-end and cross horizontal capabilities through acquisitions of niche engineering services firms

Germany based R&D spenders, particularly Automotive companies, are increasingly exploring offshoring /near shoring to service providers in low cost locations

Europe based service providers are aggressively looking at scaling up or setting offshore operations in India to access India’s cost effective large talent pool

India based Engineering R&D Service providers are building newer capabilities in support engineering functions such as supply chain, regulatory compliances and manufacturing engineering

Internet of things or Connected Products is becoming a critical investment area for global R&D spenders. 5

Global Engineering R&D LandscapeEngineering Services is getting re-

defined

Key Trends in Global Engineering & RD Services

GSPR – 2015 Rating

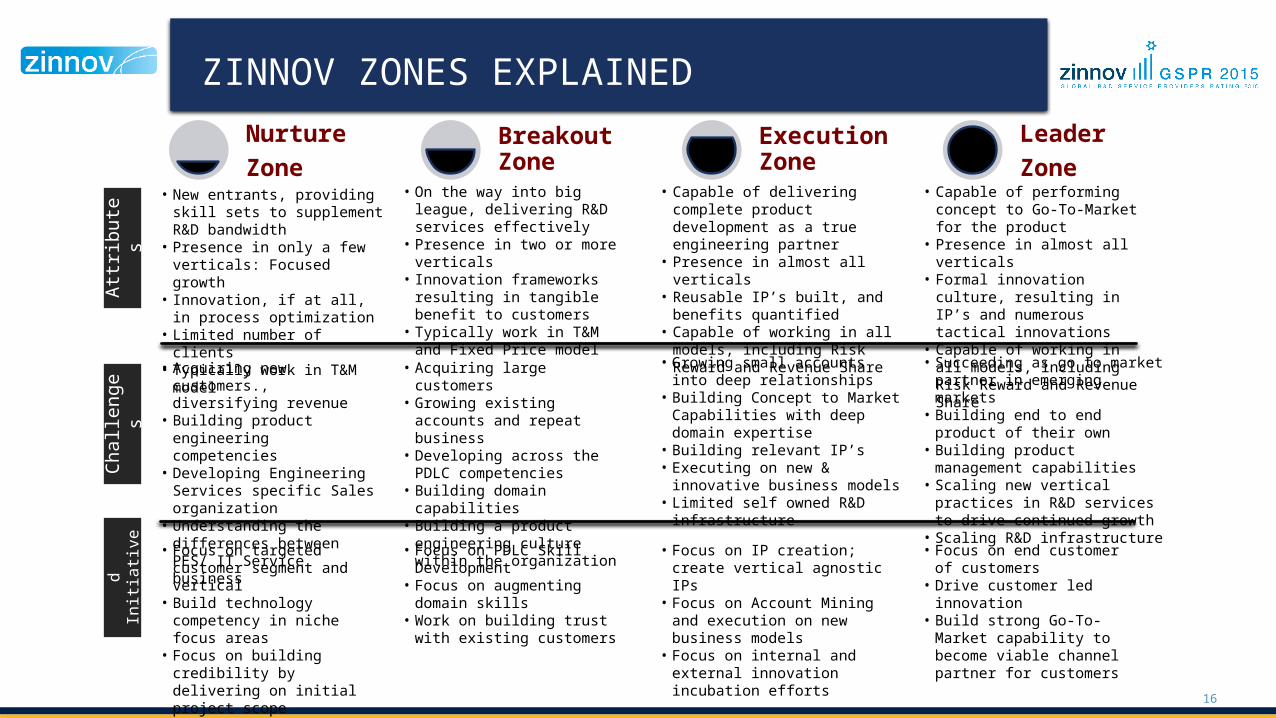

ZINNOV ZONES EXPLAINED

16

Nurture Zone

Breakout Zone

Execution Zone

Leader Zone

Attri

bute

sCh

alle

nges

Reco

mm

end

ed In

itiat

ives

• Acquiring new customers., diversifying revenue

• Building product engineering competencies

• Developing Engineering Services specific Sales organization

• Understanding the differences between PES/ IT Service business

• Focus on targeted customer segment and vertical

• Build technology competency in niche focus areas

• Focus on building credibility by delivering on initial project scope

• New entrants, providing skill sets to supplement R&D bandwidth

• Presence in only a few verticals: Focused growth

• Innovation, if at all, in process optimization

• Limited number of clients• Typically work in T&M model

• Acquiring large customers• Growing existing accounts and

repeat business• Developing across the PDLC

competencies• Building domain capabilities• Building a product engineering

culture within the organization

• Focus on PDLC Skill Development• Focus on augmenting domain

skills• Work on building trust with

existing customers

• On the way into big league, delivering R&D services effectively

• Presence in two or more verticals• Innovation frameworks resulting in

tangible benefit to customers• Typically work in T&M and Fixed

Price model

• Growing small accounts into deep relationships

• Building Concept to Market Capabilities with deep domain expertise

• Building relevant IP’s• Executing on new & innovative

business models• Limited self owned R&D infrastructure

• Focus on IP creation; create vertical agnostic IPs

• Focus on Account Mining and execution on new business models

• Focus on internal and external innovation incubation efforts

• Capable of delivering complete product development as a true engineering partner

• Presence in almost all verticals• Reusable IP’s built, and benefits

quantified• Capable of working in all models,

including Risk Reward and Revenue Share

• Succeeding as go to market partner in emerging markets

• Building end to end product of their own

• Building product management capabilities

• Scaling new vertical practices in R&D services to drive continued growth

• Scaling R&D infrastructure

• Focus on end customer of customers

• Drive customer led innovation• Build strong Go-To-Market

capability to become viable channel partner for customers

• Capable of performing concept to Go-To-Market for the product

• Presence in almost all verticals• Formal innovation culture, resulting

in IP’s and numerous tactical innovations

• Capable of working in all models, including Risk Reward and Revenue Share

17

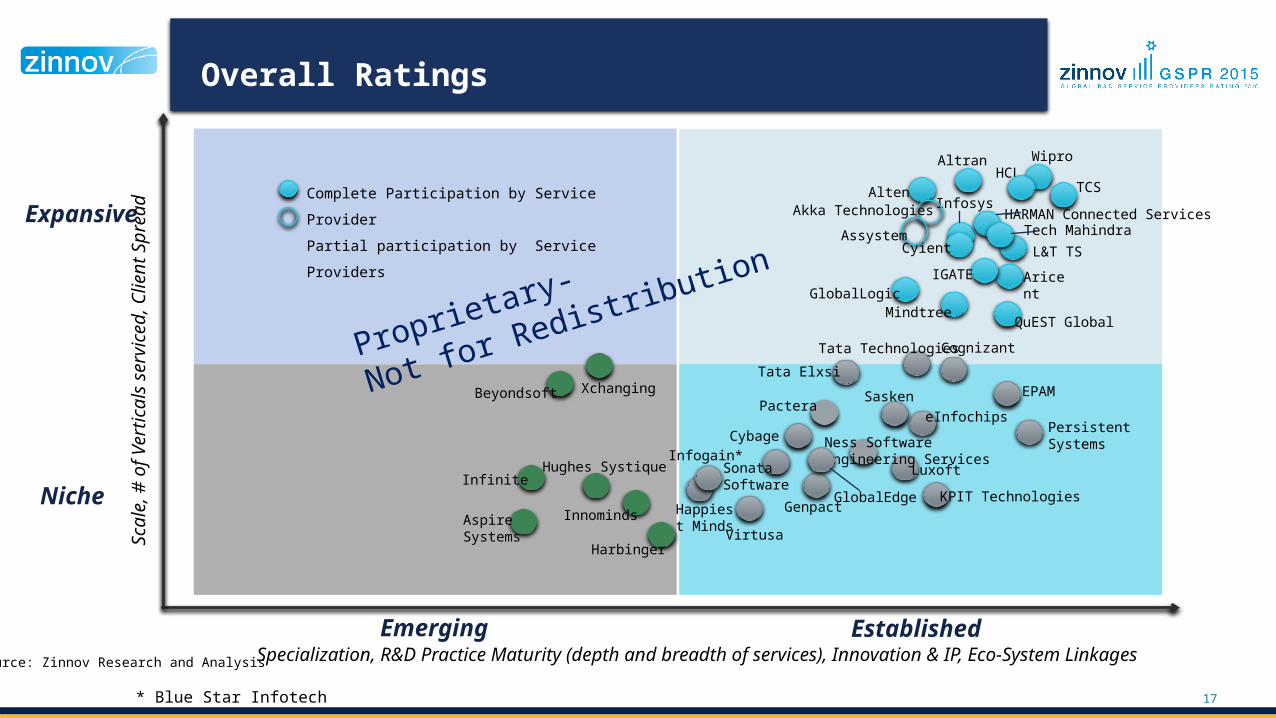

Overall Ratings

Source: Zinnov Research and Analysis

17

Niche

Expansive

Specialization, R&D Practice Maturity (depth and breadth of services), Innovation & IP, Eco-System Linkages

Scal

e, #

of V

ertic

als

serv

iced

, Clie

nt S

prea

d

Tech Mahindra

HCLWipro

Cyient

Infosys

L&T TS

Persistent Systems

TCS

KPIT Technologies

Tata Technologies

Altran

Alten

EPAM

Luxoft

Aricent

Genpact

QuEST Global

IGATE

Tata Elxsi

HARMAN Connected Services

Mindtree

Beyondsoft

Emerging Established

Harbinger

Innominds`

Xchanging

Happiest Minds

InfiniteInfogain*Hughes Systique

Pactera

Ness Software Engineering Services

VirtusaAspireSystems

GlobalLogic

eInfochipsCybage

SonataSoftware

Cognizant

AssystemAkka Technologies

Sasken

GlobalEdge

* Blue Star Infotech

Complete Participation by Service Provider Partial participation by Service Providers

Proprietary-

Not for Redistribution

Mechanical Engineering Services Rating

18Source: Zinnov Research and Analysis

Emerging Established

Niche

Expansive

Specialization, R&D Practice Maturity (depth and breadth of services), Innovation & IP, Eco-System Linkages

Scal

e, #

of V

ertic

als

serv

iced

, Clie

nt S

prea

d

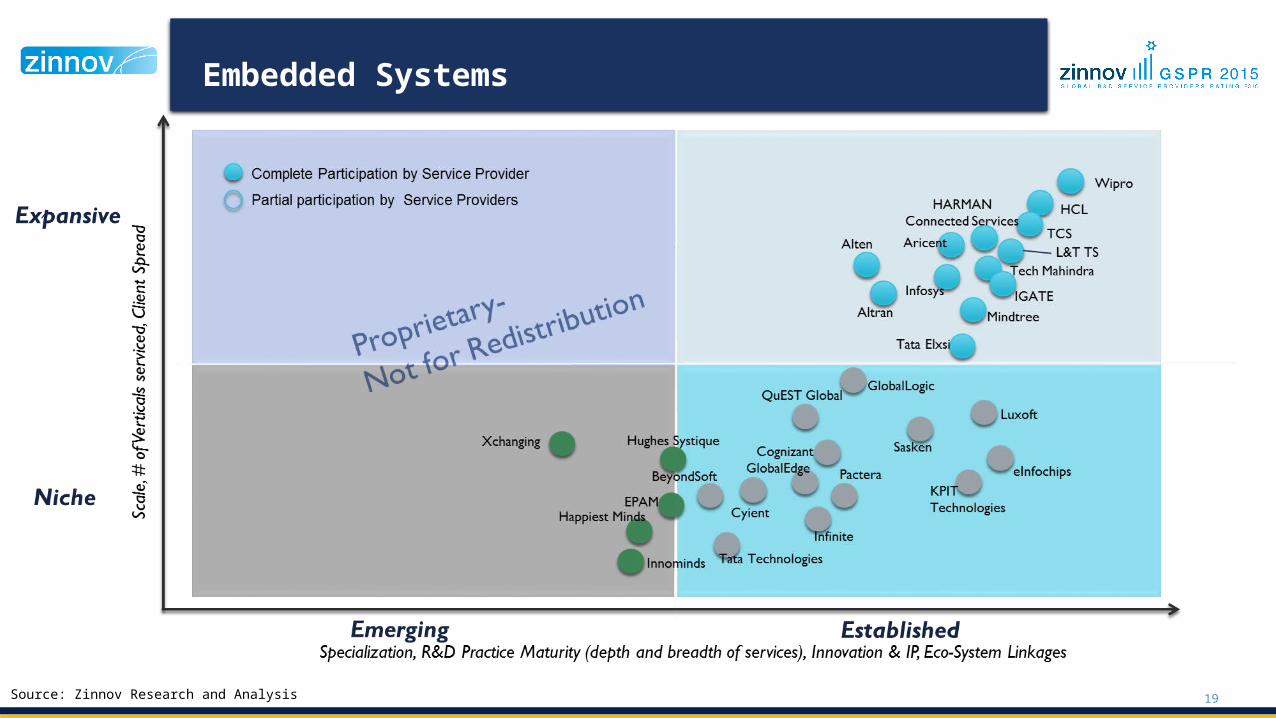

Cyient

Source: Zinnov Research and Analysis

KPIT Technologies

HCLTCS

L&T TS

Tech MahindraQuEST Global

Wipro

IGATE

HARMAN Connected Services

Tata Elxsi

Infosys

AltranAlten

Beyondsoft

AssystemAkka

Genpact

Complete Participation by Service Provider Partial participation by Service Providers

Tata Technologies

Proprietary-

Not for Redistribution

Embedded Systems

19Source: Zinnov Research and Analysis

OUTSOURCED SOFTWARE PRODUCT DEVELOPMENT – ENTERPRISE SOFTWARE - 2015

20

Zinnov Zones – Leading Service Providers

Source: Zinnov Research and Analysis

Nurture Zone Breakout Zone Execution Zone Leadership Zone

Beyondsoft

Tech Mahindra

Xchanging

TCSPersistentSystems

IGATE AspireSystem

s

Aricent

Mindtree EPAM

Pactera

• Capable of performing concept to Go-To-Market for the product

• Formal innovation culture, resulting in IP’s and strategic innovations

• Worlds Largest ISVs

• Capable of delivering complete product development as a true engineering partner

• Reusable components IP’s built, and benefits quantified

• Large ISVs and Niche ISVs

• On the way into big league

• Innovation frameworks resulting in tangible benefit to customers

• Niche ISVs

• R&D and PES as a focus area

• Innovation, if at all, in process optimization

• Generic ISVs, Startups

Sasken

SonataSoftware

GlobalLogic

Cybage

Harbinger

HARMAN Connected Services

Low

High

Scalability

R&D Practice Maturity

Scal

e, #

of S

ub-V

ertic

als

serv

iced

, Clie

nt S

prea

d

Innovation

Customer Type

Infogain*

Innominds

Infosys

Cognizant

NessSoftware

Engineering Services

Virtusa

Happiest Minds

HCL

Wipro

* Blue Star Infotech

Proprietary-

Not for Redistribution

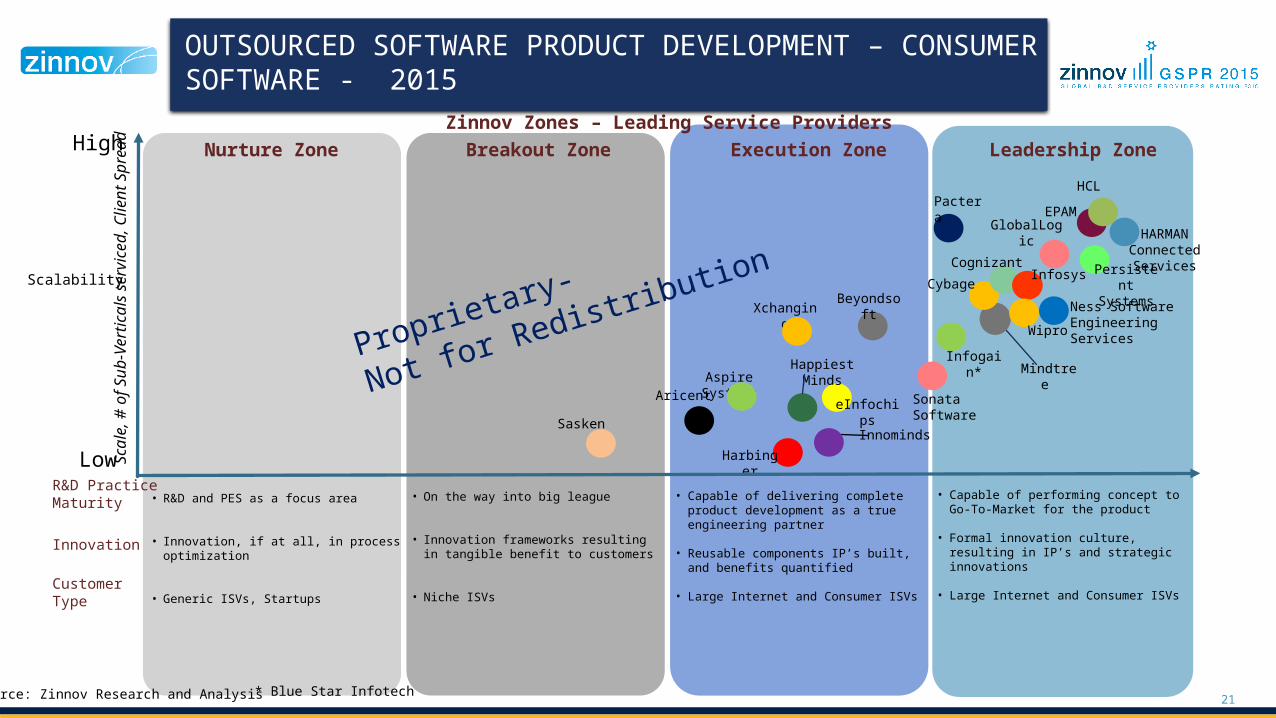

OUTSOURCED SOFTWARE PRODUCT DEVELOPMENT – CONSUMER SOFTWARE - 2015

21

Nurture Zone Breakout Zone Execution Zone Leadership Zone

Mindtree

EPAM

PersistentSystems

Pactera

Aspire Systems

Infogain*

Sonata Software

HARMAN Connected Services

HCL

• Capable of performing concept to Go-To-Market for the product

• Formal innovation culture, resulting in IP’s and strategic innovations

• Large Internet and Consumer ISVs

• Capable of delivering complete product development as a true engineering partner

• Reusable components IP’s built, and benefits quantified

• Large Internet and Consumer ISVs

• On the way into big league

• Innovation frameworks resulting in tangible benefit to customers

• Niche ISVs

• R&D and PES as a focus area

• Innovation, if at all, in process optimization

• Generic ISVs, Startups

GlobalLogic

Beyondsoft

Cybage

Harbinger

Xchanging

eInfochips

Aricent

Low

High

R&D Practice Maturity

Zinnov Zones – Leading Service Providers

Innovation

Customer Type

Scal

e, #

of S

ub-V

ertic

als

serv

iced

, Clie

nt S

prea

d

Happiest Minds

Sasken Innominds

Infosys

Ness Software Engineering Services

Cognizant

Wipro

* Blue Star InfotechSource: Zinnov Research and Analysis

Scalability

Proprietary-

Not for Redistribution

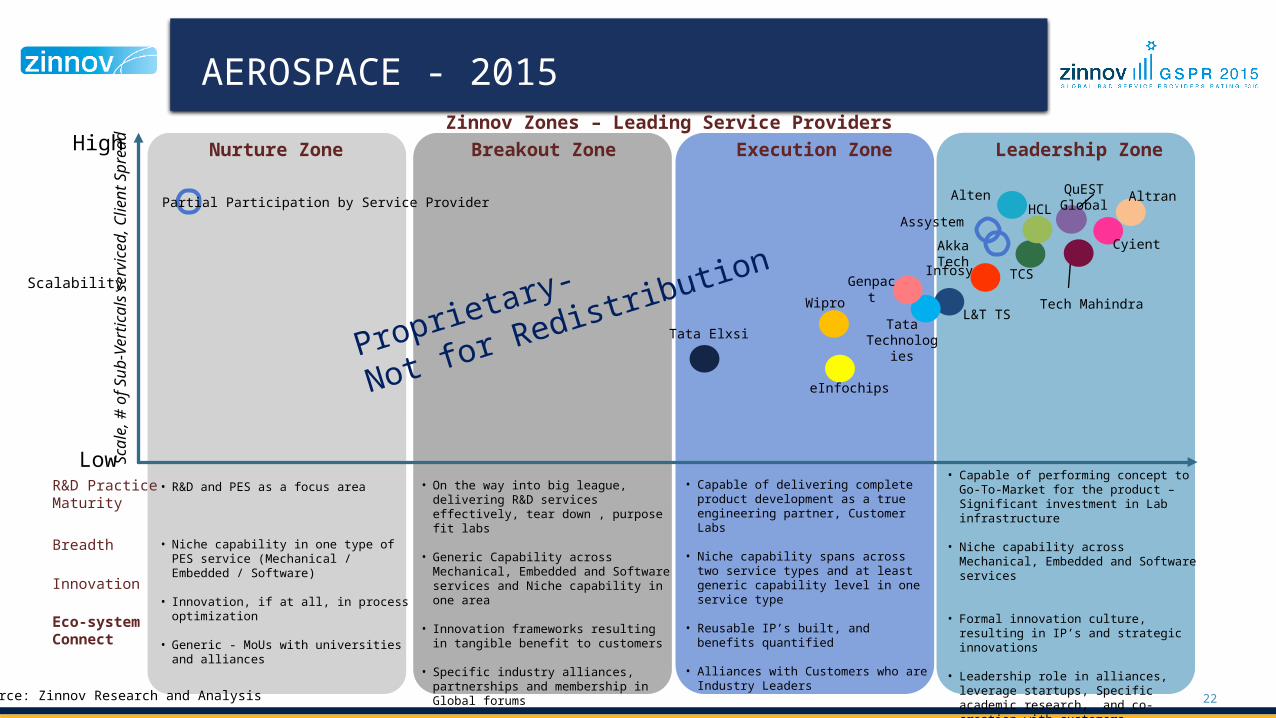

AEROSPACE - 2015

22

Nurture Zone Breakout Zone Execution Zone Leadership Zone

Tech MahindraWipro

TCS

Tata Elxsi

• Capable of performing concept to Go-To-Market for the product –Significant investment in Lab infrastructure

• Niche capability across Mechanical, Embedded and Software services

• Formal innovation culture, resulting in IP’s and strategic innovations

• Leadership role in alliances, leverage startups, Specific academic research, and co-creation with customers

• Capable of delivering complete product development as a true engineering partner, Customer Labs

• Niche capability spans across two service types and at least generic capability level in one service type

• Reusable IP’s built, and benefits quantified

• Alliances with Customers who are Industry Leaders

• On the way into big league, delivering R&D services effectively, tear down , purpose fit labs

• Generic Capability across Mechanical, Embedded and Software services and Niche capability in one area

• Innovation frameworks resulting in tangible benefit to customers

• Specific industry alliances, partnerships and membership in Global forums

• R&D and PES as a focus area

• Niche capability in one type of PES service (Mechanical / Embedded / Software)

• Innovation, if at all, in process optimization

• Generic - MoUs with universities and alliances

HCL

eInfochips

L&T TS

Cyient

Low

High

Scalability

R&D Practice Maturity

Zinnov Zones – Leading Service Providers

Breadth

Innovation

Eco-system Connect

Scal

e, #

of S

ub-V

ertic

als

serv

iced

, Clie

nt S

prea

d

Source: Zinnov Research and Analysis

Tata Technologie

s

InfosysGenpact

Altran QuEST GlobalAlten

AssystemAkka Tech

Proprietary-

Not for Redistribution

Partial Participation by Service Provider

23

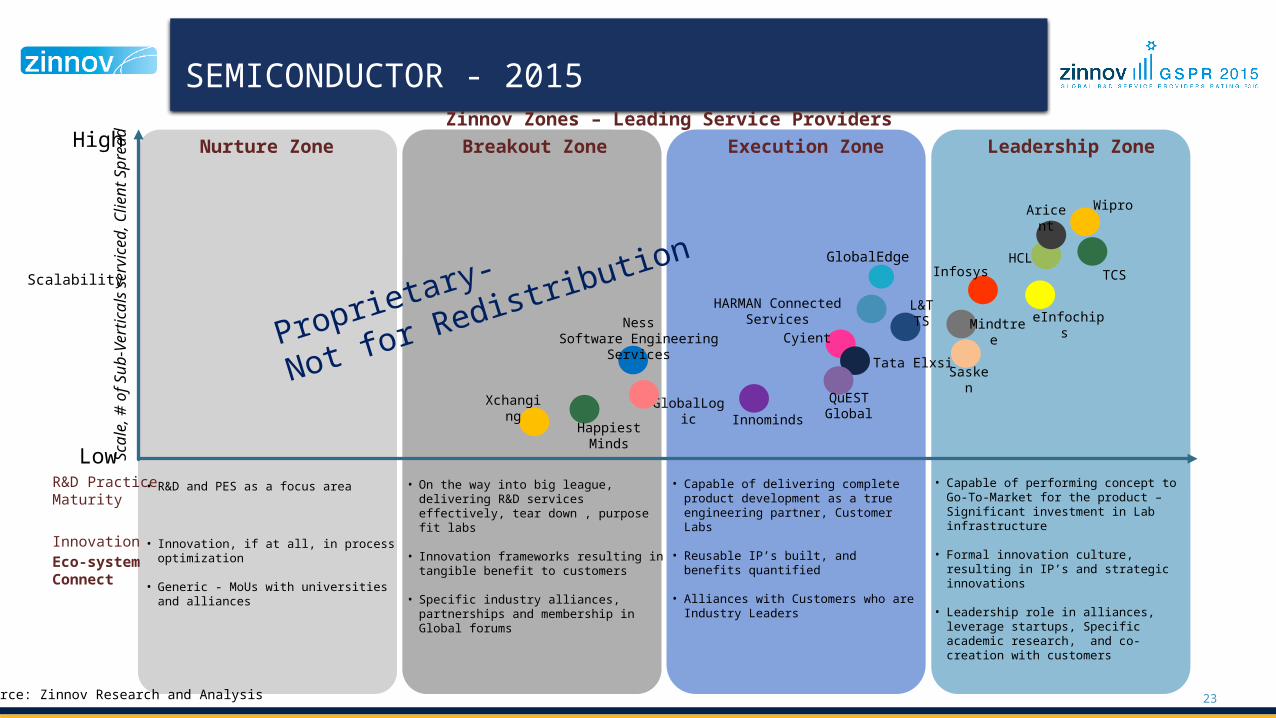

SEMICONDUCTOR - 2015Nurture Zone Breakout Zone Execution Zone Leadership Zone

HCLTCS

Sasken

Mindtree

Tata ElxsiCyient

• Capable of performing concept to Go-To-Market for the product –Significant investment in Lab infrastructure

• Formal innovation culture, resulting in IP’s and strategic innovations

• Leadership role in alliances, leverage startups, Specific academic research, and co-creation with customers

• Capable of delivering complete product development as a true engineering partner, Customer Labs

• Reusable IP’s built, and benefits quantified

• Alliances with Customers who are Industry Leaders

• On the way into big league, delivering R&D services effectively, tear down , purpose fit labs

• Innovation frameworks resulting in tangible benefit to customers

• Specific industry alliances, partnerships and membership in Global forums

• R&D and PES as a focus area

• Innovation, if at all, in process optimization

• Generic - MoUs with universities and alliances

L&T TS

Wipro

eInfochips

GlobalLogic

HARMAN Connected Services

Aricent

QuEST Global

Happiest Minds

Low

High

Scalability

R&D Practice Maturity

Zinnov Zones – Leading Service Providers

InnovationEco-system Connect

Scal

e, #

of S

ub-V

ertic

als

serv

iced

, Clie

nt S

prea

d

Source: Zinnov Research and Analysis

Xchanging Innominds

Infosys

NessSoftware Engineering

Services

GlobalEdge

Proprietary-

Not for Redistribution

24

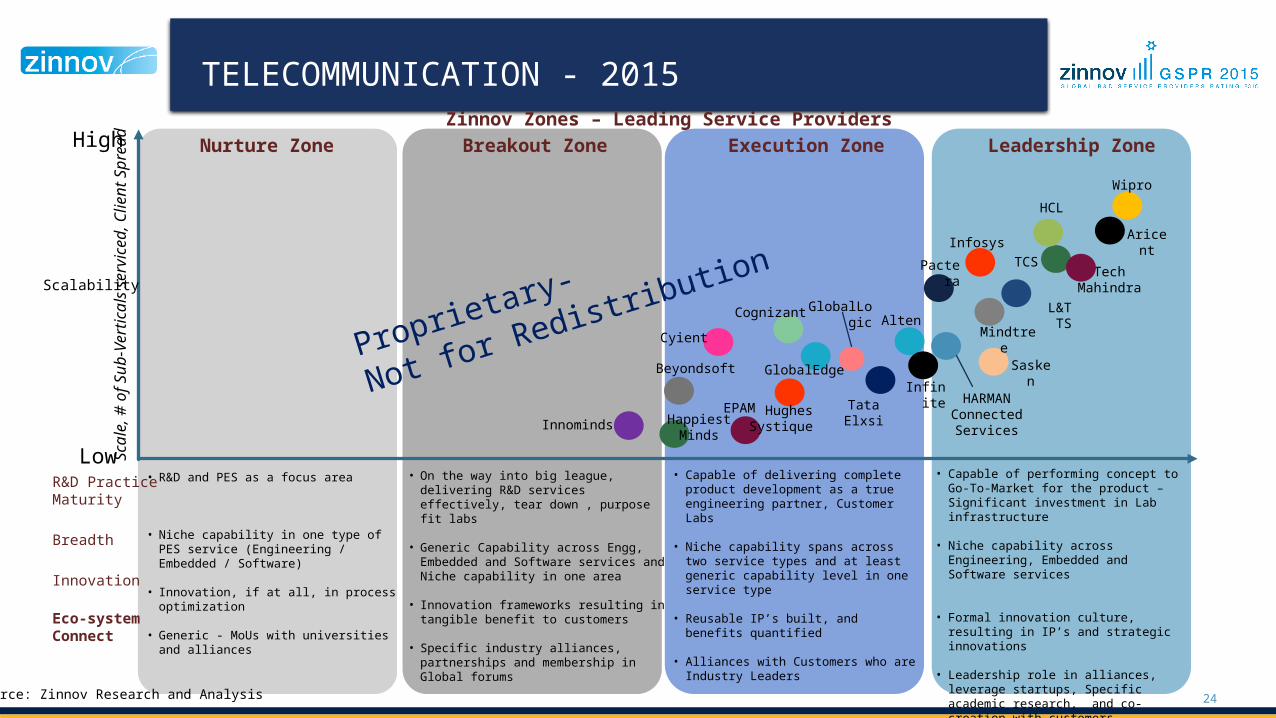

TELECOMMUNICATION - 2015Nurture Zone Breakout Zone Execution Zone Leadership Zone

Aricent

Wipro

TCS

Mindtree

Sasken

GlobalLogic

• Capable of delivering complete product development as a true engineering partner, Customer Labs

• Niche capability spans across two service types and at least generic capability level in one service type

• Reusable IP’s built, and benefits quantified

• Alliances with Customers who are Industry Leaders

• On the way into big league, delivering R&D services effectively, tear down , purpose fit labs

• Generic Capability across Engg, Embedded and Software services and Niche capability in one area

• Innovation frameworks resulting in tangible benefit to customers

• Specific industry alliances, partnerships and membership in Global forums

• R&D and PES as a focus area

• Niche capability in one type of PES service (Engineering / Embedded / Software)

• Innovation, if at all, in process optimization

• Generic - MoUs with universities and alliances

Beyondsoft

L&T TS

• Capable of performing concept to Go-To-Market for the product –Significant investment in Lab infrastructure

• Niche capability across Engineering, Embedded and Software services

• Formal innovation culture, resulting in IP’s and strategic innovations

• Leadership role in alliances, leverage startups, Specific academic research, and co-creation with customers

Tech Mahindra

Tata Elxsi

HCL

Pactera

HARMAN Connected Services

Infinite

Cyient

Happiest Minds

Low

High

Scalability

R&D Practice Maturity

Zinnov Zones – Leading Service Providers

Breadth

Innovation

Eco-system Connect

Scal

e, #

of S

ub-V

ertic

als

serv

iced

, Clie

nt S

prea

d

Source: Zinnov Research and Analysis

Hughes Systique

EPAM

Infosys

Cognizant

Innominds

Alten

GlobalEdgeProprietary-

Not for Redistribution

25

CONSUMER ELECTRONICS - 2015Nurture Zone Breakout Zone Execution Zone Leadership Zone

HCL

Xchanging

Sasken

Wipro

L&T TS

Tata Elxsi

IGATE Mindtree Infosys

• Capable of performing concept to Go-To-Market for the product –Significant investment in Lab infrastructure

• Niche capability across Engineering, Embedded and Software services

• Formal innovation culture, resulting in IP’s and strategic innovations

• Leadership role in alliances, leverage startups, Specific academic research, and co-creation with customers

• Capable of delivering complete product development as a true engineering partner, Customer Labs

• Niche capability spans across two service types and at least generic capability level in one service type

• Reusable IP’s built, and benefits quantified

• Alliances with Customers who are Industry Leaders

• On the way into big league, delivering R&D services effectively, tear down , purpose fit labs

• Generic Capability across Engg, Embedded and Software services and Niche capability in one area

• Innovation frameworks resulting in tangible benefit to customers

• Specific industry alliances, partnerships and membership in Global forums

• R&D and PES as a focus area

• Niche capability in one type of PES service (Engineering / Embedded / Software)

• Innovation, if at all, in process optimization

• Generic - MoUs with universities and alliances

TCSBeyondSoft

Tech Mahindra

GlobalLogic

HARMAN Connected Services

Aricent

NessSoftware Engineering Services

Hughes Systique

Cyient

Happiest MindsLow

High

Scalability

R&D Practice Maturity

Zinnov Zones – Leading Service Providers

Breadth

Innovation

Eco-system Connect

Scal

e, #

of S

ub-V

ertic

als

serv

iced

, Clie

nt S

prea

d

Cognizant

EPAM

Source: Zinnov Research and Analysis

Proprietary-

Not for Redistribution

26

AUTOMOTIVE - 2015

• On the way into big league, delivering R&D services effectively, tear down , purpose fit labs

• Generic Capability across Engg, Embedded and Software services and Niche capability in one area

• Innovation frameworks resulting in tangible benefit to customers

• Specific industry alliances, partnerships and membership in Global forums

• R&D and PES as a focus area

• Niche capability in one type of PES service (Engineering / Embedded / Software)

• Innovation, if at all, in process optimization

• Generic - MoUs with universities and alliances

Nurture Zone Breakout Zone Execution Zone Leadership Zone

Wipro

Tata Technologies

L&T TS

Luxoft

• Capable of performing concept to Go-To-Market for the product –Significant investment in Lab infrastructure

• Niche capability across Engineering, Embedded and Software services

• Formal innovation culture, resulting in IP’s and strategic innovations

• Leadership role in alliances, leverage startups, Specific academic research, and co-creation with customers

• Capable of delivering complete product development as a true engineering partner, Customer Labs

• Niche capability spans across two service types and at least generic capability level in one service type

• Reusable IP’s built, and benefits quantified

• Alliances with Customers who are Industry Leaders

TCSKPIT Technologies Tech

Mahindra

Mindtree

BeyondSoft

Tata Elxsi

Sasken

HCL

QuEST GlobalCyient

AricentXchanging

HARMAN Connected Services

IGATE

Happiest Minds

Low

High

Scalability

R&D Practice Maturity

Zinnov Zones – Leading Service Providers

Breadth

Innovation

Eco-system Connect

Scal

e, #

of S

ub-V

ertic

als

serv

iced

, Clie

nt S

prea

d

Source: Zinnov Research and Analysis

Infosys

Hughes Systique

Altran

Alten

Akka Technologies

Assystem

GlobalEdgeProprietary-

Not for RedistributionPartial Participation by Service Provider

27

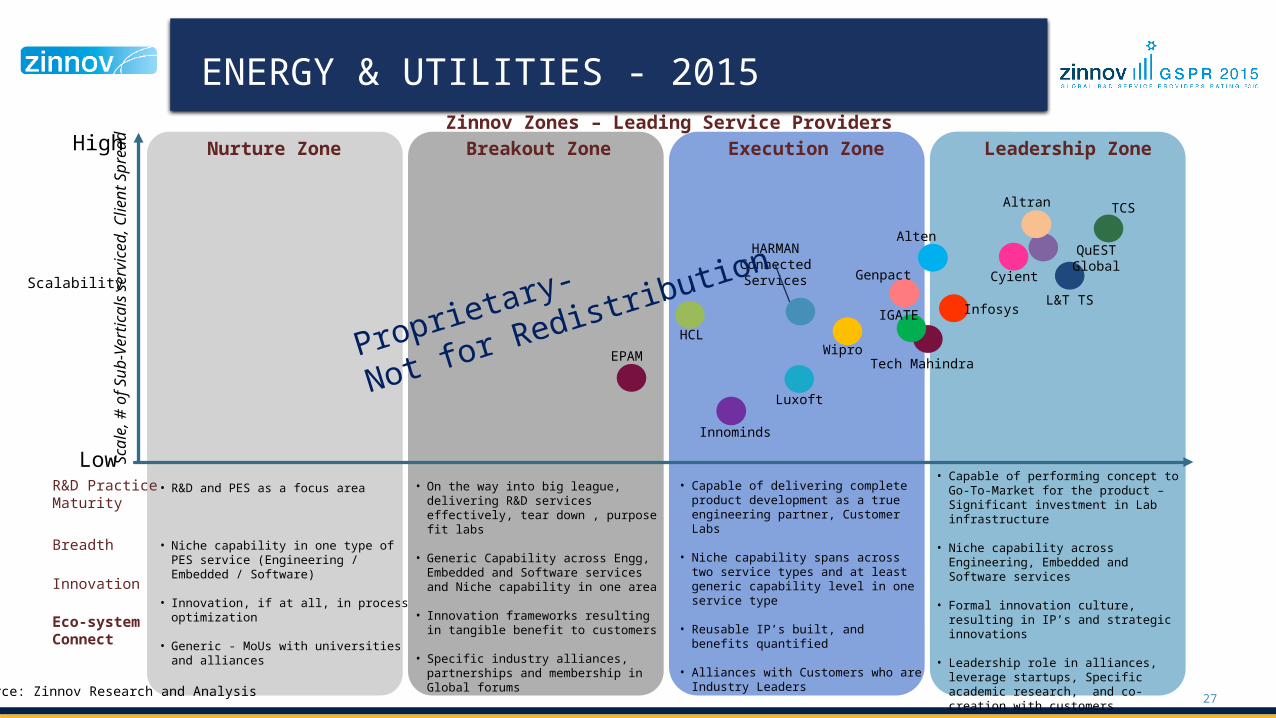

ENERGY & UTILITIES - 2015Nurture Zone Breakout Zone Execution Zone Leadership Zone

CyientL&T TS

• Capable of performing concept to Go-To-Market for the product –Significant investment in Lab infrastructure

• Niche capability across Engineering, Embedded and Software services

• Formal innovation culture, resulting in IP’s and strategic innovations

• Leadership role in alliances, leverage startups, Specific academic research, and co-creation with customers

• Capable of delivering complete product development as a true engineering partner, Customer Labs

• Niche capability spans across two service types and at least generic capability level in one service type

• Reusable IP’s built, and benefits quantified

• Alliances with Customers who are Industry Leaders

• On the way into big league, delivering R&D services effectively, tear down , purpose fit labs

• Generic Capability across Engg, Embedded and Software services and Niche capability in one area

• Innovation frameworks resulting in tangible benefit to customers

• Specific industry alliances, partnerships and membership in Global forums

• R&D and PES as a focus area

• Niche capability in one type of PES service (Engineering / Embedded / Software)

• Innovation, if at all, in process optimization

• Generic - MoUs with universities and alliances

Tech Mahindra

TCS

Luxoft

Wipro

Infosys

QuEST Global

IGATE

EPAM

Low

High

Scalability

R&D Practice Maturity

Zinnov Zones – Leading Service Providers

Breadth

Innovation

Eco-system Connect

Scal

e, #

of S

ub-V

ertic

als

serv

iced

, Clie

nt S

prea

d

Source: Zinnov Research and Analysis

HCL

HARMAN Connected Services Genpact

Innominds

Altran

Alten

Proprietary-

Not for Redistribution

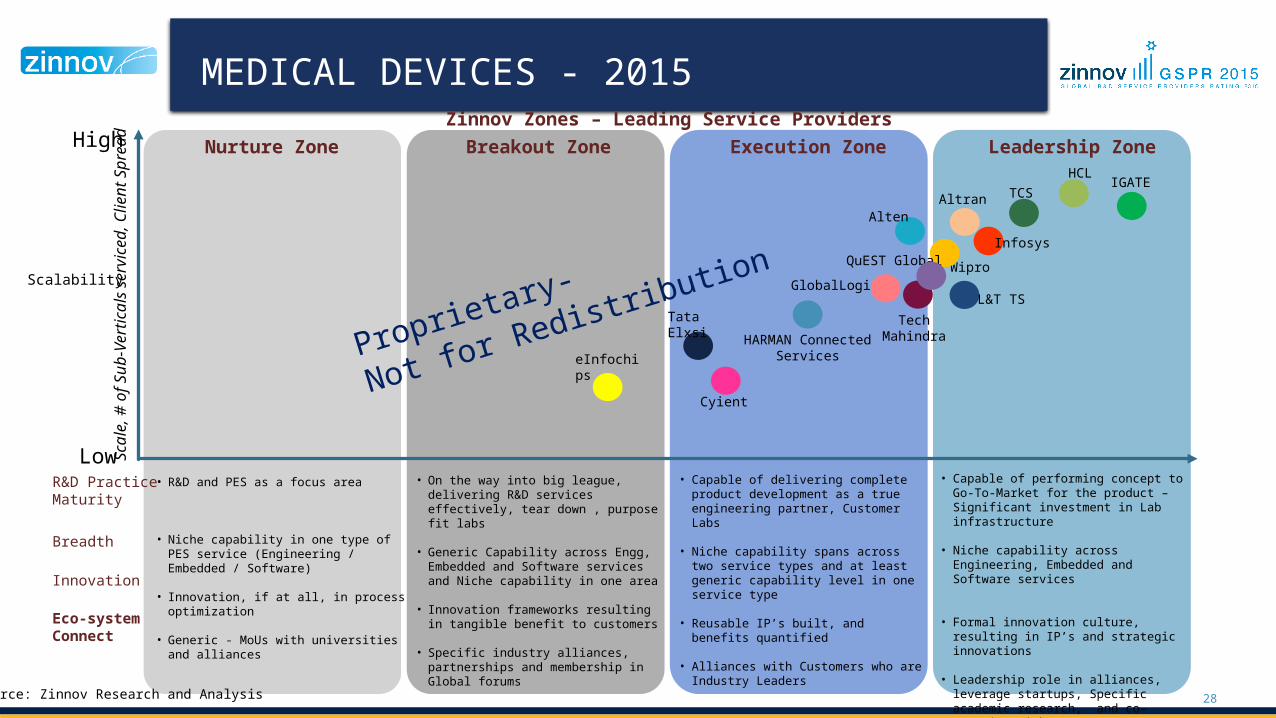

MEDICAL DEVICES - 2015

28

Nurture Zone Breakout Zone Execution Zone Leadership ZoneHCL

Wipro

L&T TS

HARMAN Connected Services

IGATE

GlobalLogic

Cyient

• Capable of performing concept to Go-To-Market for the product –Significant investment in Lab infrastructure

• Niche capability across Engineering, Embedded and Software services

• Formal innovation culture, resulting in IP’s and strategic innovations

• Leadership role in alliances, leverage startups, Specific academic research, and co-creation with customers

• Capable of delivering complete product development as a true engineering partner, Customer Labs

• Niche capability spans across two service types and at least generic capability level in one service type

• Reusable IP’s built, and benefits quantified

• Alliances with Customers who are Industry Leaders

• On the way into big league, delivering R&D services effectively, tear down , purpose fit labs

• Generic Capability across Engg, Embedded and Software services and Niche capability in one area

• Innovation frameworks resulting in tangible benefit to customers

• Specific industry alliances, partnerships and membership in Global forums

• R&D and PES as a focus area

• Niche capability in one type of PES service (Engineering / Embedded / Software)

• Innovation, if at all, in process optimization

• Generic - MoUs with universities and alliances

TCS

Tech Mahindra

QuEST Global

Tata Elxsi

eInfochips

Low

High

Scalability

R&D Practice Maturity

Zinnov Zones – Leading Service Providers

Breadth

Innovation

Eco-system Connect

Scal

e, #

of S

ub-V

ertic

als

serv

iced

, Clie

nt S

prea

d

Source: Zinnov Research and Analysis

Infosys

AltranAlten

Proprietary-

Not for Redistribution

29

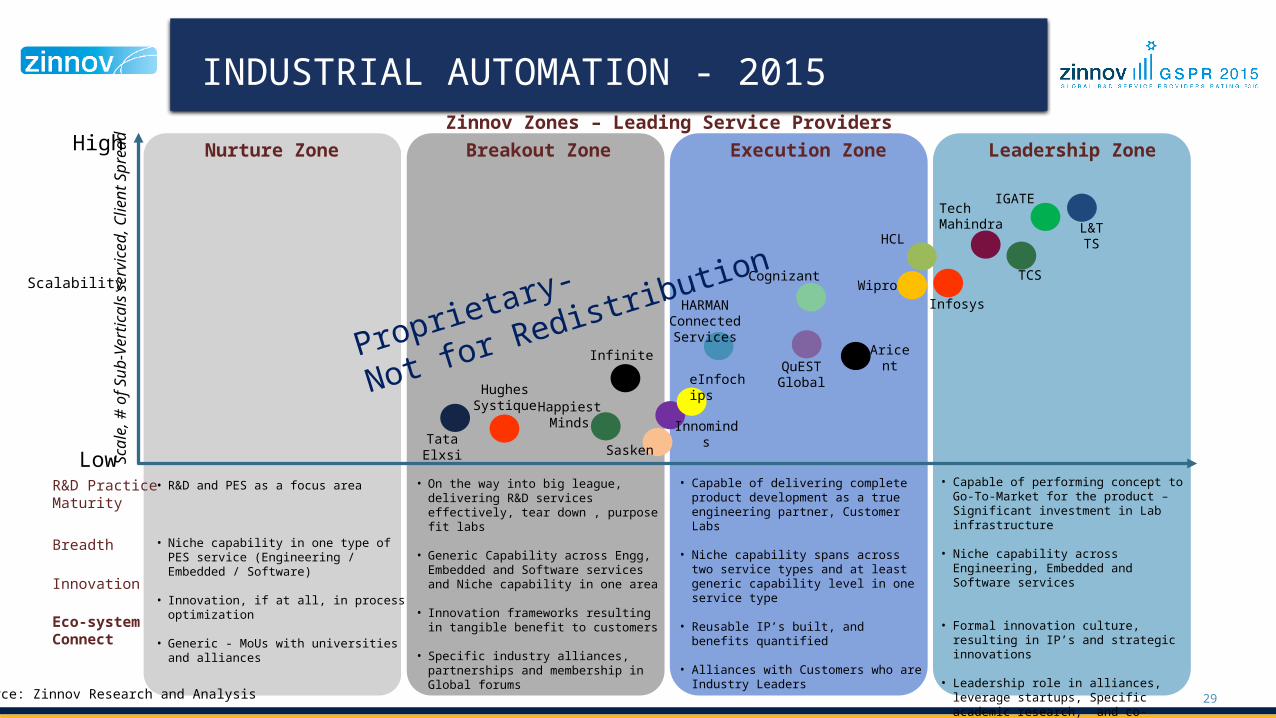

INDUSTRIAL AUTOMATION - 2015Nurture Zone Breakout Zone Execution Zone Leadership Zone

IGATE

Wipro

HCL L&T TS

• Capable of performing concept to Go-To-Market for the product –Significant investment in Lab infrastructure

• Niche capability across Engineering, Embedded and Software services

• Formal innovation culture, resulting in IP’s and strategic innovations

• Leadership role in alliances, leverage startups, Specific academic research, and co-creation with customers

• Capable of delivering complete product development as a true engineering partner, Customer Labs

• Niche capability spans across two service types and at least generic capability level in one service type

• Reusable IP’s built, and benefits quantified

• Alliances with Customers who are Industry Leaders

• On the way into big league, delivering R&D services effectively, tear down , purpose fit labs

• Generic Capability across Engg, Embedded and Software services and Niche capability in one area

• Innovation frameworks resulting in tangible benefit to customers

• Specific industry alliances, partnerships and membership in Global forums

• R&D and PES as a focus area

• Niche capability in one type of PES service (Engineering / Embedded / Software)

• Innovation, if at all, in process optimization

• Generic - MoUs with universities and alliances

Tech Mahindra

TCS

QuEST Global

Aricent

HARMAN Connected Services

Sasken

Infinite

Tata Elxsi

HappiestMinds

Low

High

Scalability

R&D Practice Maturity

Zinnov Zones – Leading Service Providers

Breadth

Innovation

Eco-system Connect

Scal

e, #

of S

ub-V

ertic

als

serv

iced

, Clie

nt S

prea

d

Source: Zinnov Research and Analysis

eInfochips

Innominds

Hughes Systique

InfosysCognizant

Proprietary-

Not for Redistribution

30

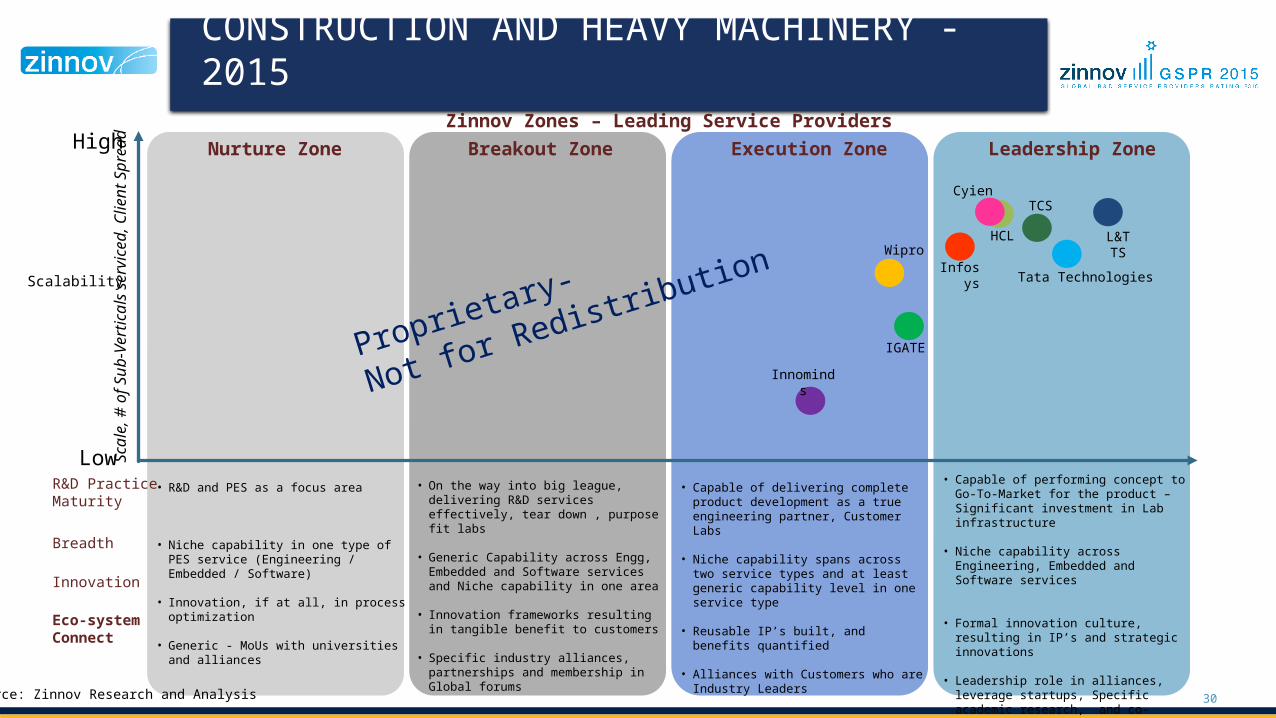

CONSTRUCTION AND HEAVY MACHINERY - 2015

Low

High

• Capable of performing concept to Go-To-Market for the product –Significant investment in Lab infrastructure

• Niche capability across Engineering, Embedded and Software services

• Formal innovation culture, resulting in IP’s and strategic innovations

• Leadership role in alliances, leverage startups, Specific academic research, and co-creation with customers

• On the way into big league, delivering R&D services effectively, tear down , purpose fit labs

• Generic Capability across Engg, Embedded and Software services and Niche capability in one area

• Innovation frameworks resulting in tangible benefit to customers

• Specific industry alliances, partnerships and membership in Global forums

Nurture Zone Breakout Zone Execution Zone Leadership Zone

TCSCyient

• Capable of delivering complete product development as a true engineering partner, Customer Labs

• Niche capability spans across two service types and at least generic capability level in one service type

• Reusable IP’s built, and benefits quantified

• Alliances with Customers who are Industry Leaders

• R&D and PES as a focus area

• Niche capability in one type of PES service (Engineering / Embedded / Software)

• Innovation, if at all, in process optimization

• Generic - MoUs with universities and alliances

L&T TS

Tata Technologies

HCLWipro

Scalability

R&D Practice Maturity

Zinnov Zones – Leading Service Providers

Breadth

Innovation

Eco-system Connect

Scal

e, #

of S

ub-V

ertic

als

serv

iced

, Clie

nt S

prea

d

Source: Zinnov Research and Analysis

IGATEInnomind

s

Infosys

Proprietary-

Not for Redistribution

31

COMPUTER PERIPHERALS AND STORAGE - 2015Nurture Zone Breakout Zone Execution Zone Leadership Zone

HCL

Wipro

Happiest Minds

IGATE

EPAM HARMAN Connected Services

• Capable of performing concept to Go-To-Market for the product –Significant investment in Lab infrastructure

• Niche capability across Engineering, Embedded and Software services

• Formal innovation culture, resulting in IP’s and strategic innovations

• Leadership role in alliances, leverage startups, Specific academic research, and co-creation with customers

• Capable of delivering complete product development as a true engineering partner, Customer Labs

• Niche capability spans across two service types and at least generic capability level in one service type

• Reusable IP’s built, and benefits quantified

• Alliances with Customers who are Industry Leaders

• On the way into big league, delivering R&D services effectively, tear down , purpose fit labs

• Generic Capability across Engg, Embedded and Software services and Niche capability in one area

• Innovation frameworks resulting in tangible benefit to customers

• Specific industry alliances, partnerships and membership in Global forums

• R&D and PES as a focus area

• Niche capability in one type of PES service (Engineering / Embedded / Software)

• Innovation, if at all, in process optimization

• Generic - MoUs with universities and alliances

TCS

Low

High

Scalability

R&D Practice Maturity

Zinnov Zones – Leading Service Providers

Breadth

Innovation

Eco-system Connect

Scal

e, #

of S

ub-V

ertic

als

serv

iced

, Clie

nt S

prea

d

Source: Zinnov Research and Analysis

Proprietary-

Not for Redistribution

32

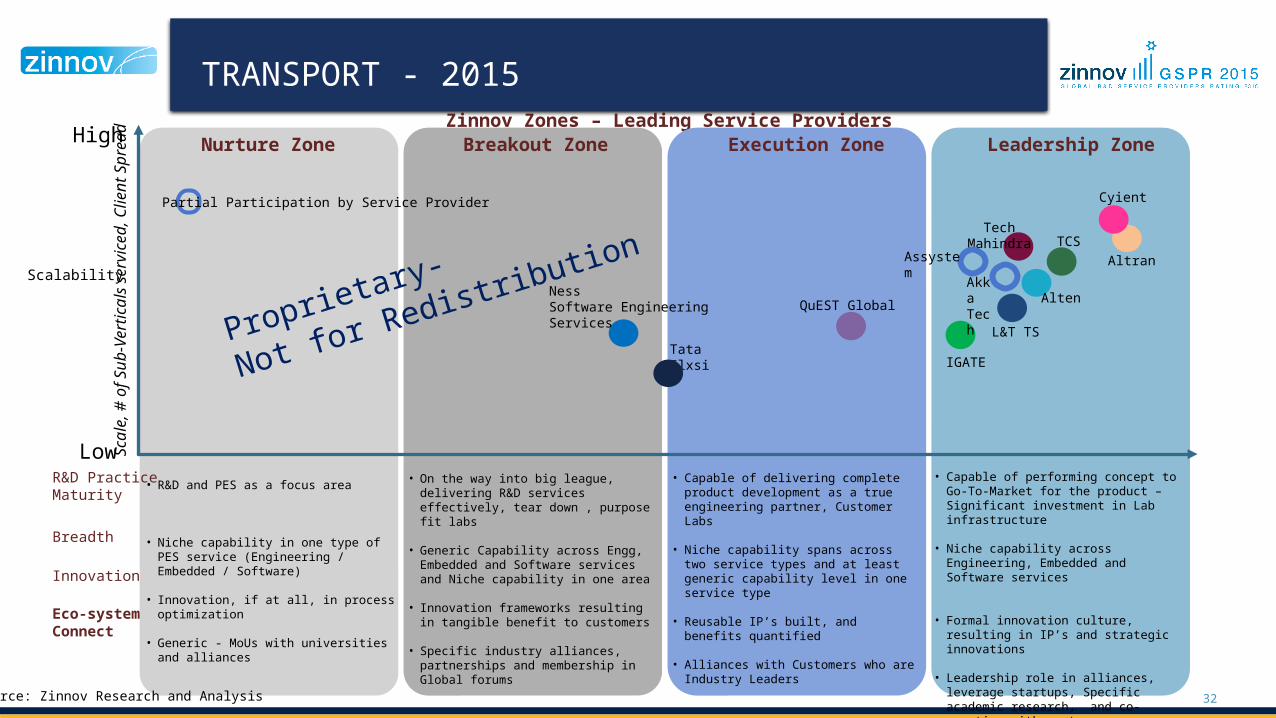

TRANSPORT - 2015Zinnov Zones – Leading Service Providers

Nurture Zone Breakout Zone Execution Zone Leadership Zone

Cyient

L&T TS

TCS

• Capable of performing concept to Go-To-Market for the product –Significant investment in Lab infrastructure

• Niche capability across Engineering, Embedded and Software services

• Formal innovation culture, resulting in IP’s and strategic innovations

• Leadership role in alliances, leverage startups, Specific academic research, and co-creation with customers

• Capable of delivering complete product development as a true engineering partner, Customer Labs

• Niche capability spans across two service types and at least generic capability level in one service type

• Reusable IP’s built, and benefits quantified

• Alliances with Customers who are Industry Leaders

• On the way into big league, delivering R&D services effectively, tear down , purpose fit labs

• Generic Capability across Engg, Embedded and Software services and Niche capability in one area

• Innovation frameworks resulting in tangible benefit to customers

• Specific industry alliances, partnerships and membership in Global forums

• R&D and PES as a focus area

• Niche capability in one type of PES service (Engineering / Embedded / Software)

• Innovation, if at all, in process optimization

• Generic - MoUs with universities and alliances

IGATE

Tech Mahindra

QuEST Global

Tata Elxsi

Low

High

Scalability

R&D Practice Maturity

Breadth

Innovation

Eco-system Connect

Scal

e, #

of S

ub-V

ertic

als

serv

iced

, Clie

nt S

prea

d

Source: Zinnov Research and Analysis

NessSoftware Engineering Services

Altran

AltenAkka Tech

Assystem

Proprietary-

Not for Redistribution

Partial Participation by Service Provider

DISCLAIMER

33

In the context of our Global Service Provider Ratings for Product Engineering Services, we reached out to a limited set of service providers that could be potential leaders in this space. Our set of inclusion criteria enables us to shortlist, effectively based on which service providers are invited to participate. While we normally see significant interest in participation, sometimes a service provider may request to be excluded from the GSPR activity if the timing of the research or circumstances within the service provider organization makes participation difficult. If a service provider declines to participate at the beginning of a GSPR process, it is important to know the following policies: Some non-participating service providers are still included in our evaluation

o As we invite only leading service providers and emerging players to participate in the GSPR, if a service provider decides not to participate, we have still included them in the final report if we think it is necessary

o Our reasoning is that a GSPR without a leading service provider would project an Partial picture of the market and make it less pertinent for our clients

The GSPR report clearly differentiates service providers that did not undergo the same rigorous

evaluation as its peerso While our analysts have evaluated the service providers that declined to participate, the service providers place in the

GSPR rating is denoted by a differentiating symbol indicating non-participation in the research processo Their assessment is based on different inputs than those used for evaluating its peers

We have reached out to the non-participating vendors to schedule a detailed briefing

o In an effort to ensure accuracy while circumventing the rigorous evaluation, we have tried to gain as much information from non-participating vendors on a briefing call as possible

o If we could not arrange such briefings, we have conducted our research through secondary means

34

Bangalore 69 "Prathiba Complex", 4th 'A' Cross, Koramangala 5th Block,Bangalore-560 095. Phone: +91-80-41127925/6

Gurgaon Office:First Floor,Plot no. 131, Sector 44, Gurgaon-122002,Phone: +91 124 4420100

SingaporeLevel 42, Suntec Tower Three8 Temasek BoulevardSingapore 038988Phone:+65 6829 2123

California Office3080 Olcott Street Suite A125, Santa Clara, CA 95054 Phone: +408-716-8432

Texas21, Waterway AveSuite 300 The WoodlandsTX-77380 USAPhone:+1-281-362-2773

BeijingMeilifang Tower 4, Entrance 4, 10/F #1003,11 Beiyuan Shuangying Road,Chaoyang District, BeijingChina 100012

Thank You